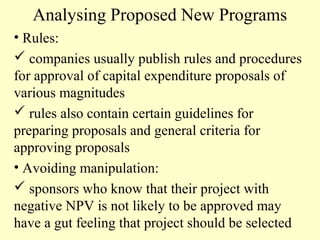

Downloaded 15 times

Strategic planning is a process where an organization decides on programs over the next 3-5 years and allocates resources to each program. It involves reviewing and updating strategic plans, setting assumptions and guidelines, business units creating initial plans, headquarters analyzing and aggregating plans, resolving issues through discussion, iterating plans, and final senior management review and approval. The process aims to align strategies, facilitate resource allocation, and develop managers through strategic thinking.

![[Whitepaper] The Definitive Guide to Strategic Planning: Here’s What You Need...](https://cdn.slidesharecdn.com/ss_thumbnails/thedefinitiveguidetostrategic-210214173358-thumbnail.jpg?width=640&height=640&fit=bounds)

![Almm monitoring and evaluation tools draft[1]acm](https://cdn.slidesharecdn.com/ss_thumbnails/almmmonitoringandevaluationtoolsdraft1acm-140417054101-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)