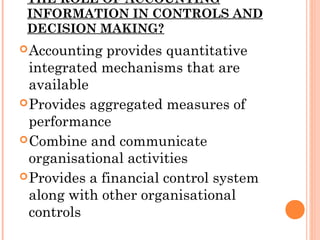

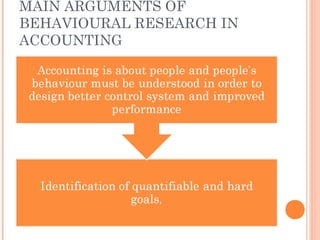

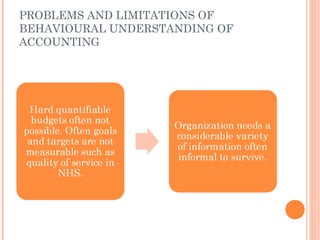

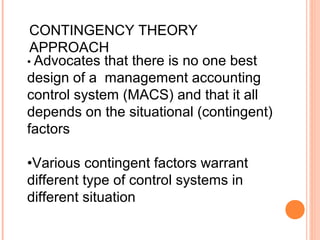

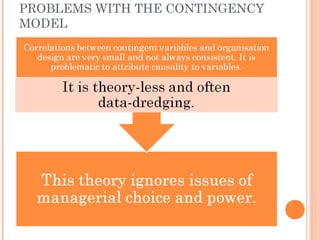

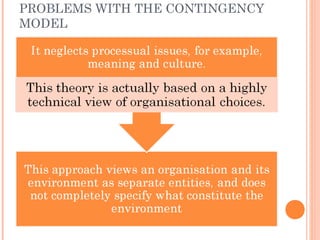

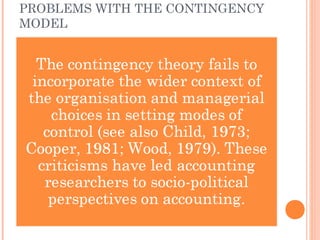

Management accounting provides information internally to help managers make better decisions and improve efficiency. It focuses on control through rational decision making processes like setting strategies, budgets, and evaluating performance. However, behavioral research shows accounting must consider human and organizational factors. Contingency theory states the best accounting system depends on situational factors like a firm's environment, strategy, and technology. While contingency theory aims to make accounting more contextual, it has limitations like oversimplifying relationships and failing to consider all relevant contingencies.