Downloaded 11 times

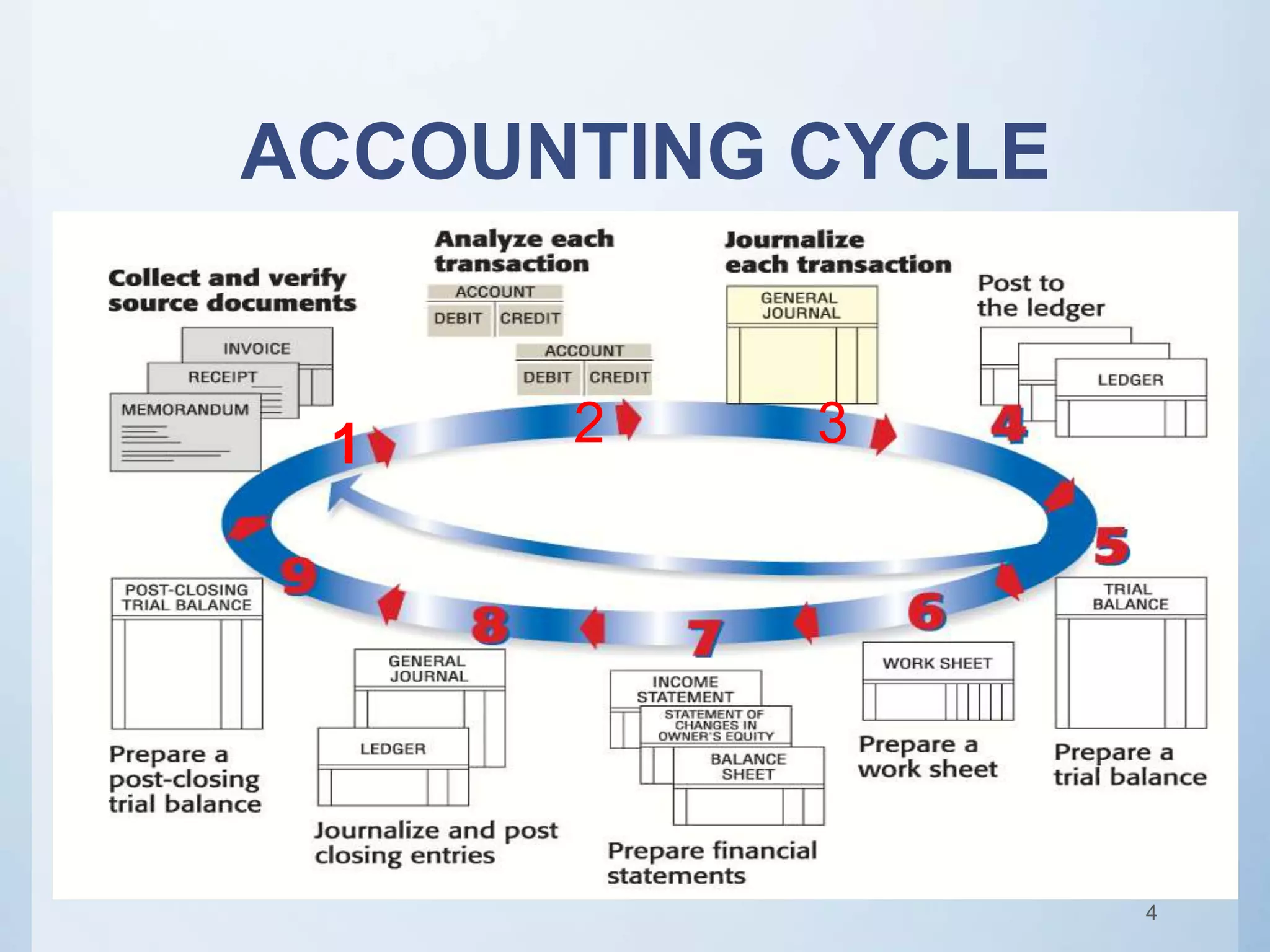

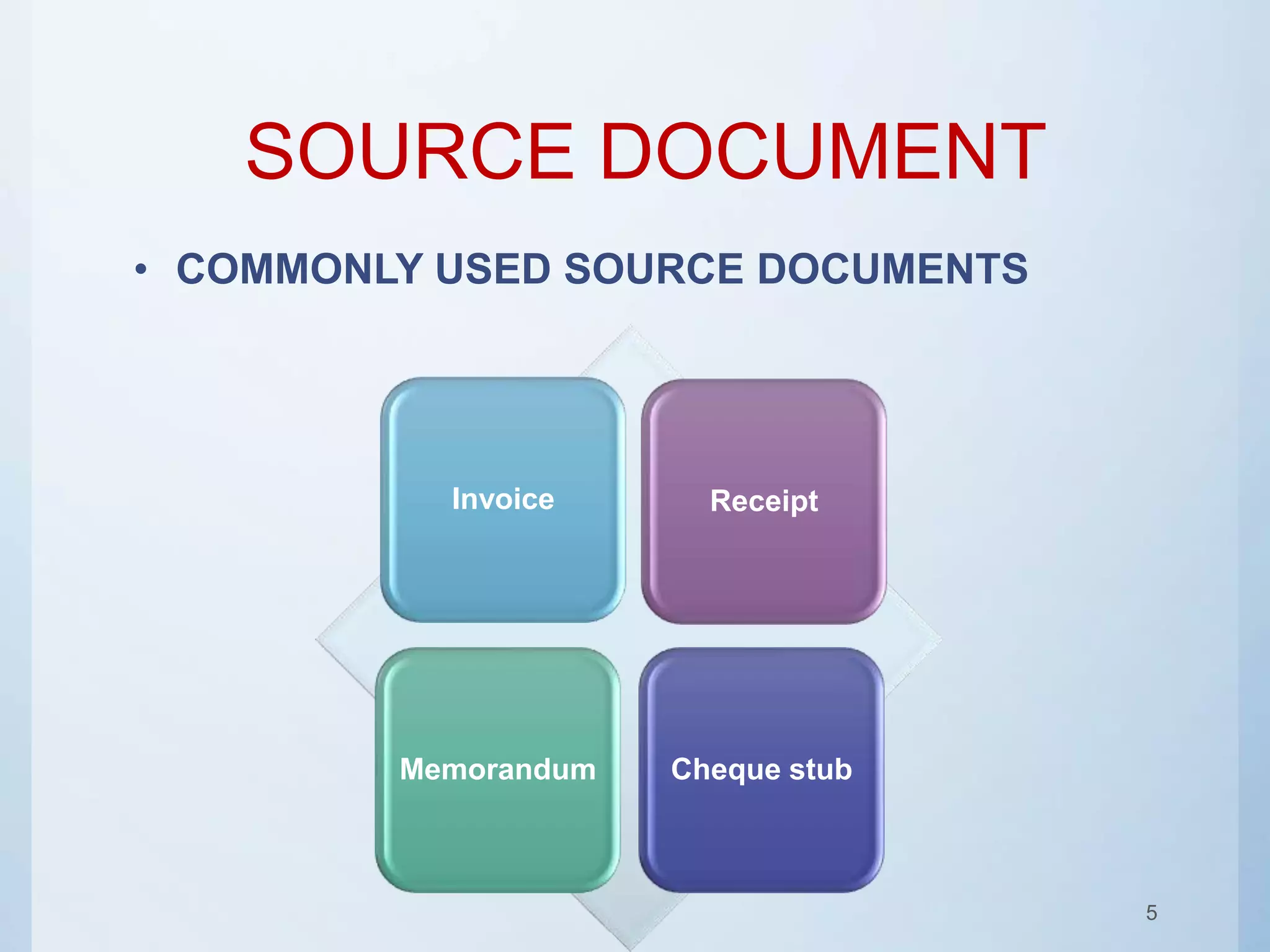

The document discusses the systematic documentation of business transactions through an accounting cycle. It begins with an introduction to accounting and the accounting cycle. It then discusses key steps in the accounting cycle including source documents, journals, ledgers, trial balances, and final accounts. The accounting cycle allows a business to systematically record and track financial transactions and prepare financial statements like the balance sheet.