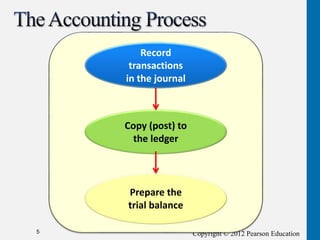

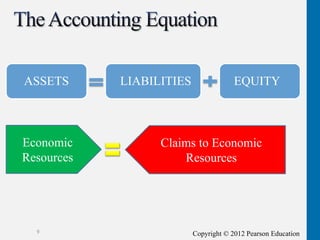

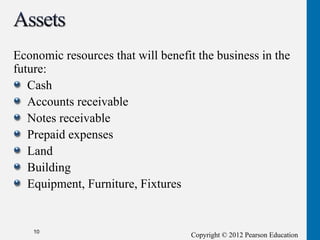

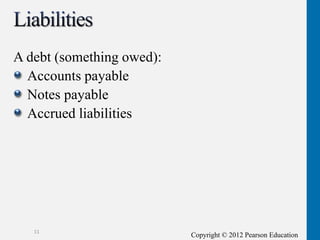

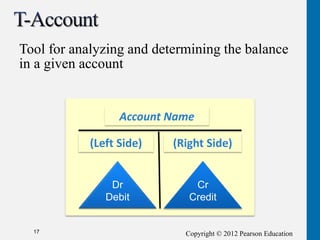

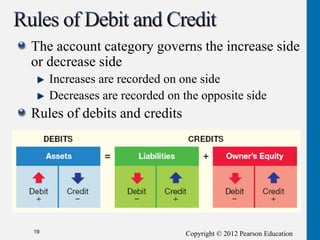

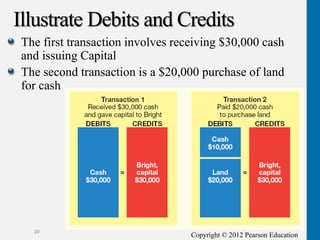

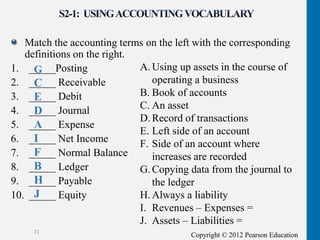

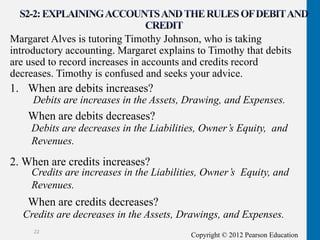

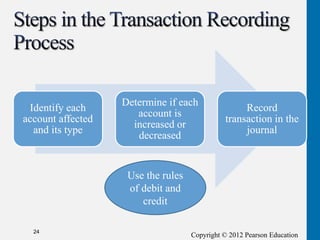

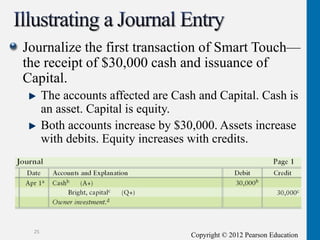

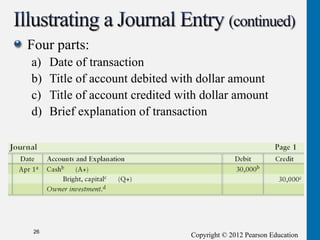

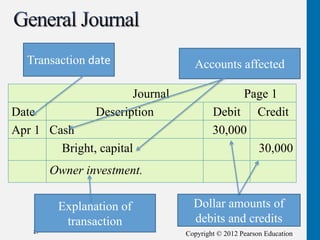

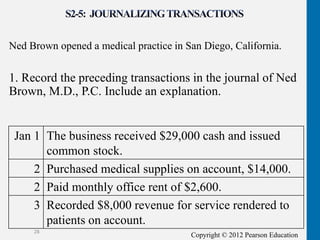

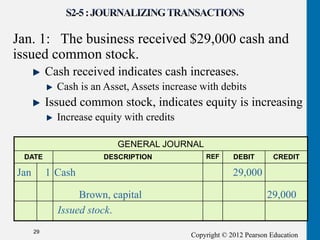

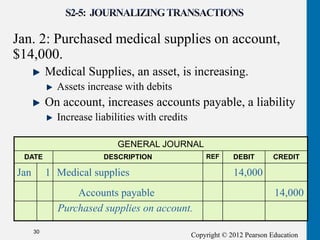

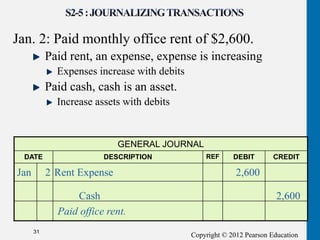

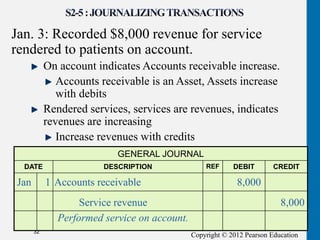

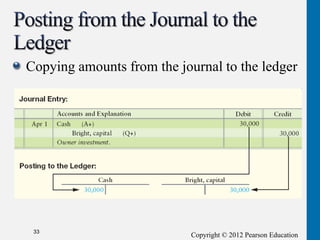

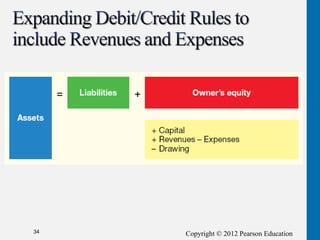

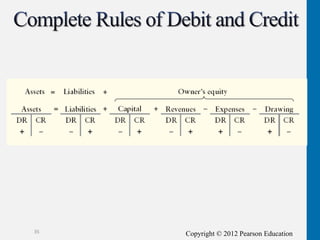

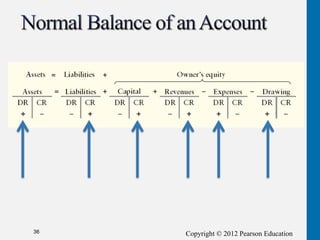

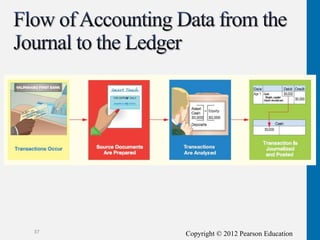

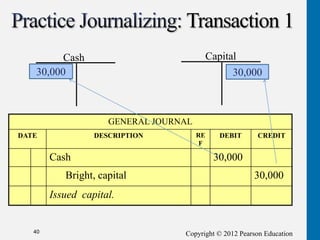

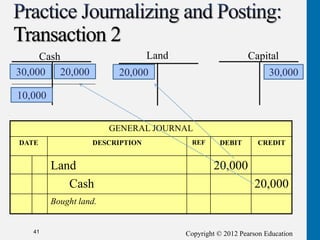

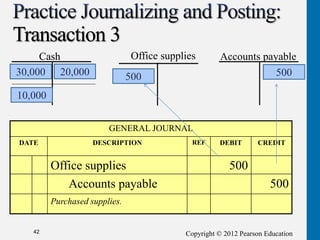

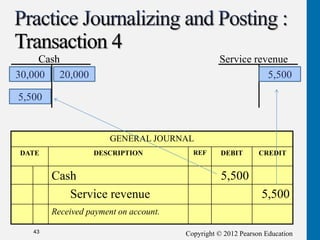

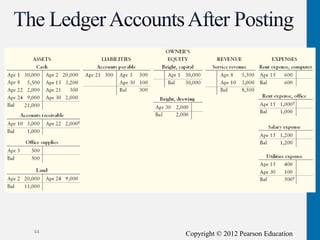

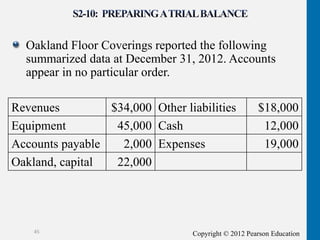

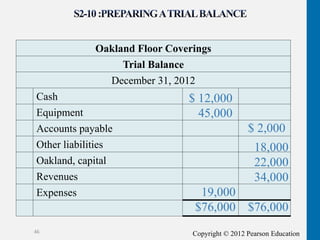

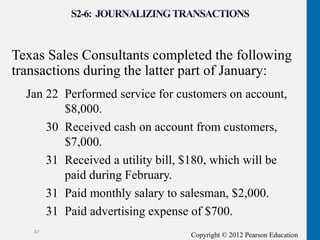

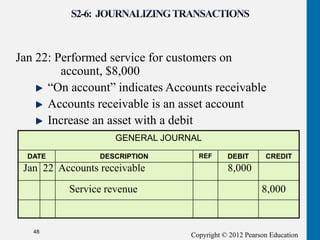

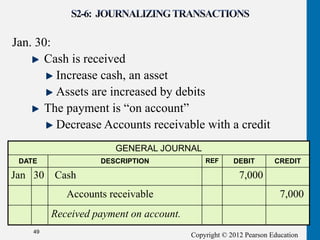

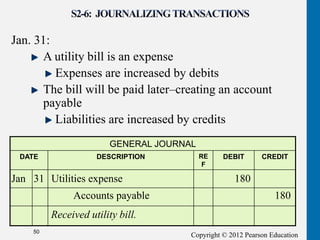

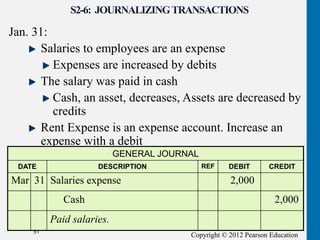

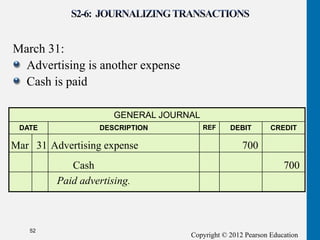

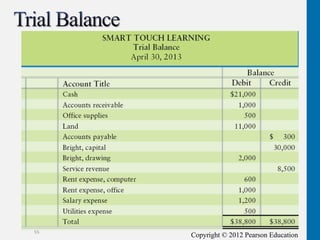

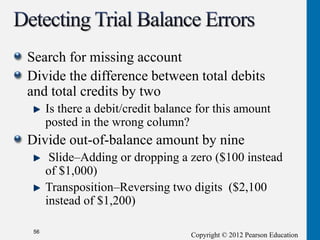

The document discusses accounting concepts such as journals, ledgers, debits and credits, and the transaction recording process. It provides examples of journalizing transactions, posting to T-accounts, and preparing a trial balance. Key steps covered include identifying accounts and amounts, determining if accounts increase or decrease using debit/credit rules, recording in the journal, and copying to the ledger. The goal is for total debits to equal total credits on the trial balance.