Download to read offline

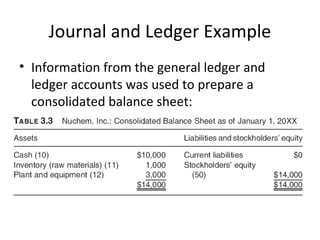

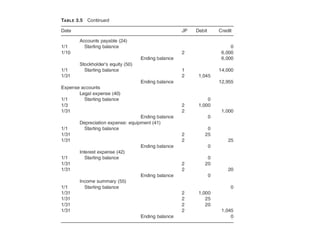

This document provides an overview of basic accounting concepts and financial statements. It explains how accounting systems record business transactions in journals and ledgers, and how this information is used to generate key financial reports like income statements and balance sheets. An example is also given to illustrate how initial transactions are recorded and how the reports are generated for a sample company over time.