Download as PDF, PPTX

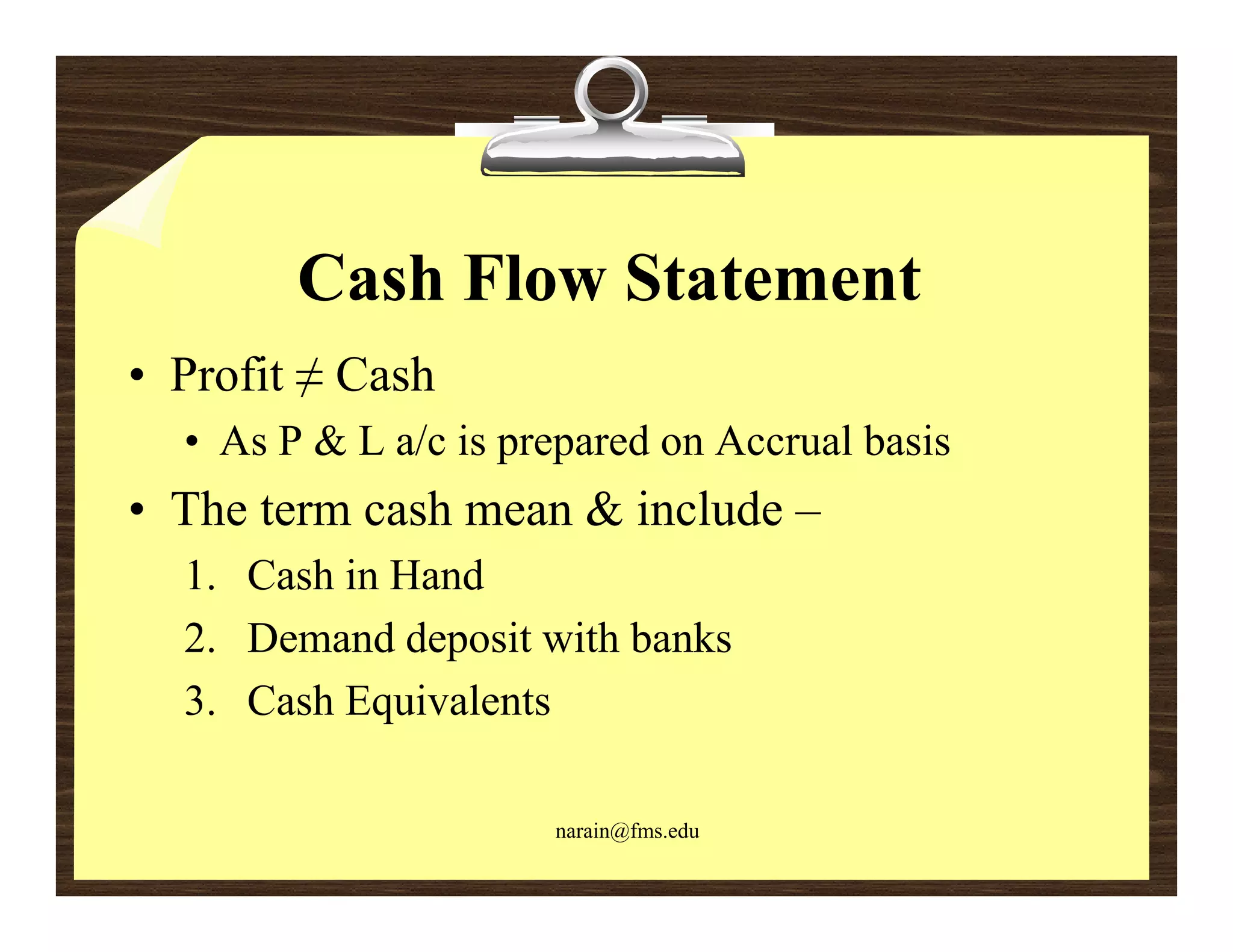

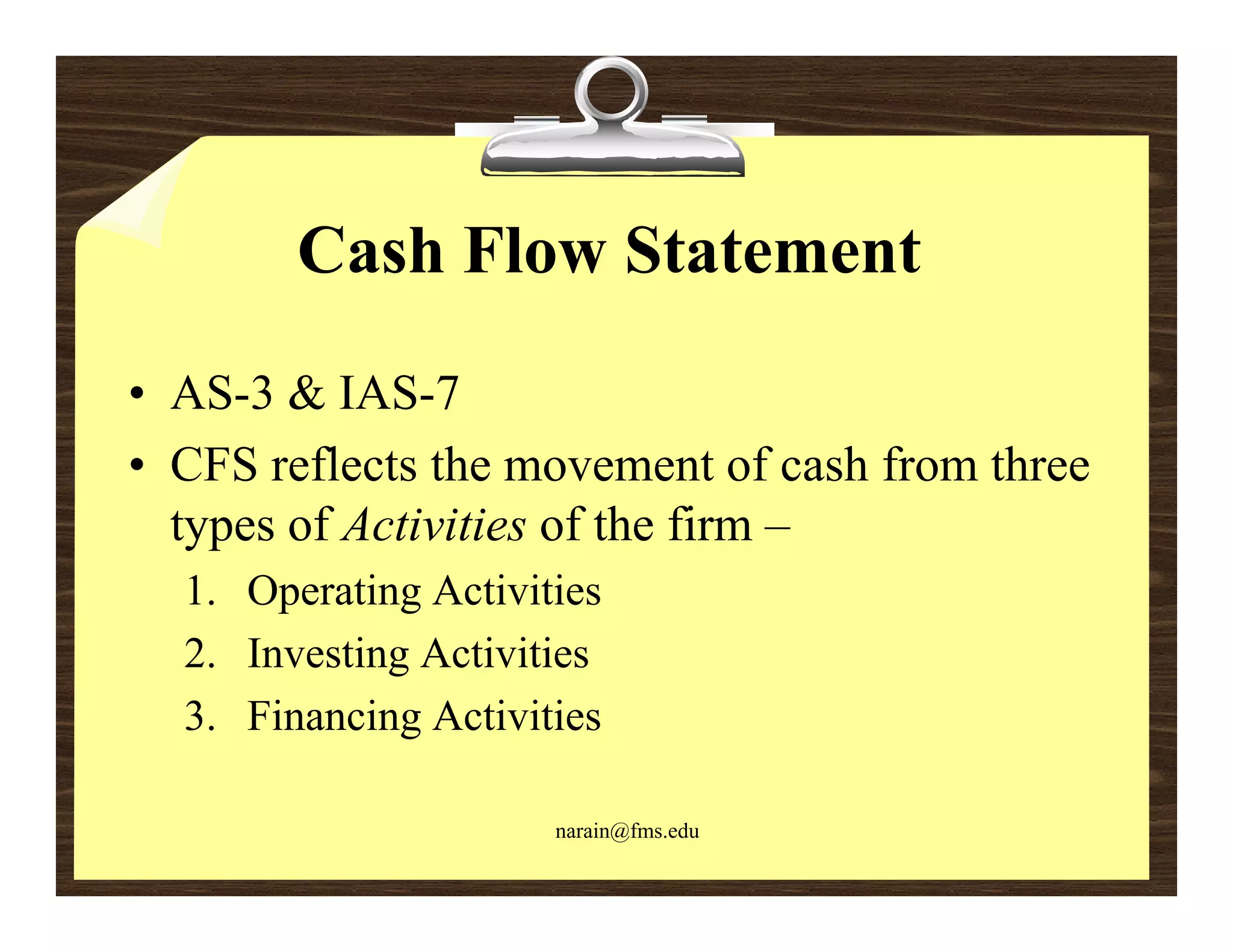

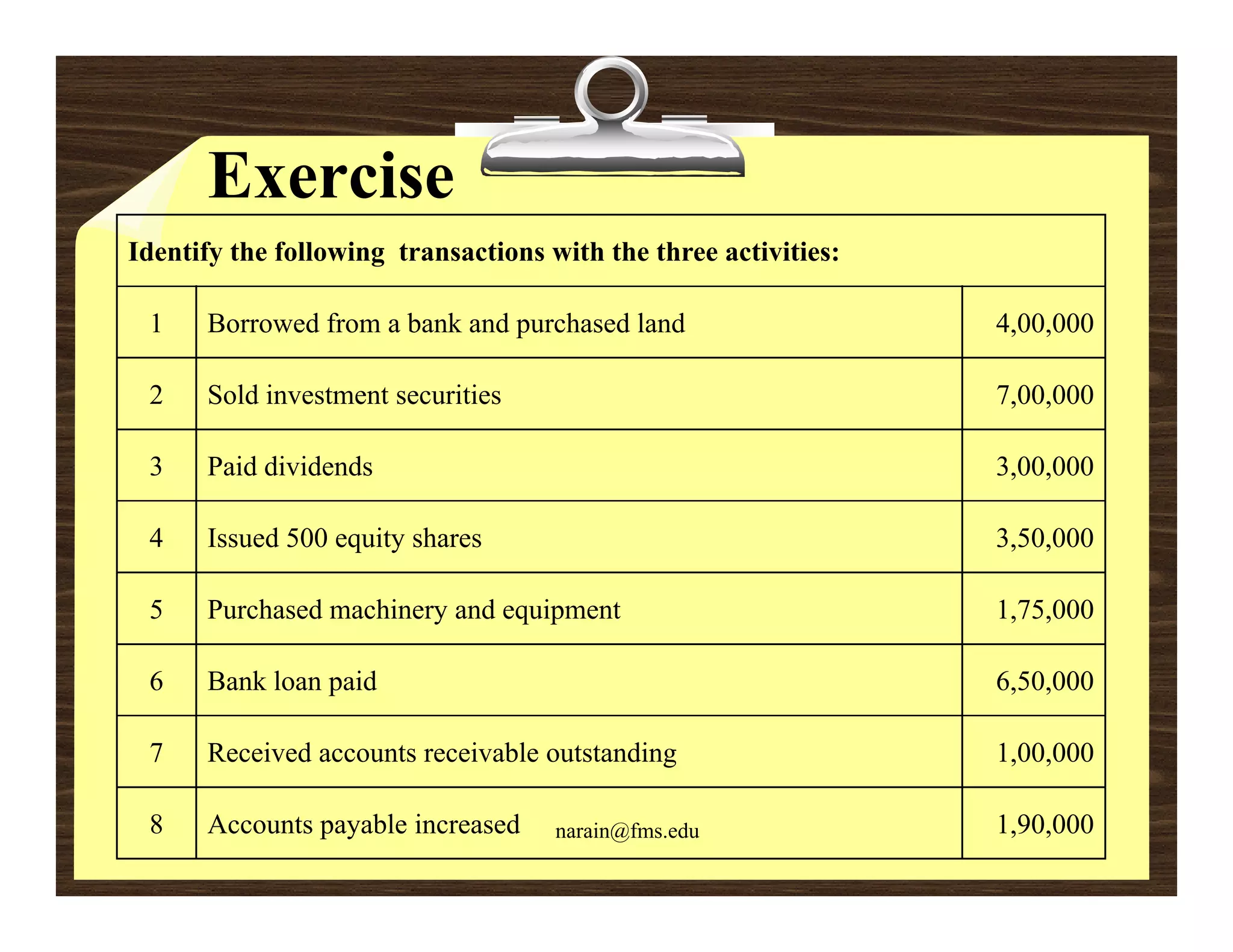

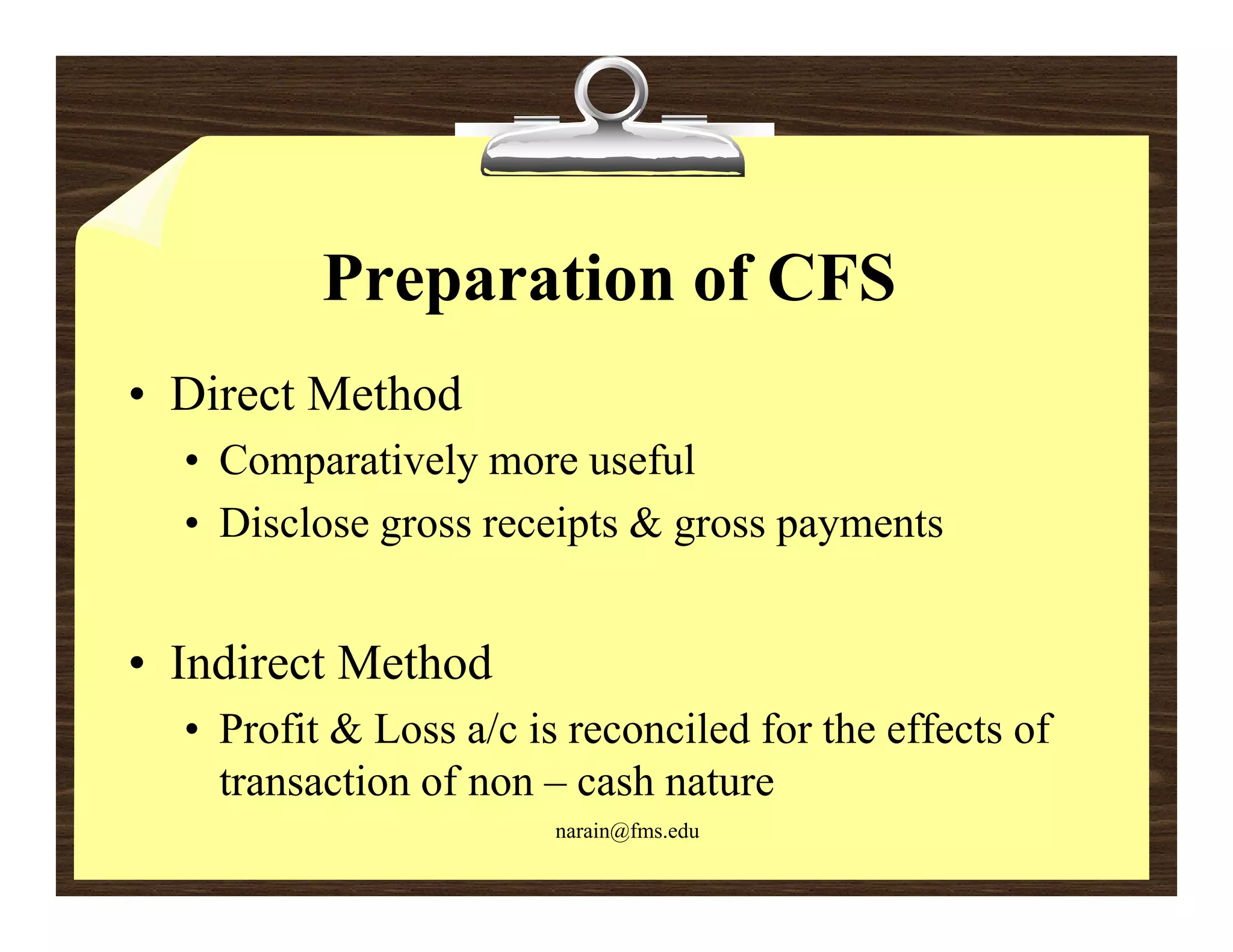

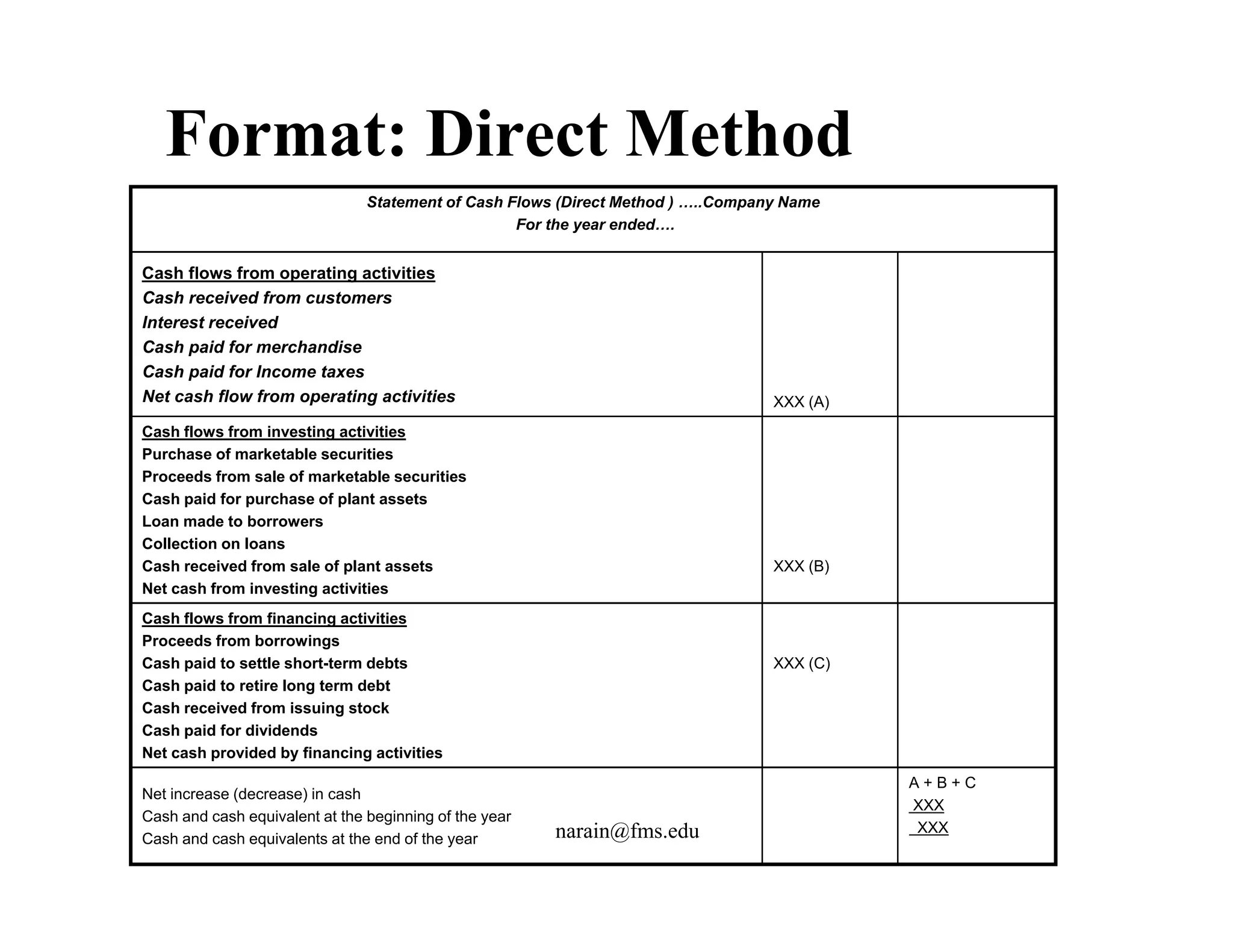

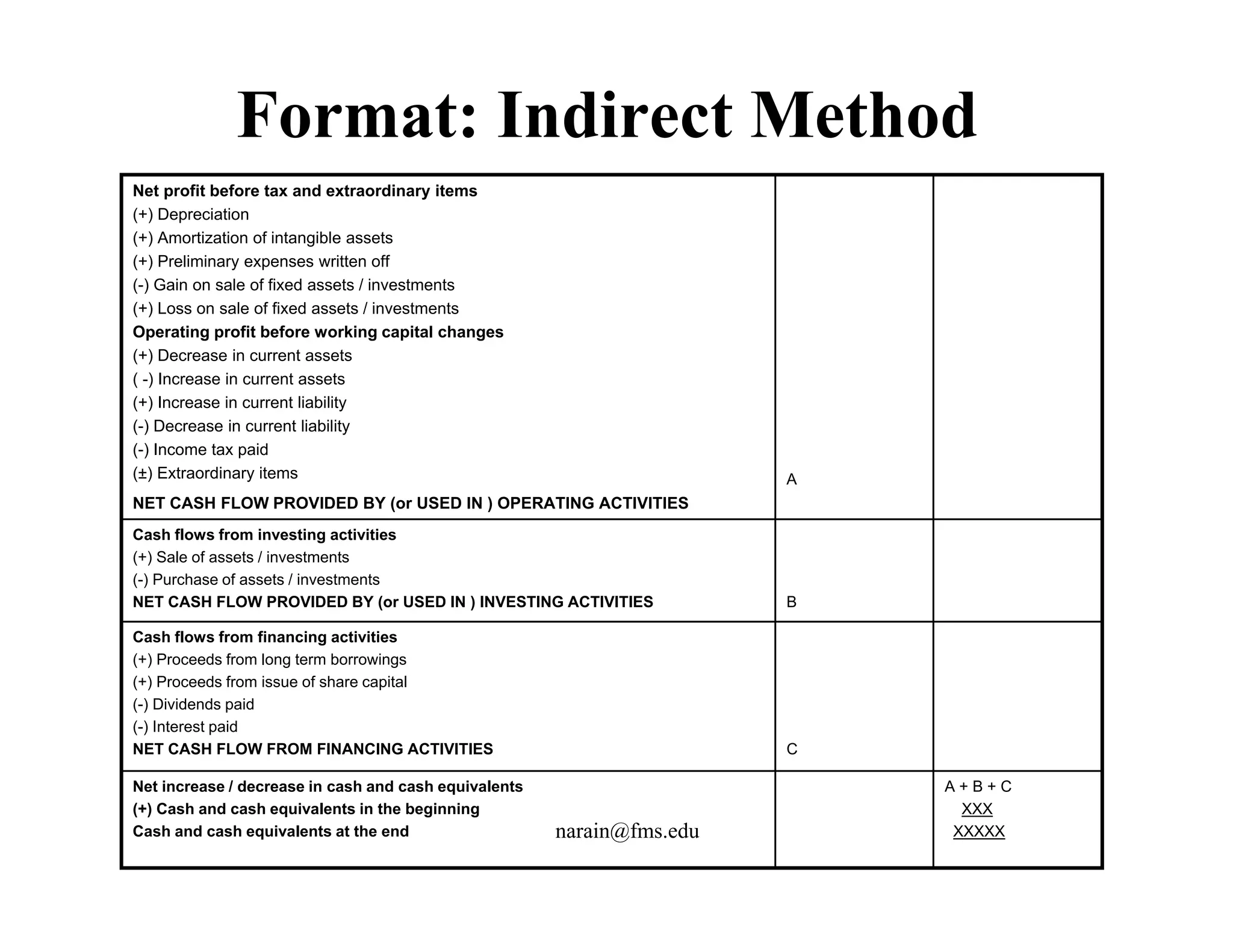

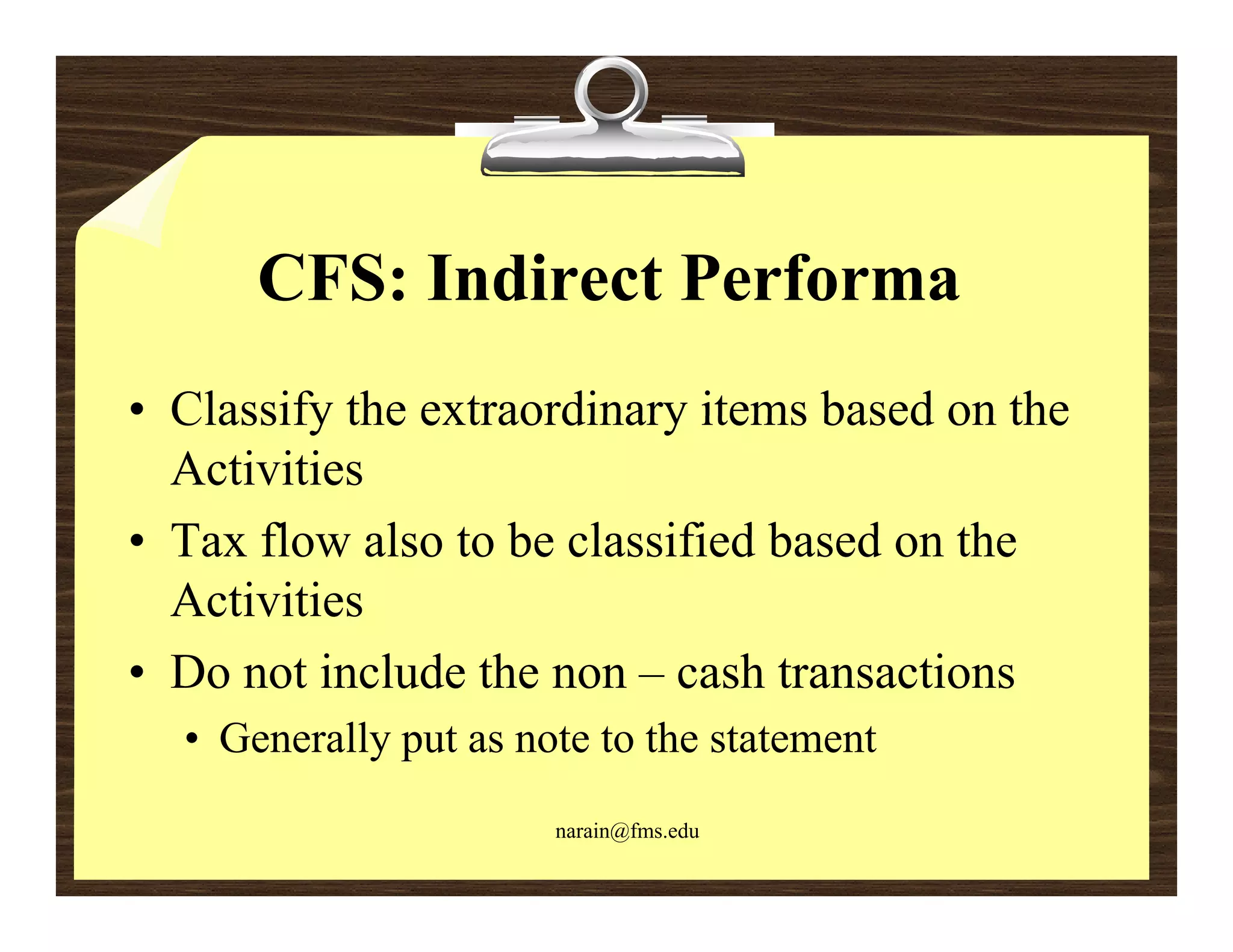

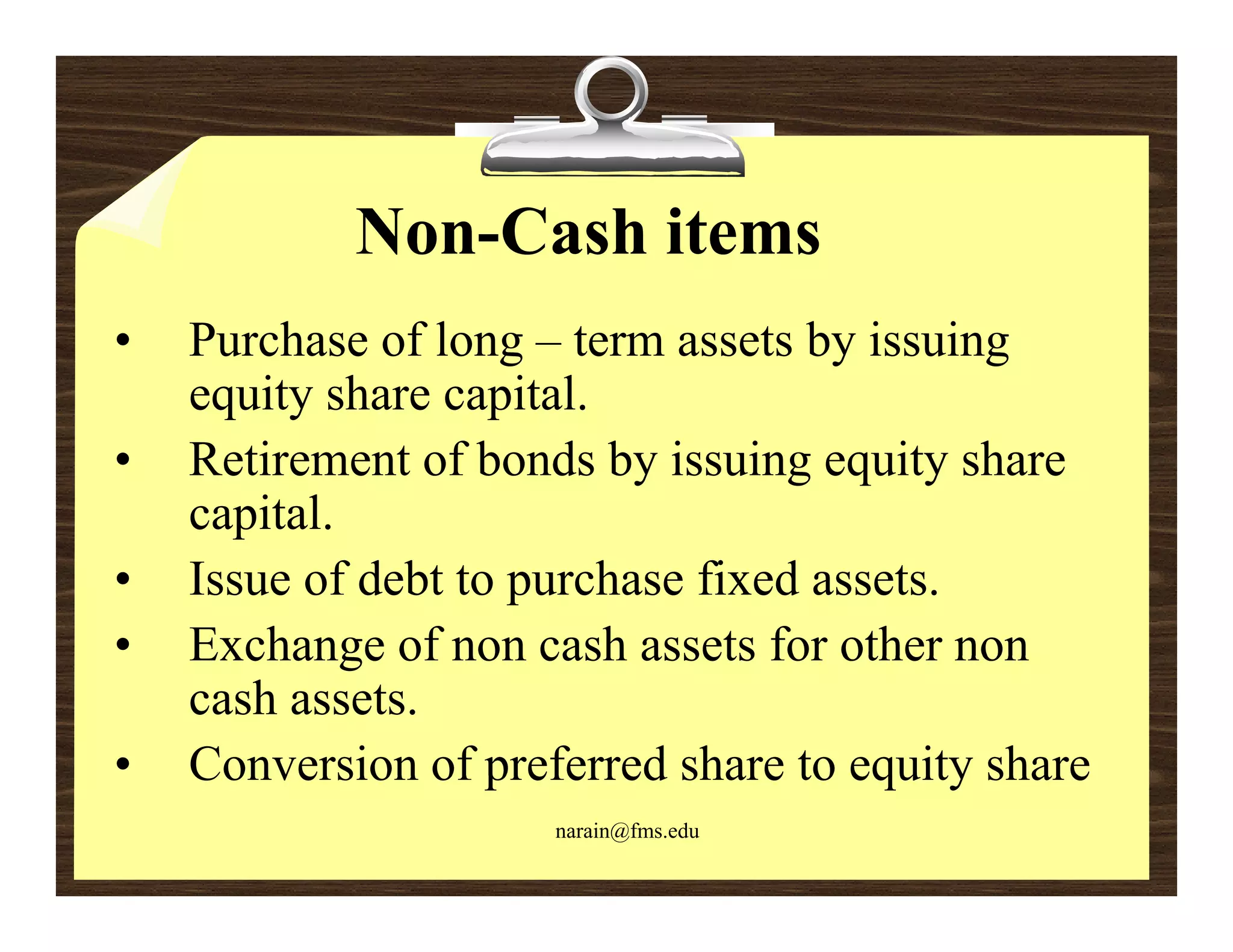

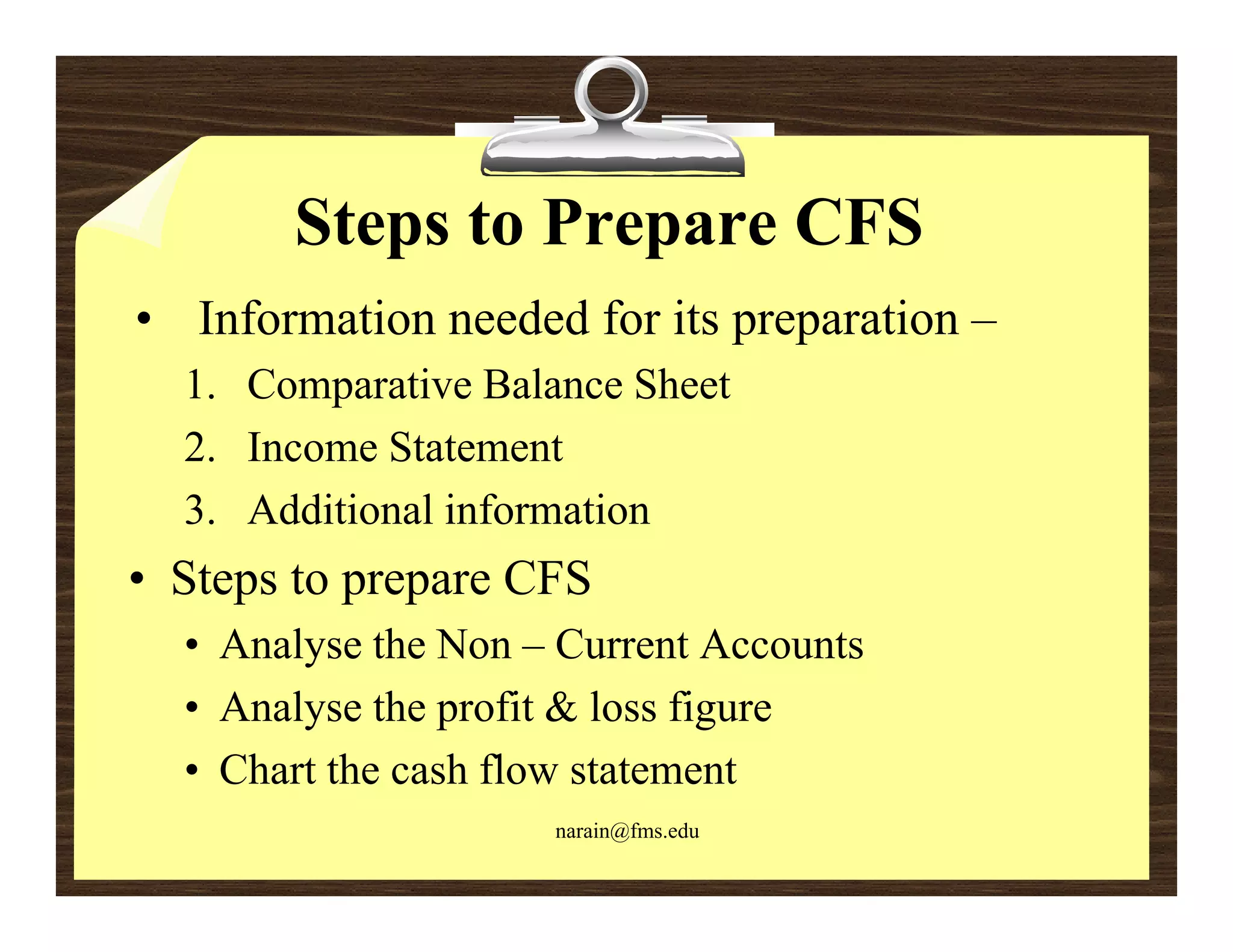

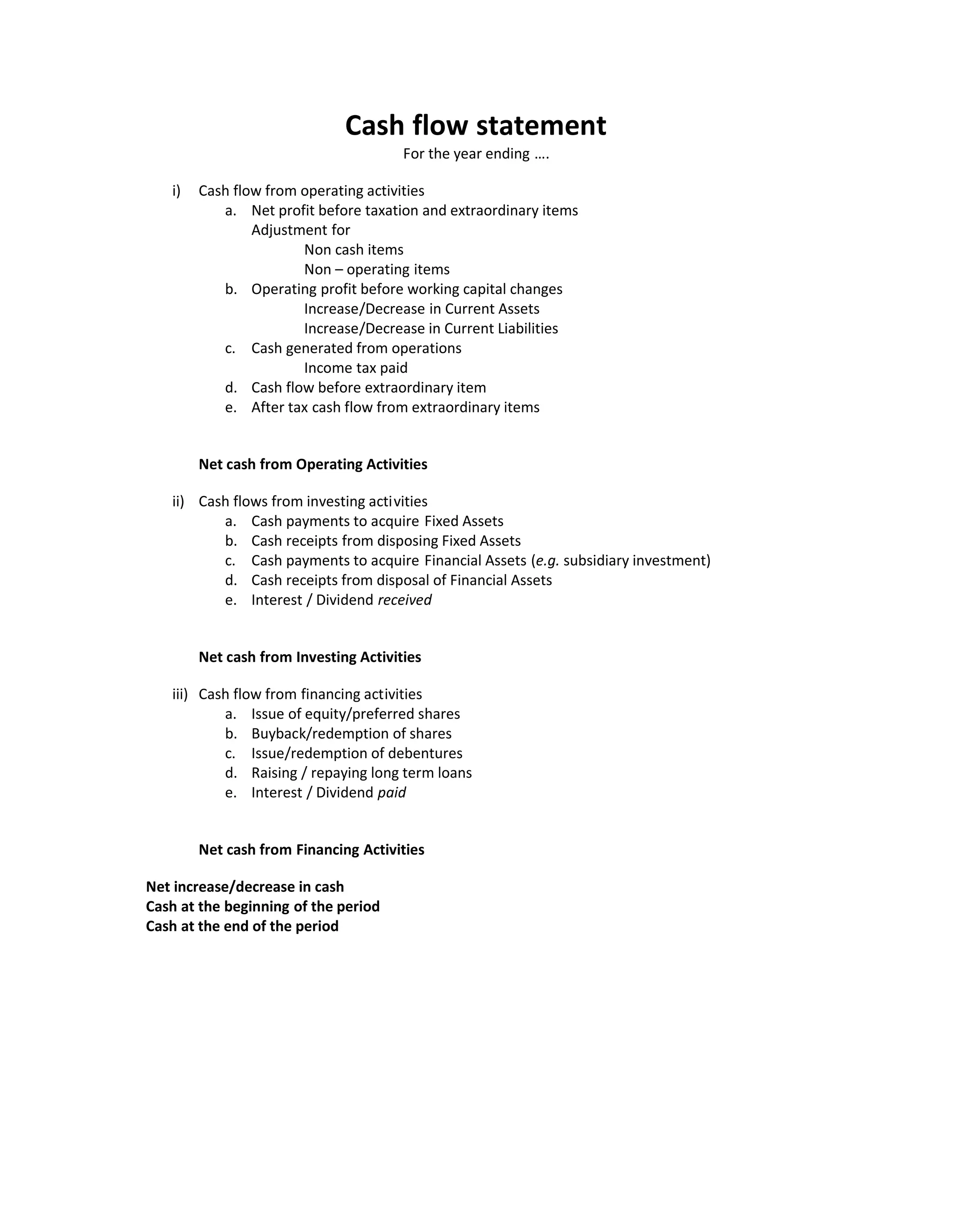

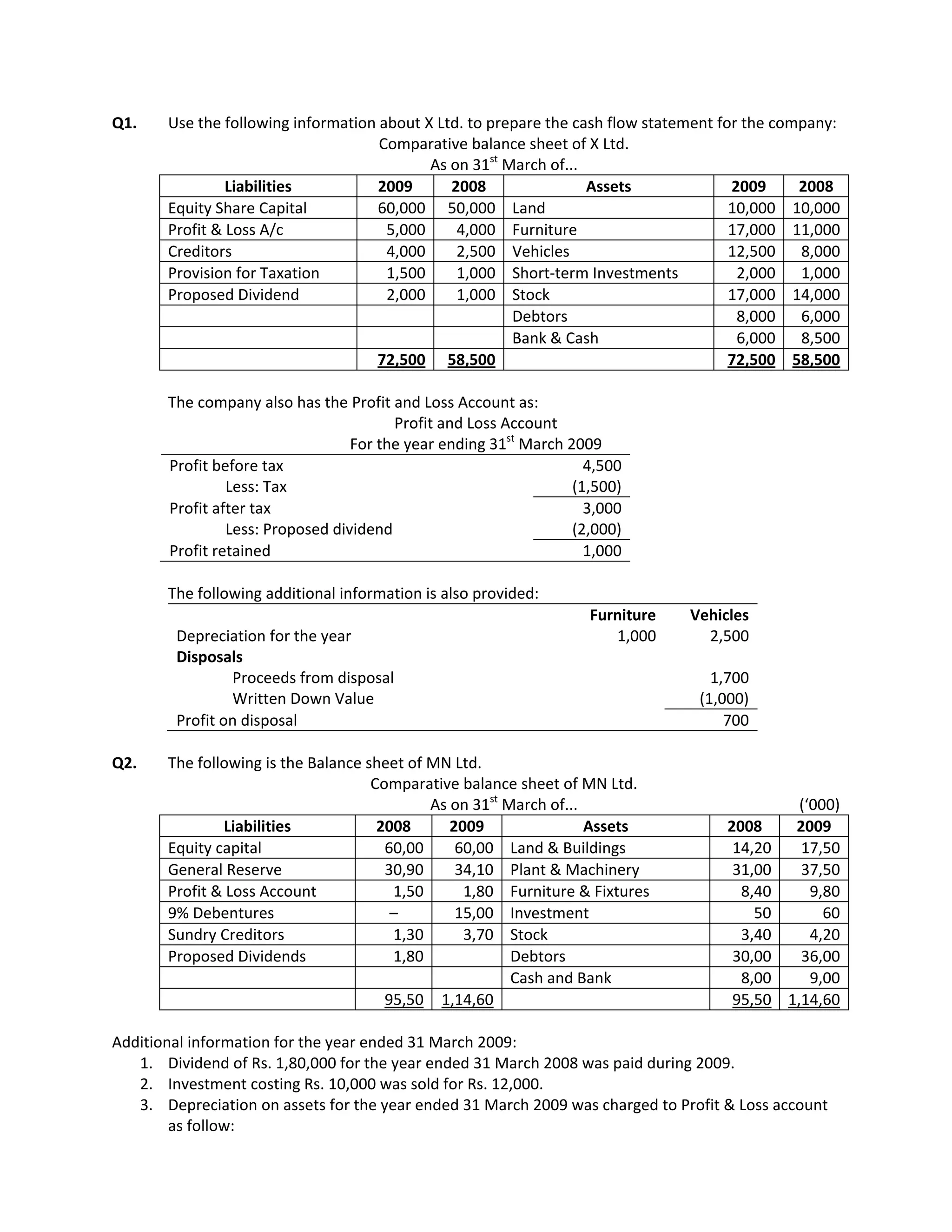

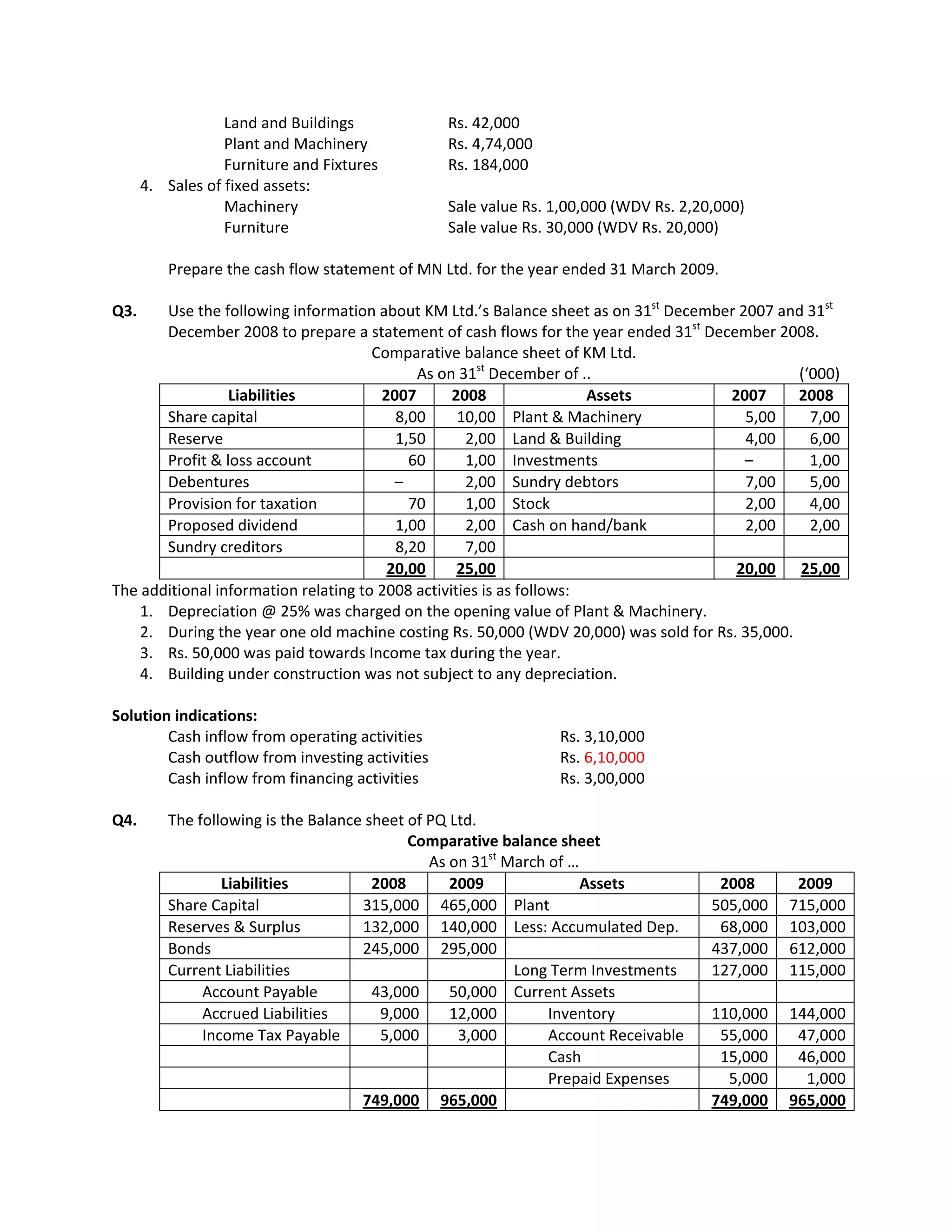

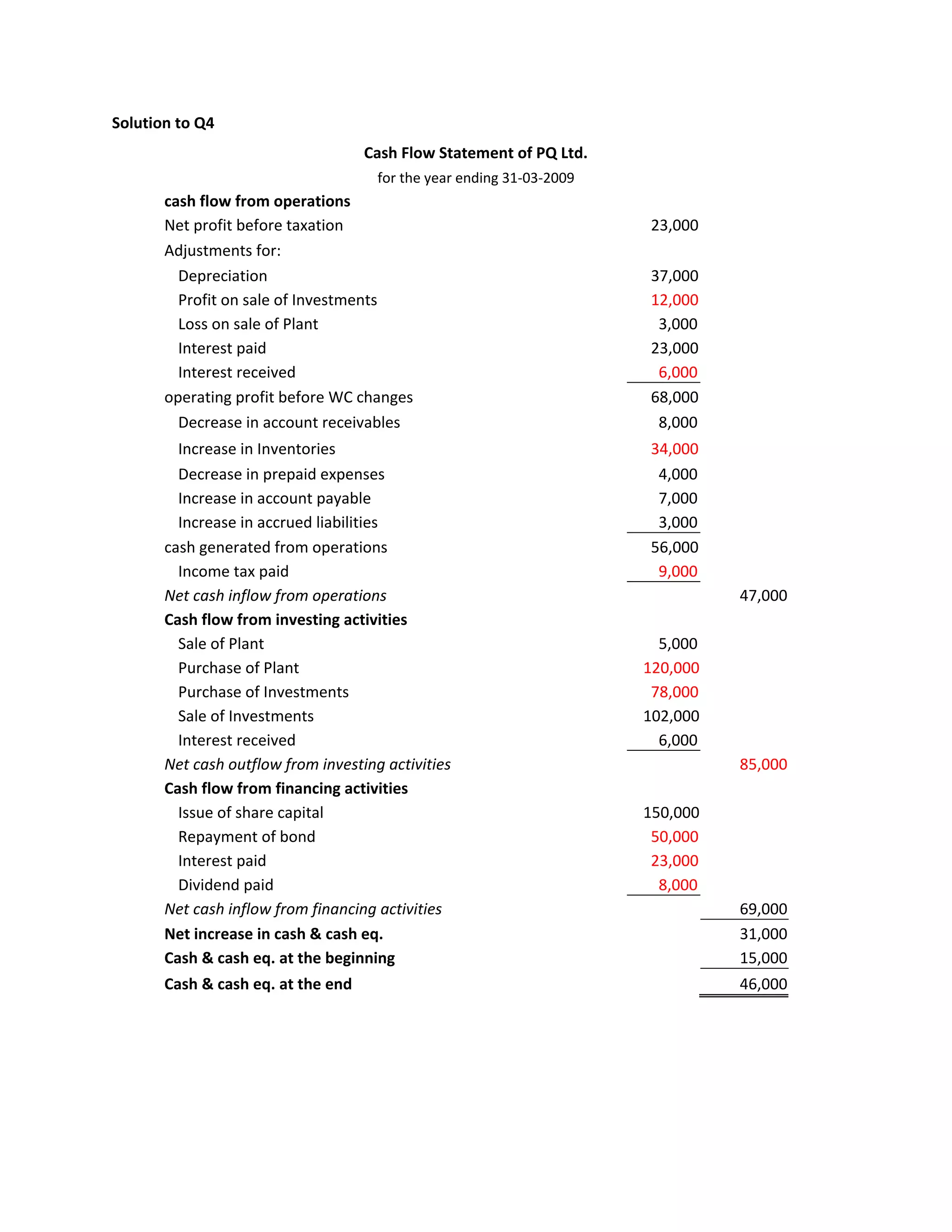

The document discusses the cash flow statement and how it differs from the profit and loss statement. It explains that the cash flow statement reflects the inflow and outflow of cash from operating, investing, and financing activities. It also provides examples of transactions that would be classified under each type of activity. Finally, it discusses the direct and indirect methods for preparing the cash flow statement.

![Working and functions_of_rbi[1]](https://cdn.slidesharecdn.com/ss_thumbnails/workingandfunctionsofrbi1-110522002449-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac10[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac101-p-110520054545-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac08[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac081-p-110520054521-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac05[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac051-p-110520054504-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac14[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac141-p-110520054443-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)

![Csac06[1].p](https://cdn.slidesharecdn.com/ss_thumbnails/csac061-p-110520054419-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)