1. Market Outlook

India Research

July 12, 2010

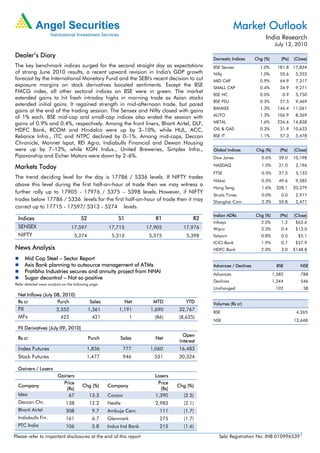

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

The key benchmark indices surged for the second straight day as expectations BSE Sensex 1.0% 181.8 17,834

of strong June 2010 results, a recent upward revision in India's GDP growth Nifty 1.0% 55.6 5,352

forecast by the International Monetary Fund and the SEBI's recent decision to cut MID CAP 0.9% 64.9 7,317

exposure margins on stock derivatives boosted sentiments. Except the BSE SMALL CAP 0.4% 34.9 9,271

FMCG index, all other sectoral indices on BSE were in green. The market

BSE HC 0.0% 0.9 5,750

extended gains to hit fresh intraday highs in morning trade as Asian stocks

BSE PSU 0.3% 27.5 9,469

extended initial gains. It regained strength in mid-afternoon trade, but pared

BANKEX 1.3% 146.4 11,061

gains at the end of the trading session. The Sensex and Nifty closed with gains

AUTO 1.3% 106.9 8,369

of 1% each. BSE mid-cap and small-cap indices also ended the session with

gains of 0.9% and 0.4%, respectively. Among the front liners, Bharti Airtel, DLF, METAL 1.6% 226.6 14,838

HDFC Bank, RCOM and Hindalco were up by 3–10%, while HUL, ACC, OIL & GAS 0.3% 31.9 10,633

Reliance Infra., ITC and NTPC declined by 0–1%. Among mid-caps, Deccan BSE IT 1.1% 57.3 5,478

Chronicle, Monnet Ispat, REI Agro, Indiabulls Financial and Dewan Housing

were up by 7–12%, while KGN Indus., United Breweries, Simplex Infra., Global Indices Chg (%) (Pts) (Close)

Pipavavship and Eicher Motors were down by 2–6%. Dow Jones 0.6% 59.0 10,198

Markets Today NASDAQ 1.0% 21.0 2,196

FTSE 0.5% 27.5 5,133

The trend deciding level for the day is 17786 / 5336 levels. If NIFTY trades

Nikkei 0.5% 49.6 9,585

above this level during the first half-an-hour of trade then we may witness a

Hang Seng 1.6% 328.1 20,379

further rally up to 17905 - 17976 / 5375 – 5398 levels. However, if NIFTY

Straits Times 0.0% 0.0 2,917

trades below 17786 / 5336 levels for the first half-an-hour of trade then it may Shanghai Com 2.3% 55.8 2,471

correct up to 17715 - 17597/ 5313 - 5274 levels.

Indian ADRs Chg (%) (Pts) (Close)

Indices S2 S1 R1 R2

Infosys 2.0% 1.2 $62.6

SENSEX 17,597 17,715 17,905 17,976 Wipro 3.3% 0.4 $13.0

NIFTY 5,274 5,313 5,375 5,398 Satyam 0.8% 0.0 $5.1

ICICI Bank 1.9% 0.7 $37.9

News Analysis HDFC Bank 2.0% 3.0 $148.8

Mid Cap Steel – Sector Report

Axis Bank planning to outsource management of ATMs Advances / Declines BSE NSE

Pratibha Industries secures and annuity project from NHAI Advances 1,582 788

Sugar decontrol – Not so positive

Declines 1,344 546

Refer detailed news analysis on the following page.

Unchanged 102 38

Net Inflows (July 08, 2010)

Rs cr Purch Sales Net MTD YTD Volumes (Rs cr)

FII 2,552 1,361 1,191 1,690 32,767

BSE 4,265

MFs 422 421 1 (86) (8,625)

NSE 13,648

FII Derivatives (July 09, 2010)

Open

Rs cr Purch Sales Net

Interest

Index Futures 1,836 777 1,060 16,483

Stock Futures 1,477 946 531 30,324

Gainers / Losers

Gainers Losers

Price Price

Company Chg (%) Company Chg (%)

(Rs) (Rs)

Idea 67 13.3 Concor 1,390 (2.5)

Deccan Chr. 138 12.2 Nestle 2,983 (2.1)

Bharti Airtel 308 9.7 Ambuja Cem. 111 (1.7)

Indiabulls Fin. 161 6.7 Glenmark 275 (1.7)

PTC India 106 5.8 Indus Ind Bank 215 (1.6)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 0109965391

2. Market Outlook | India Research

Mid Cap Steel - Sector Report

Our recent visit to Chhattisgarh's steel plants and mines was enriching, and we believe

mid-cap companies in the state stand to benefit from their captive mineral assets, flexible

business model and attractive valuations. Further, with sponge iron prices currently trading

below their marginal cost of production and domestic iron ore prices expected to remain

high, we expect sponge iron prices to increase in the coming months. Even though the

Naxal issue is still unsettled, we view it as region-specific and like companies whose

operations are unaffected. Moreover, with the government focusing on implementing a

progressive policy framework, we believe faster allotment of mines would offer a strong

foothold to these companies. Our top picks in this space are Prakash Industries (PIL) and

Godawari Power & Ispat (GPIL). We also like Monnet Ispat & Energy (MIEL) and Sarda

Energy & Minerals (SEML) and recommend investors to accumulate on declines.

Prakash Industries (PIL), through expansion of its sponge iron and billet capacity, is

addressing the imbalance in its steel business. Moreover, commissioning of the 125MW

power plant by 4QFY2011E will enable PIL to be net long on power. With EBITDA expected

to increase at a CAGR of 35.2% over FY2010-12E, we Initiate Coverage on the stock with

a Buy recommendation and target price of Rs232, valuing the stock at 5.0x FY2012E

EV/EBITDA.

We maintain our positive view on Godawari Power (GPIL) as its is expected to benefit from

the increase in mining capacity at Ari Dongri mine, starting of mining operations at Boria

Tibu iron ore mine and commercial production of pellets to start at Ardent Steel by August

2010. We maintain our Buy recommendation with a revised target price of Rs322 (earlier

Rs309), valuing the stock at 3.5x FY2012E EV/EBITDA.

Monnet Ispat & Energy (MIEL) is expanding its finished steel capacity by 1.5mn tonnes and

setting up a 1,050MW power plant in its 87.5% subsidiary Monnet Power. The timely

execution of the company's steel and power projects can provide a significant upside from

current levels. We Initiate Coverage on MIEL with an Accumulate rating and an SOTP

target price of Rs534, valuing the company's steel business at 6x FY2012E EV/EBITDA and

its investment in Monnet Power at 1.4x P/BV.

Sarda Energy and Mineral (SEML) is well poised to benefit from a) backward integration

into coal and iron ore, b) commercial production of pellets and c) increased power and

ferro alloy production. We expect full benefits of captive coal and iron ore to result in

EBITDA increasing by 189.6% yoy in FY2011E to Rs222cr. We Initiate Coverage on the

stock with an Accumulate recommendation and a target price of Rs290, valuing the stock

at 5.0x FY2012E EV/EBITDA.

Axis Bank planning to outsource management of ATMs

Axis Bank is exploring options to monetise its 4,200 automatic teller machines (ATMs). For

an upfront payment, the bank may allow a third-party service provider to collect inter-

change fees from other banks to let customers use Axis Bank’s ATMs. Thus, the bank will

be able to move its ATM assets off its balance sheet and outsource the entire network’s

management to service providers, paying them on a per-transaction basis.

Request-for-proposals seeking solutions on how this can be accomplished have already

been sent to 8–10 vendors, including Wincor-Diebold, Prizm Payment Services, AGS

Infotech and NCR, as per reports. Recently, the bank also entered into an agreement with

Prizm Payment Services and AGS Infotech to set up and manage 5,000 ATMs on a purely

variable model, enabling the bank to increase its ATM count to more than 9,000 within the

next 18 months. At the CMP, the stock is currently trading at 2.4x FY2012E ABV. We

maintain a Buy rating on the stock with a target price of Rs1,466.

July 12, 2010 2

3. Market Outlook | India Research

Pratibha Industries secures and annuity project from NHAI

Pratibha Industries has secured an annuity project from the National Highway Authority of

India (NHAI) in a joint venture with Abhyudaya Housing and Construction Pvt. Ltd. Total

annuities receivable from NHAI over the span of the concession agreement is Rs337cr. The

project involves two laning with paved shoulders of Bhopal-Sanchi section of NH-86 under

NHDP Phase III. The construction period is two years and the payments shall be through

semi annuities of Rs12.95cr for 13 years totaling to Rs337cr. In light of the rich valuations

that the stock trades at, we maintain our Neutral view.

Sugar decontrol – Not so positive

The Union Food and Agriculture Minister, Mr Sharad Pawar, said that this was the ‘right

time’ to work towards decontrolling the country's sugar industry, thus fulfilling the long

overdue request of investors and sugar manufacturers. Currently, cane prices of sugar

mills are governed by the central (statutory minimum price) as well state governments

(state advised price). The central government also controls sugar supply and price through

monthly sales quota and levy sales (% of mills production) to government at subsidies

price. Hence, any decontrol should not only be from the central government but also from

the state government to completely benefit sugar mills. We maintain our Neutral view on

the sector.

Economic and Political News

Trade minister forecasts over 9% GDP growth

Minimum tenure for infra bonds fixed at 10 years

June 2010 power output up 3.43%

Diesel subsidy may be set at Rs1.49/litre

Corporate News

Essar Power signs pact for Tori-I power plant

Piramal to get US $2.12bn in 4–6 weeks from Abbott

Apollo to invest Rs1,800cr, hire 23,000 in 3–4 yrs

Essar Oil raises US $147mn from founders

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

ABC India Ltd. Quarterly Results

Arman Financial Services Audited Results, Dividend & Others

Aurionpro Solutions Audited Results & Dividend

Beckons Industries Quarterly Results

Celebrity Fashions Preferential Issue of Shares

CMC Ltd. Quarterly Results

July 12, 2010 3

4. Market Outlook | India Research

Research Team Tel: 022-4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision. Nothing in

this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem

necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and

risks involved), and should consult their own advisors to determine the merits and risks of such an investment.

Angel Securities Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment decisions that

are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are those of the analyst, and the

company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and trading volume, as

opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be

true, and is for general guidance only. Angel Securities Limited has not independently verified all the information contained within this document.

Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this

document. While Angel Securities Limited endeavours to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced, redistributed or passed

on, directly or indirectly.

Angel Securities Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other advisory

services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Securities Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in connection with

the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section).

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel : (022) 3952 4568 / 4040 3800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546 Angel Securities Ltd:BSE: INB010994639/INF010994639 NSE:

INB230994635/INF230994635 Membership numbers: BSE 028/NSE:09946

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

July 12, 2010 4