Downloaded 155 times

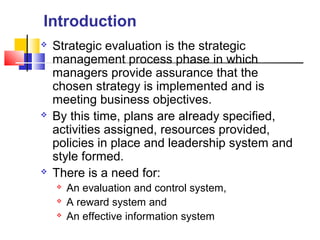

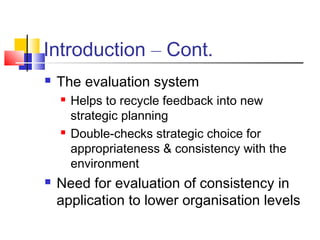

This document discusses strategy evaluation and control. It outlines that strategic evaluation assesses whether the chosen strategy is being implemented and meeting objectives. There needs to be an evaluation system, reward system, and effective information system. Evaluation should happen at different organizational levels and determine if modifications are needed. Criteria for evaluation can include quantitative factors like financial results compared to history and competitors, as well as qualitative factors like consistency with objectives and environmental assumptions. Feedback is used to determine causes of deviations and take corrective action.