The document discusses accounting periods, the accounting cycle, journalizing transactions, debit and credit rules, and the journal entry process. It defines accounting periods as segments of time used to prepare financial statements and shows the typical steps in an accounting cycle. It also explains that journalizing records transactions in journals using debit and credit rules, and that a journal entry displays all effects of a transaction through debits and credits with an explanation.

This powerpoint presentation is created by Gyanbikash.com for the students of class nine to ten from their accounting NCTB textbook for multimedia class.

BASIC ACCOUNTING FOR ALL INCLUDING MANAGERS. ACCOUNTING, DOUBLE ENTRY SYSTEM, JOURNEL (defination,advantages/limitations, how to make,) TRAIL BALANCE(defination,limitations/advantages, steps}

This powerpoint presentation is created by Gyanbikash.com for the students of class nine to ten from their accounting NCTB textbook for multimedia class.

BASIC ACCOUNTING FOR ALL INCLUDING MANAGERS. ACCOUNTING, DOUBLE ENTRY SYSTEM, JOURNEL (defination,advantages/limitations, how to make,) TRAIL BALANCE(defination,limitations/advantages, steps}

Trial balance and rectification of errorsItisha Sharma

Trial balance and rectification of errors, Introduction- Specimen of a Trial Balance- Errors and their rectification – Rectification of errors Rectification of errors detected after the preparation of Trial Balance but before the preparation of Final Accounts- Effect of errors on Profit – Rectification of errors appearing after the preparation of Final Accounts

Social development club is a leading course content provider of India with a key focus on skilling courseware development. We deliver complete package required to deliver the Skill development program effectively. We develop NCVT and SSC aligned courses of all the domains and for all the schemes.

Contact: sdccourses@gmail.com, http://www.socialdevelopment.club

Recording of Business Transactions. Defination of Journal...Blogger

Recording of Business Transaction

Recording of Business transaction is vital to a business's financial statements and a key responsibility of the accounting department. Learn the definition of a transaction, understand the importance of recording transactions, and explore the process of double-entry accounting, with examples of credits and debits

Meaning of Journal

The journal or journal is the primary or basic book of the traders. This is the register in which all business transactions are entered date wise. In this, the accounts are made in the same order in which the transactions have taken place in the business. The word 'Journal' is derived from the French word 'Jour' which means day book, diary or 'day'. It is called 'Day' or 'Din' or 'Rose' in Hindi. By adding nal in Jour, a Journal was created, whose Hindi translation is 'Roznamcha'. Therefore, Journal or Roznamcha means daily account. Since in this the transactions are recorded from the Waste Book or the Remembrance Book (or Commemorative Book), so it is also called the Permit Book. Thus, since entries are made in it every day according to date, hence it is also called daily register or daily record.

Thus, Journal is that book in which initial accounting of both the aspects of all business transactions is done date wise and according to the rules. Therefore, according to a learned writer, “The book in which all business transactions are written in a systematic manner in the beginning, it is called journal

Definition of Journal

"The journal or 'daily record' is that book of primary entries in which date wise transactions are recorded from the memory book or the junk itself. While writing the entries, they are in the form of debit and credit. It is classified, so that later it is convenient to do correct posting in the ledger. "

Trial balance and rectification of errorsItisha Sharma

Trial balance and rectification of errors, Introduction- Specimen of a Trial Balance- Errors and their rectification – Rectification of errors Rectification of errors detected after the preparation of Trial Balance but before the preparation of Final Accounts- Effect of errors on Profit – Rectification of errors appearing after the preparation of Final Accounts

Social development club is a leading course content provider of India with a key focus on skilling courseware development. We deliver complete package required to deliver the Skill development program effectively. We develop NCVT and SSC aligned courses of all the domains and for all the schemes.

Contact: sdccourses@gmail.com, http://www.socialdevelopment.club

Recording of Business Transactions. Defination of Journal...Blogger

Recording of Business Transaction

Recording of Business transaction is vital to a business's financial statements and a key responsibility of the accounting department. Learn the definition of a transaction, understand the importance of recording transactions, and explore the process of double-entry accounting, with examples of credits and debits

Meaning of Journal

The journal or journal is the primary or basic book of the traders. This is the register in which all business transactions are entered date wise. In this, the accounts are made in the same order in which the transactions have taken place in the business. The word 'Journal' is derived from the French word 'Jour' which means day book, diary or 'day'. It is called 'Day' or 'Din' or 'Rose' in Hindi. By adding nal in Jour, a Journal was created, whose Hindi translation is 'Roznamcha'. Therefore, Journal or Roznamcha means daily account. Since in this the transactions are recorded from the Waste Book or the Remembrance Book (or Commemorative Book), so it is also called the Permit Book. Thus, since entries are made in it every day according to date, hence it is also called daily register or daily record.

Thus, Journal is that book in which initial accounting of both the aspects of all business transactions is done date wise and according to the rules. Therefore, according to a learned writer, “The book in which all business transactions are written in a systematic manner in the beginning, it is called journal

Definition of Journal

"The journal or 'daily record' is that book of primary entries in which date wise transactions are recorded from the memory book or the junk itself. While writing the entries, they are in the form of debit and credit. It is classified, so that later it is convenient to do correct posting in the ledger. "

Introduction to Indian Financial System ()Avanish Goel

The financial system of a country is an important tool for economic development of the country, as it helps in creation of wealth by linking savings with investments.

It facilitates the flow of funds form the households (savers) to business firms (investors) to aid in wealth creation and development of both the parties

how to swap pi coins to foreign currency withdrawable.DOT TECH

As of my last update, Pi is still in the testing phase and is not tradable on any exchanges.

However, Pi Network has announced plans to launch its Testnet and Mainnet in the future, which may include listing Pi on exchanges.

The current method for selling pi coins involves exchanging them with a pi vendor who purchases pi coins for investment reasons.

If you want to sell your pi coins, reach out to a pi vendor and sell them to anyone looking to sell pi coins from any country around the globe.

Below is the contact information for my personal pi vendor.

Telegram: @Pi_vendor_247

Exploring Abhay Bhutada’s Views After Poonawalla Fincorp’s Collaboration With...beulahfernandes8

The financial landscape in India has witnessed a significant development with the recent collaboration between Poonawalla Fincorp and IndusInd Bank.

The launch of the co-branded credit card, the IndusInd Bank Poonawalla Fincorp eLITE RuPay Platinum Credit Card, marks a major milestone for both entities.

This strategic move aims to redefine and elevate the banking experience for customers.

How to get verified on Coinbase Account?_.docxBuy bitget

t's important to note that buying verified Coinbase accounts is not recommended and may violate Coinbase's terms of service. Instead of searching to "buy verified Coinbase accounts," follow the proper steps to verify your own account to ensure compliance and security.

Currently pi network is not tradable on binance or any other exchange because we are still in the enclosed mainnet.

Right now the only way to sell pi coins is by trading with a verified merchant.

What is a pi merchant?

A pi merchant is someone verified by pi network team and allowed to barter pi coins for goods and services.

Since pi network is not doing any pre-sale The only way exchanges like binance/huobi or crypto whales can get pi is by buying from miners. And a merchant stands in between the exchanges and the miners.

I will leave the telegram contact of my personal pi merchant. I and my friends has traded more than 6000pi coins successfully

Tele-gram

@Pi_vendor_247

Falcon stands out as a top-tier P2P Invoice Discounting platform in India, bridging esteemed blue-chip companies and eager investors. Our goal is to transform the investment landscape in India by establishing a comprehensive destination for borrowers and investors with diverse profiles and needs, all while minimizing risk. What sets Falcon apart is the elimination of intermediaries such as commercial banks and depository institutions, allowing investors to enjoy higher yields.

If you are looking for a pi coin investor. Then look no further because I have the right one he is a pi vendor (he buy and resell to whales in China). I met him on a crypto conference and ever since I and my friends have sold more than 10k pi coins to him And he bought all and still want more. I will drop his telegram handle below just send him a message.

@Pi_vendor_247

how to sell pi coins at high rate quickly.DOT TECH

Where can I sell my pi coins at a high rate.

Pi is not launched yet on any exchange. But one can easily sell his or her pi coins to investors who want to hold pi till mainnet launch.

This means crypto whales want to hold pi. And you can get a good rate for selling pi to them. I will leave the telegram contact of my personal pi vendor below.

A vendor is someone who buys from a miner and resell it to a holder or crypto whale.

Here is the telegram contact of my vendor:

@Pi_vendor_247

Turin Startup Ecosystem 2024 - Ricerca sulle Startup e il Sistema dell'Innov...Quotidiano Piemontese

Turin Startup Ecosystem 2024

Una ricerca de il Club degli Investitori, in collaborazione con ToTeM Torino Tech Map e con il supporto della ESCP Business School e di Growth Capital

BYD SWOT Analysis and In-Depth Insights 2024.pptxmikemetalprod

Indepth analysis of the BYD 2024

BYD (Build Your Dreams) is a Chinese automaker and battery manufacturer that has snowballed over the past two decades to become a significant player in electric vehicles and global clean energy technology.

This SWOT analysis examines BYD's strengths, weaknesses, opportunities, and threats as it competes in the fast-changing automotive and energy storage industries.

Founded in 1995 and headquartered in Shenzhen, BYD started as a battery company before expanding into automobiles in the early 2000s.

Initially manufacturing gasoline-powered vehicles, BYD focused on plug-in hybrid and fully electric vehicles, leveraging its expertise in battery technology.

Today, BYD is the world’s largest electric vehicle manufacturer, delivering over 1.2 million electric cars globally. The company also produces electric buses, trucks, forklifts, and rail transit.

On the energy side, BYD is a major supplier of rechargeable batteries for cell phones, laptops, electric vehicles, and energy storage systems.

Empowering the Unbanked: The Vital Role of NBFCs in Promoting Financial Inclu...Vighnesh Shashtri

In India, financial inclusion remains a critical challenge, with a significant portion of the population still unbanked. Non-Banking Financial Companies (NBFCs) have emerged as key players in bridging this gap by providing financial services to those often overlooked by traditional banking institutions. This article delves into how NBFCs are fostering financial inclusion and empowering the unbanked.

what is the future of Pi Network currency.DOT TECH

The future of the Pi cryptocurrency is uncertain, and its success will depend on several factors. Pi is a relatively new cryptocurrency that aims to be user-friendly and accessible to a wide audience. Here are a few key considerations for its future:

Message: @Pi_vendor_247 on telegram if u want to sell PI COINS.

1. Mainnet Launch: As of my last knowledge update in January 2022, Pi was still in the testnet phase. Its success will depend on a successful transition to a mainnet, where actual transactions can take place.

2. User Adoption: Pi's success will be closely tied to user adoption. The more users who join the network and actively participate, the stronger the ecosystem can become.

3. Utility and Use Cases: For a cryptocurrency to thrive, it must offer utility and practical use cases. The Pi team has talked about various applications, including peer-to-peer transactions, smart contracts, and more. The development and implementation of these features will be essential.

4. Regulatory Environment: The regulatory environment for cryptocurrencies is evolving globally. How Pi navigates and complies with regulations in various jurisdictions will significantly impact its future.

5. Technology Development: The Pi network must continue to develop and improve its technology, security, and scalability to compete with established cryptocurrencies.

6. Community Engagement: The Pi community plays a critical role in its future. Engaged users can help build trust and grow the network.

7. Monetization and Sustainability: The Pi team's monetization strategy, such as fees, partnerships, or other revenue sources, will affect its long-term sustainability.

It's essential to approach Pi or any new cryptocurrency with caution and conduct due diligence. Cryptocurrency investments involve risks, and potential rewards can be uncertain. The success and future of Pi will depend on the collective efforts of its team, community, and the broader cryptocurrency market dynamics. It's advisable to stay updated on Pi's development and follow any updates from the official Pi Network website or announcements from the team.

how can i use my minded pi coins I need some funds.DOT TECH

If you are interested in selling your pi coins, i have a verified pi merchant, who buys pi coins and resell them to exchanges looking forward to hold till mainnet launch.

Because the core team has announced that pi network will not be doing any pre-sale. The only way exchanges like huobi, bitmart and hotbit can get pi is by buying from miners.

Now a merchant stands in between these exchanges and the miners. As a link to make transactions smooth. Because right now in the enclosed mainnet you can't sell pi coins your self. You need the help of a merchant,

i will leave the telegram contact of my personal pi merchant below. 👇 I and my friends has traded more than 3000pi coins with him successfully.

@Pi_vendor_247

what is the best method to sell pi coins in 2024DOT TECH

The best way to sell your pi coins safely is trading with an exchange..but since pi is not launched in any exchange, and second option is through a VERIFIED pi merchant.

Who is a pi merchant?

A pi merchant is someone who buys pi coins from miners and pioneers and resell them to Investors looking forward to hold massive amounts before mainnet launch in 2026.

I will leave the telegram contact of my personal pi merchant to trade pi coins with.

@Pi_vendor_247

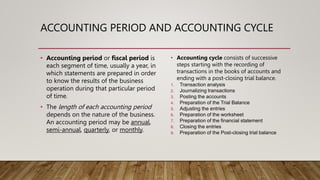

1. ACCOUNTING PERIOD AND ACCOUNTING CYCLE

• Accounting period or fiscal period is

each segment of time, usually a year, in

which statements are prepared in order

to know the results of the business

operation during that particular period

of time.

• The length of each accounting period

depends on the nature of the business.

An accounting period may be annual,

semi-annual, quarterly, or monthly.

• Accounting cycle consists of successive

steps starting with the recording of

transactions in the books of accounts and

ending with a post-closing trial balance.

1. Transaction analysis

2. Journalizing transactions

3. Posting the accounts

4. Preparation of the Trial Balance

5. Adjusting the entries

6. Preparation of the worksheet

7. Preparation of the financial statement

8. Closing the entries

9. Preparation of the Post-closing trial balance

2. JOURNALIZING

• It is the process of recording business transactions in a journal. In order to have a

permanent record of an entire transaction, the accountant uses a book or record

known as a journal.

• A journal is called the book of original entry. Journals are prepared in accordance

with industry practice and generally accepted accounting principles/Philippine

Financial Reporting Standards for transactions and events

• A journal entry is the recording of a business transaction in a journal.

• A journal entry shows all of the effects of a transaction as expressed in terms of

debit and credit and may include an explanation of the transaction.

3. STEPS FOR THE PROCESS OF JOURNALIZING

1. Determine the titles of the accounts involved.

2. Understand nature of the accounts.

3. Apply the rule of Debit & Credit.

4. Make the necessary journal entry.

Assets = Liabilities + Owner's Equity

And

Debits = Credits

4. DEBIT AND CREDIT

• The left side of a T-account is called

the debit side; often abbreviated Dr.

• When the sum of debits exceeds the

sum of credits, the account has a

debit balance.

• The right side is called the credit

side, abbreviated Cr.

• It has a credit balance when the sum

of credits exceeds the sum of debits.

5. RULES IN USING DEBIT AND CREDIT

Rule 1: All accounts that normally contain a debit balance will increase in amount when a

debit (left column) is added to them, and reduced when a credit (right column) is added to

them. The types of accounts to which this rule applies areexpenses, assets, and dividends.

Rule 2: All accounts that normally contain a credit balance will increase in amount when a

credit (right column) is added to them, and reduced when a debit (left column) is added to

them. The types of accounts to which this rule applies areliabilities, revenues, and equity.

6. RULES IN USING DEBIT AND CREDIT

Rule 3: Contra accounts reduce the balances of the accounts with which they are

paired. This means that (for example) a contra account paired with an assetaccount

behaves as though it were a liability account.

Rule 4: The total amount of debits must equal the total amount of credits in a

transaction. Otherwise, a transaction is said to be unbalanced, and the financial

statements from which a transaction is constructed will be inherently incorrect. An

accounting software package will flag any journal entries that areunbalanced.

7. THE JOURNAL ENTRY

• The General Journal is flexible in that it can be used to record any economic

transaction. A General Journal entry includes the following information about

each transaction:

1. Date of transaction.

2. Titles of affected accounts.

3. Peso amount of each debit and credit.

4. Explanation of transaction.

9. JOURNALIZING TRANSACTIONS

There are standard procedures for recording entries in a General Journal.

1. Enter the year on the first line at the top of the first column.

2. Enter the month in Column One on the first line of the journal entry. Later

entries for the same month and year on the same page of the journal do not

require re-entering the same month and year.

3. Enter the day of the transaction in Column Two on the first line of each entry.

Transactions are journalized in chronological order (by date).

4. Enter the titles of accounts debited. Account titles are taken from the chart of

accounts and are aligned with the left margin of the Account Titles and

Explanation column.

5. Enter the debit amounts in the Debit column on the same line as the

accountsto be debited.

10. JOURNALIZING TRANSACTIONS

6. Enter the titles of accounts credited. Account titles are taken from the

chart of accounts and are indented from the left margin of the Account

Titles and Explanation column to distinguish them from debited

accounts (an indent of 1 cm is common).

7. Enter the credit amounts in the Credit column on the same line as

the accounts to be credited.

8. Enter a brief explanation of the transaction on the line below the entry.

This explanation is indented about half as far as the credited account

titles to avoid confusing an explanation with accounts. For illustrative

purposes, we italicize explanations so they stand out. This is not normally

done.

9. Skip a line after each journal entry for clarity.