Download to read offline

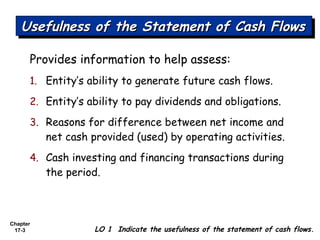

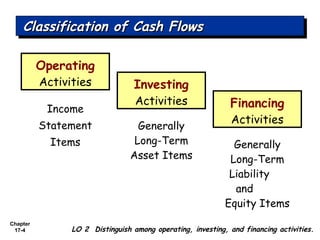

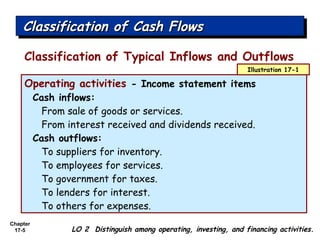

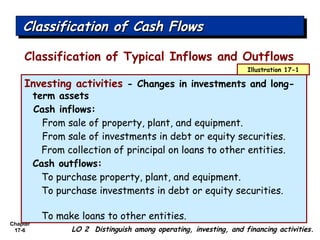

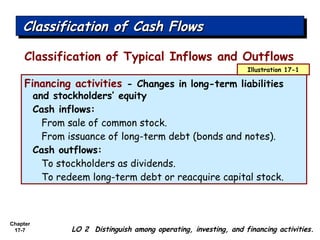

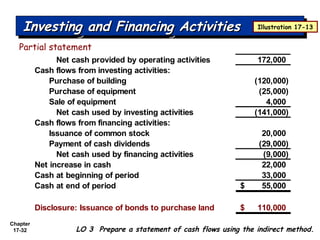

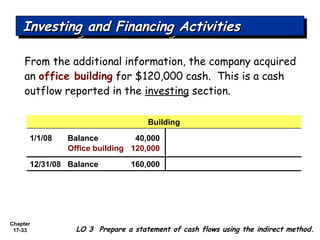

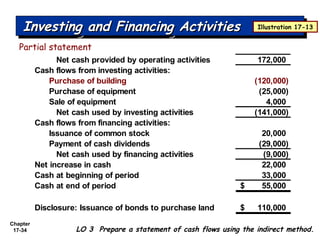

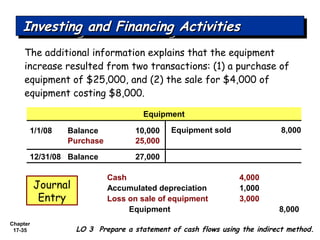

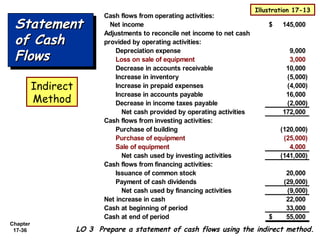

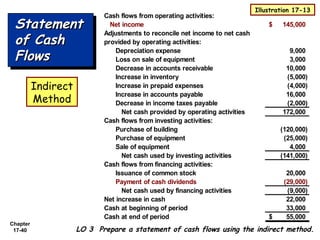

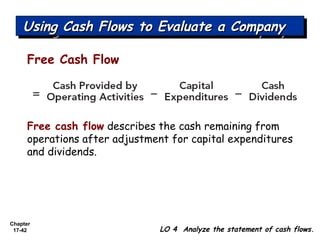

The document discusses the statement of cash flows, including: 1. It provides information about a company's ability to generate cash flows, pay obligations, and reasons for differences between net income and cash flows from operations. 2. Activities are classified as operating, investing, or financing based on whether they are from income statement items, long-term asset items, or long-term liability/equity items. 3. The indirect method is most commonly used to prepare the statement of cash flows, where net income is adjusted for non-cash expenses to determine cash flows from operations.