Downloaded 29 times

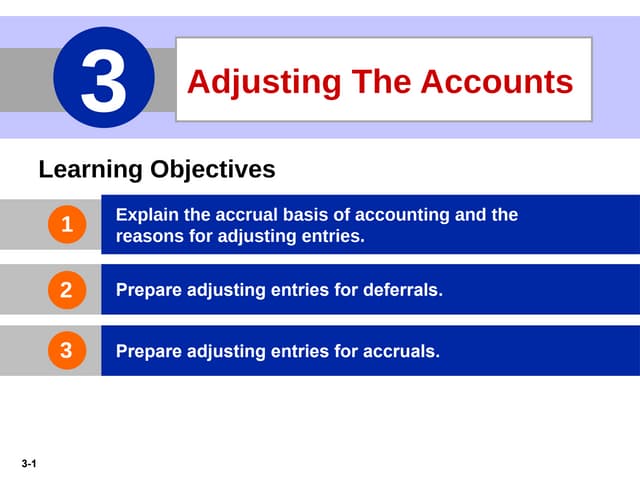

The document discusses accounting principles related to adjusting accounts, including the time period assumption, accrual basis of accounting, and different types of adjusting entries. It provides examples of adjusting entries for deferrals like prepaid expenses and unearned revenues. Specifically, it explains that adjusting entries are needed to ensure revenues are recorded when earned and expenses are recognized when incurred in accordance with the revenue recognition and matching principles. It also provides illustrations of adjusting entry journal entries for prepaid insurance, depreciation, and unearned rent revenue.