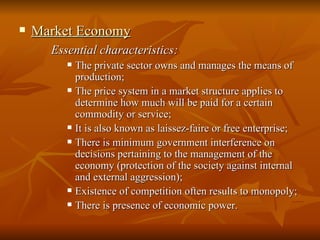

This document discusses different economic systems and their key characteristics. It begins by outlining the three basic economic problems of what to produce, how to produce, and for whom to produce. It then defines four main economic systems - traditional, command, market, and mixed - and describes their essential features. The document also distinguishes between the economic philosophies of capitalism, communism, and socialism.

![Lesson 1--fop-and-types-of-econ[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-1-fop-and-types-of-econ1-130409195929-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)