Downloaded 591 times

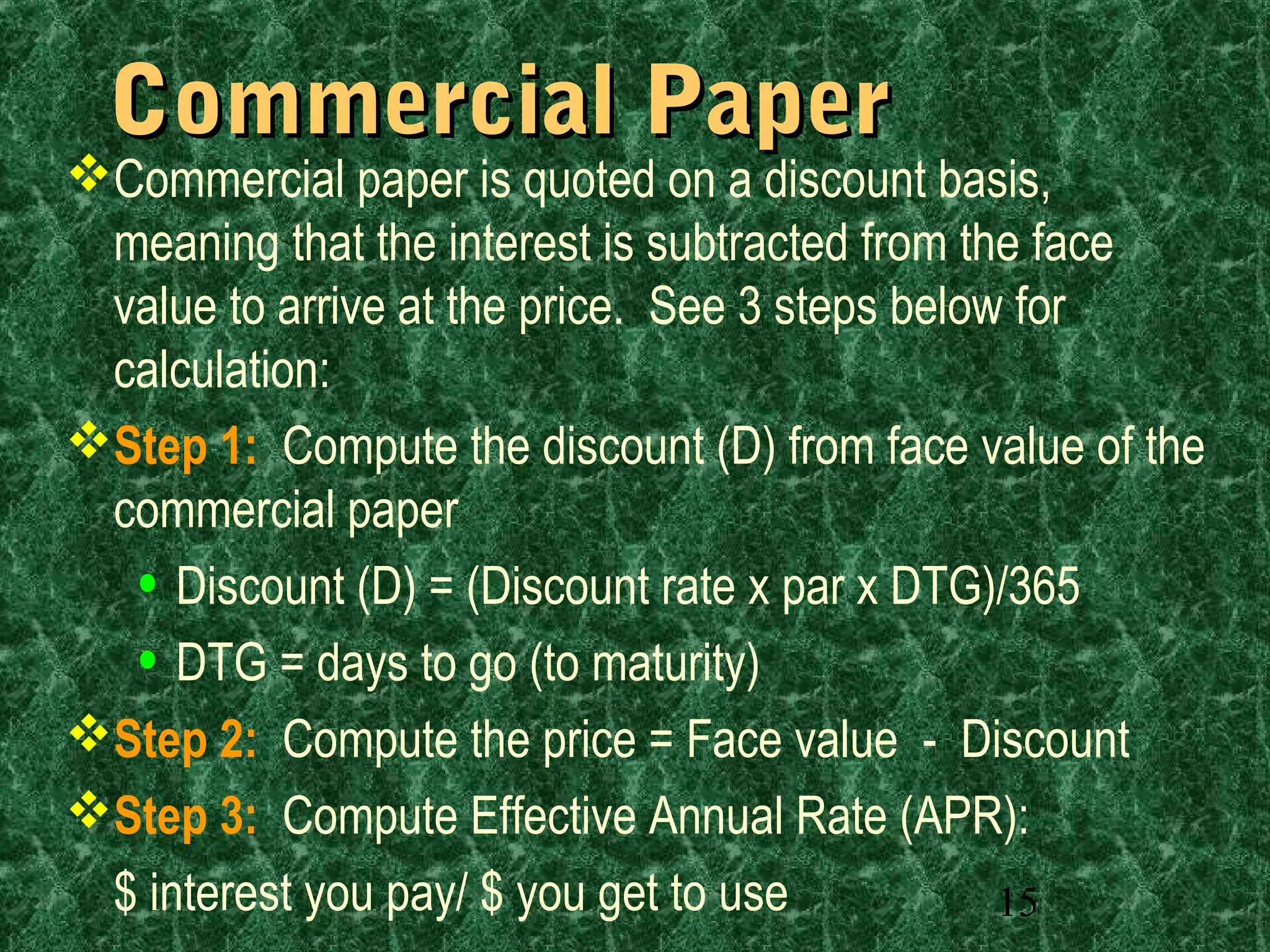

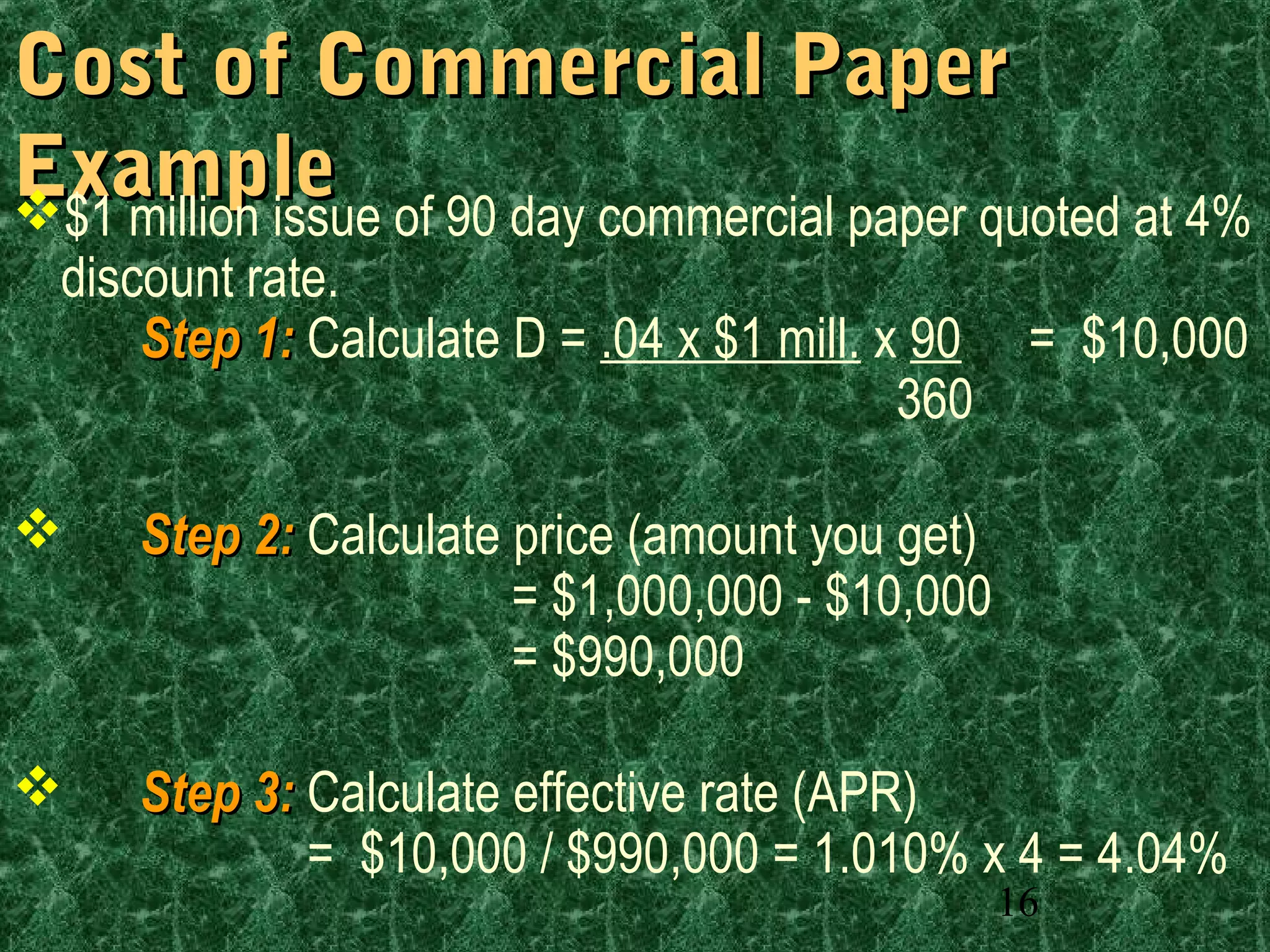

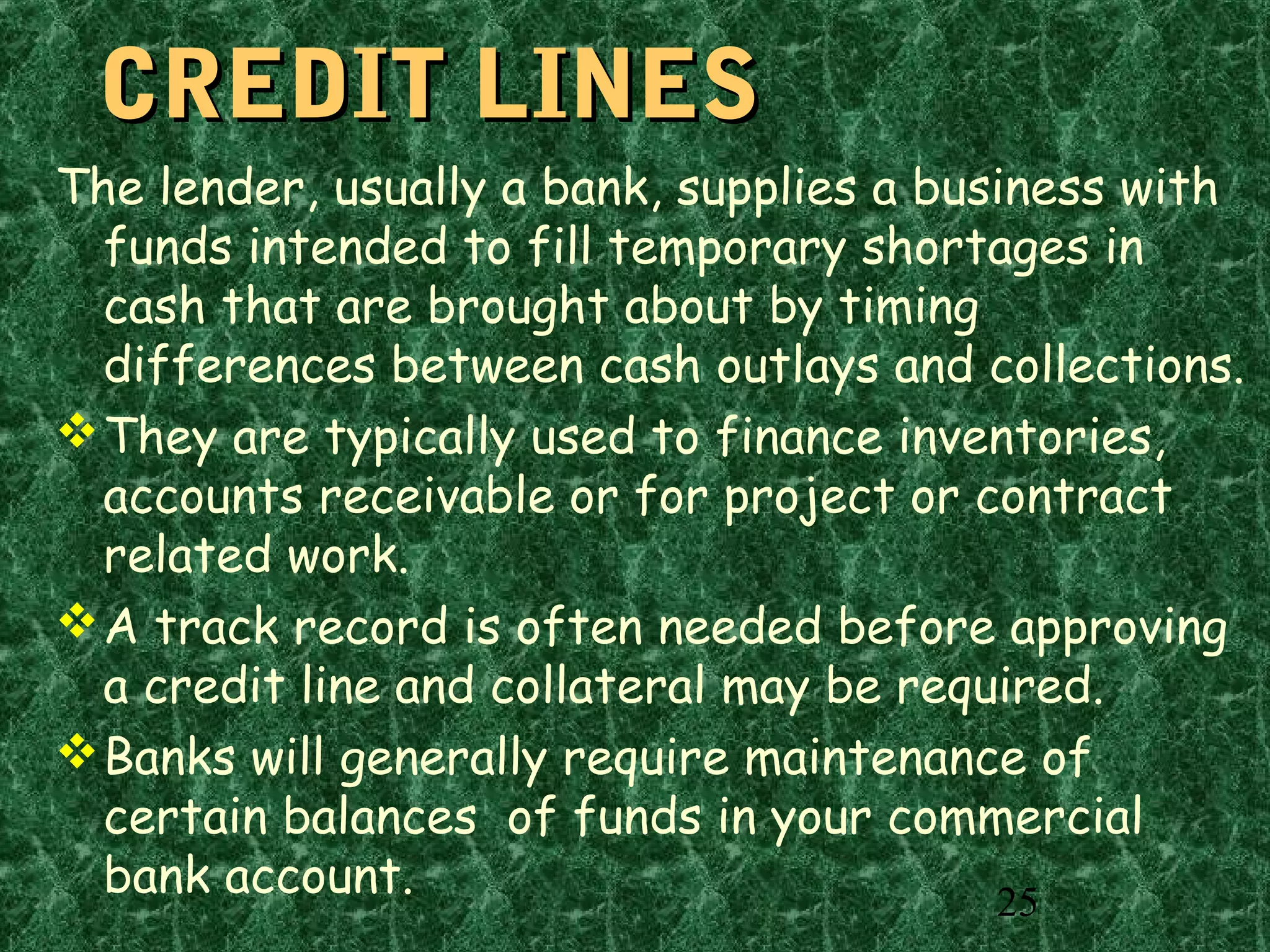

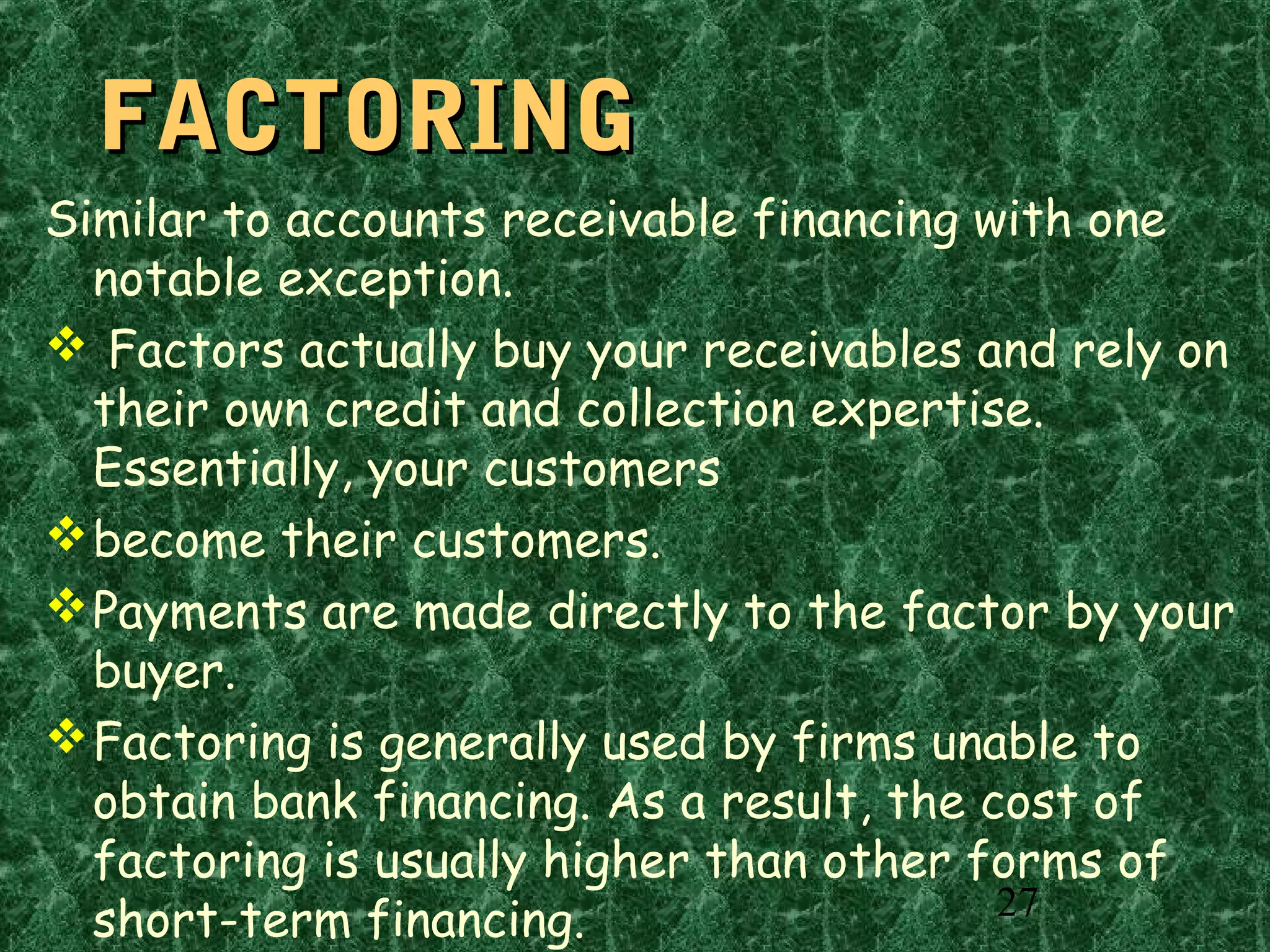

This document discusses various types of short-term financing. It defines short-term financing as financing for one year or less, including short-term loans from banks, trade credit from suppliers, and commercial paper. The document outlines the advantages of short-term financing over long-term options and describes how firms can use accounts receivable and inventory as collateral for short-term loans. Various short-term financing sources and their costs are defined, including calculations for determining effective interest rates.