Downloaded 27 times

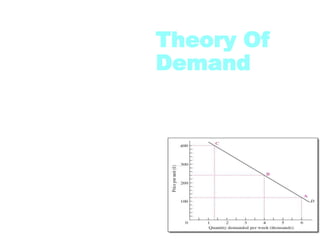

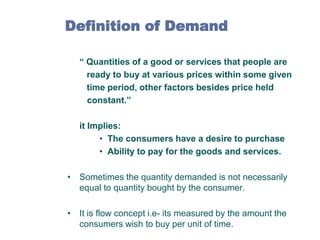

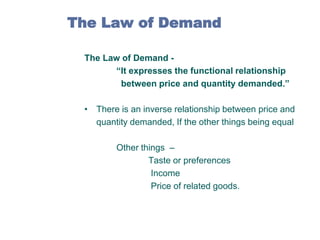

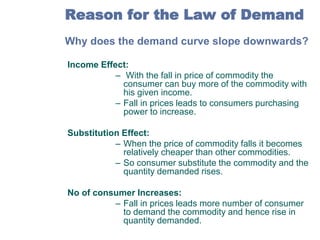

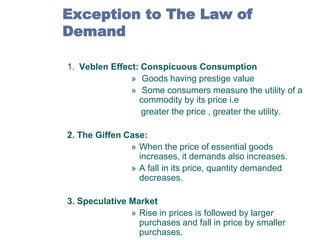

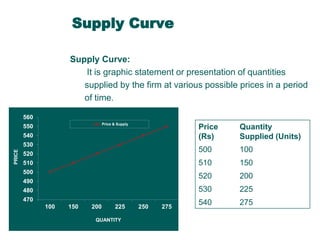

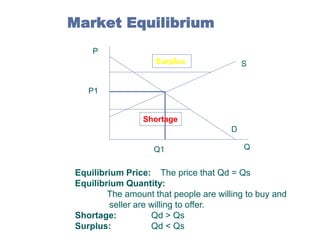

1) The document discusses the theory of demand and supply. It defines demand as the quantities of a good that consumers are willing and able to purchase at various prices. Supply is defined as the quantities of a good that producers are willing to offer for sale at various prices. 2) The law of demand states that, other things remaining constant, as price increases, quantity demanded decreases. The law of supply states that as price increases, quantity supplied also increases. 3) Market equilibrium occurs where quantity demanded equals quantity supplied. This establishes an equilibrium price where markets clear without surplus or shortage.