Download as PDF, PPTX

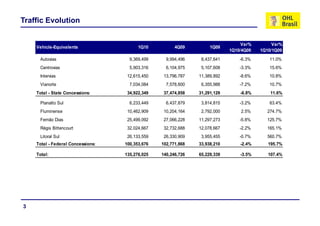

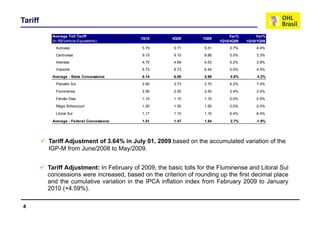

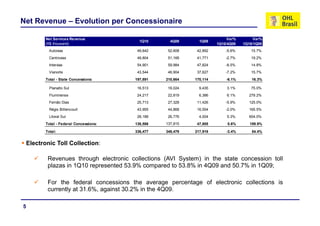

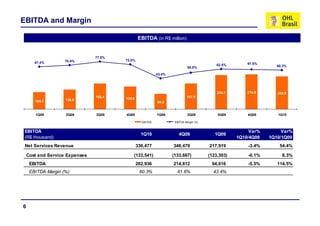

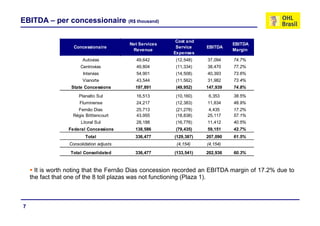

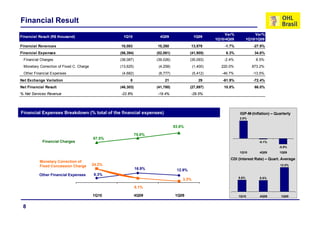

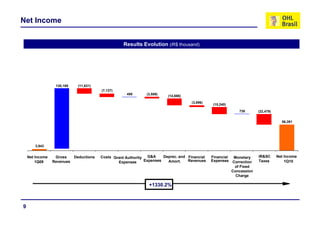

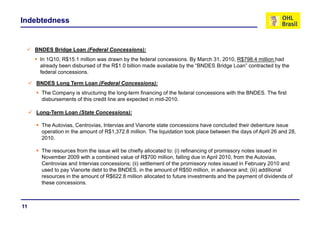

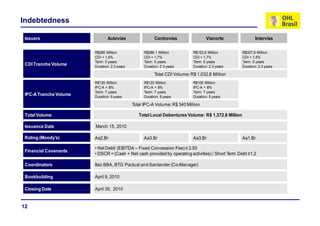

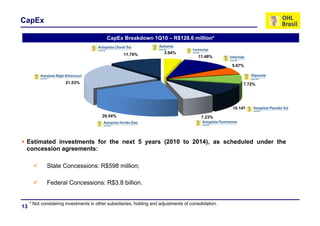

The document provides financial results and traffic data for OHL Brasil for the first quarter of 2010. Some key points: - Total traffic increased 11.6% compared to the first quarter of 2009 across state concessions and 195.7% across federal concessions. - Net revenue increased 54.4% overall compared to the first quarter of 2009, with strong growth across all concessions. - EBITDA was R$202.9 million for the quarter, a 114.5% increase over the first quarter of 2009, with an EBITDA margin of 60.3%. - Net income was R$56.4 million for the quarter compared to a net loss in the prior year period