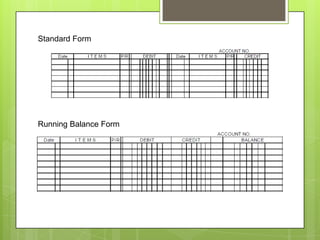

The document outlines the steps in the accounting cycle which include analyzing transactions, journalizing transactions, posting to ledgers, preparing a trial balance, adjusting entries, preparing financial statements, and closing entries. It also provides details on journalizing, including columns for date, account titles, debit/credit amounts, and posting references. The recording process involves analyzing source documents, writing details in the journal columns, and providing explanations.