Downloaded 611 times

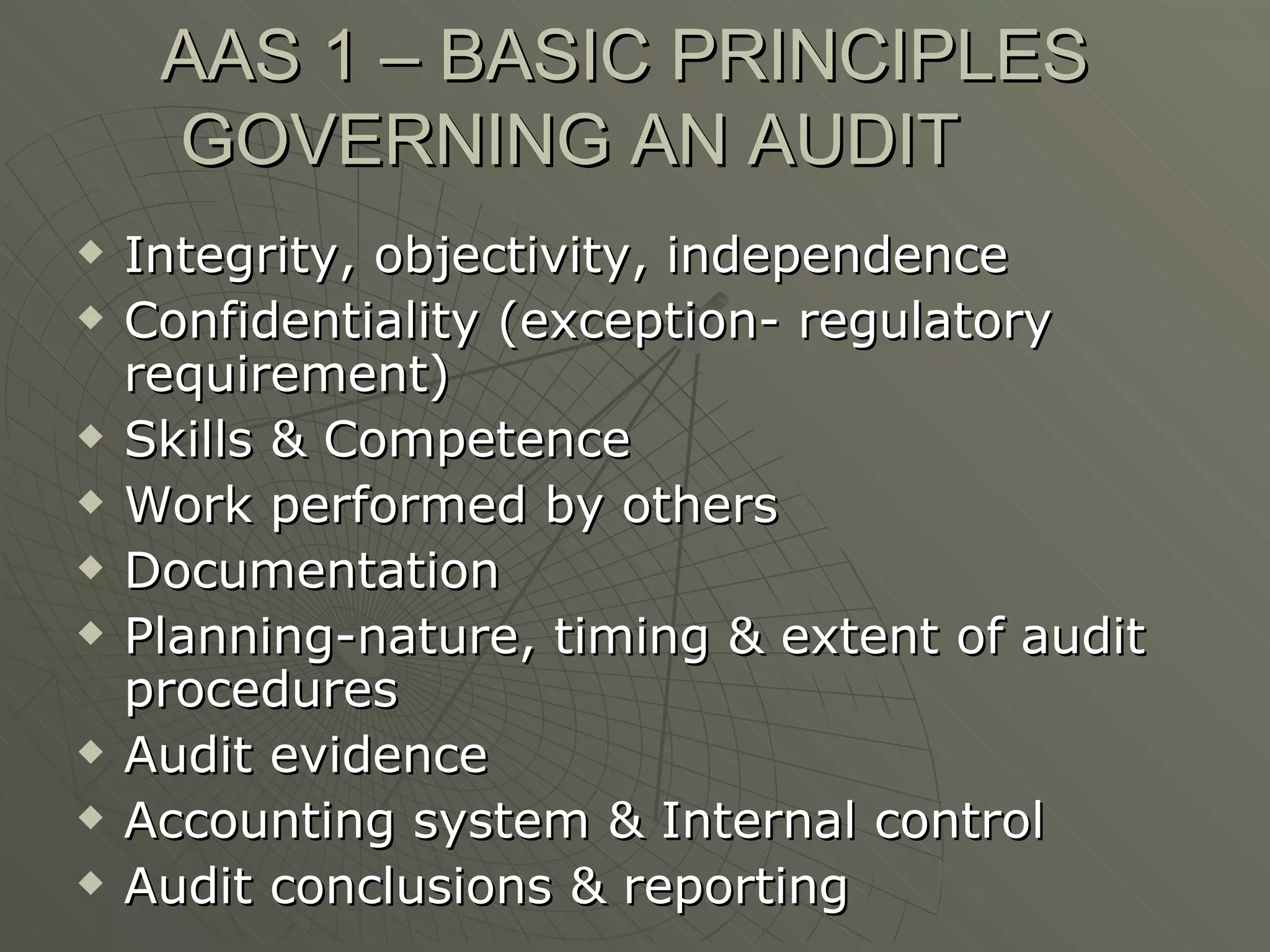

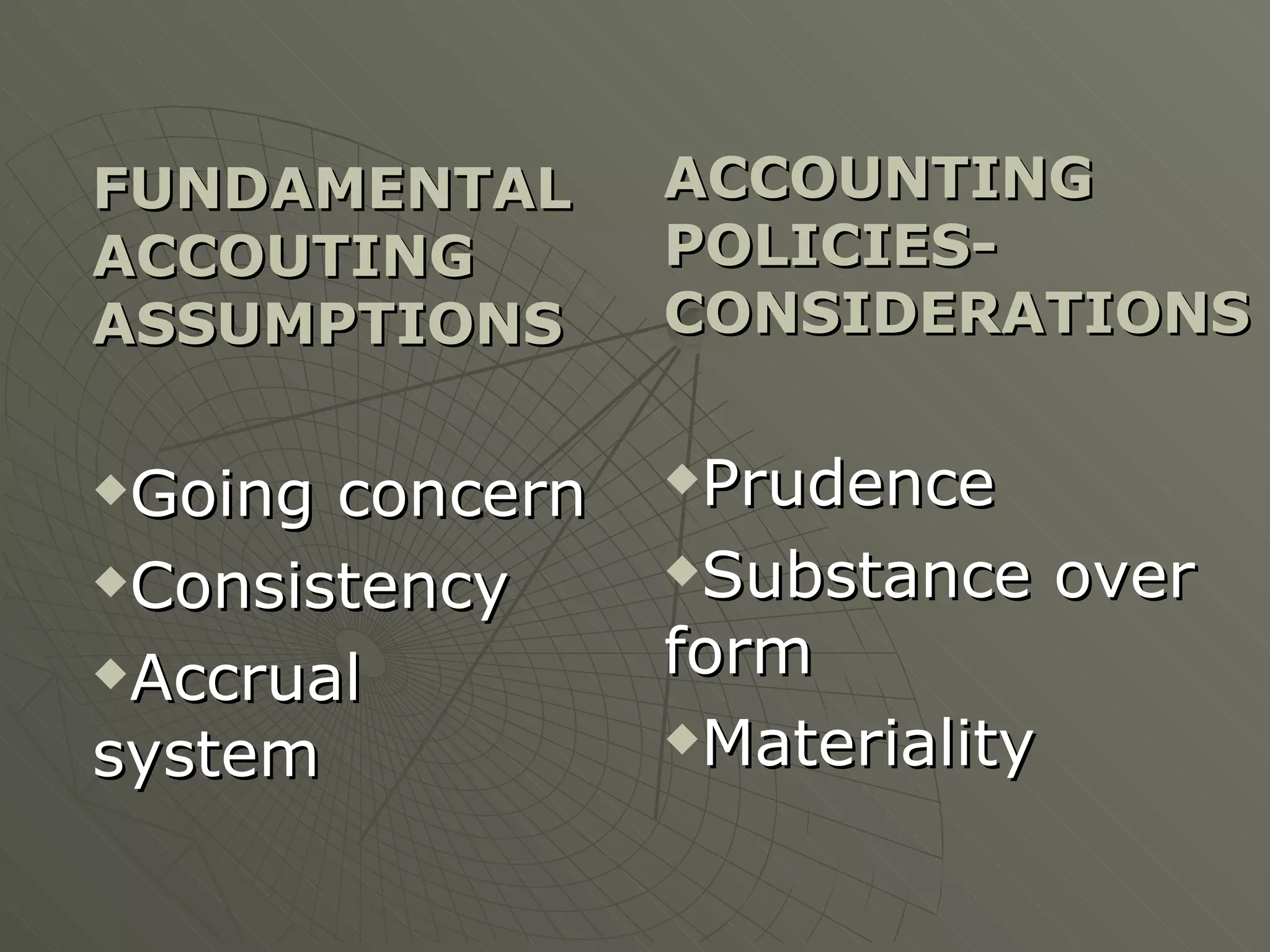

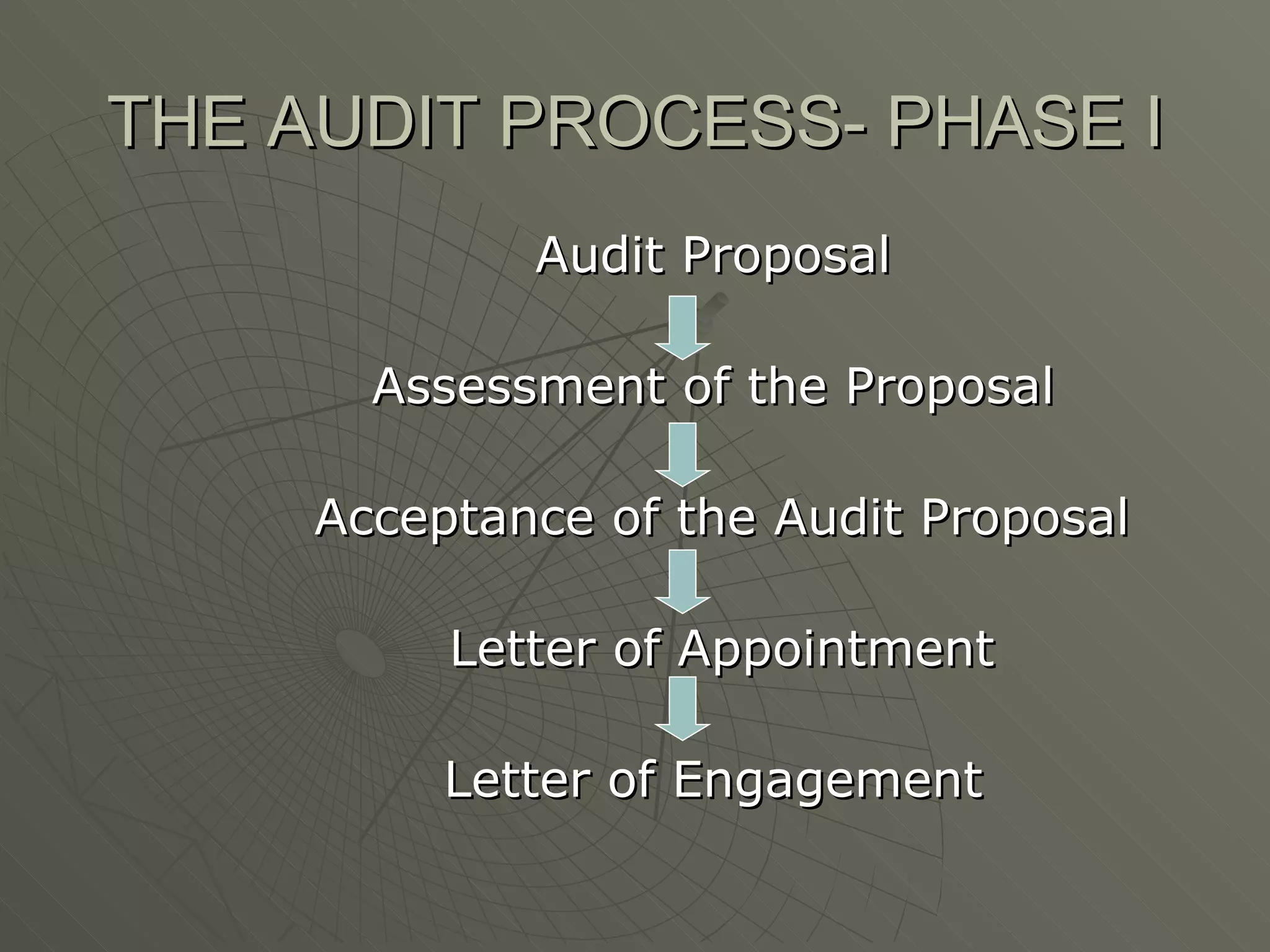

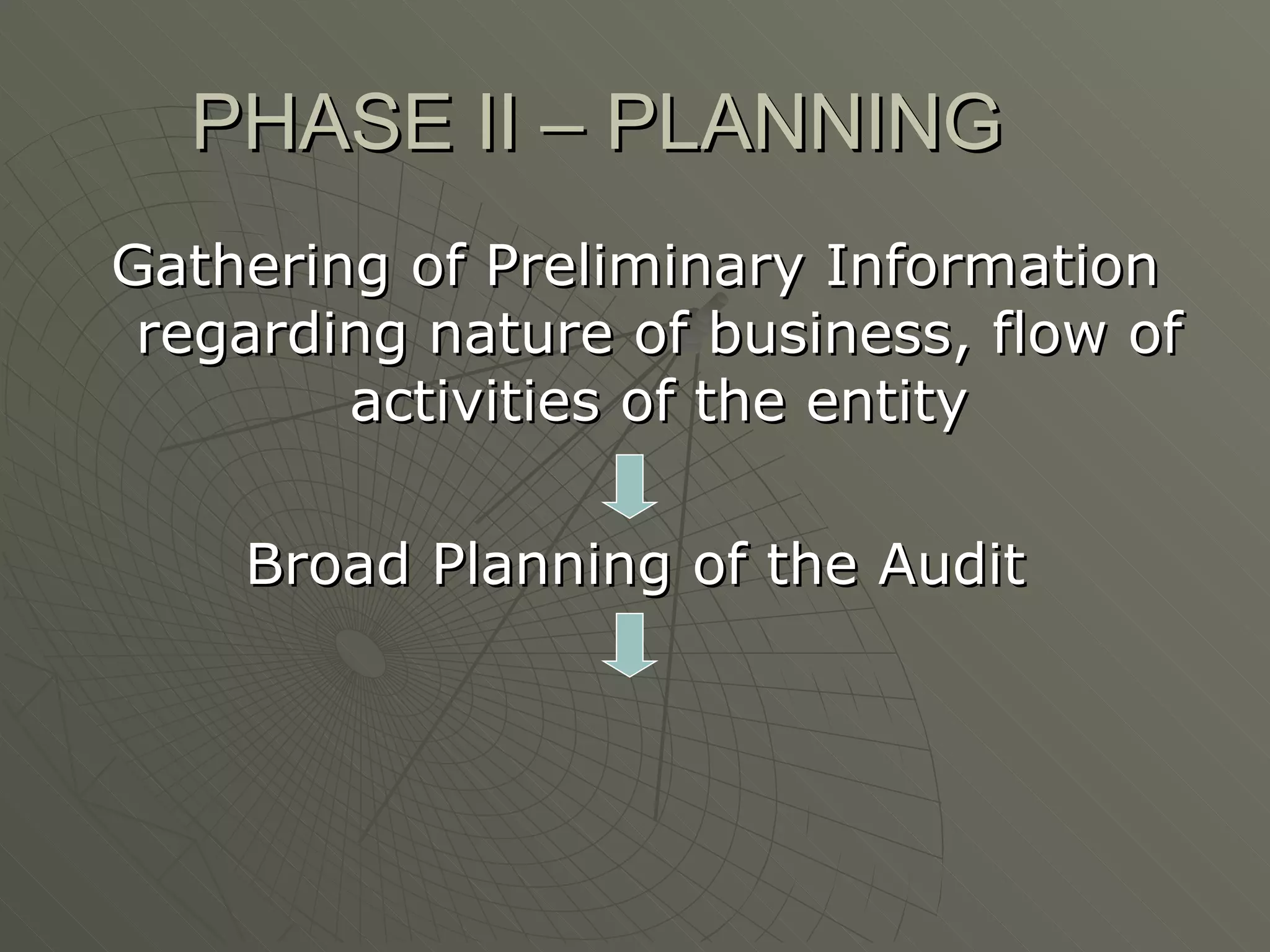

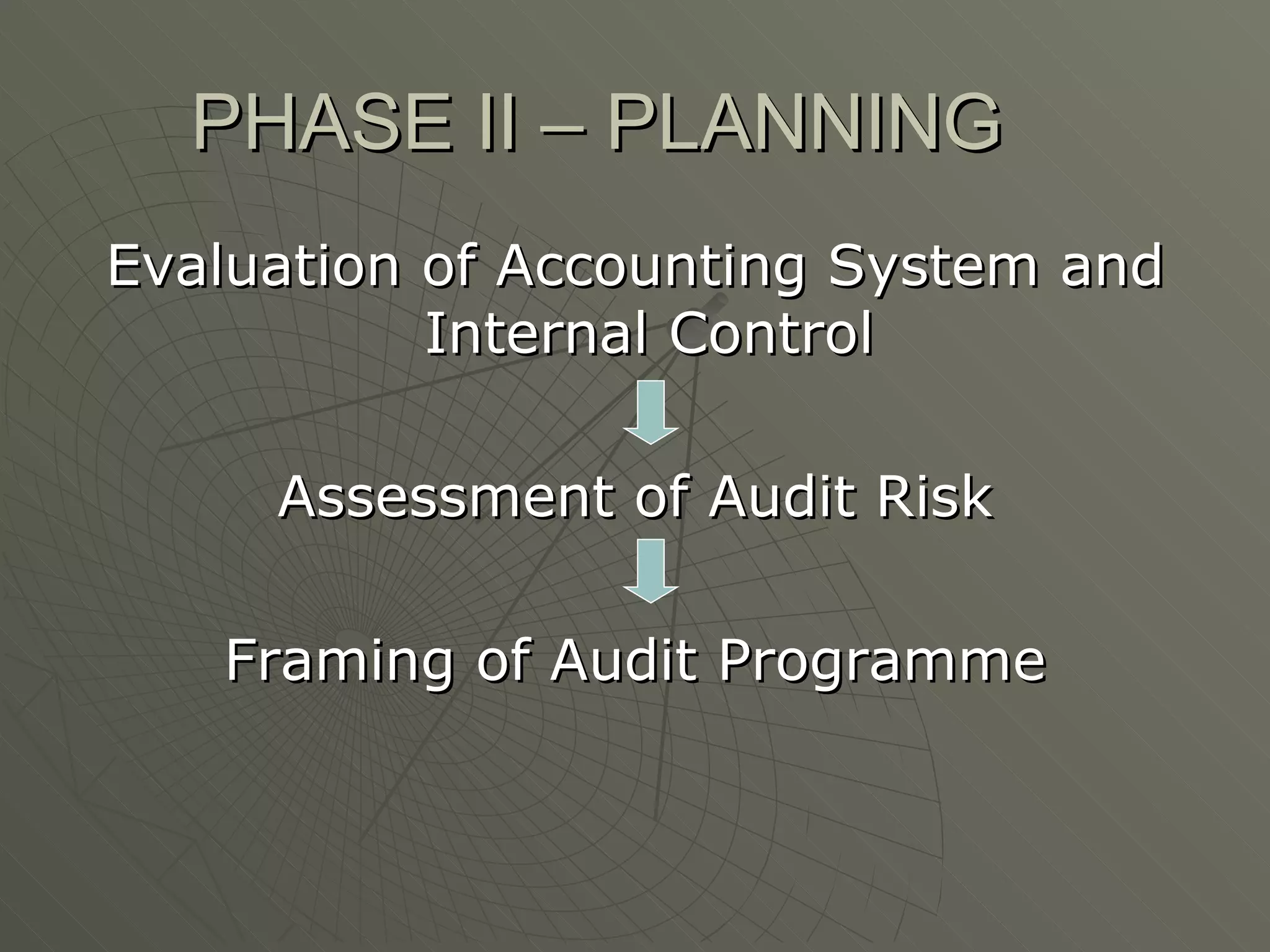

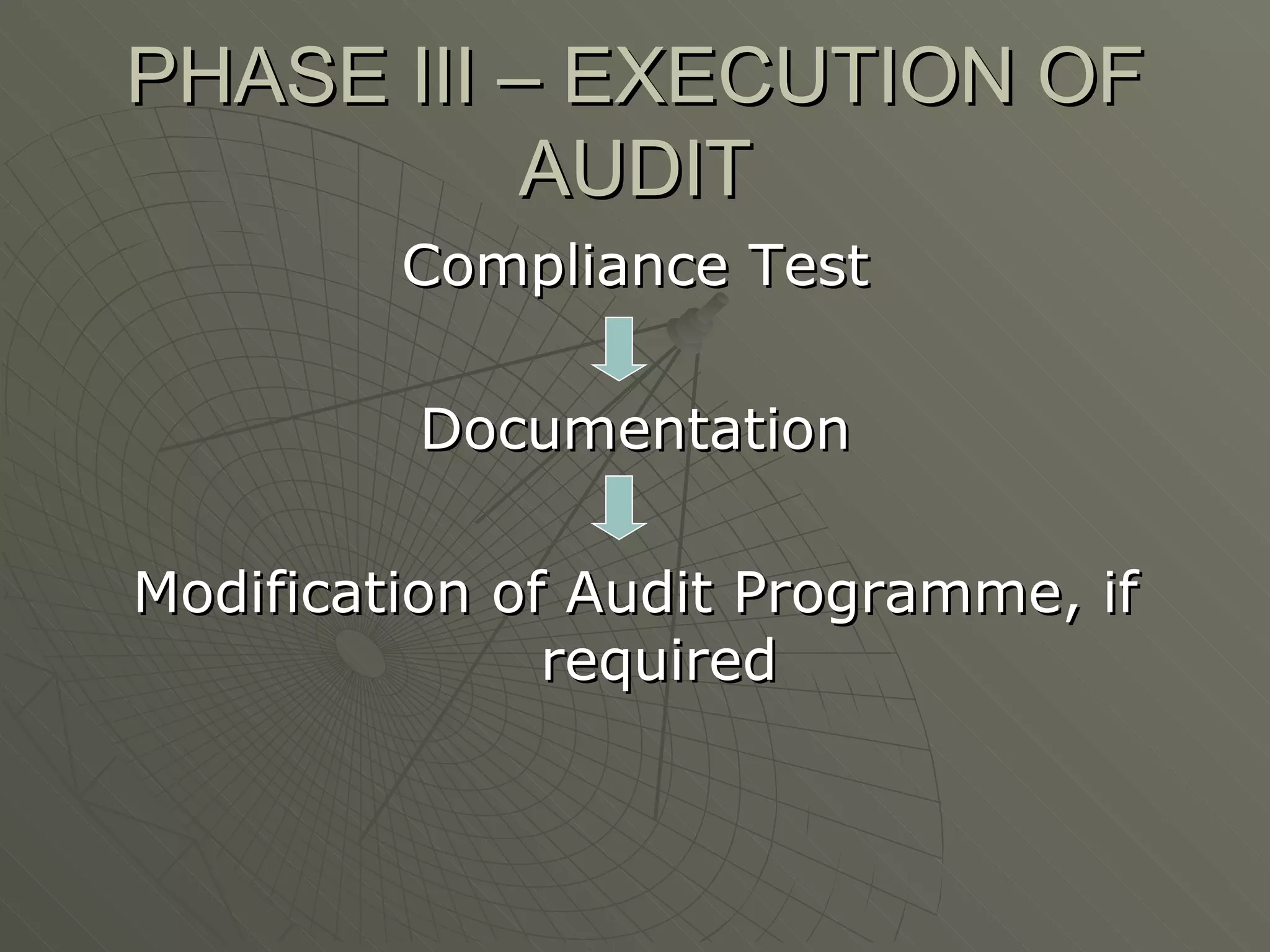

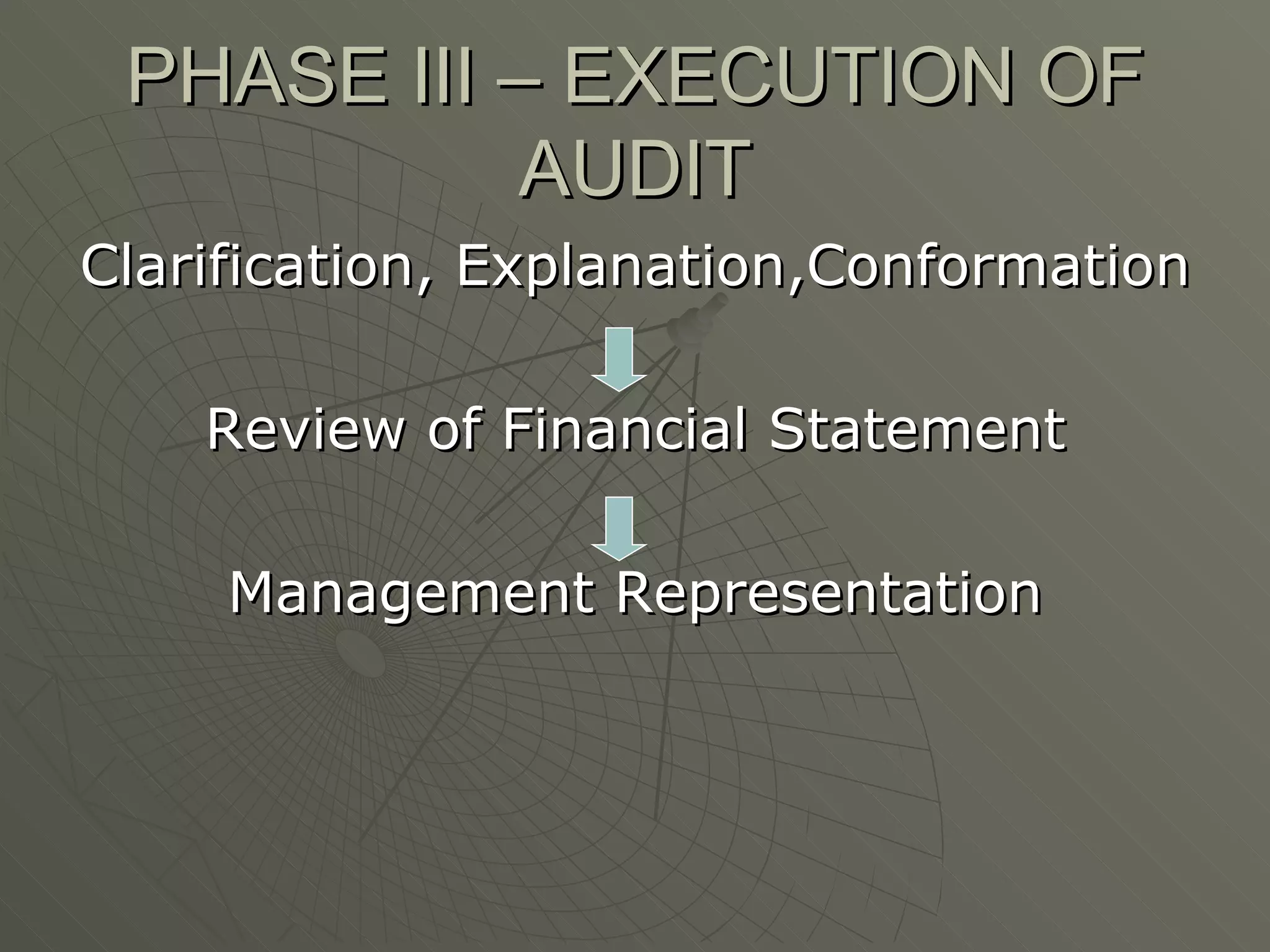

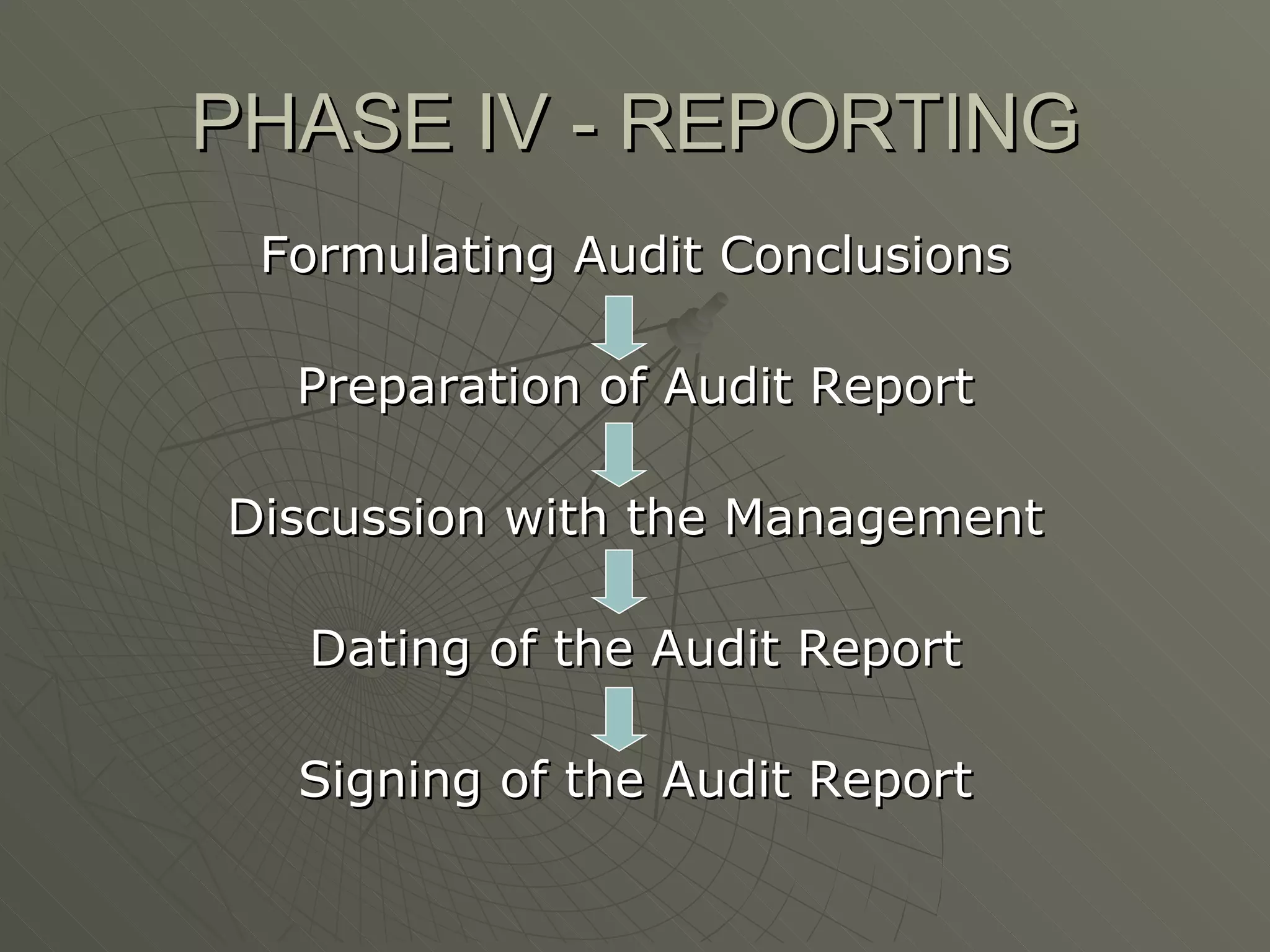

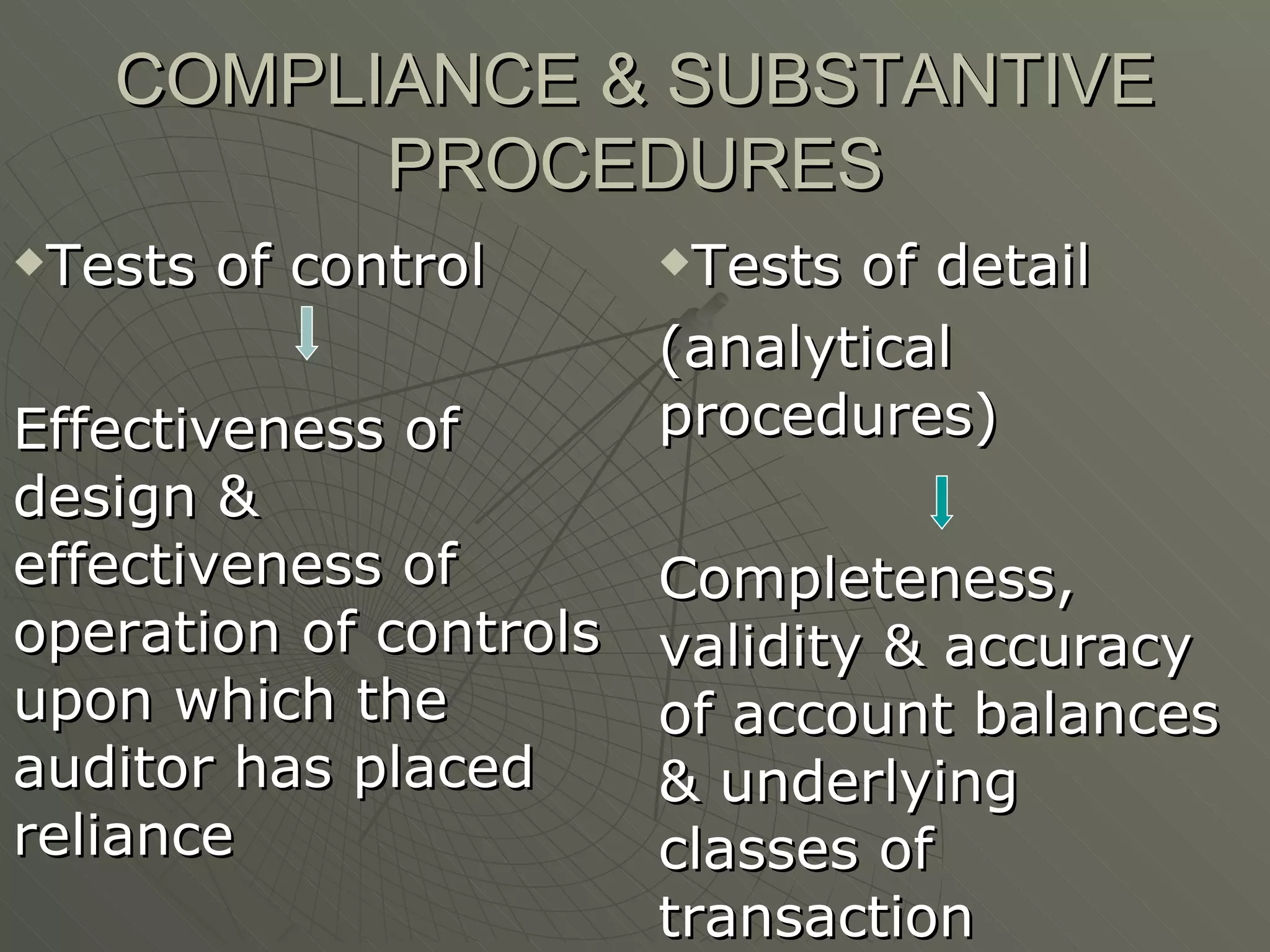

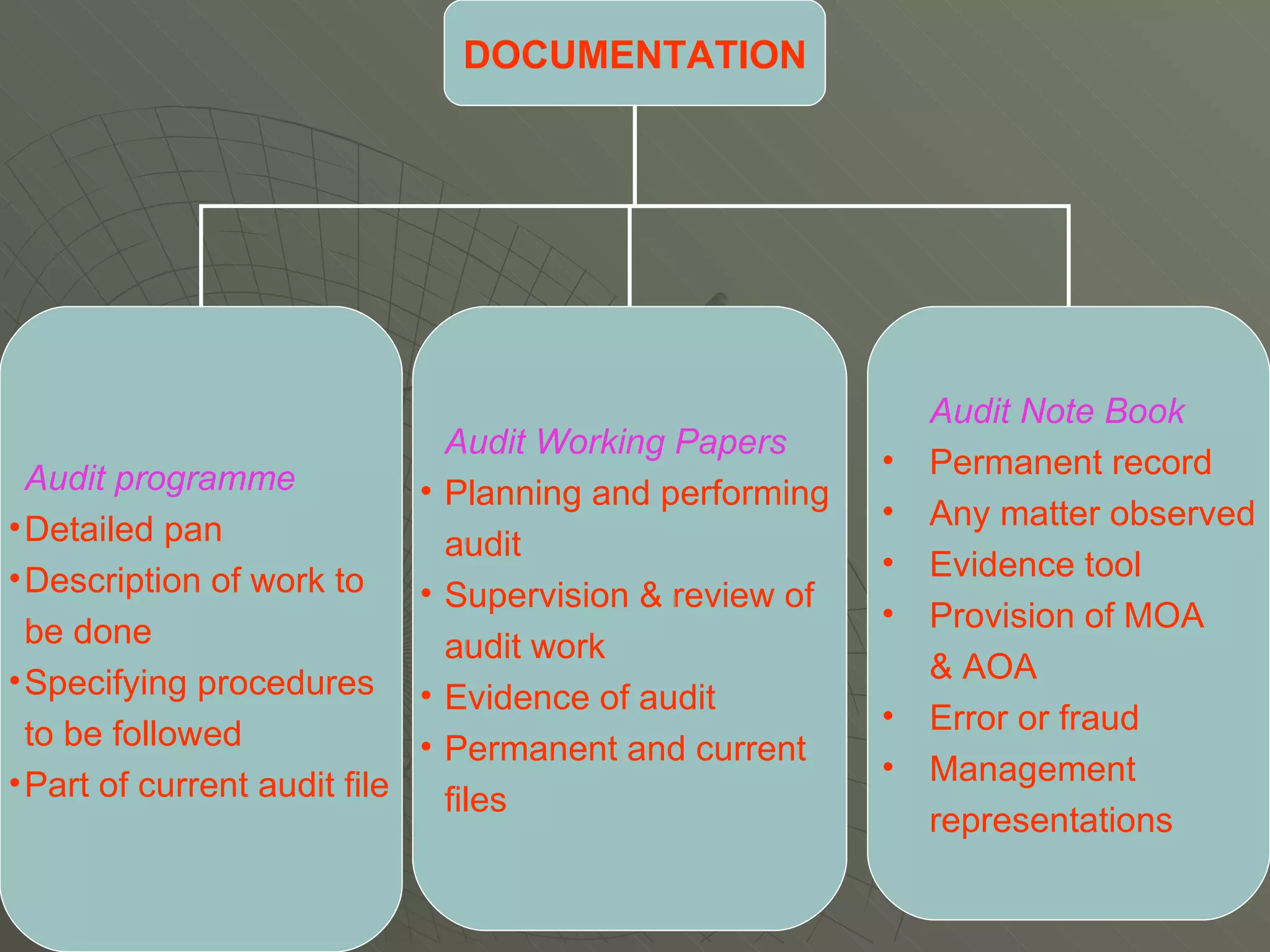

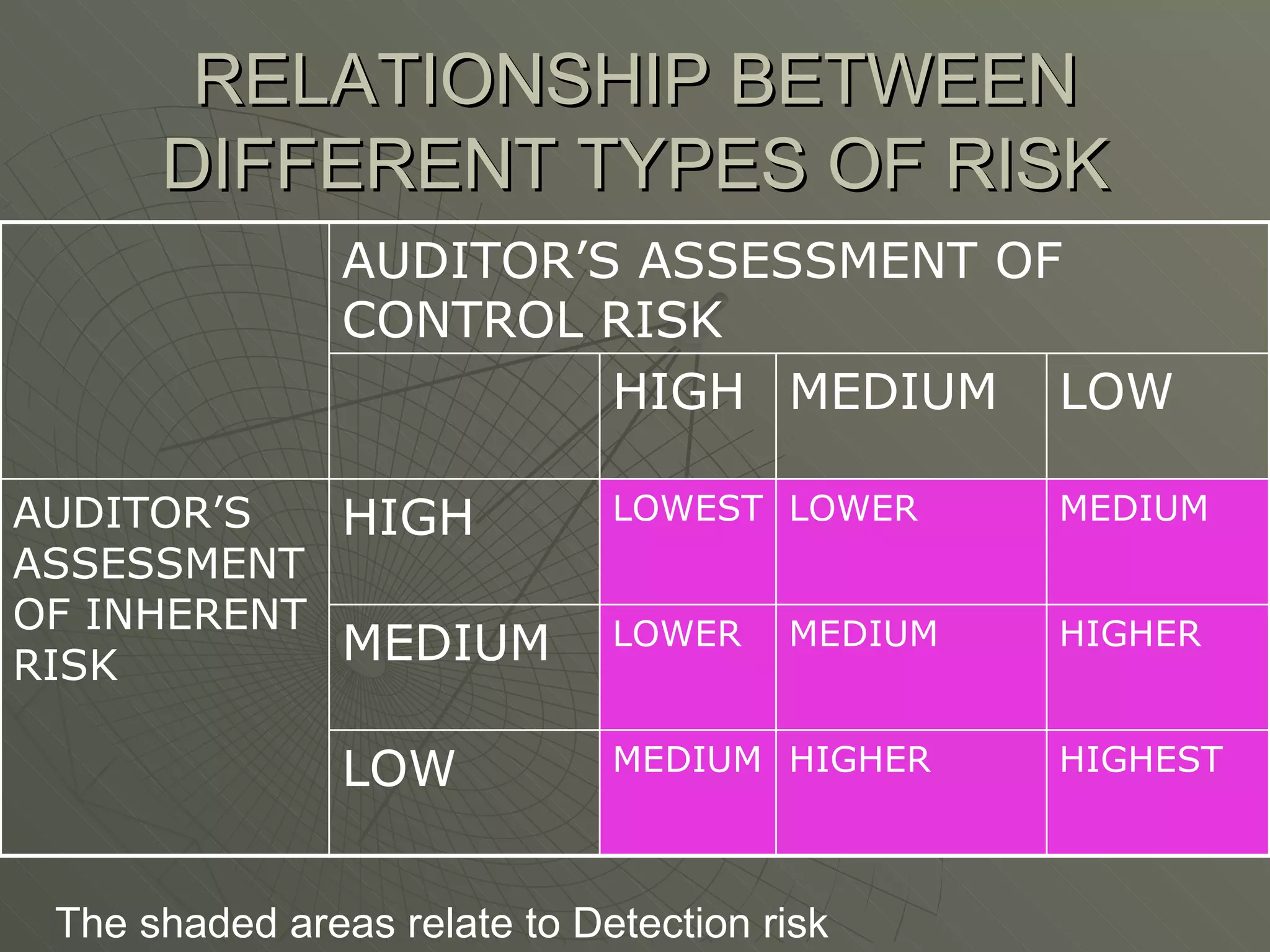

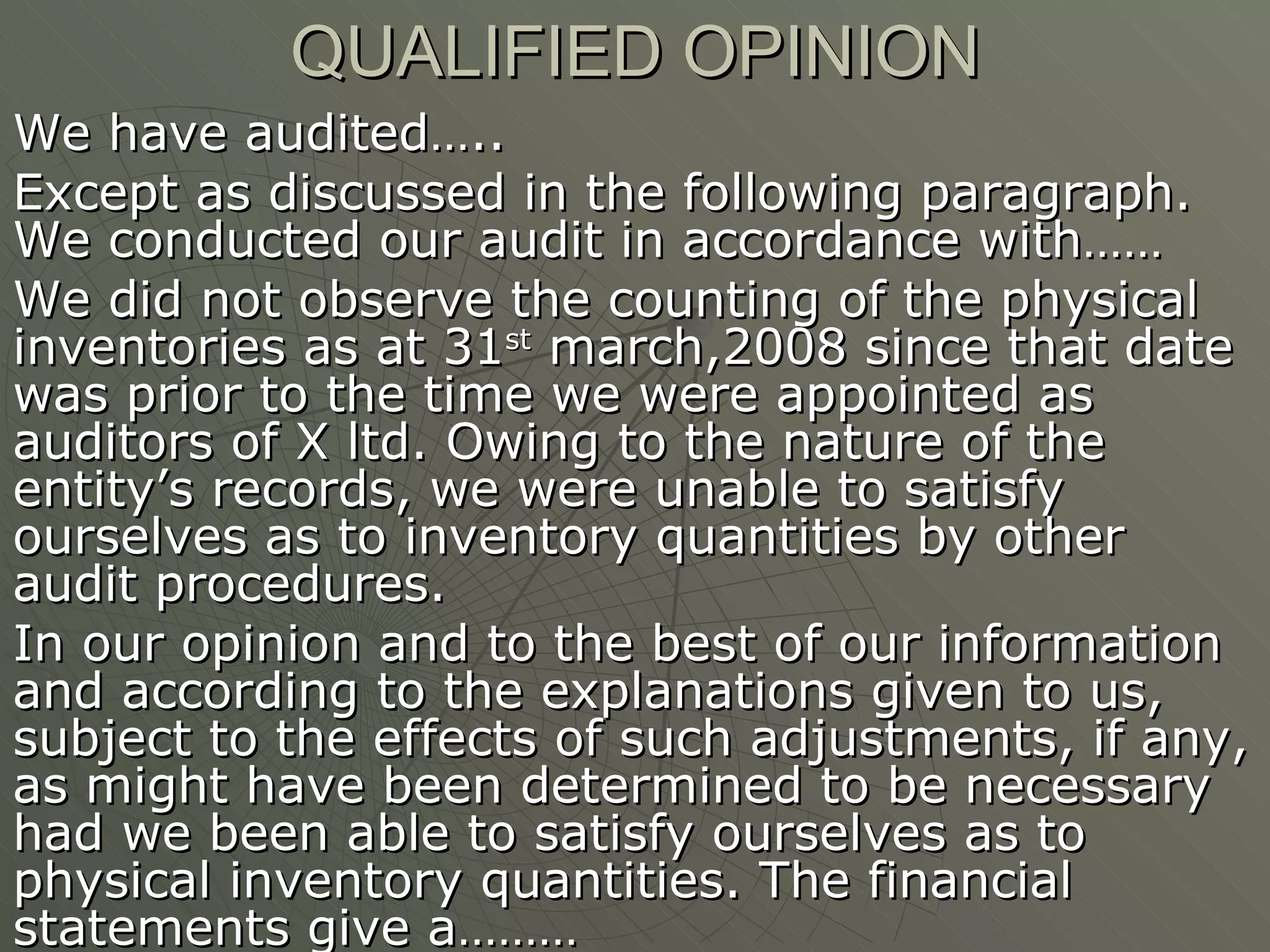

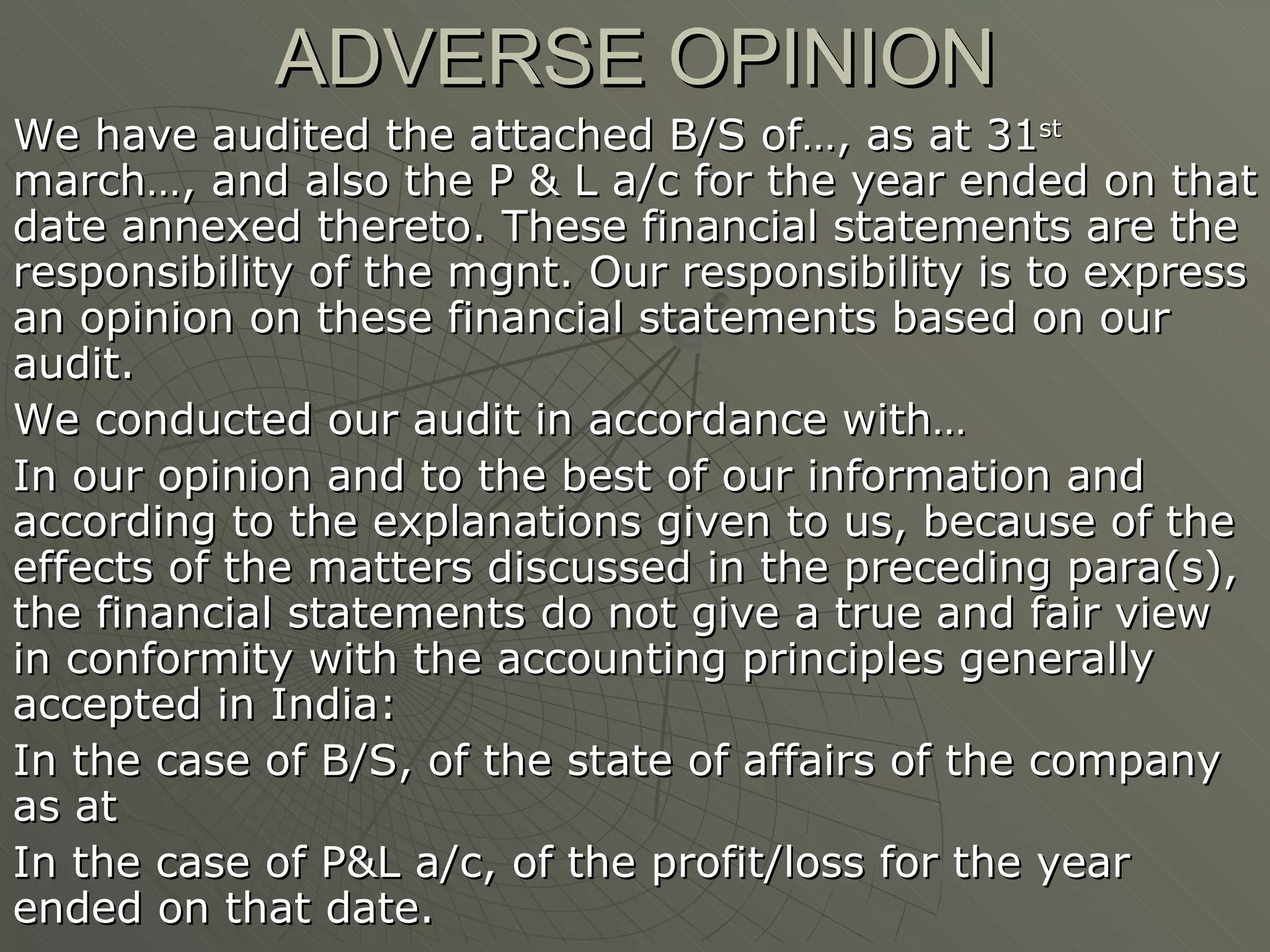

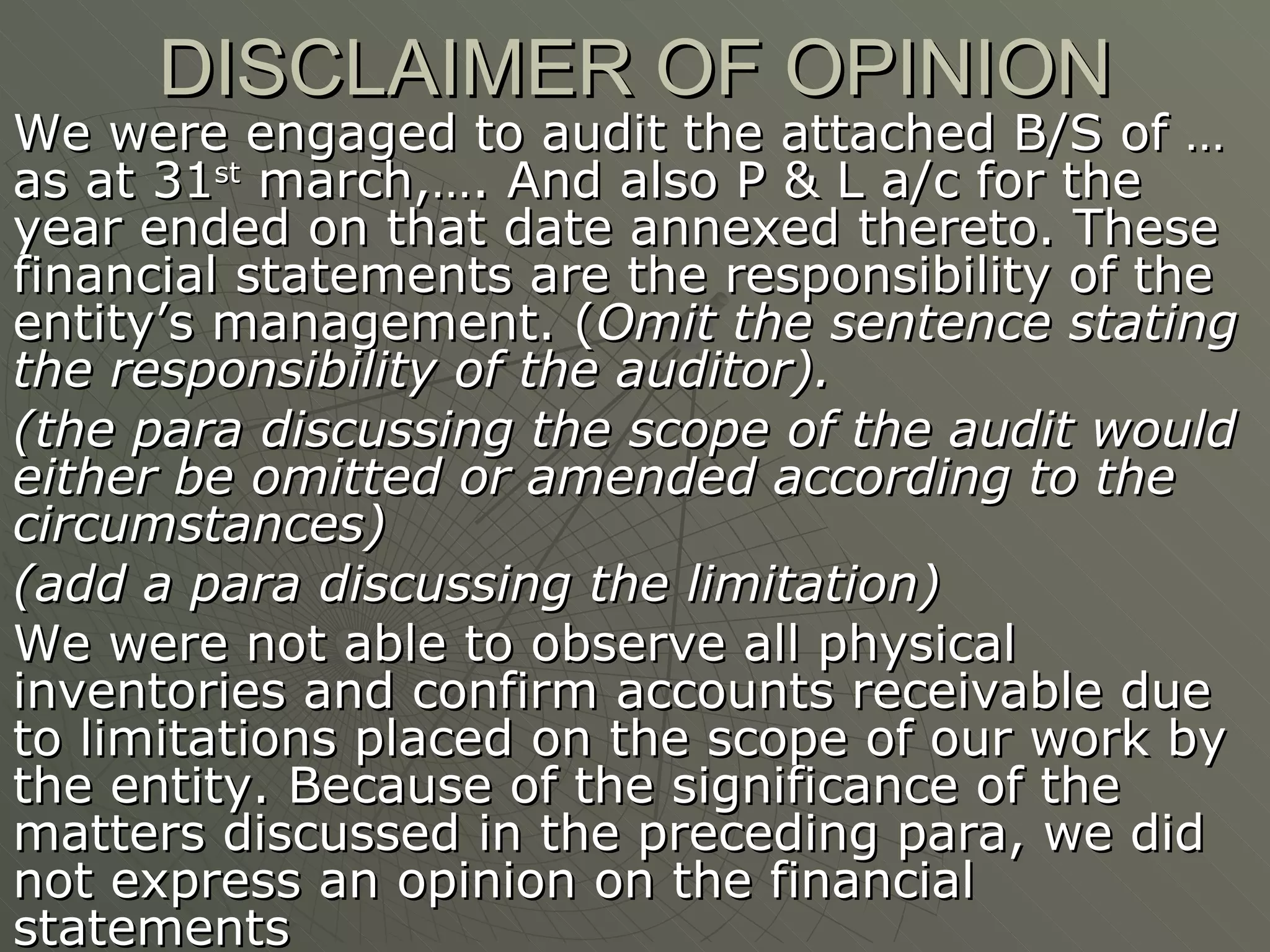

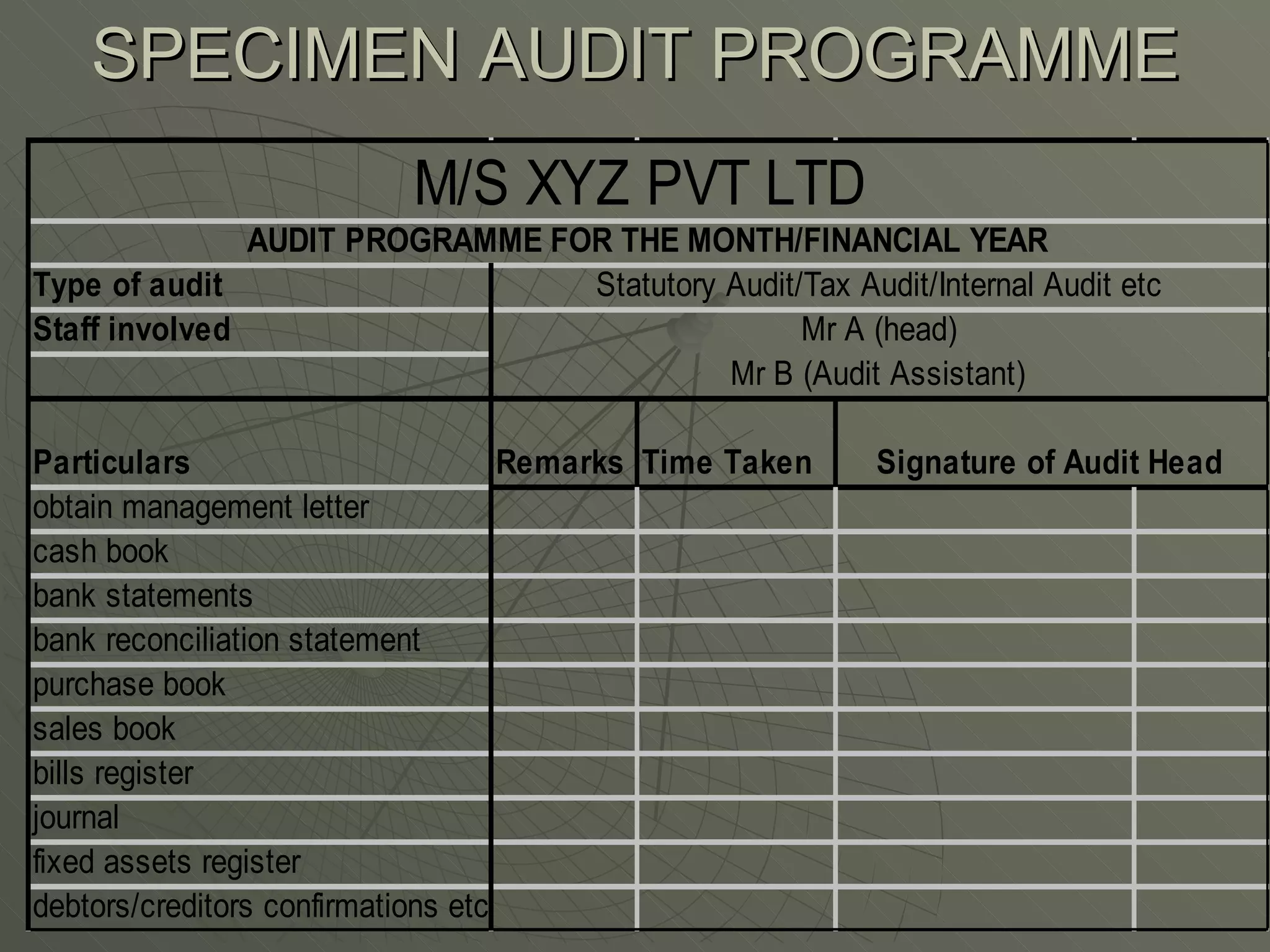

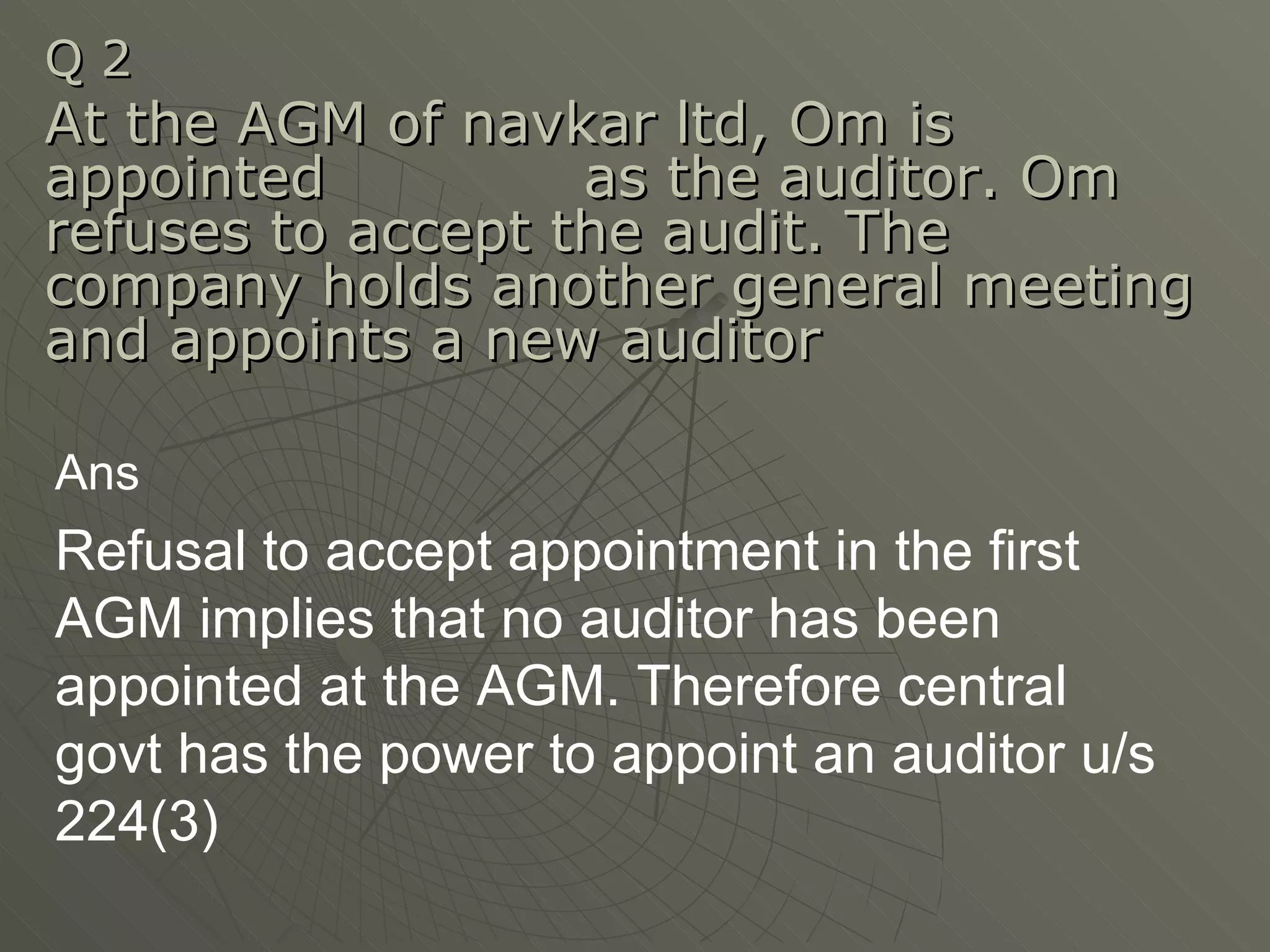

The document discusses the audit process in four phases - planning, execution, reporting, and compliance and substantive procedures. It covers the basic principles of auditing like integrity, objectivity, independence. It also discusses audit risk, documentation, auditor's report and qualifications in reports.

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (2).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites2-251124191348-c246988b-thumbnail.jpg?width=640&height=640&fit=bounds)