Downloaded 2,894 times

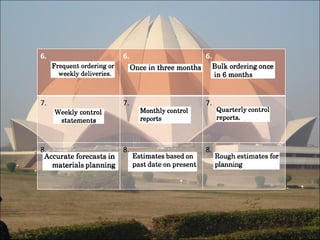

ABC analysis is a method for inventory management that categorizes inventory items into three classes - A, B, and C - based on their value and consumption. Class A items account for the highest monetary value or consumption but represent a small percentage of total items. These require the most attention and tight controls. Class B items are intermediate in value and consumption, while Class C items have low value or consumption but represent the largest percentage of total items, requiring the least amount of management attention. ABC analysis helps businesses prioritize their resources for optimal inventory management.