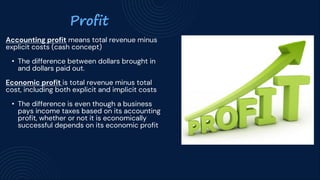

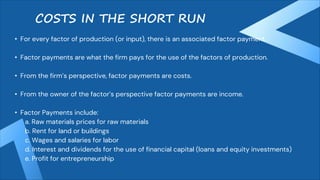

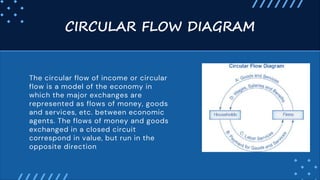

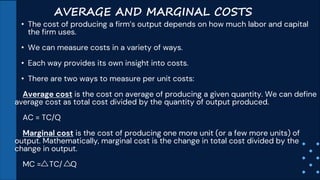

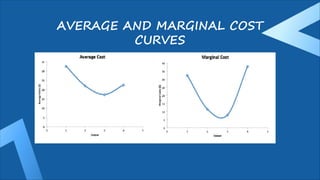

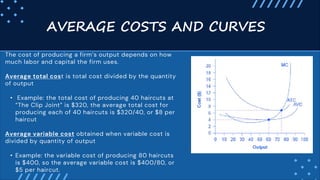

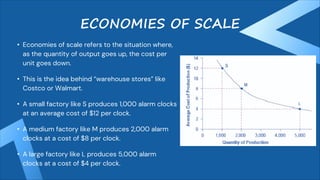

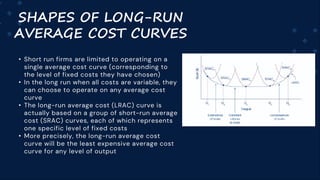

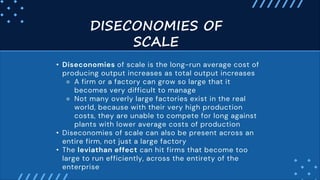

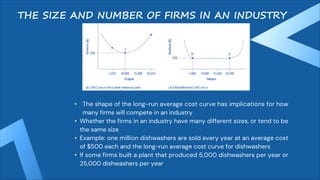

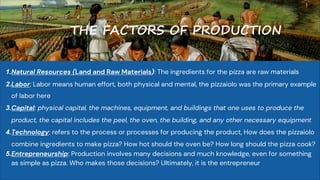

The document outlines the basic concepts of production in microeconomics, including key decisions firms must make regarding product choice, production methods, output levels, pricing, and labor employment. It discusses the distinctions between fixed and variable inputs, short-run and long-run production, and the implications of different market structures on firm behavior. Additionally, it addresses the concepts of average and marginal costs, economies of scale, and factors that influence production costs and efficiency.

![• A mathematical expression or equation that explains

the relationship between a firm’s inputs and its

outputs:

Q = F [NR,L,K,t,E]

• By plugging in the amount of labor, capital and other

inputs the firm is using, the production function tells

how much output will be produced by those inputs.

• Different products have different production

functions.

• The amount of labor a farmer uses to produce a

bushel of corn is likely different than that required to

produce an automobile.

• Firms in the same industry may have somewhat

different production functions, since each firm may

produce a little differently.

• We can describe inputs as either fixed or variable.

THE PRODUCTION FUNCTION](https://image.slidesharecdn.com/production-and-cost-basmic-group-4-241207122611-0d29b326/85/Basic-Microeconomics-PRODUCTION-AND-COST-8-320.jpg)

![VARIABLE INPUTS

Variable inputs are those that can easily be increased or

decreased in a short period of time.

• In the pizza example, the pizzaiolo can order more

ingredients with a phone call, so ingredients would be

variable inputs.

• The owner could hire a new person to work the counter

pretty quickly as well.

• Variable inputs increase or decrease as output changes.

Note:

Economics often use a short-hand form for the

production:

Q = f [L,K]

where L represents all the variables inputs, and K

represents all the fixed inputs.](https://image.slidesharecdn.com/production-and-cost-basmic-group-4-241207122611-0d29b326/85/Basic-Microeconomics-PRODUCTION-AND-COST-10-320.jpg)

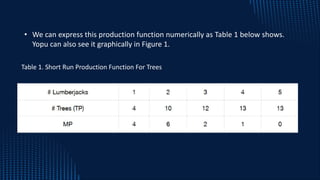

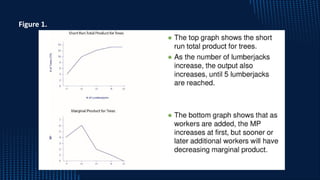

![• Note that there is another important distinction between fixed and variable

inputs.

• In the short run, since the firm’s fixed inputs are fixed, the only way to vary a

firm’s output is by changing its variable inputs.

• Example: tree-cutting with a two-person crosscut saw.

• Since by definition capital is fixed in the short run, our production function

becomes:

Q=f [L, K] or Q = f [L]

• This equation simply indicates that since capital is fixed, then changing the

amount of output (e.g. trees cut down per day) depends only on changing the

amount of labor employed (e.g. number of lumberjacks working).

Short Run](https://image.slidesharecdn.com/production-and-cost-basmic-group-4-241207122611-0d29b326/85/Basic-Microeconomics-PRODUCTION-AND-COST-12-320.jpg)