Downloaded 22 times

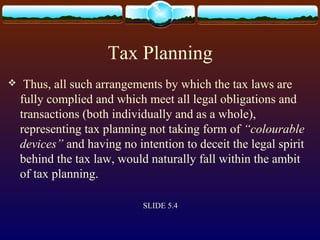

![Tax Planning

Colourable devices cannot be part of tax planning and it

is wrong to encourage or entertain the belief that it is

honourable to avoid payment of tax by resorting to

dubious methods [McDowell & Co. Ltd. v. CTO [1985]

154 ITR 148 (Supreme Court)]

SLIDE 5.4](https://image.slidesharecdn.com/taxavoidance5-140821075811-phpapp02/85/Tax-avoidance-5-4-4-320.jpg)

Tax planning involves legally arranging one's financial affairs to minimize tax liability, while complying with all applicable tax laws. Tax avoidance uses artificial or dubious methods to reduce taxes in a manner that defeats the intent of tax statutes. Tax evasion illegally avoids taxes through actions like knowingly making untrue statements or omitting required information. The line between tax planning and avoidance is thin, with avoidance including an element of mala fide intent or use of "colorable devices" to circumvent the spirit of tax laws.