1. Market Outlook

India Research

May 21, 2010

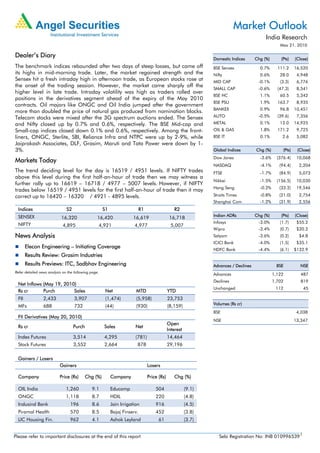

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The benchmark indices rebounded after two days of steep losses, but came off BSE Sensex 0.7% 111.2 16,520

its highs in mid-morning trade. Later, the market regained strength and the Nifty 0.6% 28.0 4,948

Sensex hit a fresh intraday high in afternoon trade, as European stocks rose at MID CAP -0.1% (3.3) 6,776

the onset of the trading session. However, the market came sharply off the

SMALL CAP -0.6% (47.3) 8,541

higher level in late trade. Intraday volatility was high as traders rolled over

BSE HC 1.1% 60.5 5,342

positions in the derivatives segment ahead of the expiry of the May 2010

BSE PSU 1.9% 163.7 8,935

contracts. Oil majors like ONGC and Oil India jumped after the government

BANKEX 0.9% 96.8 10,451

more than doubled the price of natural gas produced from nomination blocks.

Telecom stocks were mixed after the 3G spectrum auctions ended. The Sensex AUTO -0.5% (39.6) 7,356

and Nifty closed up by 0.7% and 0.6%, respectively. The BSE Mid-cap and METAL 0.1% 12.0 14,925

Small-cap indices closed down 0.1% and 0.6%, respectively. Among the front- OIL & GAS 1.8% 171.2 9,725

liners, ONGC, Sterlite, SBI, Reliance Infra and NTPC were up by 2-9%, while BSE IT 0.1% 2.6 5,082

Jaiprakash Associates, DLF, Grasim, Maruti and Tata Power were down by 1-

3%. Global Indices Chg (%) (Pts) (Close)

Dow Jones -3.6% (376.4) 10,068

Markets Today

NASDAQ -4.1% (94.4) 2,204

The trend deciding level for the day is 16519 / 4951 levels. If NIFTY trades FTSE -1.7% (84.9) 5,073

above this level during the first half-an-hour of trade then we may witness a

Nikkei -1.5% (156.5) 10,030

further rally up to 16619 – 16718 / 4977 – 5007 levels. However, if NIFTY

Hang Seng -0.2% (33.2) 19,546

trades below 16519 / 4951 levels for the first half-an-hour of trade then it may

correct up to 16420 – 16320 / 4921 - 4895 levels. Straits Times -0.8% (21.0) 2,754

Shanghai Com -1.2% (31.9) 2,556

Indices S2 S1 R1 R2

SENSEX Indian ADRs Chg (%) (Pts) (Close)

16,320 16,420 16,619 16,718

Infosys -3.0% (1.7) $55.2

NIFTY 4,895 4,921 4,977 5,007

Wipro -3.4% (0.7) $20.2

News Analysis Satyam -3.6% (0.2) $4.8

ICICI Bank -4.0% (1.5) $35.1

Elecon Engineering – Initiating Coverage

HDFC Bank -4.4% (6.1) $132.9

Results Review: Grasim Industries

Results Previews: ITC, Sadbhav Engineering Advances / Declines BSE NSE

Refer detailed news analysis on the following page.

Advances 1,122 487

Declines 1,702 819

Net Inflows (May 19, 2010)

Unchanged 112 45

Rs cr Purch Sales Net MTD YTD

FII 2,433 3,907 (1,474) (5,958) 23,753

Volumes (Rs cr)

MFs 688 732 (44) (930) (8,159)

BSE 4,038

FII Derivatives (May 20, 2010)

NSE 13,347

Open

Rs cr Purch Sales Net

Interest

Index Futures 3,514 4,295 (781) 14,464

Stock Futures 3,552 2,664 878 29,196

Gainers / Losers

Gainers Losers

Company Price (Rs) Chg (%) Company Price (Rs) Chg (%)

OIL India 1,260 9.1 Educomp 504 (9.1)

ONGC 1,118 8.7 HDIL 220 (4.8)

Indusind Bank 196 8.6 Jain Irrigation 916 (4.5)

Piramal Health 570 8.5 Bajaj Finserv. 452 (3.8)

LIC Housing Fin. 962 4.1 Ashok Leyland 61 (3.7)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 0109965391

2. Market Outlook | India Research

Elecon Engineering – Initiating Coverage

Elecon Engineering (EEC) is a leading and experienced Material Handling Equipment

(MHE) turnkey solutions and Gear provider for the core sectors of the economy such as

Power, Steel and Infra. Additionally, over the years, the company has built a strong

domain expertise in coal-handling. Hence, we believe that EEC is well placed to capitalise

on the burgeoning industrial capex (that majorly comprises of power). We estimate the

company to register a CAGR of 13.5% in Sales and of 37% in Adj. Profit over FY2010-12E.

At Rs79, the stock is trading at attractive valuations of 7.7x FY2012E Earnings and 5x

FY2012E EV/EBITDA. We Initiate Coverage on the stock, with a Buy recommendation and

Target Price of Rs102.

Recovery augurs well for the Sector: We expect industrial capex to revert back to the growth

path, with the economy reviving (indicated by the improvement in the IIP), the continuous

government focus on infrastructure spend, and a pick up in private capex. The Domestic

MHE Industry (Rs5,700cr in FY2009) has a strong correlation with industrial growth. As per

Crisil Research, overall emerging opportunities in the MHE Industry are estimated to be

around Rs32,500cr over FY2009-12E. This augurs well for MHE solution players like EEC.

The near-term growth for the MHE companies is expected to be driven by high capex likely

to be incurred in the core sectors of Power and Steel (Rs25,500cr).

Improving financials: We estimate EEC to post a CAGR of 13.5% in its Revenues over

FY2010-12E. The OPMs are expected to remain stable at the current levels of 15%. We

believe that due to a strong correction in the commodity prices and easing of the working

capital cycle, EEC’s net working capital would start aligning with the historical average and

stand reduced. Overall, this is likely to de-leverage the company’s Balance Sheet and

lower its Interest outflow, improving the overall Profitability. We expect a CAGR of 37% in

the Adj. PAT over FY2010-12E, as against the 13% CAR decline witnessed during FY2008-

10. We expect the RoCE and RoE to improve from 15% and 17% in FY2010, to 21% and

23% in FY2012E, respectively.

Grasim Industries - 4QFY2010 Result Review

Grasim Industries’ (Grasim) 4QFY2010 consolidated net revenue grew by 10.8% yoy to

Rs5,475cr (Rs4,942cr). The cement business clocked a 5.2% yoy growth in net sales to

Rs4,162cr (Rs3,956cr), aided by a 9% increase in sale volumes to 10.36 mn tonnes. The

VSF division’s net sales grew by a robust 65% to Rs1,045cr (Rs634cr), aided by a 31%

growth in volumes and a 29% growth in realisations. The operating profit of the company

rose by a substantial 11.5% yoy to Rs1,433cr, primarily on account of an excellent

performance from the VSF division. The operating margins of the VSF division grew by a

whopping 1,810bp yoy to 34.3% (16.2%). The company’s consolidated net profit grew by

15.1% to Rs654.5cr (Rs568.8cr) during the quarter. We maintain an Accumulate on the

stock.

4QFY2010 Result Previews

ITC

ITC is expected to announce its 4QFY2010 results. For the quarter, we expect ITC to report

a 21% yoy growth in its Top-line to Rs4,708cr, on the back of price hikes across its

portfolio (after 10-18% Excise duty hike for filter cigarettes exceeding 60mm length this

Budget), and steady Cigarette Volumes (factoring in a ~2% volume growth for the

quarter). ITC's Earnings are expected to grow by a strong 33% yoy, aided by Top-line

growth (up-tick in Hotel Revenue) and Margin expansion. At the operating front, the

company is expected to report a margin expansion of 146bp. We maintain a Buy on the

stock, with a Target Price of Rs300.

May 21, 2010 2

3. Market Outlook | India Research

Sadbhav Engineering

Sadbhav Engineering (SEL) is expected to announce its 4QFY2010 results today. We expect

SEL to register a Top-line growth of 40.4% to Rs560cr. On the operating margin front, we

expect margins to be strong at 11.0%. The Net profit for the quarter is expected to register

a growth of 13.3% to Rs32.9cr. In the backdrop of the rich valuations that the Stock trades

at, we maintain our Neutral view.

Economic and Political News

Govt. likely to raise power tariff: Power Minister

India to launch oil block auctions in FY11: Official

TRAI to complete consultation on 3G-2G price-linking by July 15, 2010

Corporate News

RIL halts some KG output as cyclone approaches

Panacea vaccine gets clean chit from WHO

JSPL to acquire Oman steel firm for US $464mn

ICICI-BoR deal faces Government hurdle

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Dolphin Offshore Dividend, Results

Edelweiss Capital Dividend, Results

Gammon Infrastructure Results

Garware Offshore Dividend, Results

Inox Dividend, Results

ITC Dividend, Results

Jyoti Structures Results

Sadbhav Engineering Dividend, Results

Varun Shipping Dividend, Results

Zylog Systems Dividend, Results

May 21, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in

this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem

necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and

risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that

are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the

company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be

true, and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document.

Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed

on, directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory

services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with

the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

May 21, 2010 4