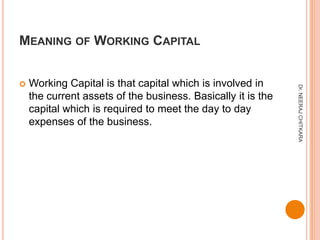

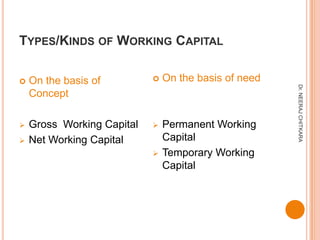

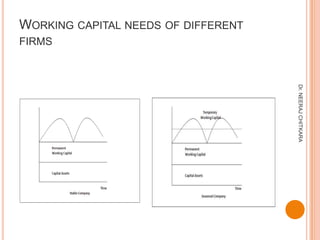

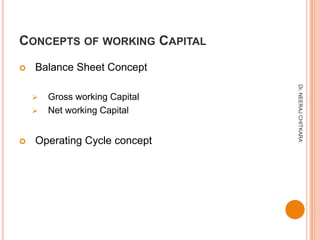

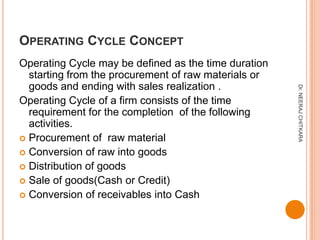

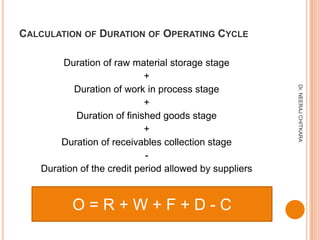

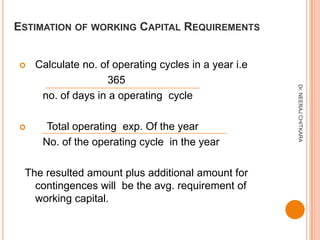

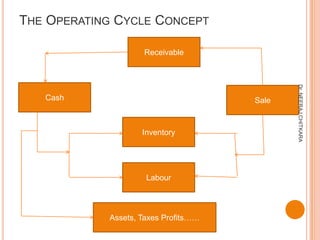

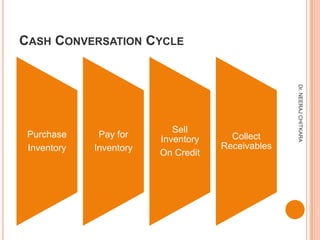

This document provides an introduction to working capital management. It defines working capital as the capital required to meet the day-to-day expenses of a business. Working capital can be classified based on concept into gross working capital and net working capital, and based on need into permanent, temporary, regular and reserve working capital. The operating cycle concept and cash conversion cycle are also introduced as methods to estimate working capital requirements. Working capital needs vary between different types of firms.