Downloaded 361 times

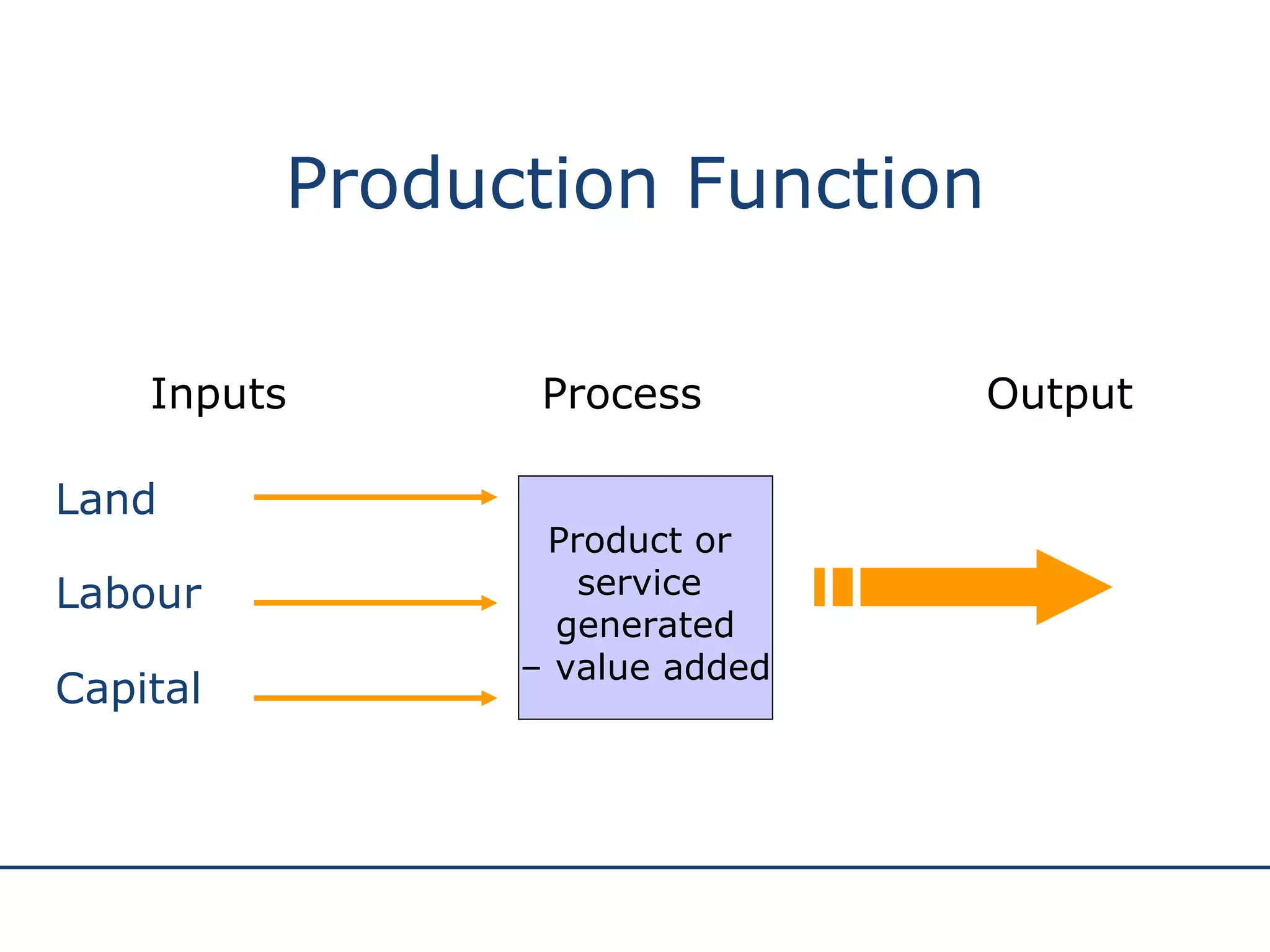

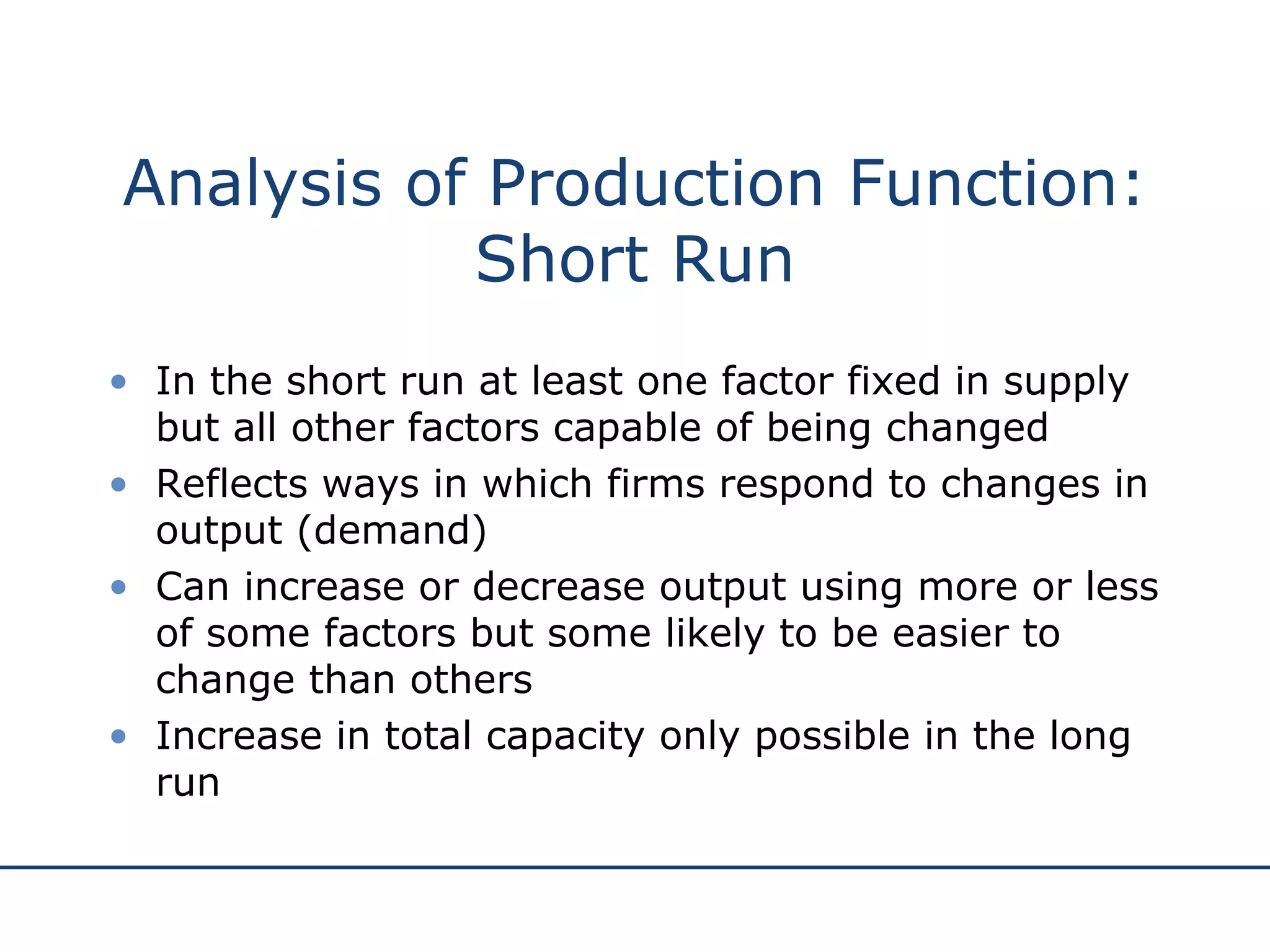

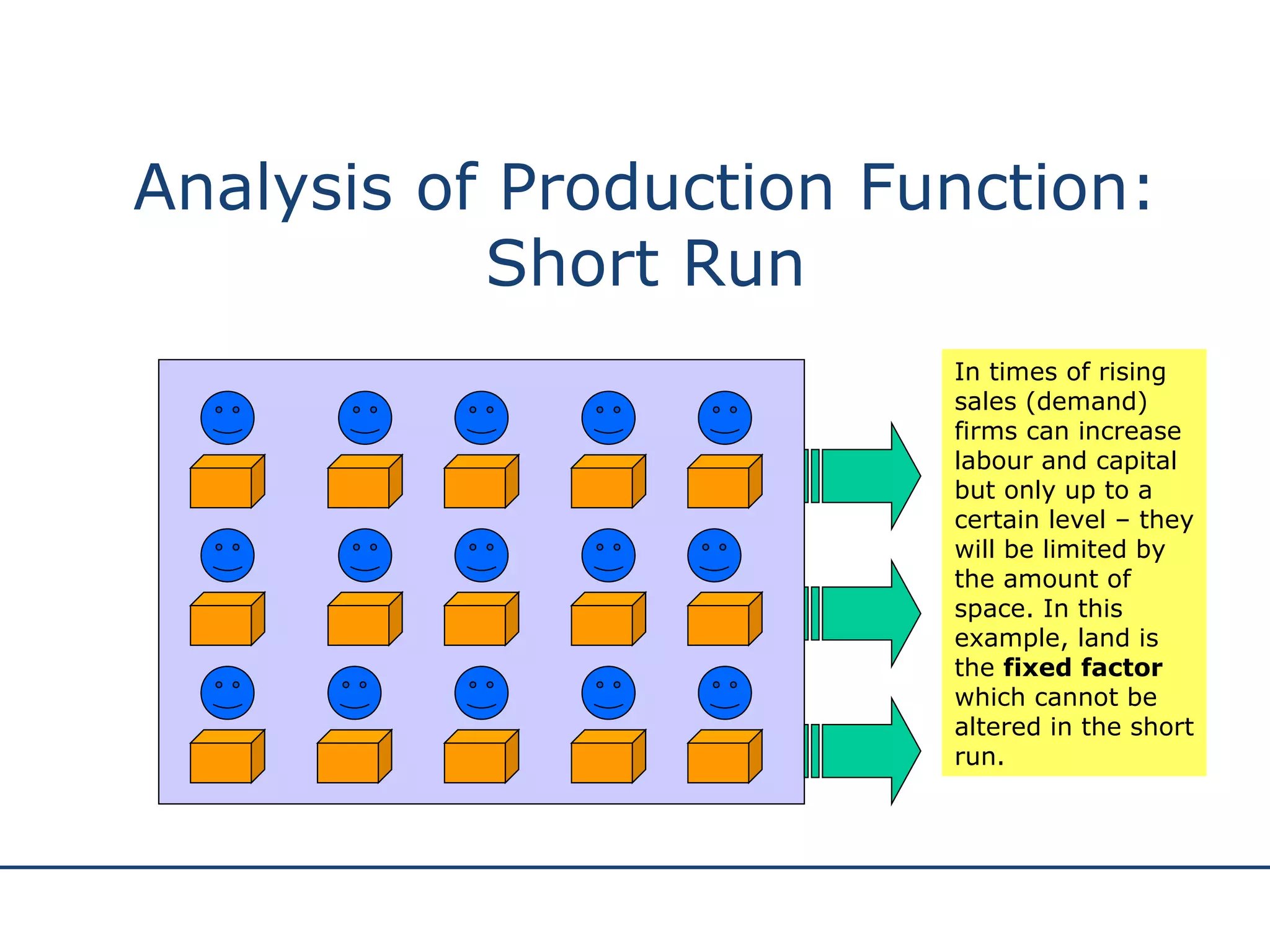

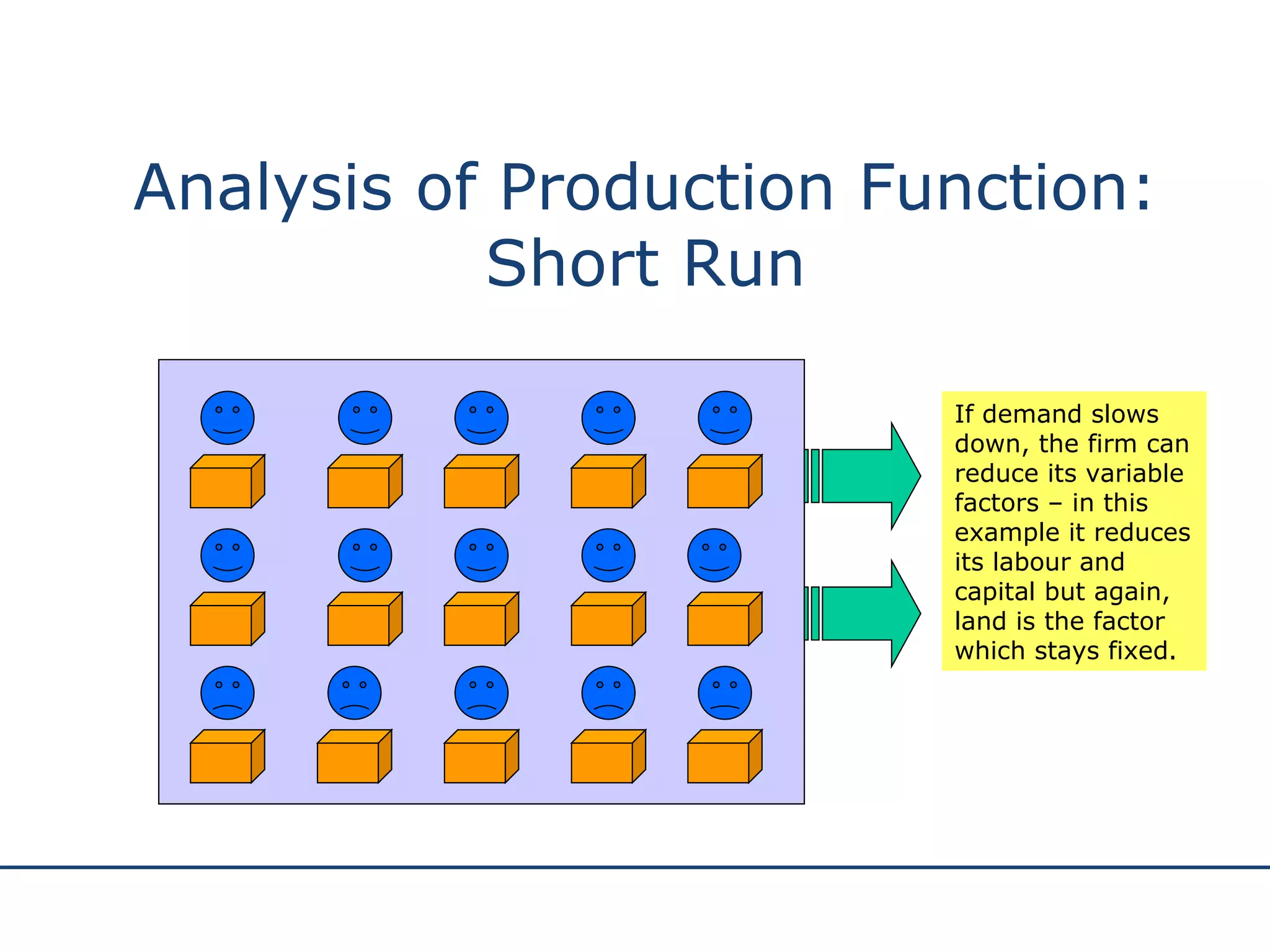

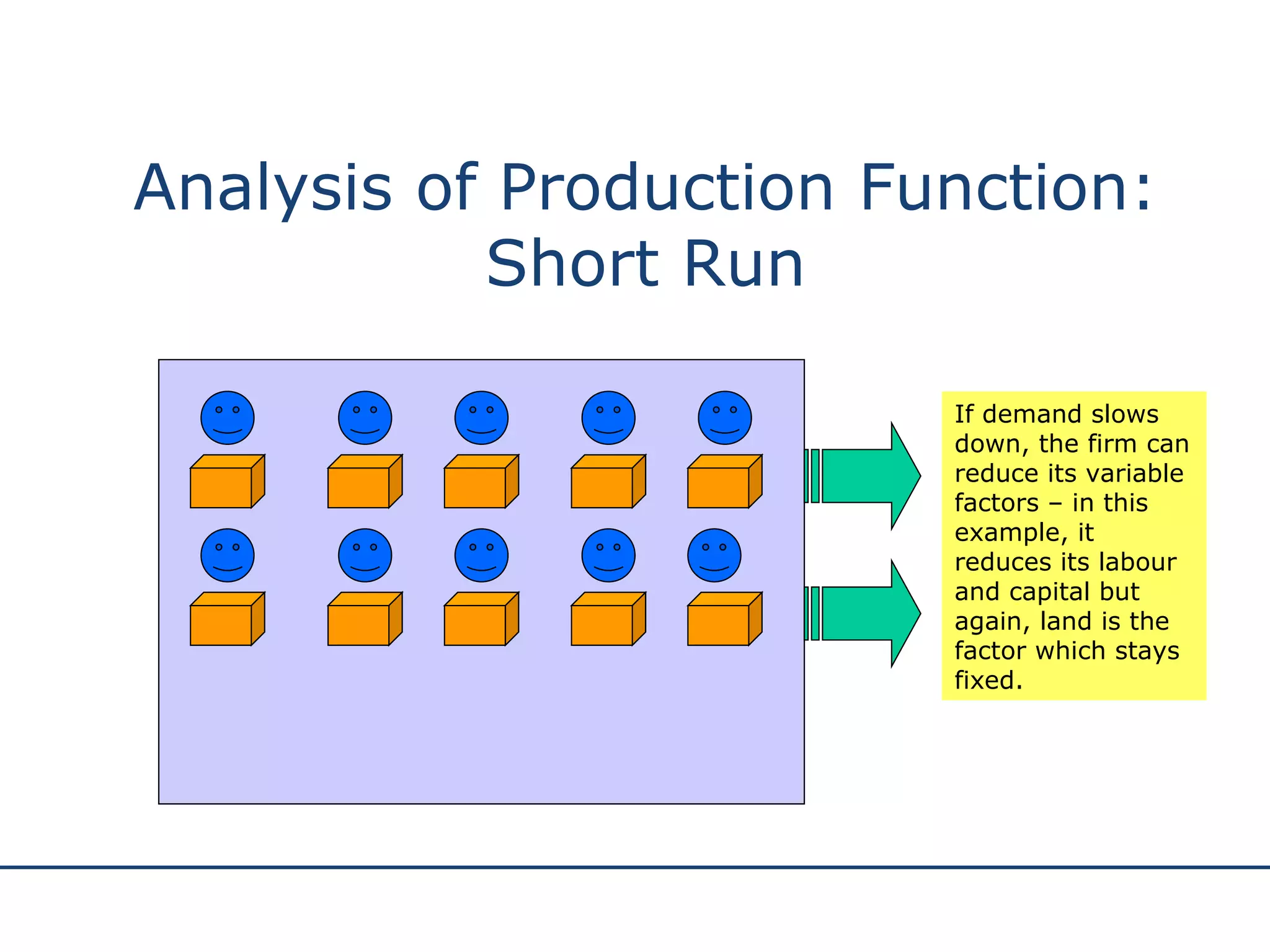

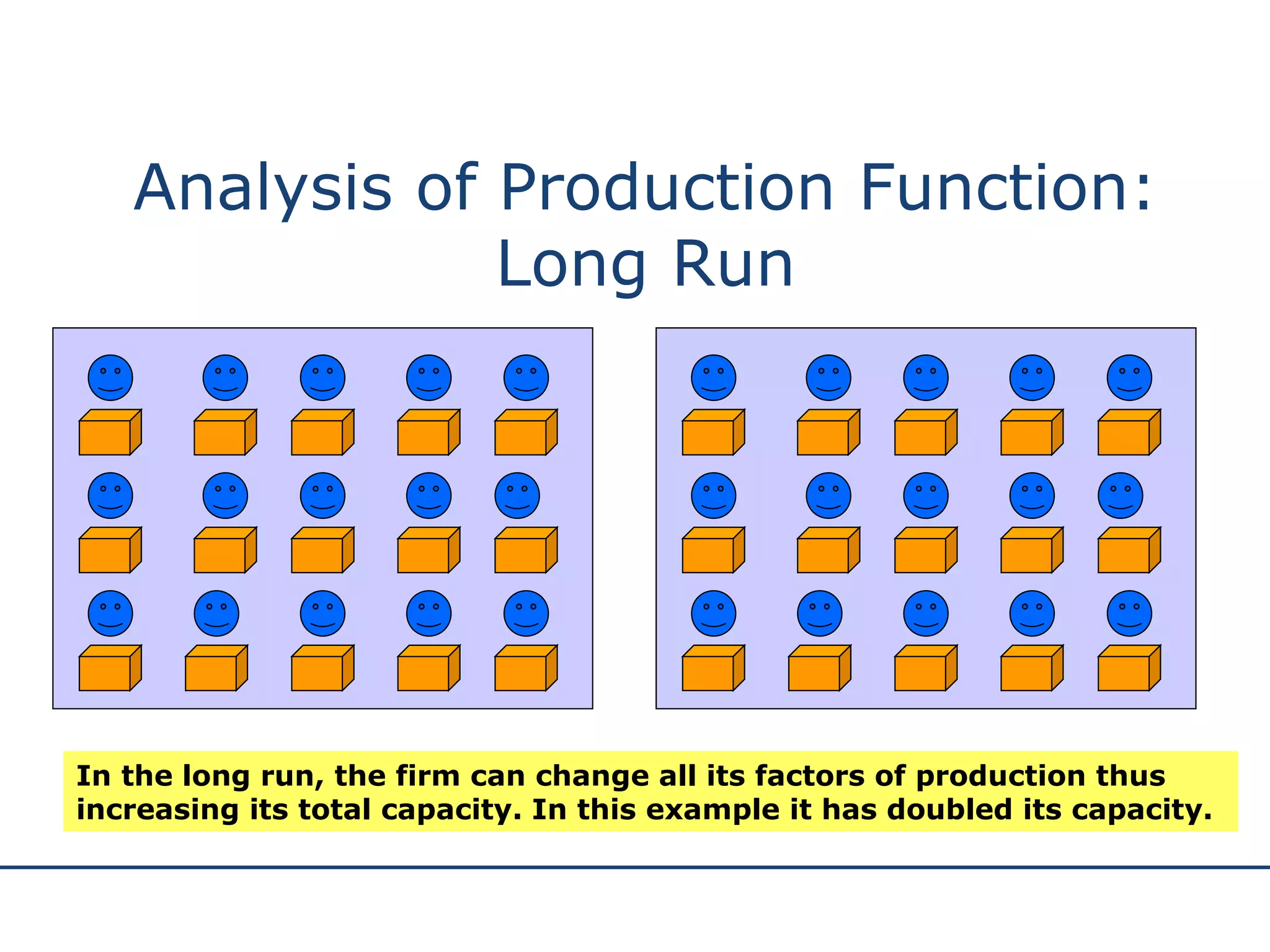

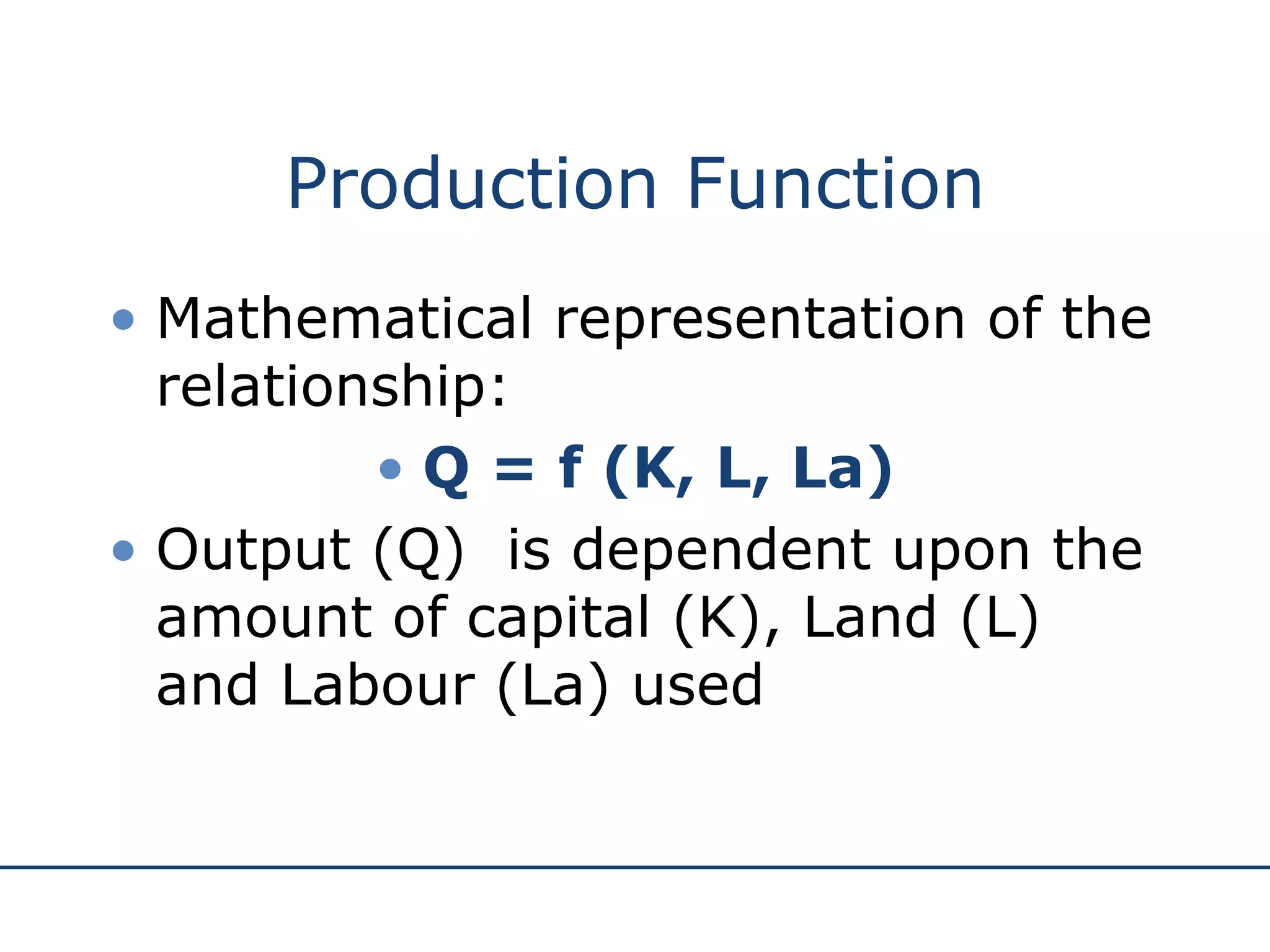

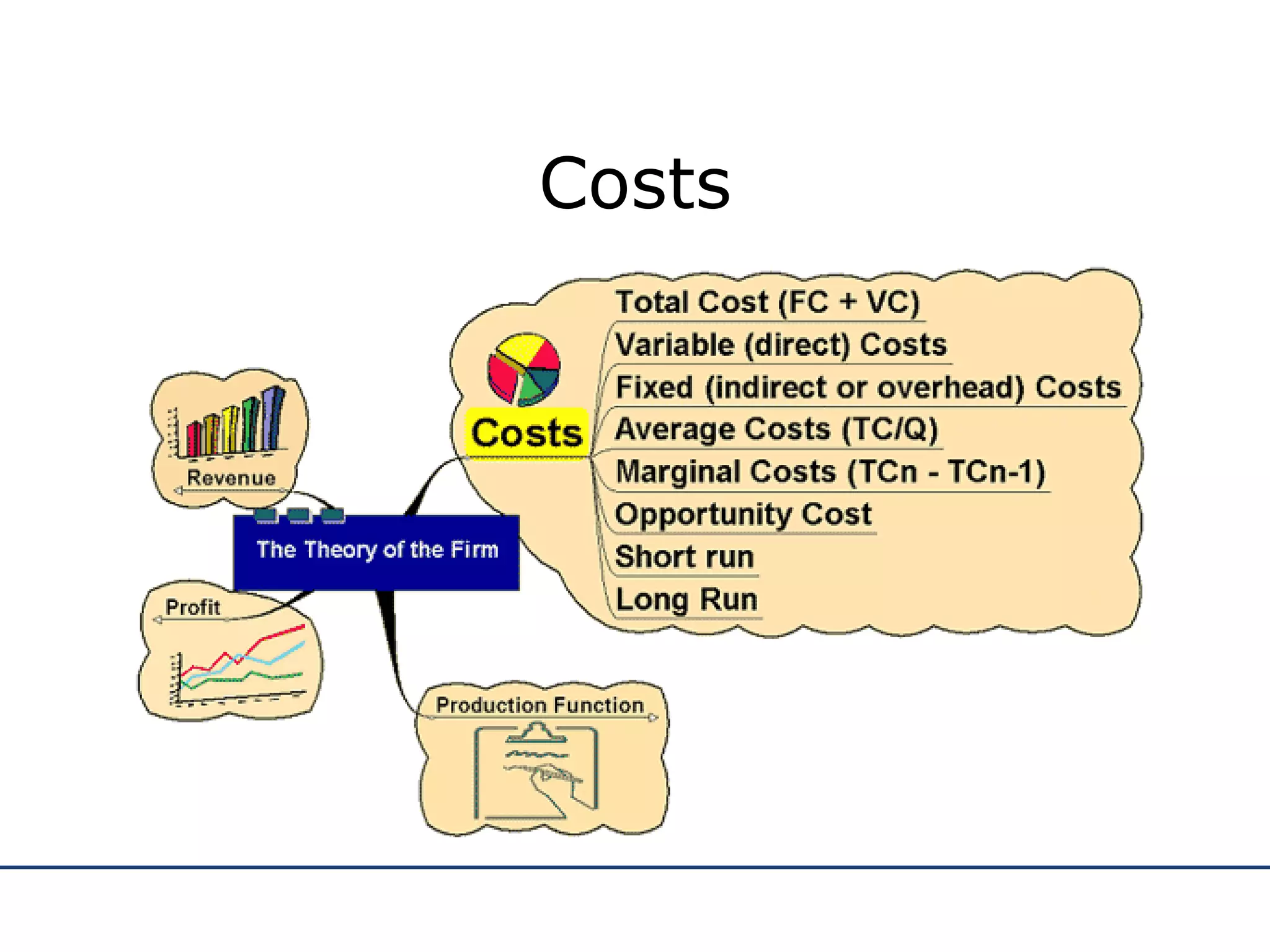

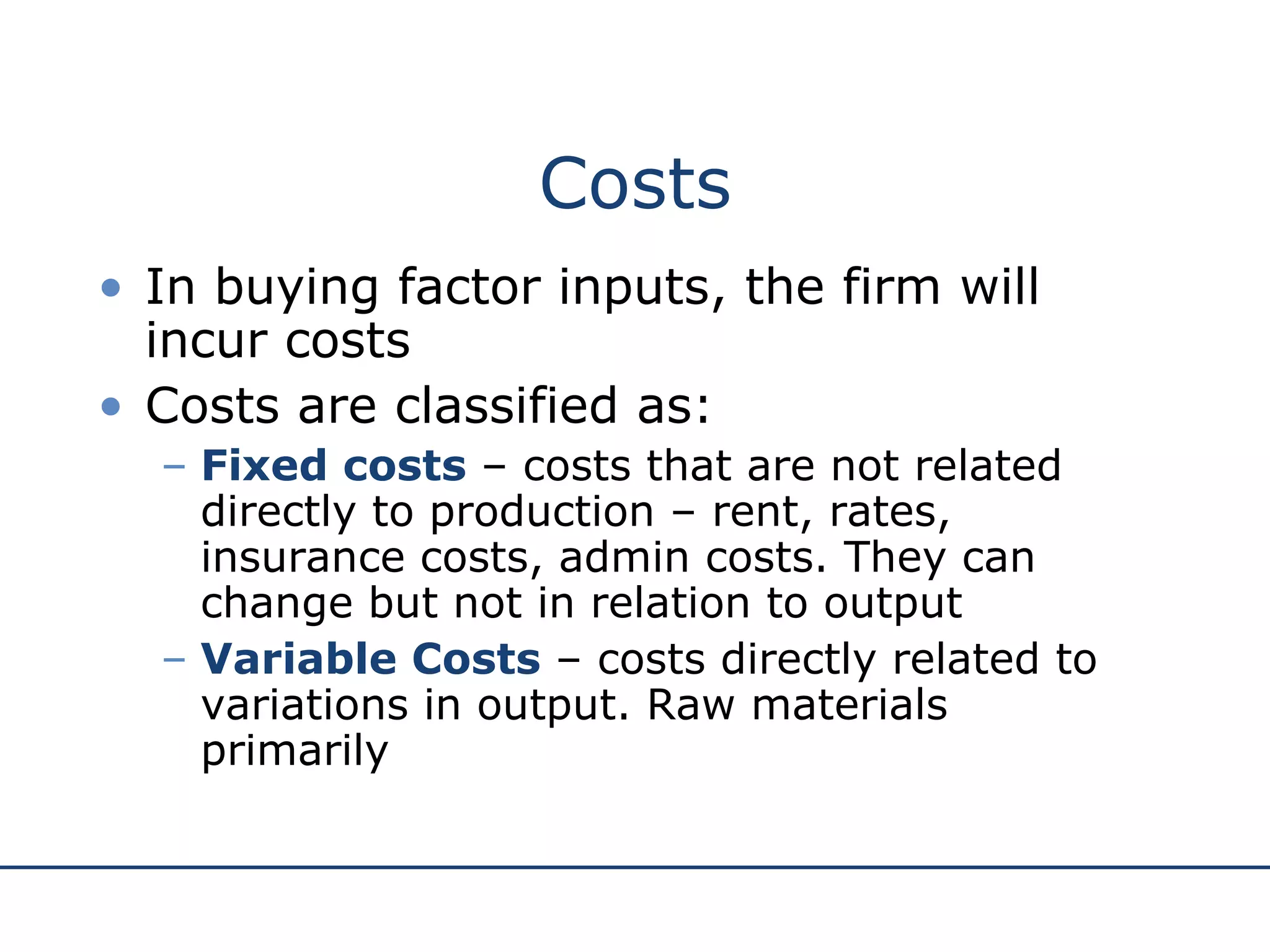

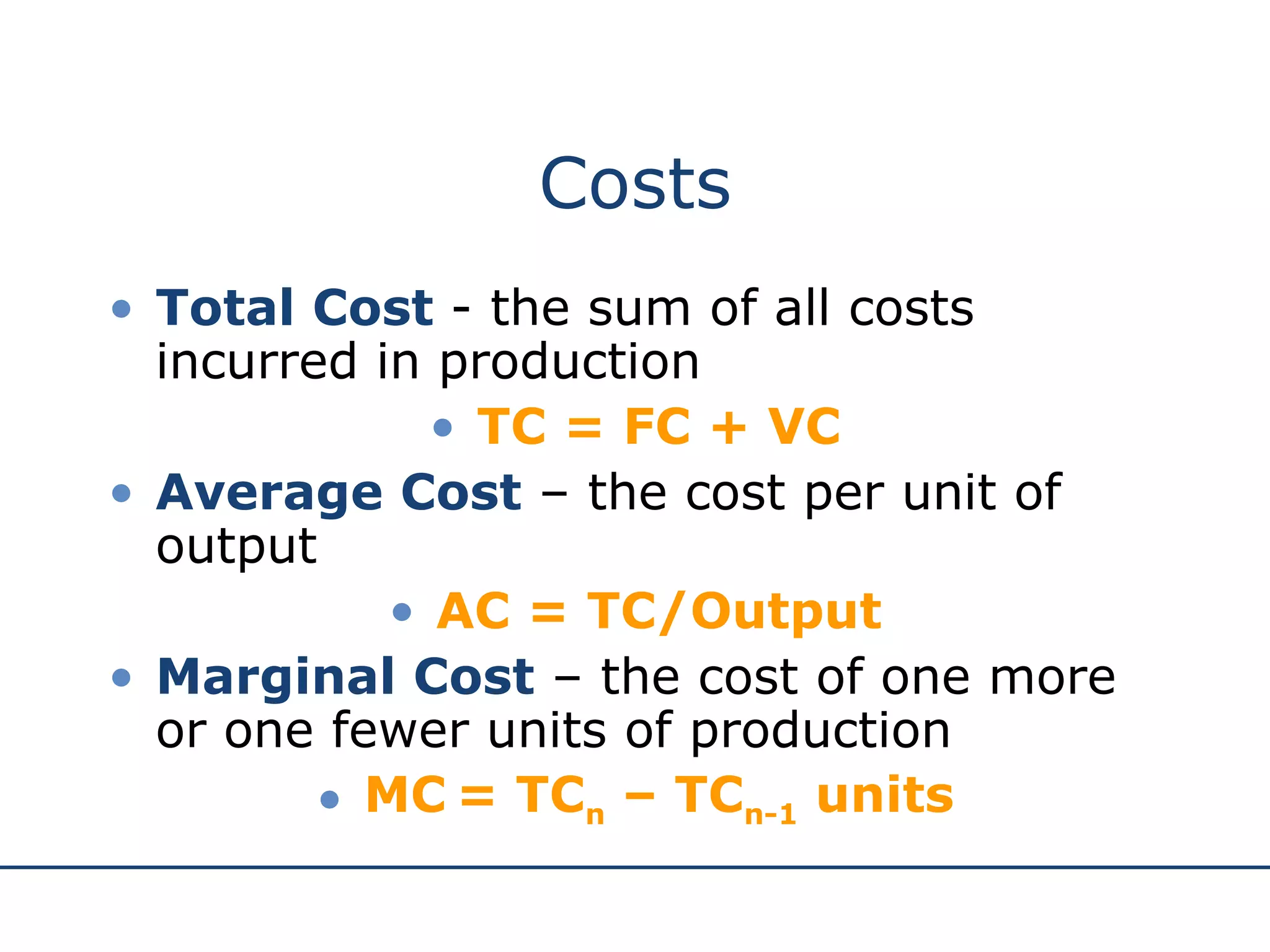

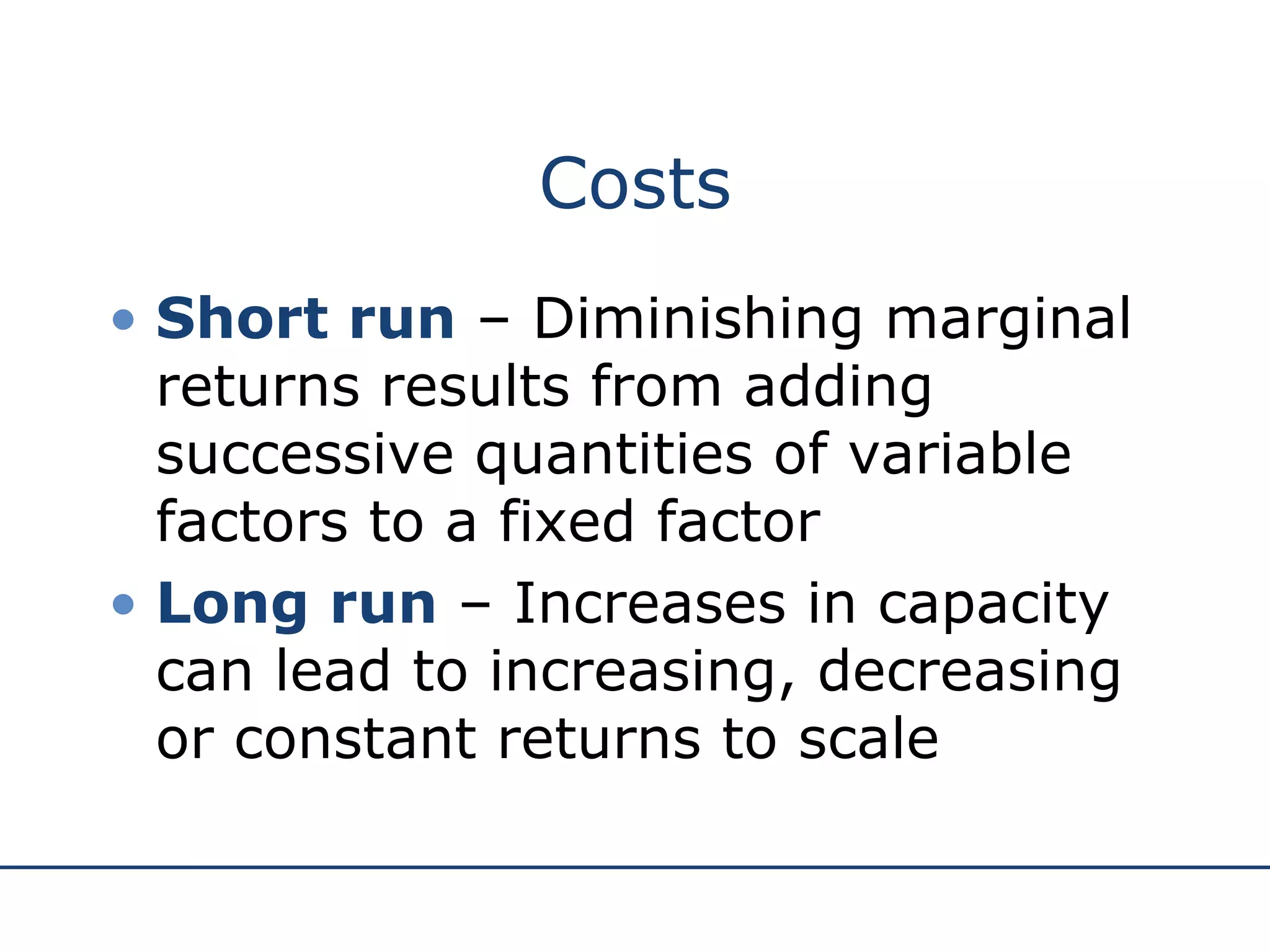

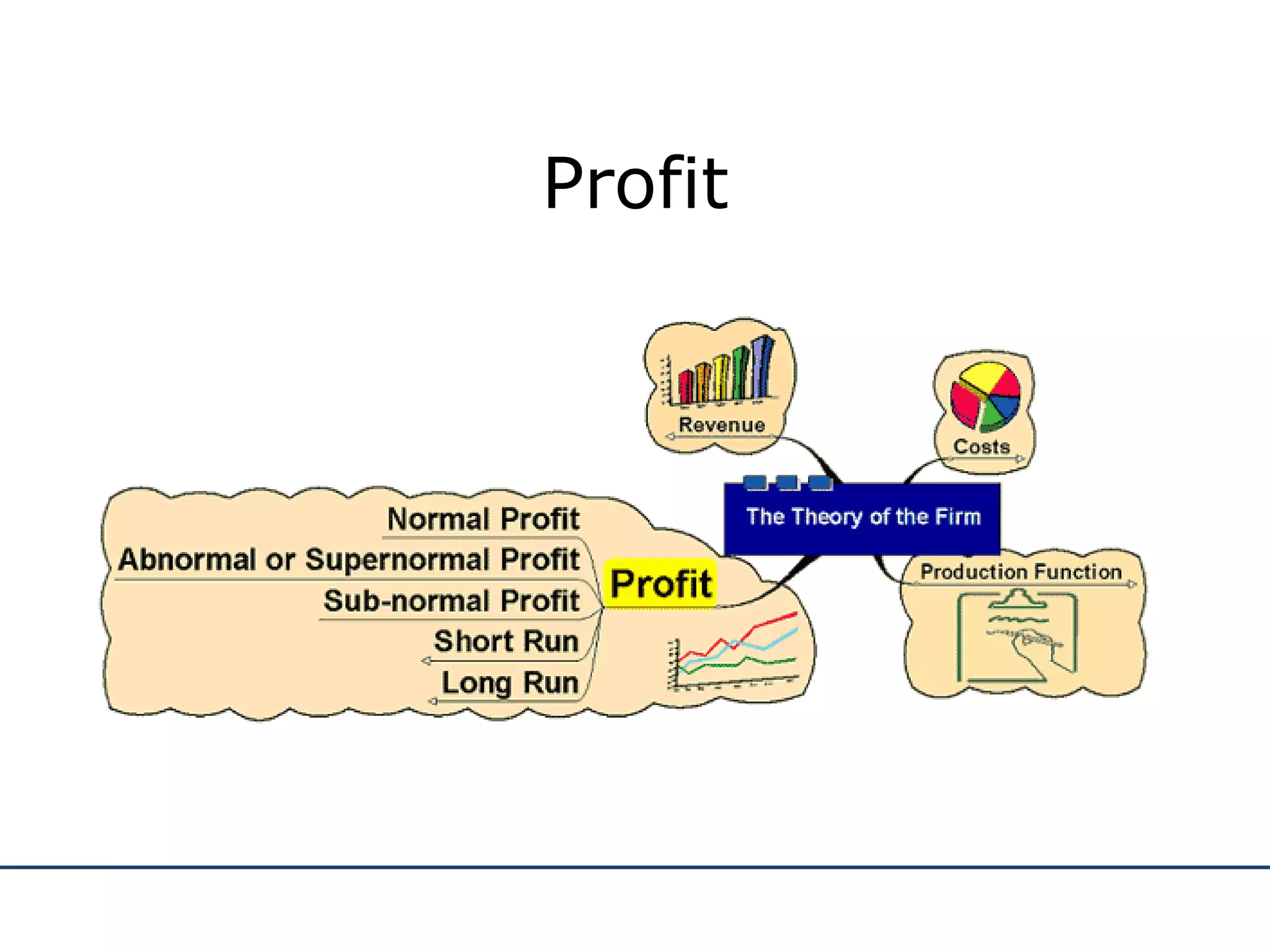

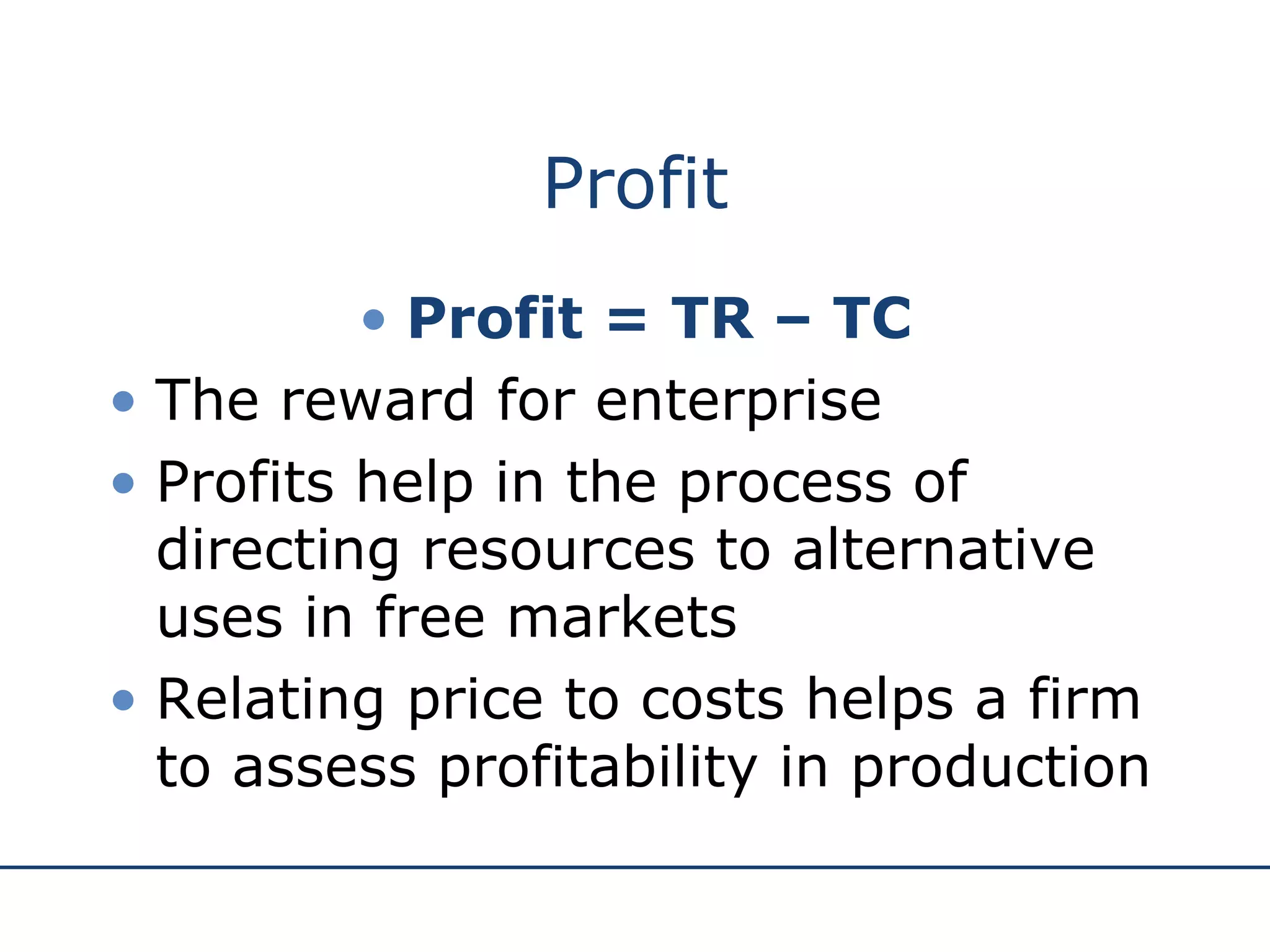

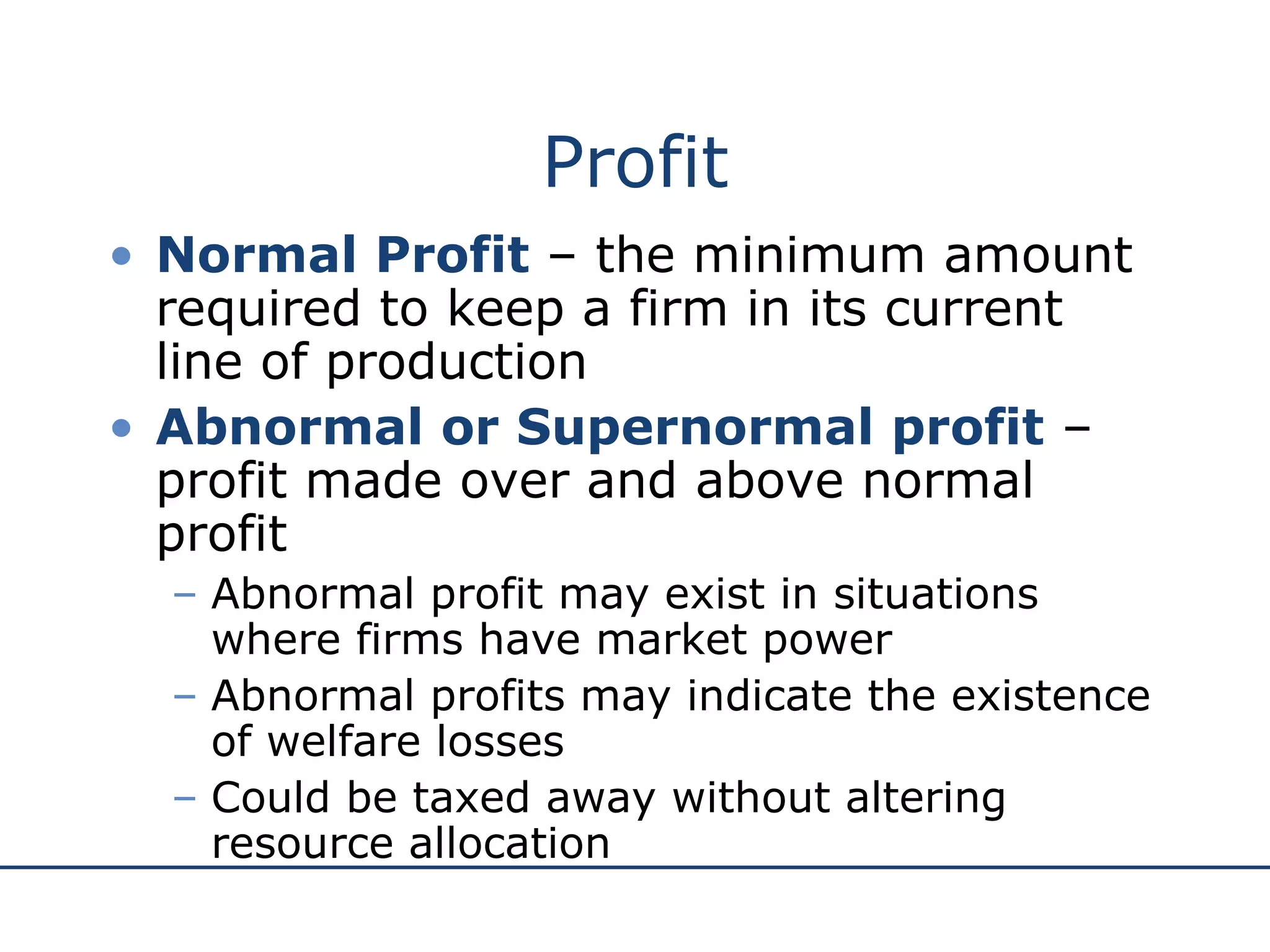

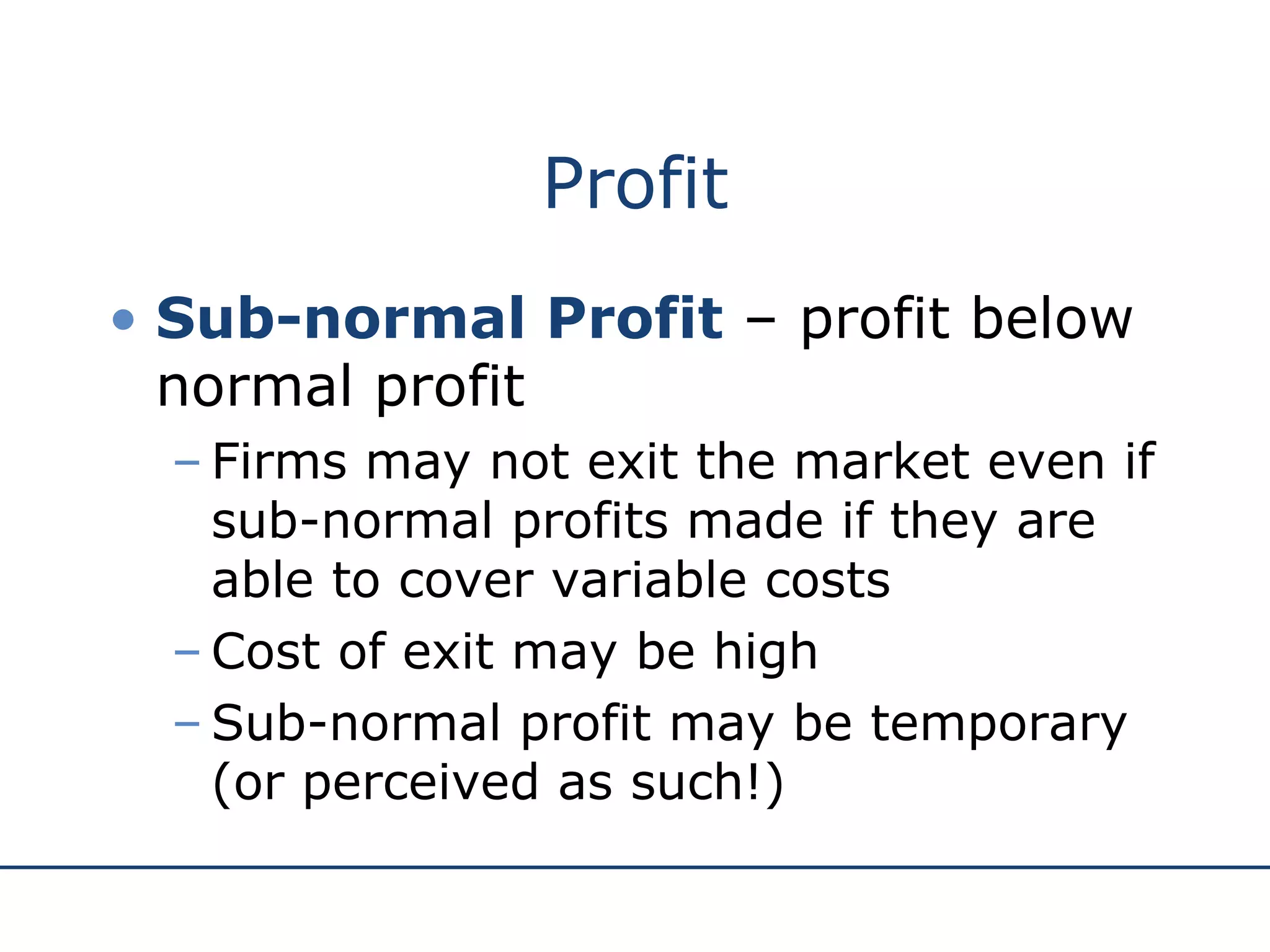

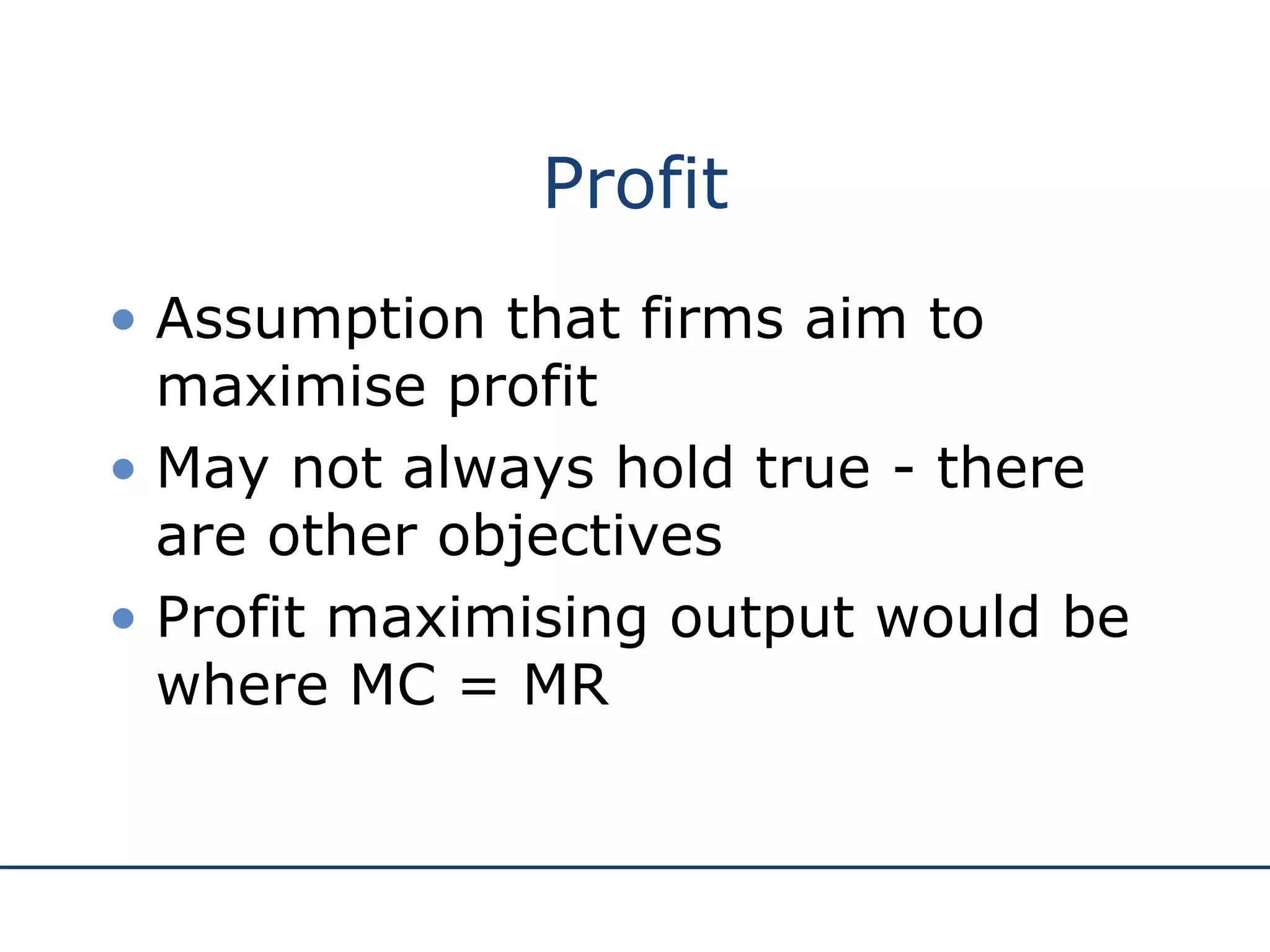

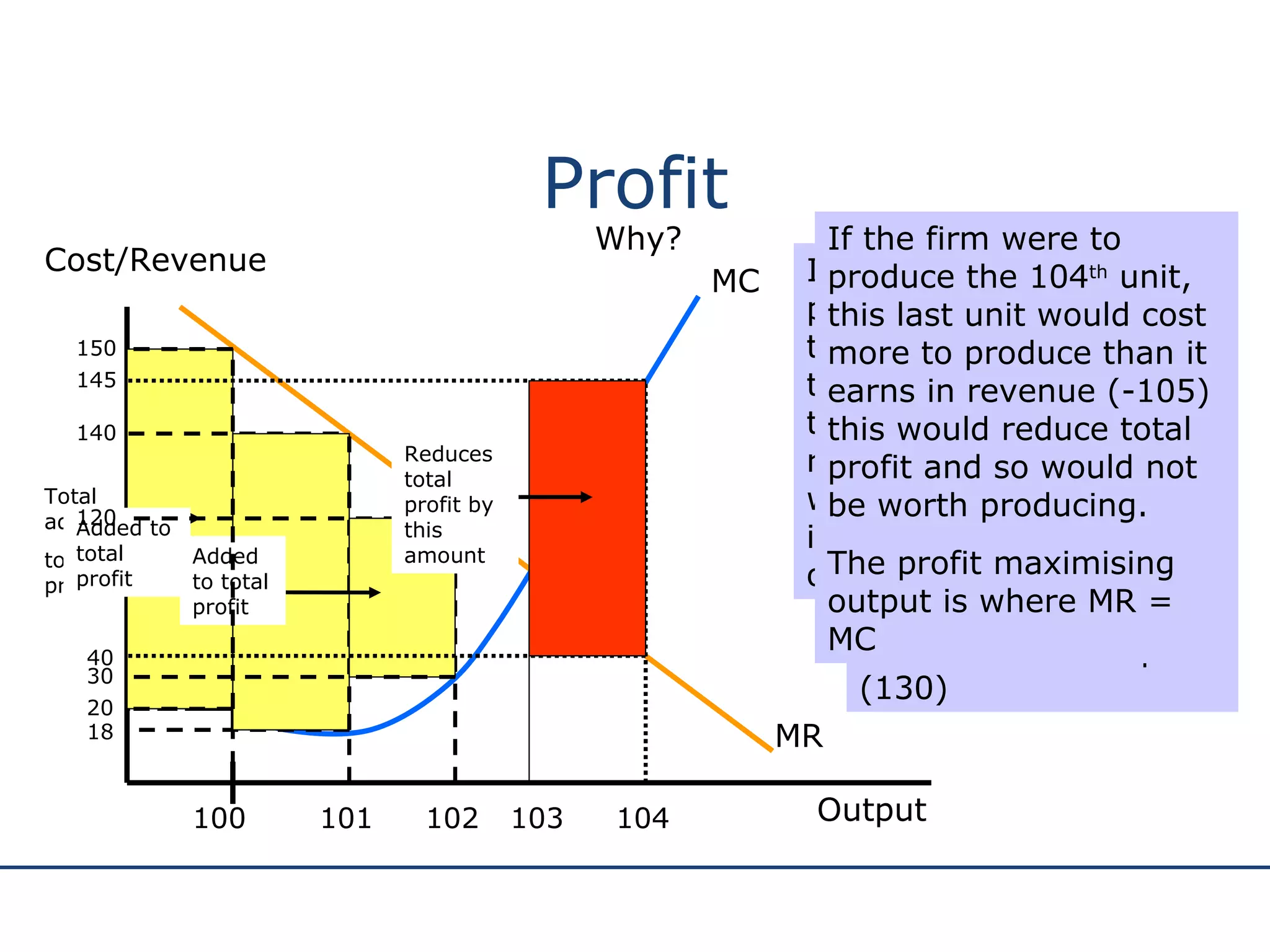

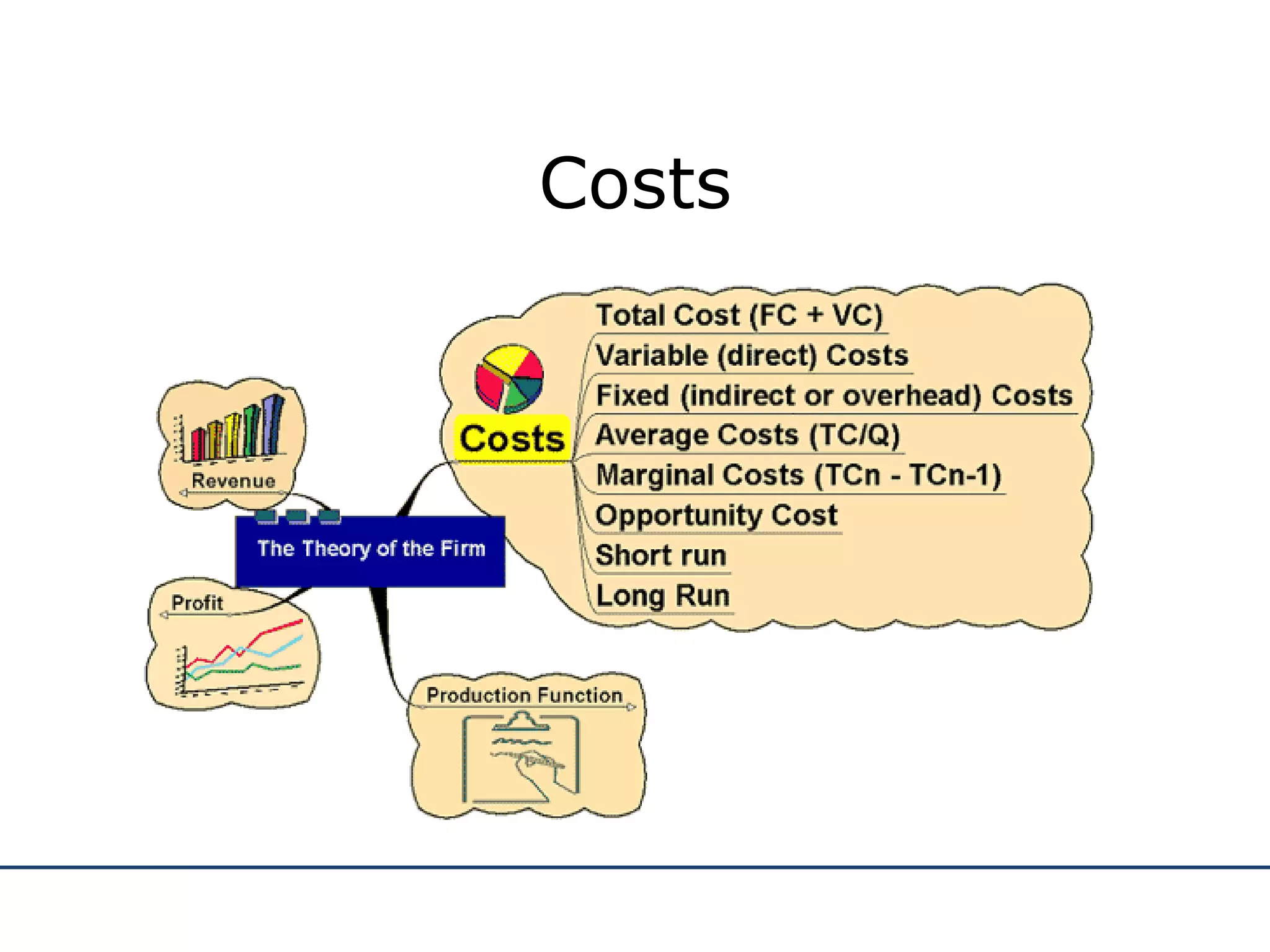

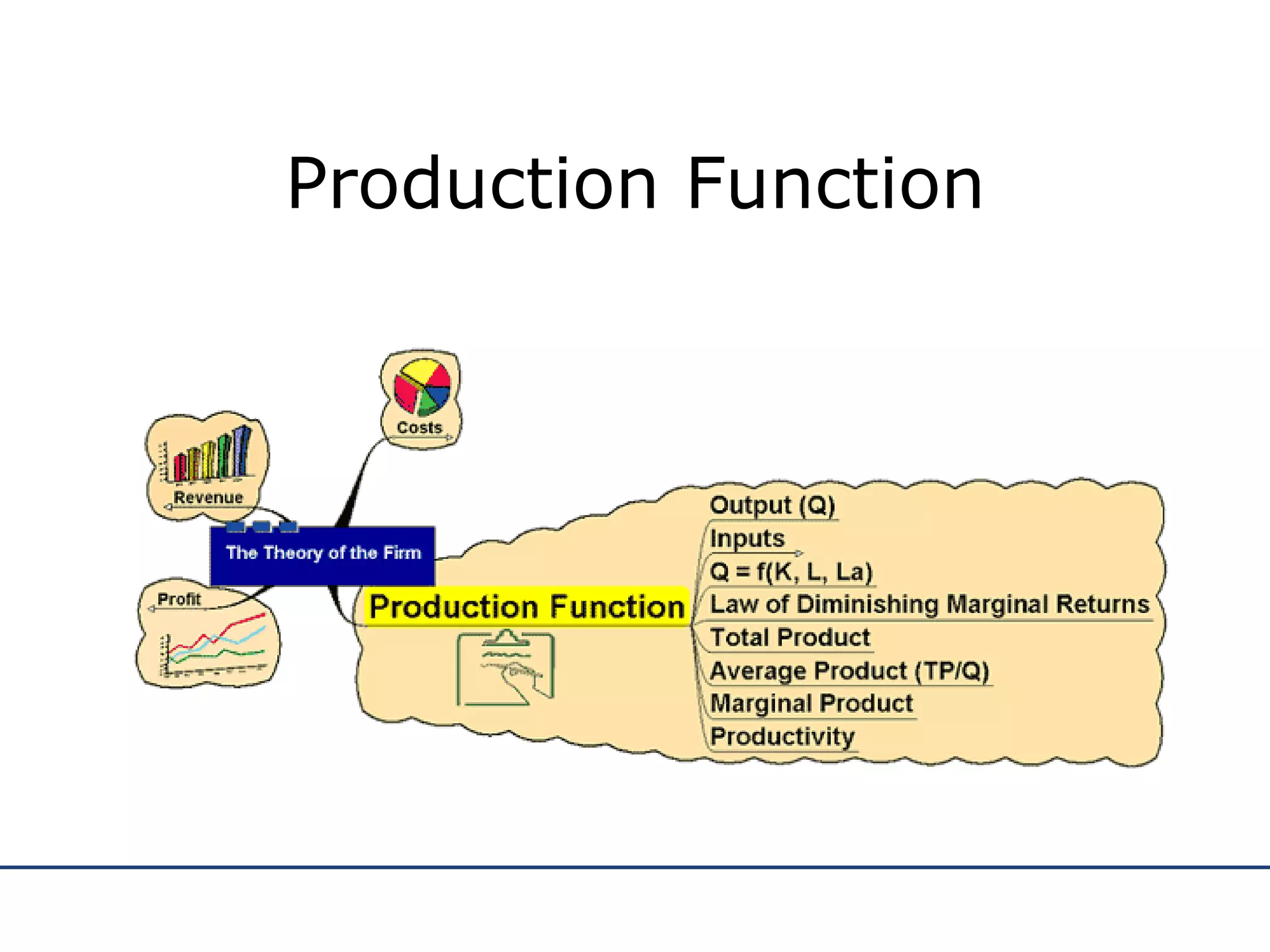

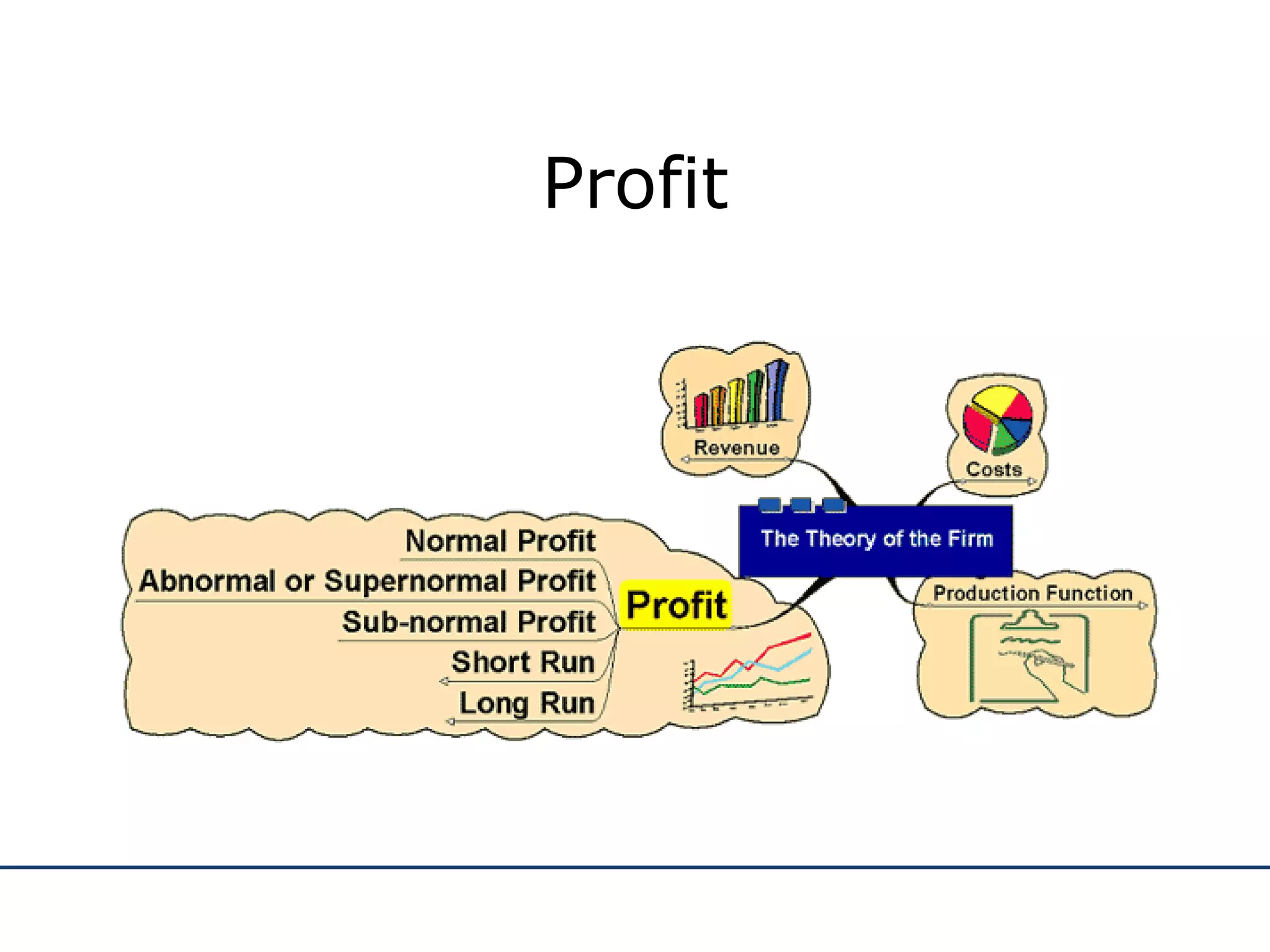

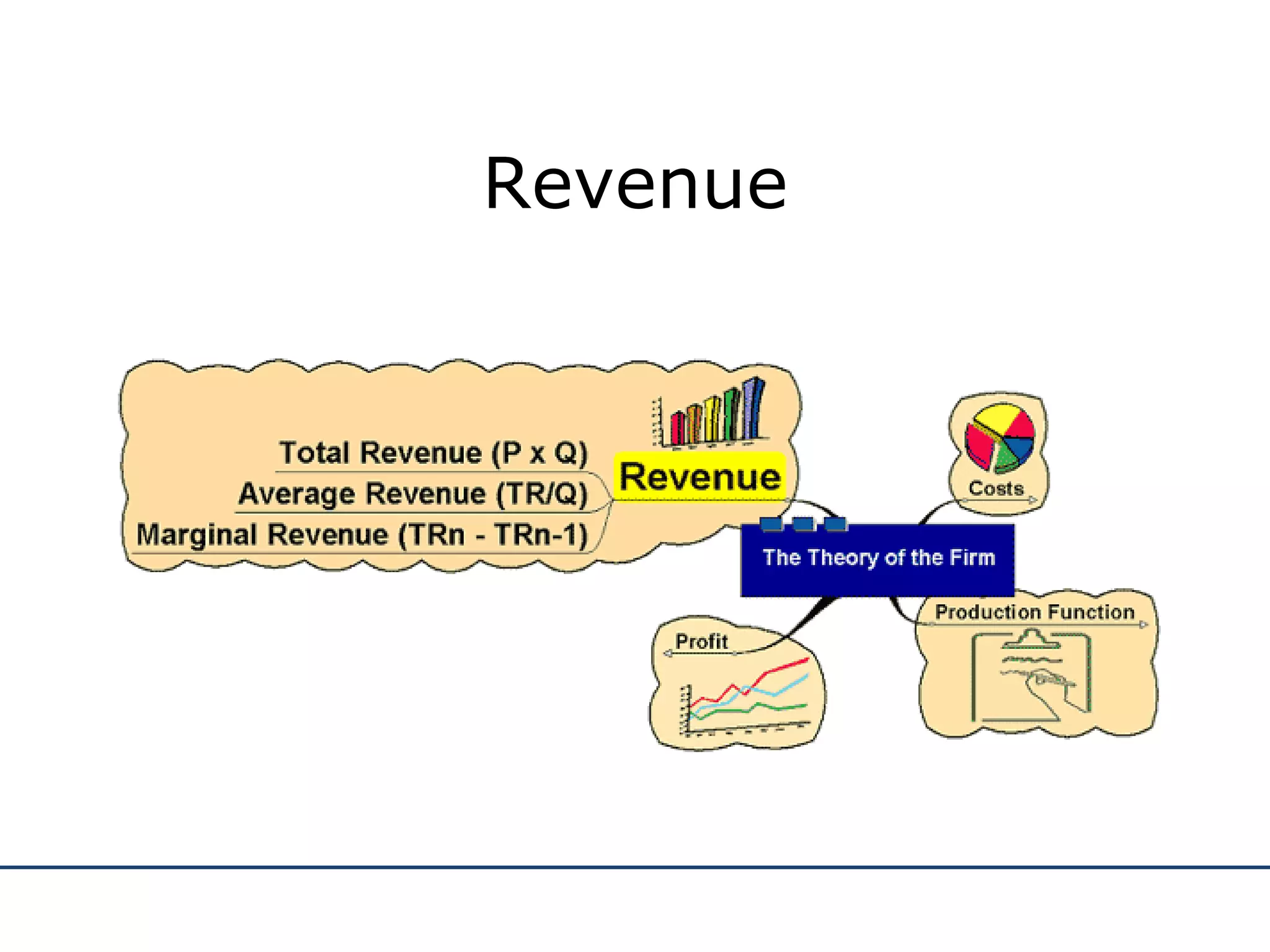

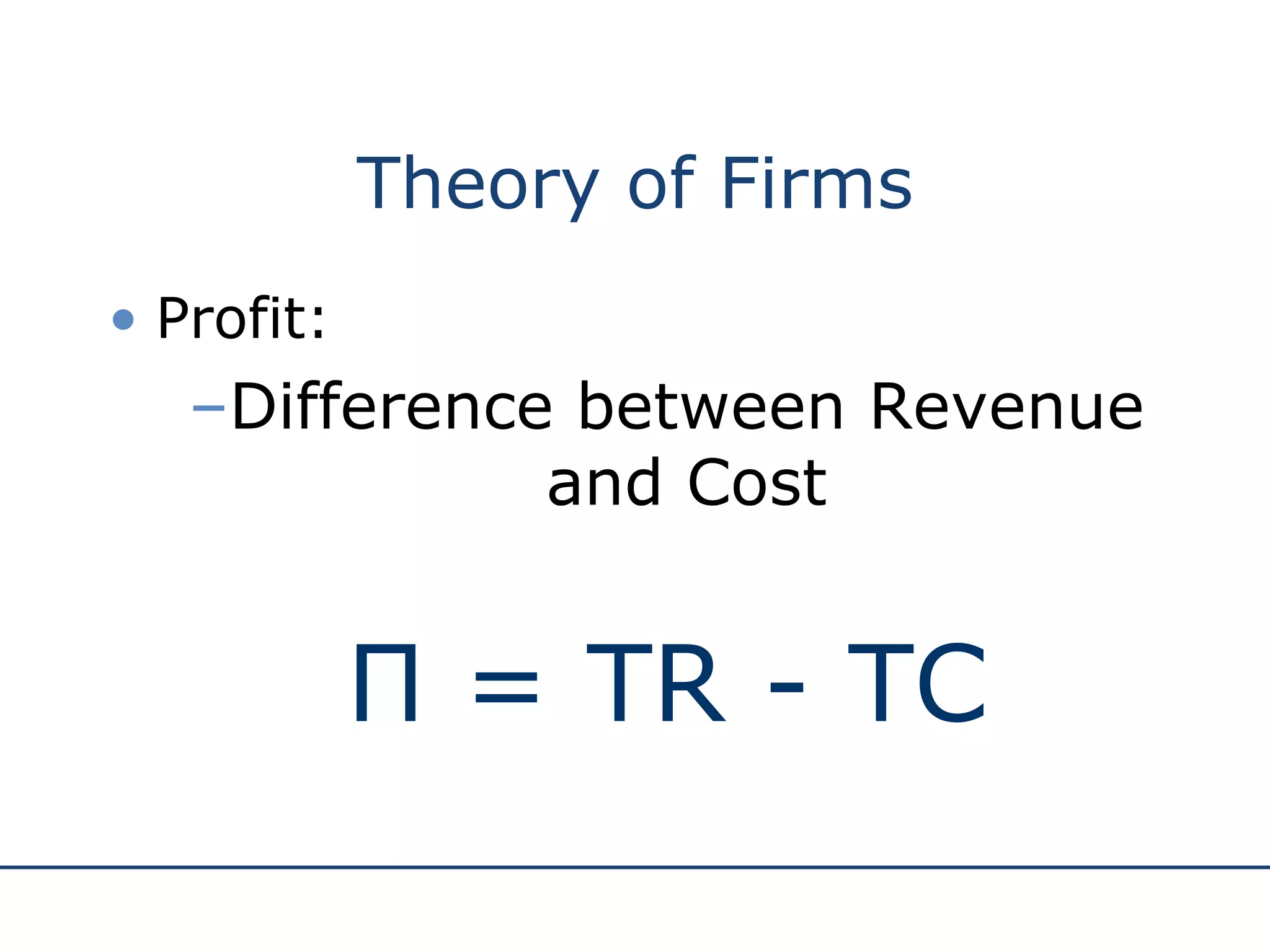

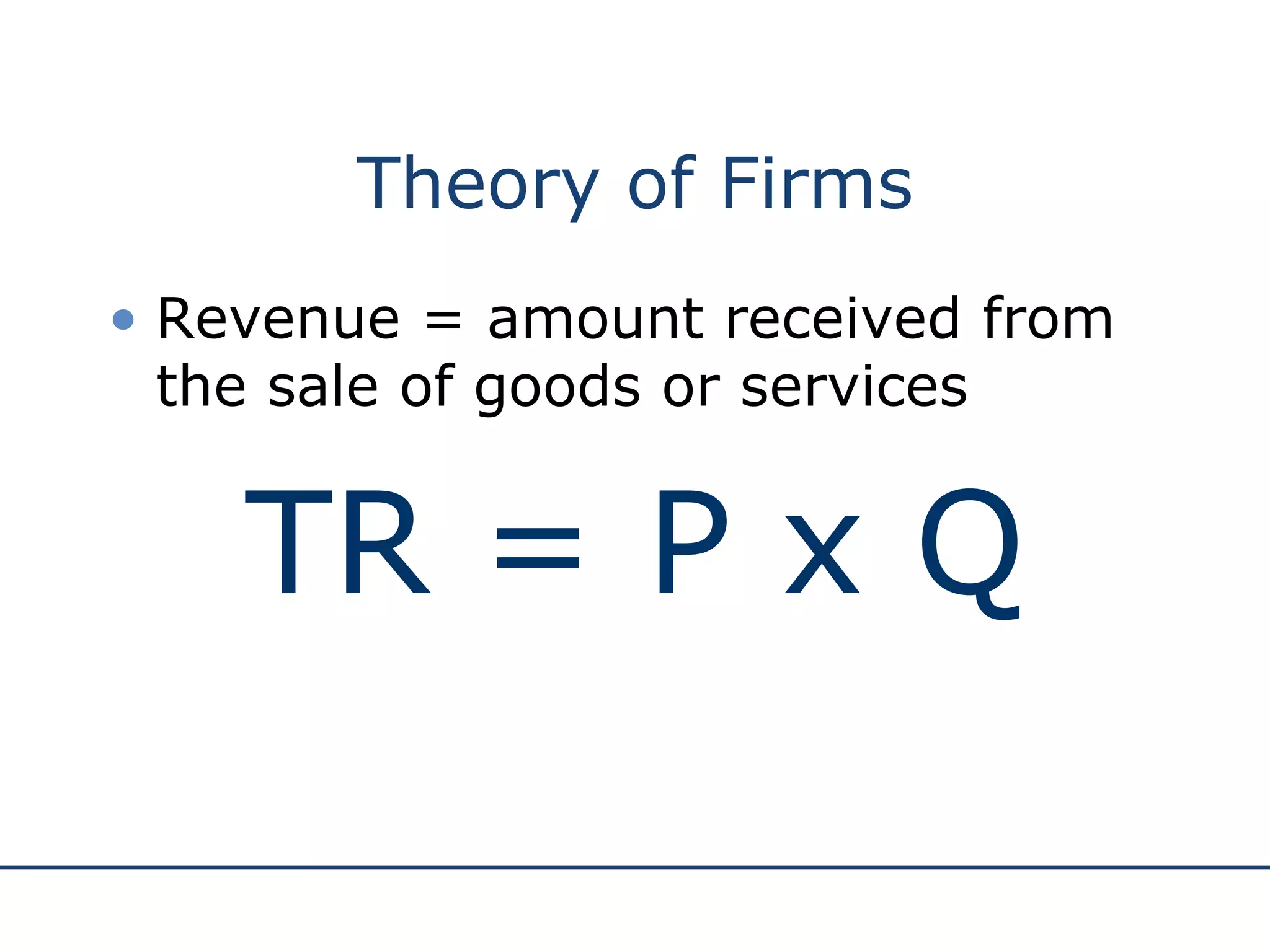

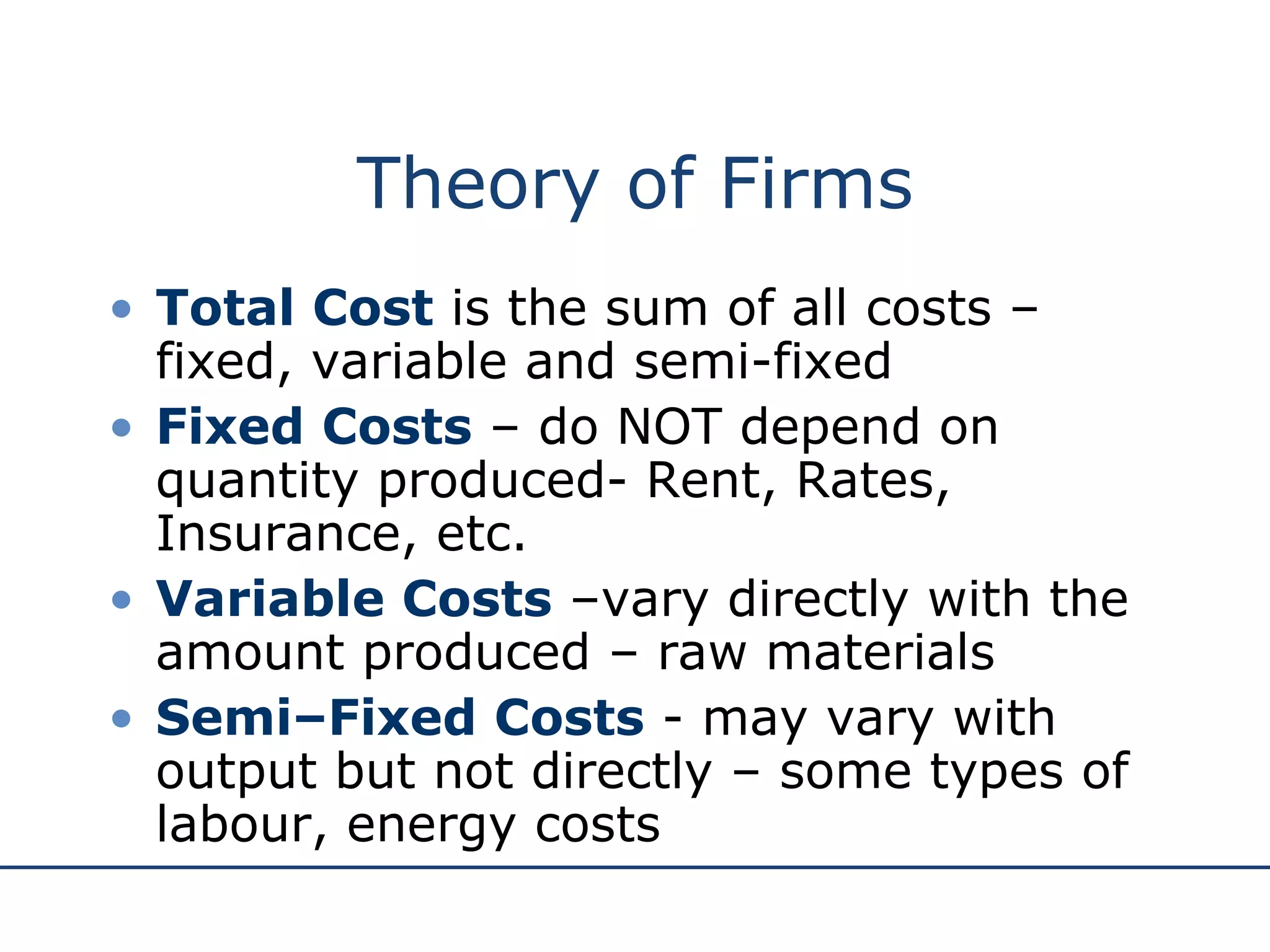

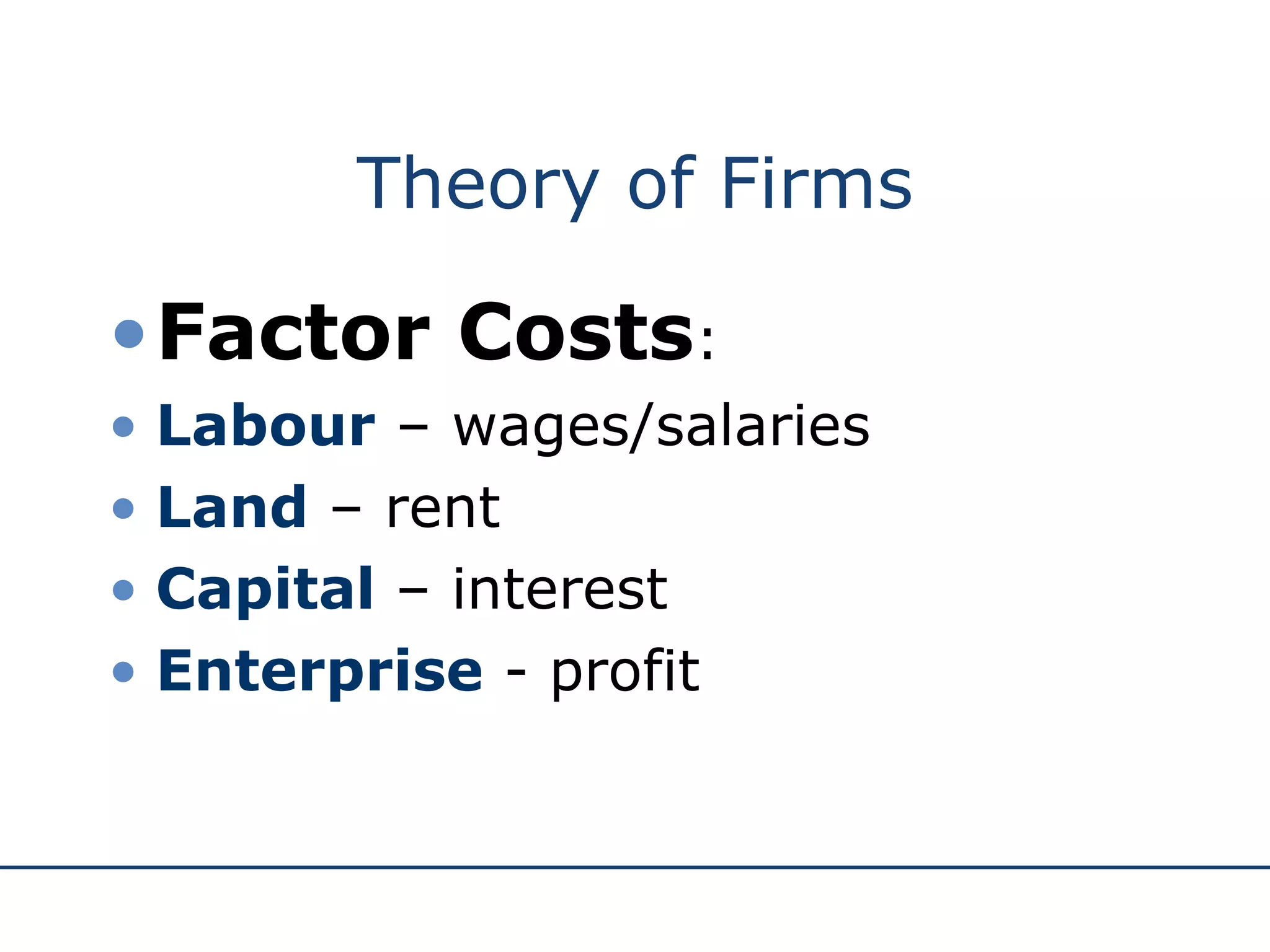

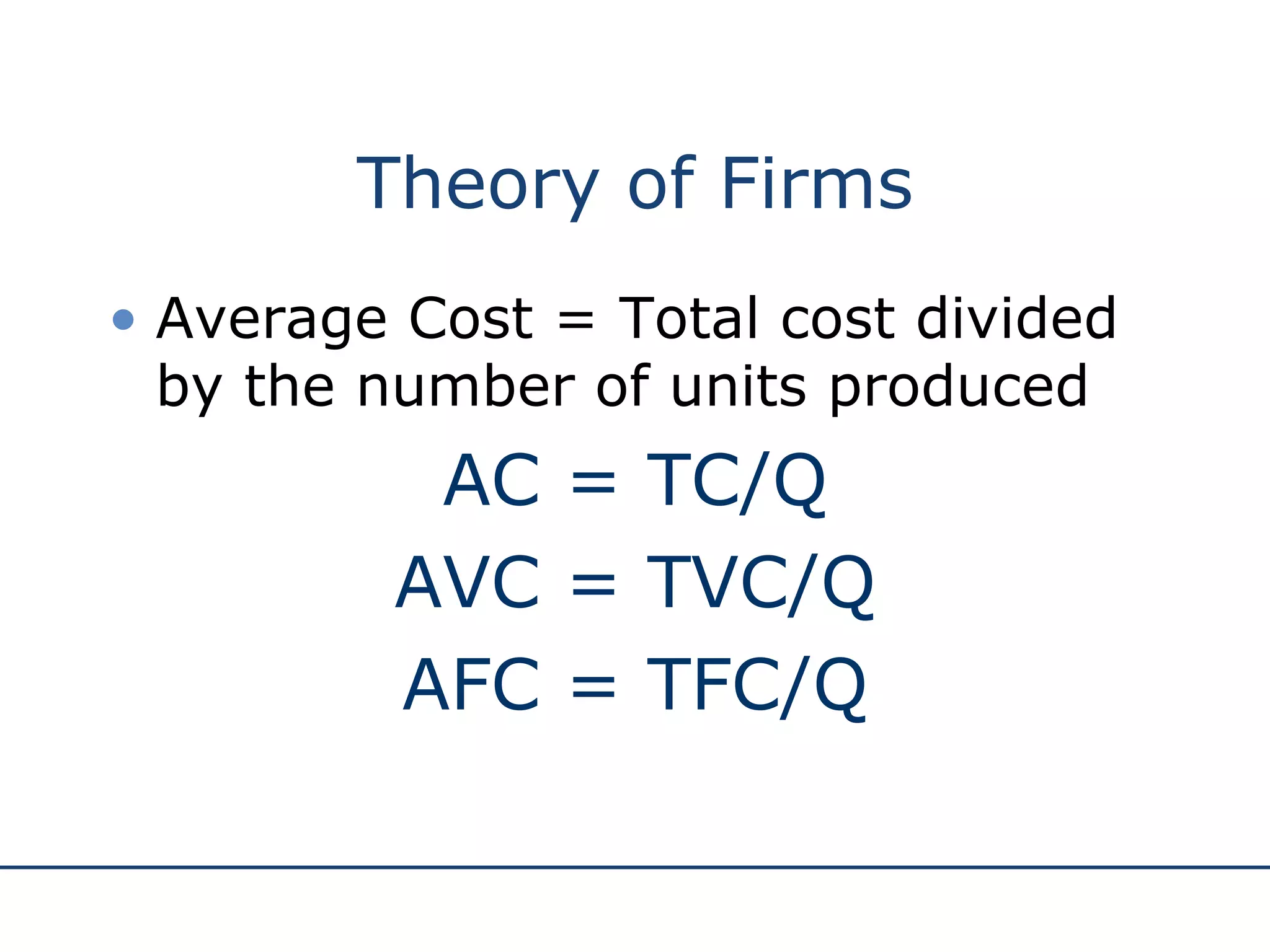

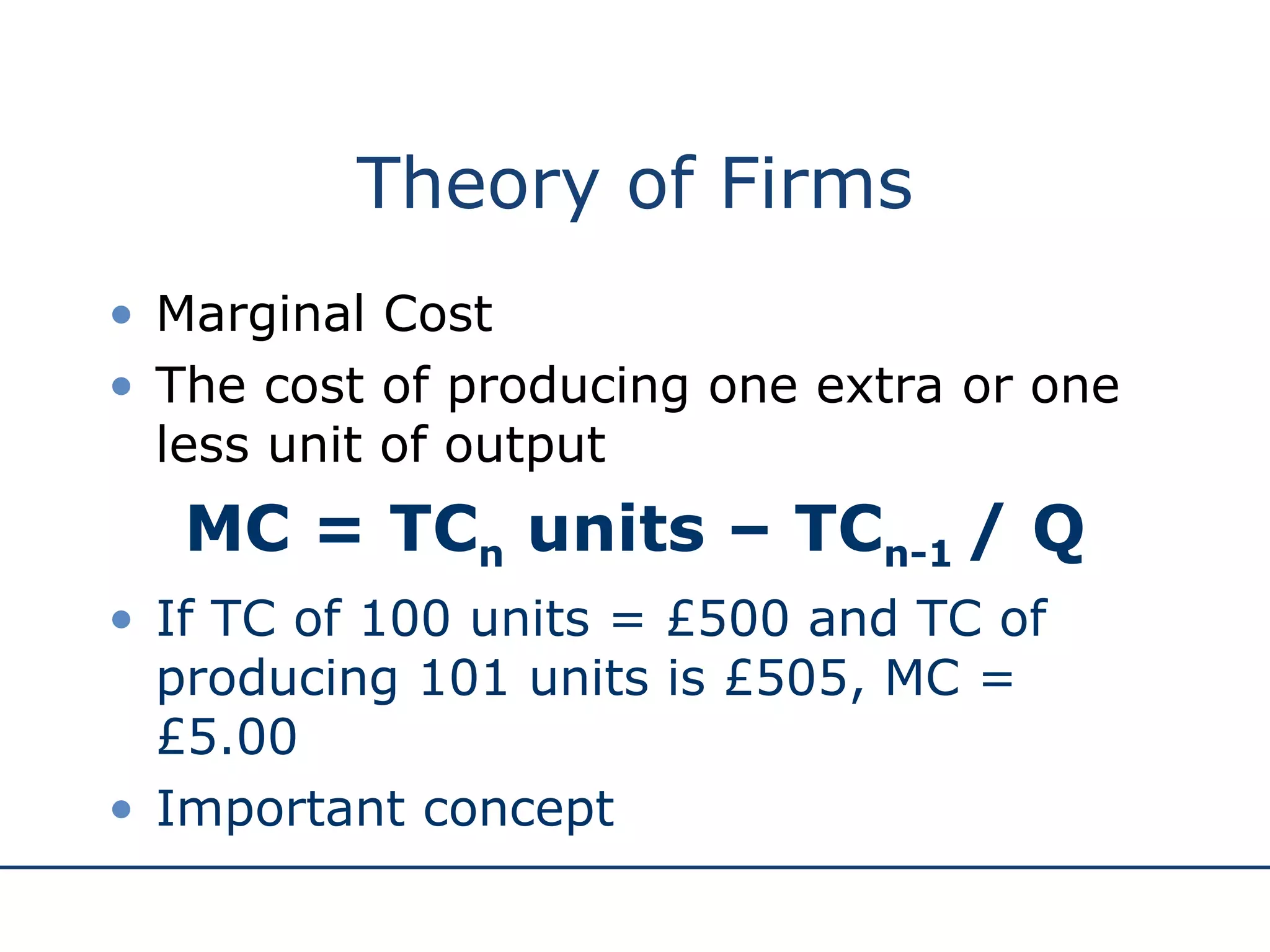

The document discusses the theory of the firm, including production functions, costs, revenues, and profit maximization. It explains that in the short run, firms have at least one fixed factor of production, while in the long run all factors are variable. It also describes how firms aim to maximize profit by producing at the quantity where marginal revenue equals marginal cost.