Call Girls Near Golden Tulip Essential Hotel, New Delhi 9873777170

Market outlook 01 06-10

1. Market Outlook

India Research

June 1, 2010

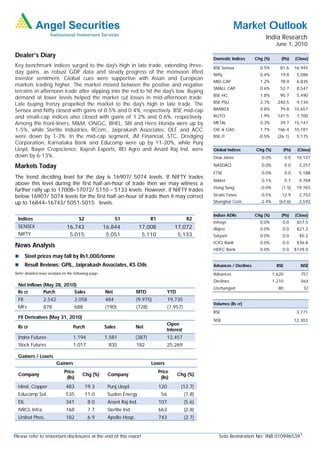

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

Key benchmark indices surged to the day's high in late trade, extending three- BSE Sensex 0.5% 81.6 16,945

day gains, as robust GDP data and steady progress of the monsoon lifted Nifty 0.4% 19.8 5,086

investor sentiment. Global cues were supportive with Asian and European

MID CAP 1.2% 78.9 6,835

markets trading higher. The market moved between the positive and negative

SMALL CAP 0.6% 52.7 8,547

terrains in afternoon trade after slipping into the red to hit the day's low. Buying

BSE HC 1.8% 95.7 5,490

demand at lower levels helped the market cut losses in mid-afternoon trade.

Late buying frenzy propelled the market to the day's high in late trade. The BSE PSU 2.7% 240.5 9,134

Sensex and Nifty closed with gains of 0.5% and 0.4%, respectively. BSE mid-cap BANKEX 0.8% 79.8 10,657

and small-cap indices also closed with gains of 1.2% and 0.6%, respectively. AUTO 1.9% 141.5 7,700

Among the front-liners, M&M, ONGC, BHEL, SBI and Hero Honda were up by METAL 0.3% 39.7 15,147

1-5%, while Sterlite Industries, RCom., Jaiprakash Associates, DLF and ACC OIL & GAS 1.7% 166.4 10,181

were down by 1-3%. In the mid-cap segment, JM Financial, STC, Dredging BSE IT -0.5% (26.1) 5,175

Corporation, Karnataka Bank and Educomp were up by 11-20%, while Punj

Lloyd, Bayer Cropscience, Rajesh Exports, REI Agro and Anant Raj Ind. were Global Indices Chg (%) (Pts) (Close)

down by 6-13%. Dow Jones 0.0% 0.0 10,137

Markets Today NASDAQ 0.0% 0.0 2,257

FTSE 0.0% 0.0 5,188

The trend deciding level for the day is 16907/ 5074 levels. If NIFTY trades

Nikkei 0.1% 5.7 9,769

above this level during the first half-an-hour of trade then we may witness a

Hang Seng -0.0% (1.5) 19,765

further rally up to 17008–17072/ 5110 – 5133 levels. However, if NIFTY trades

below 16907/ 5074 levels for the first half-an-hour of trade then it may correct Straits Times 0.5% 12.9 2,753

up to 16844–16743/ 5051-5015 levels. Shanghai Com -2.4% (63.6) 2,592

Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2

Infosys 0.0% 0.0 $57.5

SENSEX 16,743 16,844 17,008 17,072 Wipro 0.0% 0.0 $21.2

NIFTY 5,015 5,051 5,110 5,133 Satyam 0.0% 0.0 $5.2

ICICI Bank 0.0% 0.0 $36.8

News Analysis

HDFC Bank 0.0% 0.0 $139.0

Steel prices may fall by Rs1,000/tonne

Result Reviews: GPIL, Jaiprakash Associates, KS Oils Advances / Declines BSE NSE

Refer detailed news analysis on the following page. Advances 1,620 751

Declines 1,210 564

Net Inflows (May 28, 2010)

Unchanged 80 32

Rs cr Purch Sales Net MTD YTD

FII 2,542 2,058 484 (9,975) 19,735

Volumes (Rs cr)

MFs 878 688 (190) (728) (7,957)

BSE 3,771

FII Derivatives (May 31, 2010)

NSE 12,303

Open

Rs cr Purch Sales Net

Interest

Index Futures 1,194 1,581 (387) 12,457

Stock Futures 1,017 835 182 25,269

Gainers / Losers

Gainers Losers

Price Price

Company Chg (%) Company Chg (%)

(Rs) (Rs)

Hind. Copper 483 19.3 Punj Lloyd 120 (12.7)

Educomp Sol. 535 11.0 Suzlon Energy 56 (7.8)

EIL 341 8.0 Anant Raj Ind. 107 (5.6)

IVRCL Infra. 168 7.7 Sterlite Ind. 663 (2.8)

United Phos. 182 6.9 Apollo Hosp. 743 (2.7)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 0109965391

2. Market Outlook | India Research

Steel prices may fall by Rs1,000/tonne

According to steel secretary, steel prices may fall further by another Rs1,000/tonne in June

2010 due to a softening global trend originating from the financial crisis in Europe and

demand slowdown ahead of the monsoons. Last month, many large players reduced long

products prices by Rs1500–2000/tonne, while flat product prices were cut by Rs1000–

1500/tonne. We believe this will narrow the gap between domestic prices and import

prices of steel. Price cuts will not materially impact our estimates as our price assumptions

are lower even if the price cut takes place. We continue to maintain our Buy rating on JSW

Steel and Tata Steel.

4QFY2010 Result Reviews

Godawari Power and Ispat (GPIL)

GPIL’s consolidated 4QFY2010 results were in line with our estimates. Net revenue grew

by 21.3% yoy to Rs238.5cr during the quarter, against our estimate of Rs237.3cr. Lower

sales volume of sponge iron, HB wire and power was compensated by a) higher sales of

billets, power and ferro alloys and b) higher realisations across segments, except power.

During the quarter, the company also sold 8,473 tonnes of pellet. EBITDA grew by 47.5%

qoq and 136.7% yoy to Rs46.7cr, as margins expanded by 392bp qoq and 955bp yoy to

19.6%. Interest expense and depreciation increased by 68.4% yoy and 17.8% yoy to

Rs10.9cr each during the quarter. Lower tax rate of 10.9%, as compared to 20.8% in

4QFY2009, led to adjusted net income growing by 194% yoy to Rs24.3cr, in line with our

estimate of Rs25cr.

We believe the stock is at an inflection point, as full benefits of the 0.6mn tonne

pelletization plant will be seen in FY2011E and savings of Rs125cr–150cr are expected in

FY2011E. Consequently, earnings are expected to grow at a 78.7% CAGR over FY2010-

12E. We maintain our Buy rating on the stock with a Target Price of Rs309, valuing the

stock at 3.5x FY2012E EV/EBITDA.

Jaiprakash Associates

Jaiprakash Associates reported top-line growth of 60.5% to Rs3,345cr in 4QFY2010. On

the operating profit front, the company reported margin of 25.8%. Bottom-line registered a

yoy decline of 36.7% to Rs244cr.

The company’s sales grew 68% to Rs10,355cr in FY2010, against Rs6,148cr in FY2009.

Net profit stood at Rs 1708cr for FY2010, as compared to Rs 897cr in FY2009, growing

90%. For FY2010, revenue from the cement segment registered growth of 62.7%, while

that from the construction and real estate segments reported growth of 90.9% and 48.1%,

respectively. The stock is under review.

KS Oils

KS Oils’ 4QFY2010 results were below our estimates. Sales for the quarter grew 20% yoy

to Rs1,063cr, against our estimate of Rs1,198cr. During 4QFY2010, the company’s edible

oil segment grew 20% yoy, and the power segment registered growth of 71% yoy. OPM

came in at 11.2%, marginally ahead of our expectation of 11%. For the quarter, EBIT

margin for the edible oil segment contracted by 100bp to 9.8% yoy. Higher depreciation

(61% yoy) and interest costs (103% yoy) led to a decline in overall profit. PAT for the

quarter dropped by 21% yoy to Rs38cr. We currently have a Buy rating on the stock, which

will be revised post the conference call.

June 1, 2010 2

3. Market Outlook | India Research

Economic and Political News

Manufacturing helps GDP grow 7.4% in FY2010

OECD economies expand 0.7% in 1QFY2010

Govt. may soon give its nod for divestment in Coal India and three others

DoT expects Rs 40,000cr from BWA auction

Indian Railways raised iron ore freight cost for exports by Rs300/tonne for June 2010

Tobacco exports surged by 7.4% to 21,659 tonnes in the first month of FY2011

Corporate News

McLeod Russel expects FY2011 tea production at 102mn kgs

NMDC doubles iron ore price supplied to foreign mills

J&K Bank has invested Rs100cr in Lavasa Corporation, a subsidiary of HCC Ltd

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Event for the day

NRB Bearings Bonus

June 1, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in

this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem

necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and

risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that

are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the

company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be

true, and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document.

Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed

on, directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory

services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with

the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

June 1, 2010 4