Malegaon Call Girls Service ☎ ️82500–77686 ☎️ Enjoy 24/7 Escort Service

Persistent systems

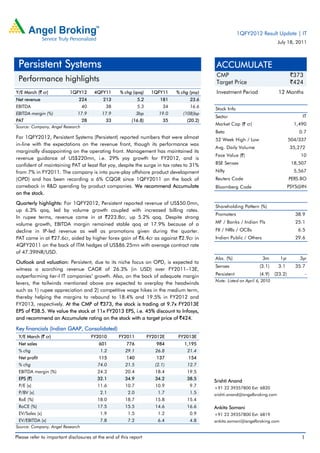

1. 1QFY2012 Result Update | IT

July 18, 2011

Persistent Systems ACCUMULATE

CMP `373

Performance highlights Target Price `424

Y/E March (` cr) 1QFY12 4QFY11 % chg (qoq) 1QFY11 % chg (yoy) Investment Period 12 Months

Net revenue 224 213 5.2 181 23.6

EBITDA 40 38 5.3 34 16.6

Stock Info

EBITDA margin (%) 17.9 17.9 3bp 19.0 (108)bp

Sector IT

PAT 28 33 (16.8) 35 (20.2)

Market Cap (` cr) 1,490

Source: Company, Angel Research

Beta 0.7

For 1QFY2012, Persistent Systems (Persistent) reported numbers that were almost 52 Week High / Low 504/337

in-line with the expectations on the revenue front, though its performance was

Avg. Daily Volume 35,272

marginally disappointing on the operating front. Management has maintained its

Face Value (`) 10

revenue guidance of US$220mn, i.e. 29% yoy growth for FY2012, and is

confident of maintaining PAT at least flat yoy, despite the surge in tax rates to 31% BSE Sensex 18,507

from 7% in FY2011. The company is into pure-play offshore product development Nifty 5,567

(OPD) and has been recording a 6% CQGR since 1QFY2011 on the back of Reuters Code PERS.BO

comeback in R&D spending by product companies. We recommend Accumulate Bloomberg Code PSYS@IN

on the stock.

Quarterly highlights: For 1QFY2012, Persistent reported revenue of US$50.0mn,

Shareholding Pattern (%)

up 6.3% qoq, led by volume growth coupled with increased billing rates.

Promoters 38.9

In rupee terms, revenue came in at `223.8cr, up 5.2% qoq. Despite strong

volume growth, EBITDA margin remained stable qoq at 17.9% because of a MF / Banks / Indian Fls 25.1

decline in IP-led revenue as well as promotions given during the quarter. FII / NRIs / OCBs 6.5

PAT came in at `27.6cr, aided by higher forex gain of `6.4cr as against `2.9cr in Indian Public / Others 29.6

4QFY2011 on the back of ITM hedges of US$86.25mn with average contract rate

of 47.39INR/USD.

Abs. (%) 3m 1yr 3yr

Outlook and valuation: Persistent, due to its niche focus on OPD, is expected to

Sensex (3.1) 3.1 35.7

witness a scorching revenue CAGR of 26.3% (in USD) over FY2011–13E,

outperforming tier-I IT companies’ growth. Also, on the back of adequate margin Persistent (4.9) (23.2) -

Note: Listed on April 6, 2010

levers, the tailwinds mentioned above are expected to overplay the headwinds

such as 1) rupee appreciation and 2) competitive wage hikes in the medium term,

thereby helping the margins to rebound to 18.4% and 19.5% in FY2012 and

FY2013, respectively. At the CMP of `373, the stock is trading at 9.7x FY2013E

EPS of `38.5. We value the stock at 11x FY2013 EPS, i.e. 45% discount to Infosys,

and recommend an Accumulate rating on the stock with a target price of `424.

Key financials (Indian GAAP, Consolidated)

Y/E March (` cr) FY2010 FY2011 FY2012E FY2013E

Net sales 601 776 984 1,195

% chg 1.2 29.1 26.8 21.4

Net profit 115 140 137 154

% chg 74.0 21.5 (2.1) 12.7

EBITDA margin (%) 24.3 20.4 18.4 19.5

EPS (`) 32.1 34.9 34.2 38.5

Srishti Anand

P/E (x) 11.6 10.7 10.9 9.7 +91 22 39357800 Ext: 6820

P/BV (x) 2.1 2.0 1.7 1.5 srishti.anand@angelbroking.com

RoE (%) 18.0 18.7 15.8 15.4

RoCE (%) 17.5 15.5 14.6 16.6 Ankita Somani

EV/Sales (x) 1.9 1.5 1.2 0.9 +91 22 39357800 Ext: 6819

EV/EBITDA (x) 7.8 7.2 6.4 4.8 ankita.somani@angelbroking.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Persistent | 1QFY2012 Result Update

Exhibit 1: 1QFY2012 performance (Indian GAAP, Consolidated)

Y/E March (` cr) 1QFY12 4QFY11 % chg (qoq) 1QFY11 % chg (yoy) FY2011 FY2010 % chg (yoy)

Net revenue 224 213 5.2 181 23.6 776 601 29.1

Cost of revenue 140 133 5.3 112 25.0 472 337 40.1

Gross profit 83 80 4.8 69 21.3 304 264 15.0

S&M expenses 18 16 7.7 14 23.8 62 46 33.5

G&A expenses 26 25 2.3 20 27.5 83 71 17.1

EBITDA 40 38 5.3 34 16.6 158 146 8.2

Depreciation 13 12 6.0 10 29.6 42 34 26.4

EBIT 27 26 5.0 25 11.4 116 113 2.7

Other income 6 6 3 17 8

Forex gain/(loss) 6 3 9 17 3

PBT 40 35 14.9 37 7.9 150 124 21.2

Income tax 12 2 628.2 3 382.6 11 9 17.3

PAT 28 33 (16.8) 35 (20.2) 140 115 21.5

EPS 6.9 8.3 (16.8) 8.6 (19.8) 34.9 32.1 8.8

Gross margin (%) 37.3 37.4 (11)bp 38.0 (71)bp 39.1 43.9 (478)bp

EBITDA margin (%) 17.9 17.9 3bp 19.0 (108)bp 20.4 24.3 (394)bp

EBIT margin (%) 12.3 12.3 (2)bp 13.6 (134)bp 14.9 18.8 (383)bp

PAT margin (%) 11.7 15.0 (329)bp 17.8 (618)bp 17.2 18.8 (154)bp

Source: Company, Angel Research

Revenue momentum continues

For 1QFY2012, Persistent reported revenue of US$50.0mn, up 6.3% qoq,

primarily led by volume growth. Also, the company’s billing rates, onsite as well as

offshore, improved by 2.3% and 1.3% qoq to US$13,033 per person per month

(ppm) and US$3,770 ppm, respectively. The improvement in billing rates during

the quarter was due to selling of high-end services like technology consulting,

mobility and analytics.

In rupee terms, revenue came in `223.8cr, up 5.2% qoq – lower growth as against

dollar revenue due to 1.0% qoq INR appreciation against USD in 1QFY2012.

Exhibit 2: Trend in revenue growth (qoq)

55 10

8.8 9

50

50.0 8

45 47.0 7

(US$ mn)

6.7

6.3

6

(%)

5.8 43.2

40 5

40.5

39.5

4

35

3

2.6

30 2

1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Revenue (US$mn) qoq growth (%)

Source: Company, Angel Research

July 18, 2011 2

3. Persistent | 1QFY2012 Result Update

Exhibit 3: Trend in billing rates (qoq)

14,000 12,896 12,746 13,033

12,414 12,470

12,000

10,000

(US$/ppm)

8,000

6,000

3,600 3,601 3,661 3,723 3,770

4,000

2,000

-

1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Onsite Offshore

Source: Company, Angel Research

Industry wise, the company’s growth was led by the telecom and wireless segment

(contributing 22.2% to revenue), which grew by 15.1% qoq, majorly led by

European clients. The anchor industry segment – infrastructure and systems

(contributed 67.9% to revenue) – continued its revenue traction and grew by 5.7%

qoq. In absolute terms, revenue contribution from the lifesciences and healthcare

segment stood modest; however, on a qoq basis, revenue declined by 6.0% due to

base effect, as higher growth was reported in this segment in 2HFY2011.

Exhibit 4: Growth trend in industry segments

% to revenue % chg (qoq) % chg (yoy)

Infrastructure and systems 67.9 5.7 19.9

Telecom and wireless 22.2 15.1 51.9

Lifesciences and healthcare 9.9 (6.0) 27.9

Source: Company, Angel Research

Geography wise, growth was led by Europe, revenue from which grew by 35.7%

qoq – whopping growth due to low base effect and ramp-up in revenue from few

European clients. North America continued to grow during this quarter as well

at 2.0% qoq.

Exhibit 5: Growth trend in geographies

% to revenue % chg (qoq) % chg (yoy)

North America 82.8 2.0 23.2

Europe 7.4 35.7 44.1

Asia-Pacific 9.8 31.9 47.7

Source: Company, Angel Research

Revenue contribution from IP-led services declined in 1QFY2012 to 6.1% from

10.3% in 4QFY2012 because of lower revenue from the company’s top customer

that contributes almost 60% to the company’s IP-led revenue. Management has

indicated that it is a one-time issue and revenue from the top customer is expected

to scale up again in the coming quarters. IP-led revenue seems low also because

of higher base in 4QFY2011, which was due to higher product sale from the top

customer’s end in 3QFY2011, the royalty revenue of which got reflected in

July 18, 2011 3

4. Persistent | 1QFY2012 Result Update

Persistent’s account in 4QFY2011. The company expects IP-led revenue to touch

US$25mn by the end of FY2012, i.e. whopping 68% yoy growth.

Hiring and utilisation

Persistent continued its modest hiring trend and added 260 net employees during

the quarter. Gross addition during the quarter was 545. In the technical employee

base of the company, 228 net employees were added. Attrition rate (LTM basis)

declined significantly in 1QFY2012 to 18.4% from 19.6% in 4QFY2011, as the

company gave wage hikes in 4QFY2011 to control attrition and, as a result,

quarterly attrition rate in 1QFY2012 stood merely at 3.2% (quarterly annualised at

12.8%), leading to an overall decline in attrition rates on an LTM basis.

Exhibit 6: Employee metrics

Particulars 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Technical 4,554 4,907 5,070 5,950 6,178

Sales 79 87 94 108 119

Rest 278 287 296 302 323

Total 4,911 5,281 5,460 6,360 6,620

Net addition 249 370 179 900 260

Attrition – LTM (%) 16.3 18.6 21.5 19.6 18.4

Source: Company, Angel Research

For FY2012, management has a gross hiring target of 2,300 employees (1,000

freshers and 1,200–1,300 laterals) and a net hiring target of ~1,500 employees.

Net utilisation (excluding resources in IP-led work) increased by 170bp qoq to

72.7%. However, in 2QFY2012, we expect utilisation to dip due to intake of

freshers into the system. Management expects utilisation to inch up and reach

75–77% over the next 3–4 quarters.

Exhibit 7: Utilisation trend

80

78.5

78

76

74.2

(%)

74 72.7

71.7

72 71.0

70

68

1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Utilisation (%)

Source: Company, Angel Research

July 18, 2011 4

5. Persistent | 1QFY2012 Result Update

Margin profile

In 1QFY2012, the company’s EBITDA and EBIT margins remained almost stable

qoq at 17.9% and 12.3%, respectively, despite higher revenue growth due to

higher costs incurred on account of promotions given in 1QFY2012 and drop in

IP-led revenue.

Going ahead, for 2QFY2012, the company has announced wage hikes — 7–8%

for offshore employees and 4% for onsite employees, effective from July 1, 2011.

This is expected to negatively affect the company’s operating margins by

200–220bp qoq in the next quarter. However, for the full year, the company

expects margins to remain stable at FY2011 levels.

Exhibit 8: Margin profile

45

40

42.2

35 38.0 39.1

37.4 37.3

30

23.0 21.9

25

(%)

19.0 17.9 17.9

20

15 17.6 16.5

10 13.6

12.3 12.3

5

1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Gross margin EBITDA margin EBIT margin

Source: Company, Angel Research

Client pyramid

The client metrics of the company saw a qualitative movement with six new clients

in the US$1mn–3mn revenue bracket. Also, four clients were added in the

<US$1mn revenue bracket.

In 1QFY2012, Persistent added 32 new clients, out of which eight were from the

company’s partners. The total active client base of the company increased to 239

from 229 in 4QFY2011.

Exhibit 9: Client metrics

Particulars 1QFY11 2QFY11 3QFY11 4QFY11 1QFY12

Customers billed 196 201 207 229 239

<US$1mn 165 171 169 194 198

US$1mn-3mn 22 21 29 26 32

>US$3mn 9 9 9 9 9

Source: Company, Angel Research

July 18, 2011 5

6. Persistent | 1QFY2012 Result Update

Investment rationale

Established footprint in the resurging OPD market

Persistent has a dominant market share of ~16% (in CY2010) in the Indian OPD

market. The company is witnessing a robust uptick in the deal pipeline as clients

are flocking to generate new products in shorter time to market to capture market

share. This is driving many ISVs and wireless equipment manufacturers to spend

on R&D and engineering services. As per IDC, out of the global size of US$40bn in

2010 for R&D and product engineering, the Indian OPD market is just

worth ~US$1bn. The global OPD market is expected to grow at a 14% CAGR to

US$65.7bn by 2014. The offshore segment of the global OPD market in

2010 crossed the US$10bn mark and is expected to grow at a 19% CAGR to

US$16bn by 2014.

Exhibit 10: Worldwide R&D/PES spending (US$ mn)

70,000 25

60,000 18.2 19.1 20

17.9 16.3

50,000 13.2 15

(US$ mn)

(%)

9.7 10.2

40,000 10

30,000 5

3.9

20,000 0

CY2006 CY2007 CY2008 CY2009 CY2010 CY2011 CY2012 CY2013

IT spending (US$ mn) yoy growth (%)

Source: IDC, Angel Research

Exhibit 11: Worldwide R&D/PES offshore spending (US$ mn)

18,000 23.5 25

21.7

16,000 19.4

20

14,000 17.9

15

(US$ mn)

12,000 11.8

(%)

9.7

10,000 10

8,000

5

6,000 3.9

3.8

4,000 0

CY2006 CY2007 CY2008 CY2009 CY2010 CY2011 CY2012 CY2013

IT spending (US$ mn) yoy growth (%)

Source: IDC, Angel Research

July 18, 2011 6

7. Persistent | 1QFY2012 Result Update

Non-linear services already a sizeable part of the portfolio

Persistent has a sizeable portfolio coming in from IP-led revenue, which was ~9%

in FY2011. The company expects it to scale up to ~11% in FY2012 and reach

~20% by FY2015. The company has been investing in the areas of 1) cloud,

2) analytics, 3) collaboration and 4) mobility, which are towards consulting. With

the expected increase in contribution from IP revenue, the company is likely to

benefit at the margin front because of its non-linear nature.

Exhibit 12: IP-led revenue as a % of total revenue

12 11.4

11

10.2

10

8.8

9

8

(%)

7.2

7

6 5.2

5

4

FY2009 FY2010 FY2011 FY2012E FY2013E

IP driven revenue (as % of sales)

Source: Company, Angel Research

Marquee clientele

Out of its active clients, 37 have revenue of more than US$1bn and dedicated

annual R&D budgets of 6–20% of revenue to drive product innovation.

The company has marquee clients (with R&D budgets) including MNCs like IBM

(~6.0%), Google (~12.8%), Microsoft (~13.9%), Oracle (~12.8%), Intel

(~15.1%), Cisco (~13.2%), Nokia (~14%), Samsung, Yahoo (~17%) and eBay.

In addition, the company’s client mining is strong as the company manages to get

~11% of its revenue from new clients vis-à-vis peers who get mere 3–5%.

Exhibit 13: Revenue (CY2010/FY2010) and R&D budget as a % of sales

120

99.9

100

80

62.5

60

43.6 40.0

40 29.3

20 13.9 15.1 13.2 13.8 12.8

12.5 6.0

0

Microsoft Intel Cisco SAP Google IBM

Revenue (US$ mn) R&D as % of sales

Source: Company, Angel Research

July 18, 2011 7

8. Persistent | 1QFY2012 Result Update

Robust revenue growth with gradual improvement in margins

Persistent is expected to report a robust revenue CAGR of 26.3% over FY2011–13E

on the back of return in demand for OPD services. In fact the company has

indicated net hiring to be 1,500 plus for FY2012E on the back of a strong deal

pipeline. On the operating front, we expect margins to rebound in 2HFY2012 from

17.9% in 1QFY2012 to 18.4% in FY2012 and 19.5% in FY2013. We expect this

margin improvement because of margin levers such as 1) employee pyramid

rationalisation (indicated to hire 700 freshers out of 1,500 net people in FY2012);

2) higher revenue productivity due to the expected increase in IP-led revenue

contribution; 3) gradual increase in utilisations to 74.7% in FY2013 from 72% in

1QFY2012 and 4) stable G&A in absolute terms even with higher growth.

On the PAT front, we expect factors like 1) improvement in profitability and 2) forex

gains due to In-the-Money (with average contract rate of 47.39INR/USD) hedges

worth US$86.25mn to counter the headwinds due to higher tax rate of 31%

compared to 7% in FY2011.

Exhibit 14: Revenue expectations

300

250 28.8% 271.7

CAGR

200 221.4

(US$ mn)

150 170.2

127.9 127.3

100

50

FY2009 FY2010 FY2011 FY2012E FY2013E

Revenue (US$ mn)

Source: Company, Angel Research

Exhibit 15: Margin expectations

31 30.1

29

27

24.3

25

(%)

23

20.4

21 19.5

18.4

19

17

FY2009 FY2010 FY2011 FY2012E FY2013E

EBITDA margin (%)

Source: Company, Angel Research

July 18, 2011 8

9. Persistent | 1QFY2012 Result Update

Outlook and valuation

Persistent, due to its niche focus on OPD, is expected to record a scorching

revenue CAGR of 26.3% (in USD) over FY2011–13E, outperforming tier-I IT

companies’ growth. Also, on the back of adequate margin levers, the tailwinds

mentioned above are expected to overplay the headwinds such as 1) rupee

appreciation and 2) competitive wage hikes in the medium term and help the

margins to rebound to 18.4% and 19.5% in FY2012 and FY2013, respectively.

At the CMP of `373, the stock is trading at 9.7x FY2013E EPS of `38.5. We value

the stock at 11x FY2013 EPS, i.e. 45% discount to Infosys, and recommend an

Accumulate rating on the stock with a target price of `424.

Exhibit 16: Key assumptions

FY2012 FY2013

Revenue growth – USD terms (%) 30.1 22.7

USD-INR rate 44.5 44.0

Revenue growth – INR terms (%) 26.8 21.4

EBITDA margin (%) 18.4 19.5

Tax rate (%) 31.0 31.0

EPS growth (%) (2.0) 12.7

Source: Company, Angel Research

Exhibit 17: One-year forward PE(x) chart

700

600

500

(` )

400

300

200

Dec-10

Apr-10

Jul-10

Aug-10

Apr-11

Jul-11

Mar-11

Oct-10

Sep-10

Nov-10

Feb-11

May-10

May-11

Jun-10

Jun-11

Jan-11

Price 16 14 12 10 8

Source: Company, Angel Research

July 18, 2011 9

15. Persistent | 1QFY2012 Result Update

Research Team Tel: 022 - 3935 7800 E-mail: research@angelbroking.com Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Persistent

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below `1 lakh for Angel, its Group companies and Directors

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 18, 2011 15