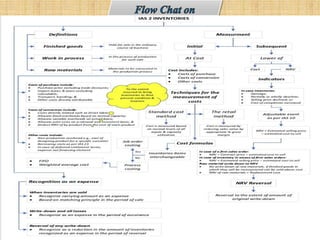

Standard: International AccountingStandard issued by the IASB.

Issued: 1975;

Re-issued in 1993 and 2003.

Effective Date: 1 January 2005.

Purpose:

Defines accounting treatment for inventories.

Guides on cost determination and measurement (lower of cost or

net realizable value).

Specifies cost formulas: FIFO and Weighted Average.

Details recognition and disclosure requirements in financial

statements.

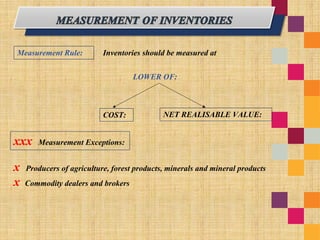

Measurement Rule: Inventoriesshould be measured at

LOWER OF:

COST: NET REALISABLE VALUE:

xxx Measurement Exceptions:

x Producers of agriculture, forest products, minerals and mineral products

x Commodity dealers and brokers

7.

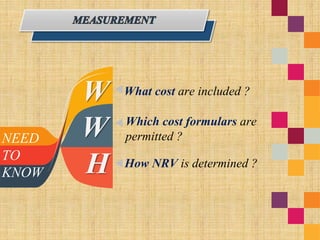

What cost areincluded ?

Which cost formulars are

permitted ?

How NRV is determined ?

NEED

TO

KNOW

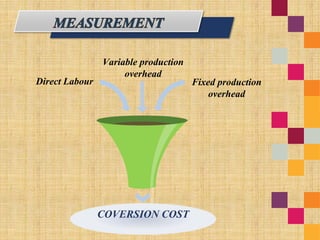

Direct Labour Fixedproduction

overhead

Variable production

overhead

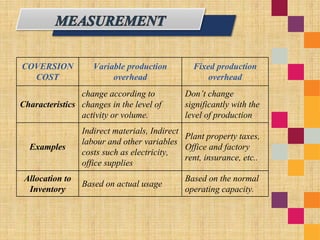

COVERSION COST

11.

COVERSION

COST

Variable production

overhead

Fixed production

overhead

Characteristics

changeaccording to

changes in the level of

activity or volume.

Don’t change

significantly with the

level of production

Examples

Indirect materials, Indirect

labour and other variables

costs such as electricity,

office supplies

Plant property taxes,

Office and factory

rent, insurance, etc..

Allocation to

Inventory

Based on actual usage

Based on the normal

operating capacity.

12.

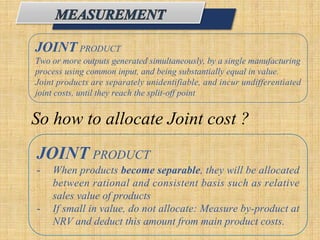

JOINT PRODUCT

Two ormore outputs generated simultaneously, by a single manufacturing

process using common input, and being substantially equal in value.

Joint products are separately unidentifiable, and incur undifferentiated

joint costs, until they reach the split-off point.

So how to allocate Joint cost ?

JOINT PRODUCT

- When products become separable, they will be allocated

between rational and consistent basis such as relative

sales value of products

- If small in value, do not allocate: Measure by-product at

NRV and deduct this amount from main product costs.

13.

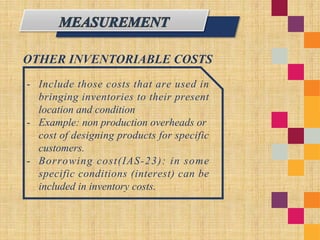

OTHER INVENTORIABLE COSTS

-Include those costs that are used in

bringing inventories to their present

location and condition

- Example: non production overheads or

cost of designing products for specific

customers.

- Borrowing cost(IAS-23): in some

specific conditions (interest) can be

included in inventory costs.

14.

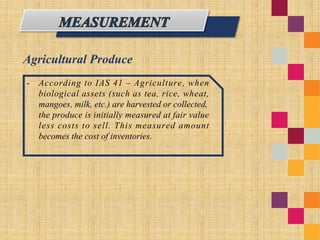

Agricultural Produce

- Accordingto IAS 41 – Agriculture, when

biological assets (such as tea, rice, wheat,

mangoes, milk, etc.) are harvested or collected,

the produce is initially measured at fair value

less costs to sell. This measured amount

becomes the cost of inventories.

15.

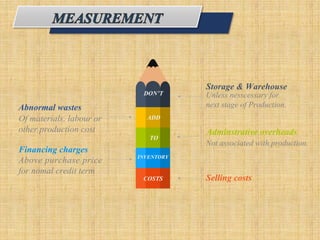

Abnormal wastes

Financing charges

Abovepurchase price

for nomal credit term

Storage & Warehouse

Unless nesscessary for

next stage of Production.

Adminstrative overheads

Not associated with production.

Selling costs

DON’T

ADD

TO

INVENTORY

COSTS

Of materials, labour or

other production cost

16.

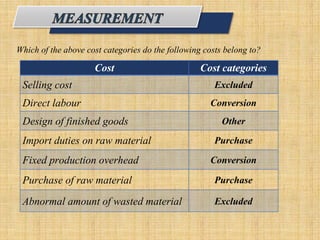

Which of theabove cost categories do the following costs belong to?

Cost Cost categories

Selling cost Excluded

Direct labour Conversion

Design of finished goods Other

Import duties on raw material Purchase

Fixed production overhead Conversion

Purchase of raw material Purchase

Abnormal amount of wasted material Excluded

17.

Standard Cost

Method

used foraccounts of

normal level of materials,

supplies, labours,

efficiency and capacity

Retail inventory

Method

used in retail industry for

measuring large number of

rapidly changing items.

cost is determined by reducing

the sales value of inventory by

percentage gross margin.

For convenience to approximate cost of inventories

18.

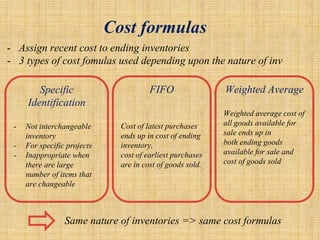

Specific

Identification

- Not interchangeable

inventory

-For specific projects

- Inappropriate when

there are large

number of items that

are changeable

FIFO

Cost of latest purchases

ends up in cost of ending

inventory,

cost of earliest purchases

are in cost of goods sold.

Weighted Average

Weighted average cost of

all goods available for

sale ends up in

both ending goods

available for sale and

cost of goods sold

- Assign recent cost to ending inventories

- 3 types of cost fomulas used depending upon the nature of inv

Same nature of inventories => same cost formulas

Cost formulas

19.

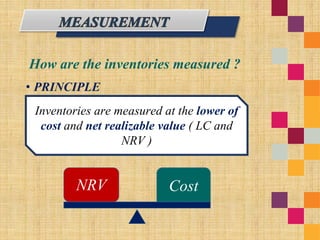

• PRINCIPLE

Inventories aremeasured at the lower of

cost and net realizable value ( LC and

NRV )

How are the inventories measured ?

NRV Cost

21.

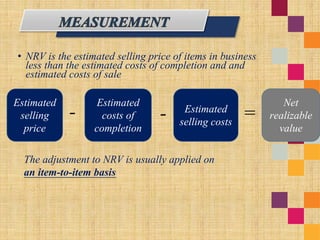

• NRV isthe estimated selling price of items in business

less than the estimated costs of completion and and

estimated costs of sale

Estimated

selling

price

Estimated

costs of

completion

Estimated

selling costs

Net

realizable

value

- - =

The adjustment to NRV is usually applied on

an item-to-item basis

22.

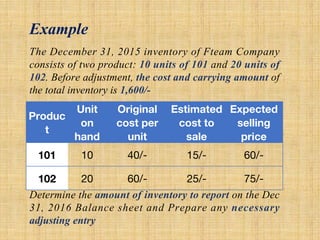

Produc

t

Unit

on

hand

Original

cost per

unit

Estimated

cost to

sale

Expected

selling

price

10110 40/- 15/- 60/-

102 20 60/- 25/- 75/-

The December 31, 2015 inventory of Fteam Company

consists of two product: 10 units of 101 and 20 units of

102. Before adjustment, the cost and carrying amount of

the total inventory is 1,600/-

Determine the amount of inventory to report on the Dec

31, 2016 Balance sheet and Prepare any necessary

adjusting entry

Example

23.

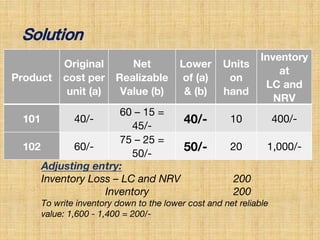

Product

Original

cost per

unit (a)

Net

Realizable

Value(b)

Lower

of (a)

& (b)

Units

on

hand

Inventory

at

LC and

NRV

101 40/-

60 – 15 =

45/-

40/- 10 400/-

102 60/-

75 – 25 =

50/-

50/- 20 1,000/-

Adjusting entry:

Inventory Loss – LC and NRV 200

Inventory 200

To write inventory down to the lower cost and net reliable

value: 1,600 - 1,400 = 200/-

Solution

24.

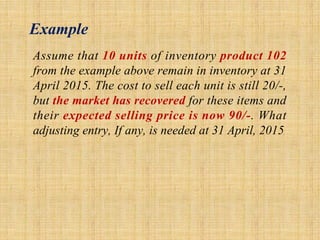

Example

Assume that 10units of inventory product 102

from the example above remain in inventory at 31

April 2015. The cost to sell each unit is still 20/-,

but the market has recovered for these items and

their expected selling price is now 90/-. What

adjusting entry, If any, is needed at 31 April, 2015

25.

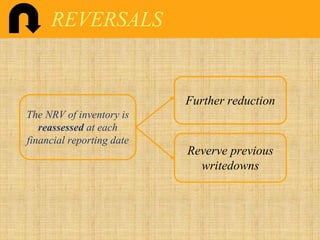

REVERSALS

The NRV ofinventory is

reassessed at each

financial reporting date

Further reduction

Reverve previous

writedowns

26.

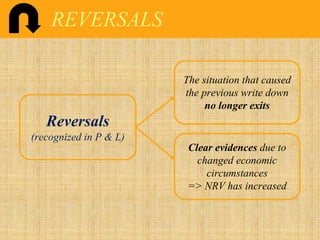

REVERSALS

Reversals

(recognized in P& L)

The situation that caused

the previous write down

no longer exits

Clear evidences due to

changed economic

circumstances

=> NRV has increased

27.

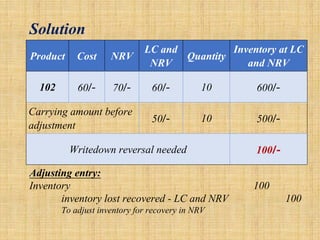

Solution

Product Cost NRV

LCand

NRV

Quantity

Inventory at LC

and NRV

102 60/- 70/- 60/- 10 600/-

Carrying amount before

adjustment

50/- 10 500/-

Writedown reversal needed 100/-

Adjusting entry:

Inventory 100

inventory lost recovered - LC and NRV 100

To adjust inventory for recovery in NRV

28.

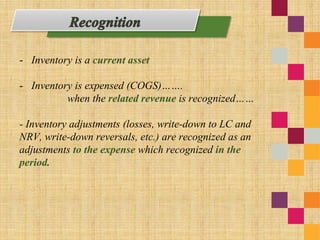

- Inventory isa current asset

- Inventory is expensed (COGS)…….

when the related revenue is recognized……

- Inventory adjustments (losses, write-down to LC and

NRV, write-down reversals, etc.) are recognized as an

adjustments to the expense which recognized in the

period.

29.

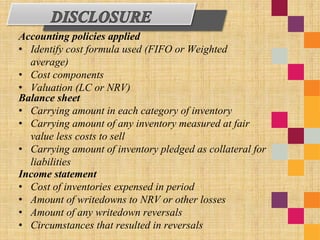

Accounting policies applied

•Identify cost formula used (FIFO or Weighted

average)

• Cost components

• Valuation (LC or NRV)

Balance sheet

• Carrying amount in each category of inventory

• Carrying amount of any inventory measured at fair

value less costs to sell

• Carrying amount of inventory pledged as collateral for

liabilities

Income statement

• Cost of inventories expensed in period

• Amount of writedowns to NRV or other losses

• Amount of any writedown reversals

• Circumstances that resulted in reversals

30.

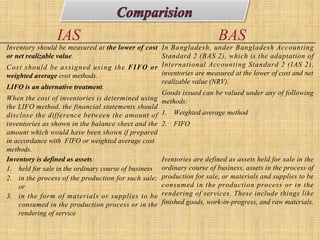

Inventory should bemeasured at the lower of cost

or net realizable value.

Cost should be assigned using the FIFO or

weighted average cost methods.

LIFO is an alternative treatment.

When the cost of inventories is determined using

the LIFO method, the financial statements should

disclose the difference between the amount of

inventories as shown in the balance sheet and the

amount which would have been shown if prepared

in accordance with FIFO or weighted average cost

methods.

In Bangladesh, under Bangladesh Accounting

Standard 2 (BAS 2), which is the adaptation of

International Accounting Standard 2 (IAS 2),

inventories are measured at the lower of cost and net

realizable value (NRV).

Goods issued can be valued under any of following

methods:

1. Weighted average method

2. FIFO

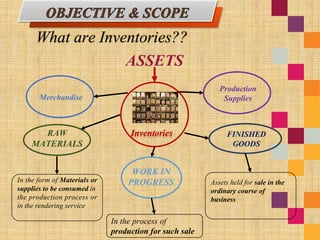

Inventory is defined as assets:

1. held for sale in the ordinary course of business

2. in the process of the production for such sale;

or

3. in the form of materials or supplies to be

consumed in the production process or in the

rendering of service

Iventories are defined as assets held for sale in the

ordinary course of business, assets in the process of

production for sale, or materials and supplies to be

consumed in the production process or in the

rendering of services. These include things like

finished goods, work-in-progress, and raw materials.

IAS BAS