Downloaded 1,887 times

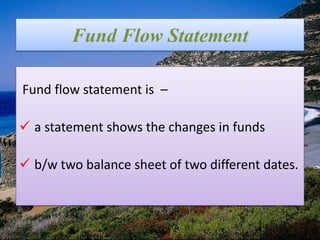

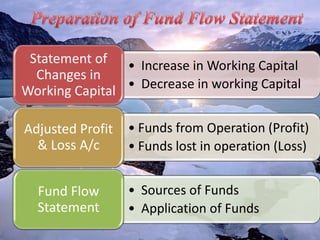

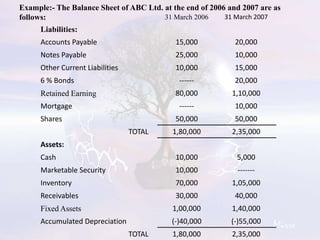

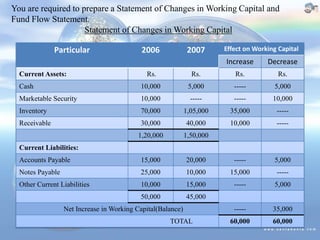

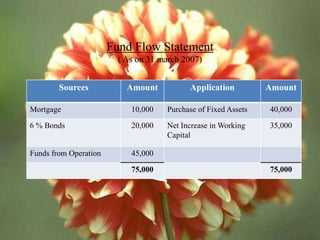

This document presents a fund flow statement example for ABC Ltd. between 2006 and 2007. Key points: - A fund flow statement shows changes in funds between two balance sheet dates by listing sources and applications of funds. - For ABC Ltd., sources of funds included taking a mortgage, redeeming bonds, and funds from operations. Applications included purchasing fixed assets and increasing working capital. - A statement of changes in working capital and adjusted profit and loss account were also prepared to determine the increase in working capital and funds from operations. - The completed fund flow statement for ABC Ltd. balanced sources of funds totalling Rs. 75,000 with applications of funds.