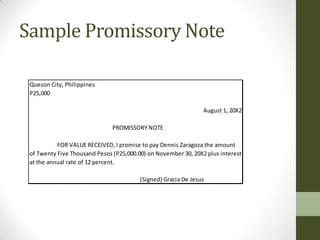

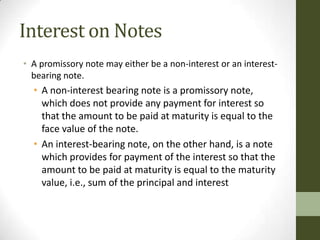

This document discusses accounting for promissory notes. It defines a promissory note as a written promise to pay a fixed amount of money at a future date, which may include interest. It provides a sample promissory note and identifies the key components of a note, including the maker, payee, principal amount, interest rate, maturity date, and place of issue. It describes how promissory notes can arise from transactions like services on credit, outstanding accounts, or loans. Finally, it distinguishes between non-interest bearing notes and interest-bearing notes.