Download as PDF, PPTX

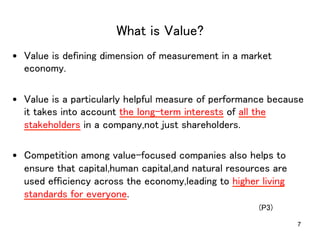

This document summarizes key points from a valuation seminar in Japanese. It discusses various topics related to valuation including foundations of value, core valuation techniques, intrinsic value and the stock market, and managing for value. Some of the main points discussed include defining value, the relationship between growth, return on invested capital and value, discounted cash flow models, and how companies can create value through strategic portfolio management, performance management, mergers and acquisitions, and capital structure decisions.