Download to read offline

![The life of each part is calculated by the formula:

D = P[(100 – rd)/100]n

Where,

D- depreciated value,

P- cost at present market rate,

rd- fixed percentage of depreciation (r stands for rate and d for

depreciation),

n- the number of years the building had been constructed.

To find the total valuation of the property, the present value of land, water

supply, electric and sanitary fitting etc., should be added to the above

value.](https://image.slidesharecdn.com/valuation08-200408064937/85/Valuation-08-04-2020-19-320.jpg)

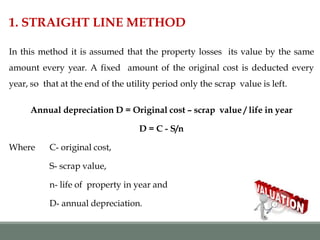

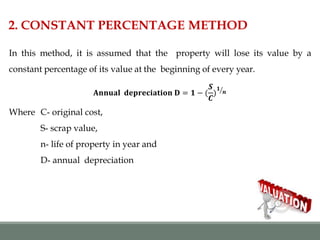

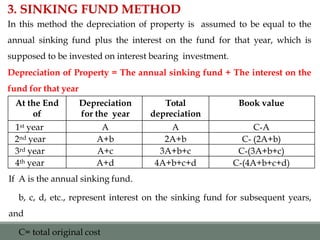

The lecture discusses valuation techniques for estimating the fair price of properties, with applications in buying, selling, taxation, and securing loans. Various methods for calculating depreciation and property value are explored, including the straight line and constant percentage methods, as well as approaches for determining rent and capital costs. Key concepts include net income, salvage value, and obsolescence, highlighting their impact on property valuation.