Chapter 14 Audit of the Sales and Collection Cycle.ppt

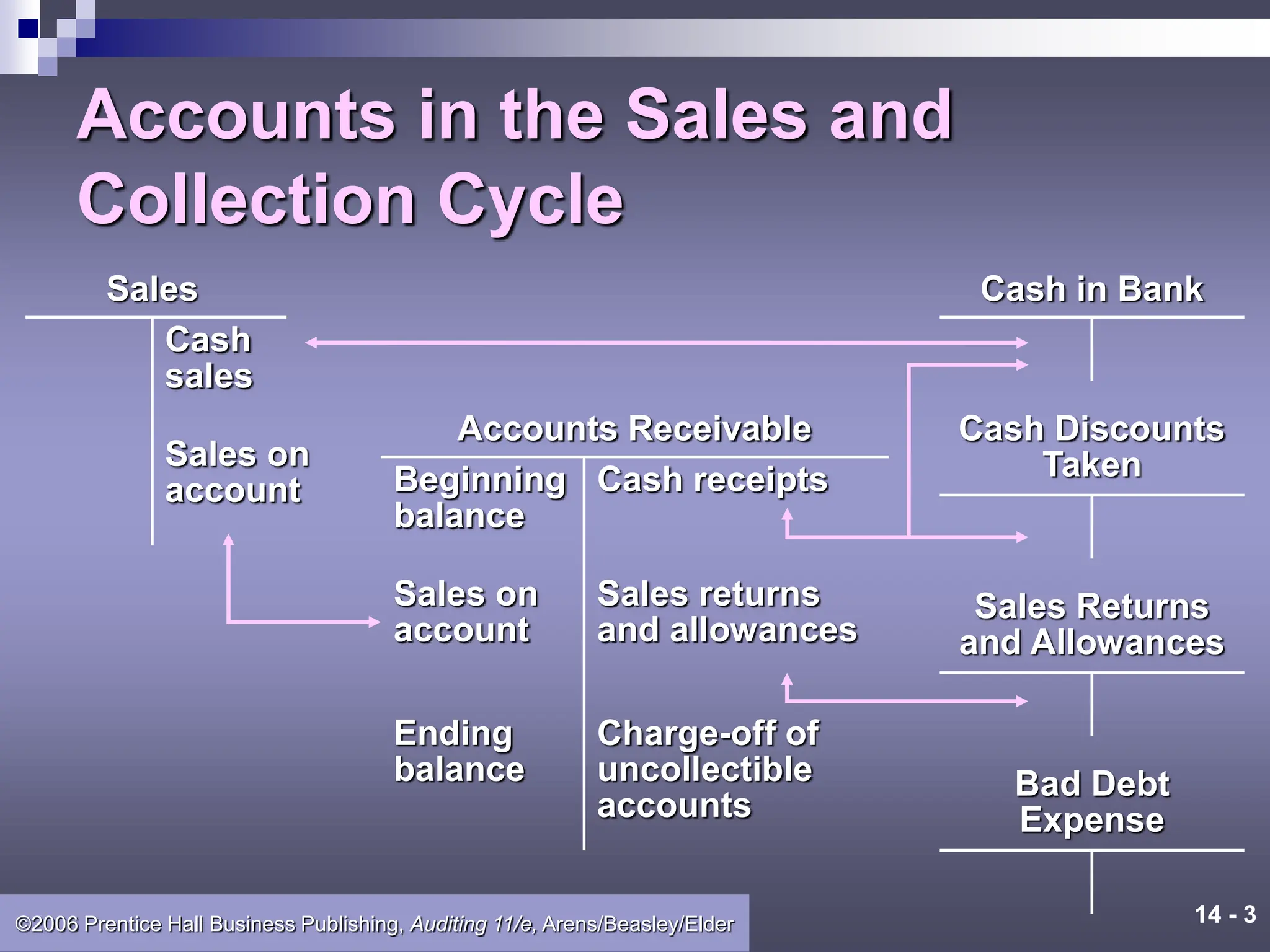

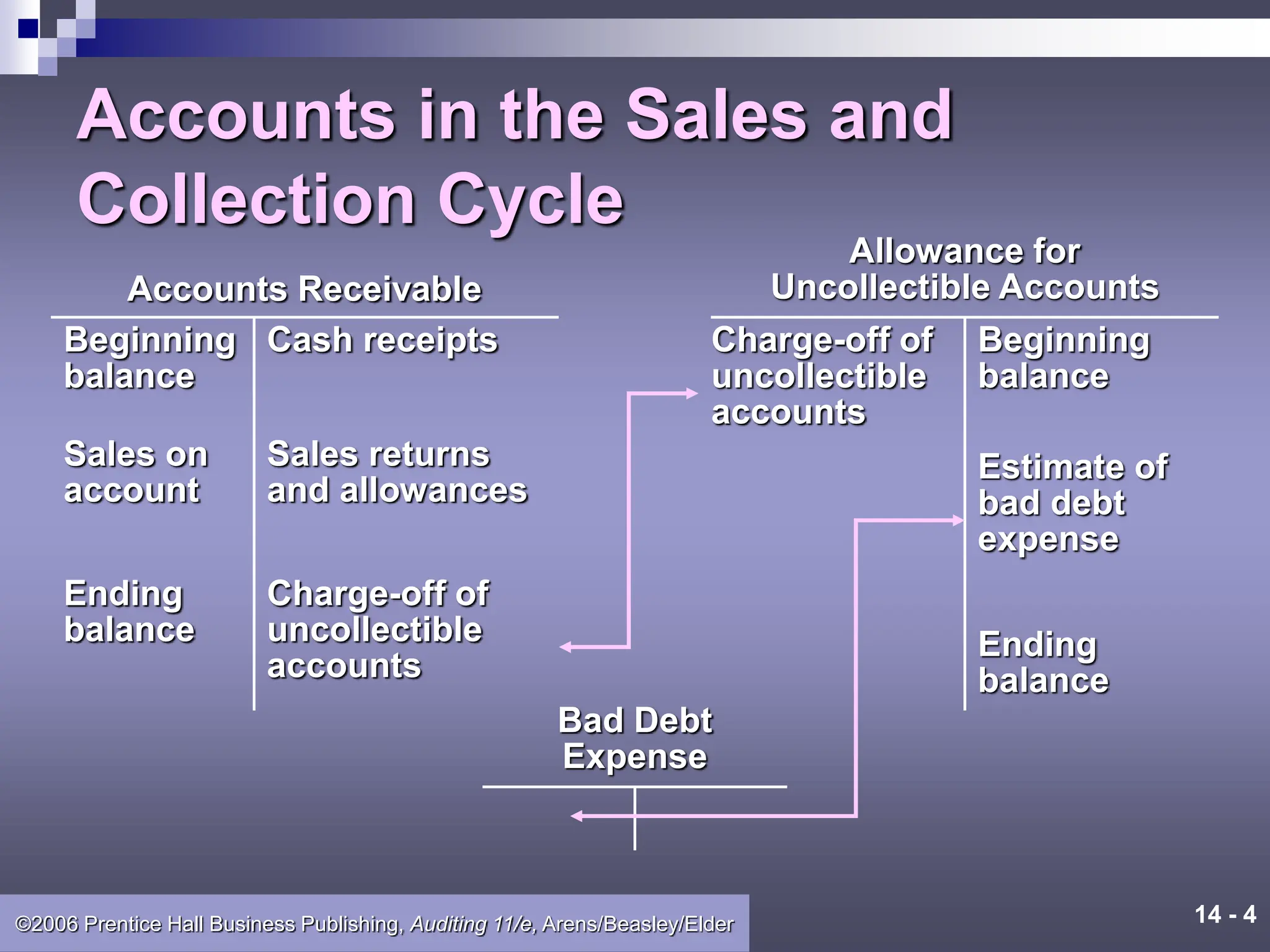

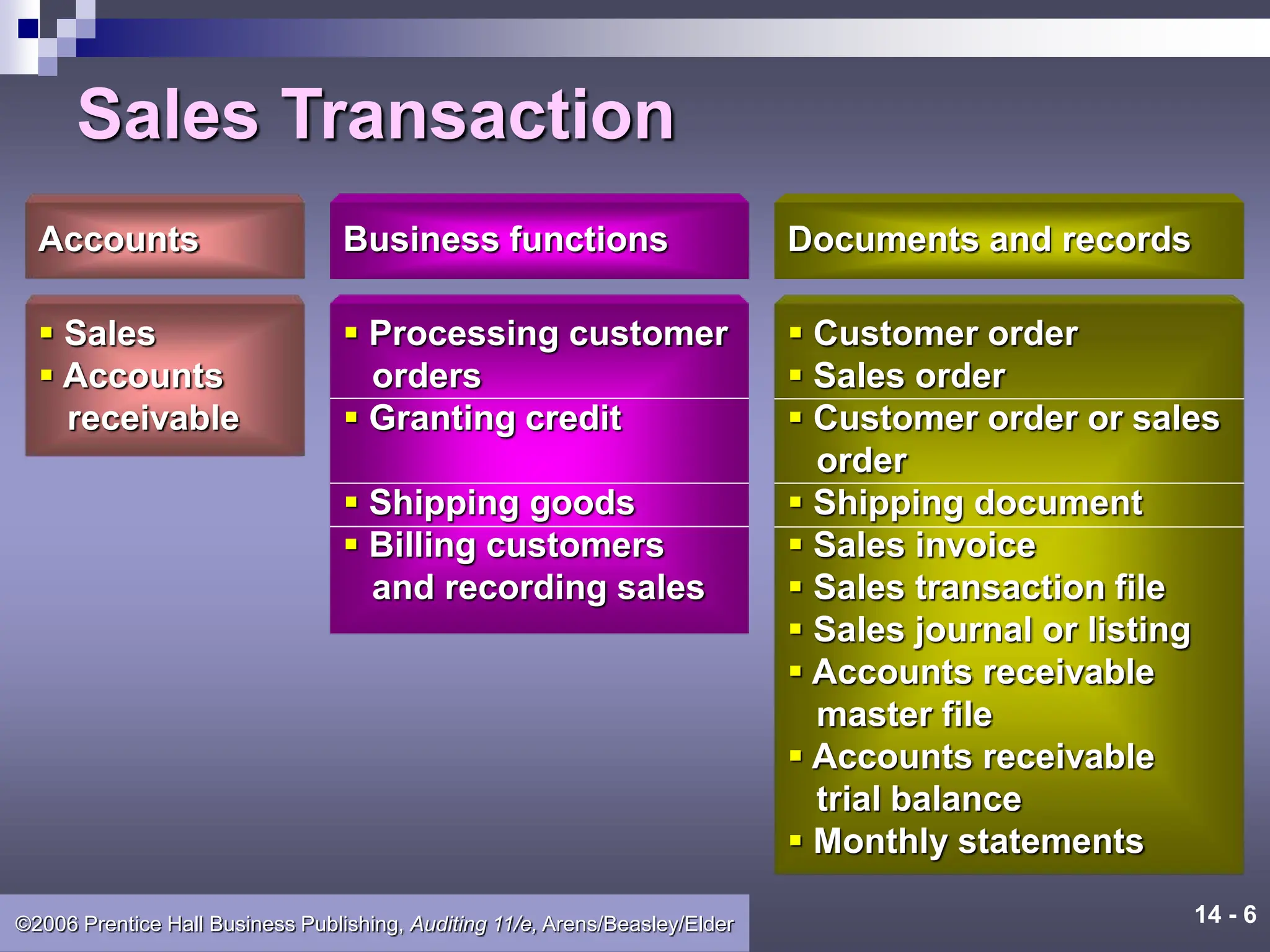

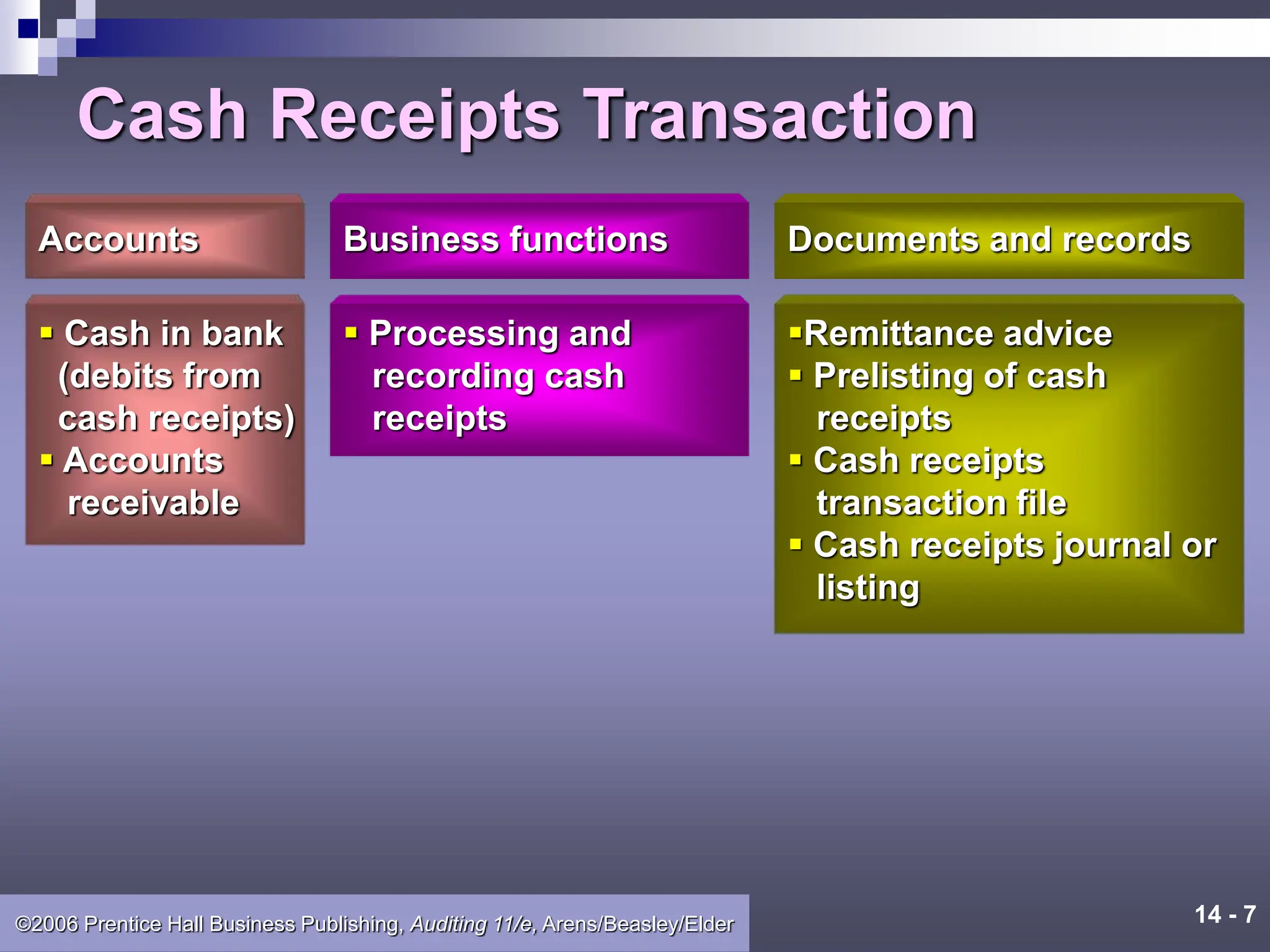

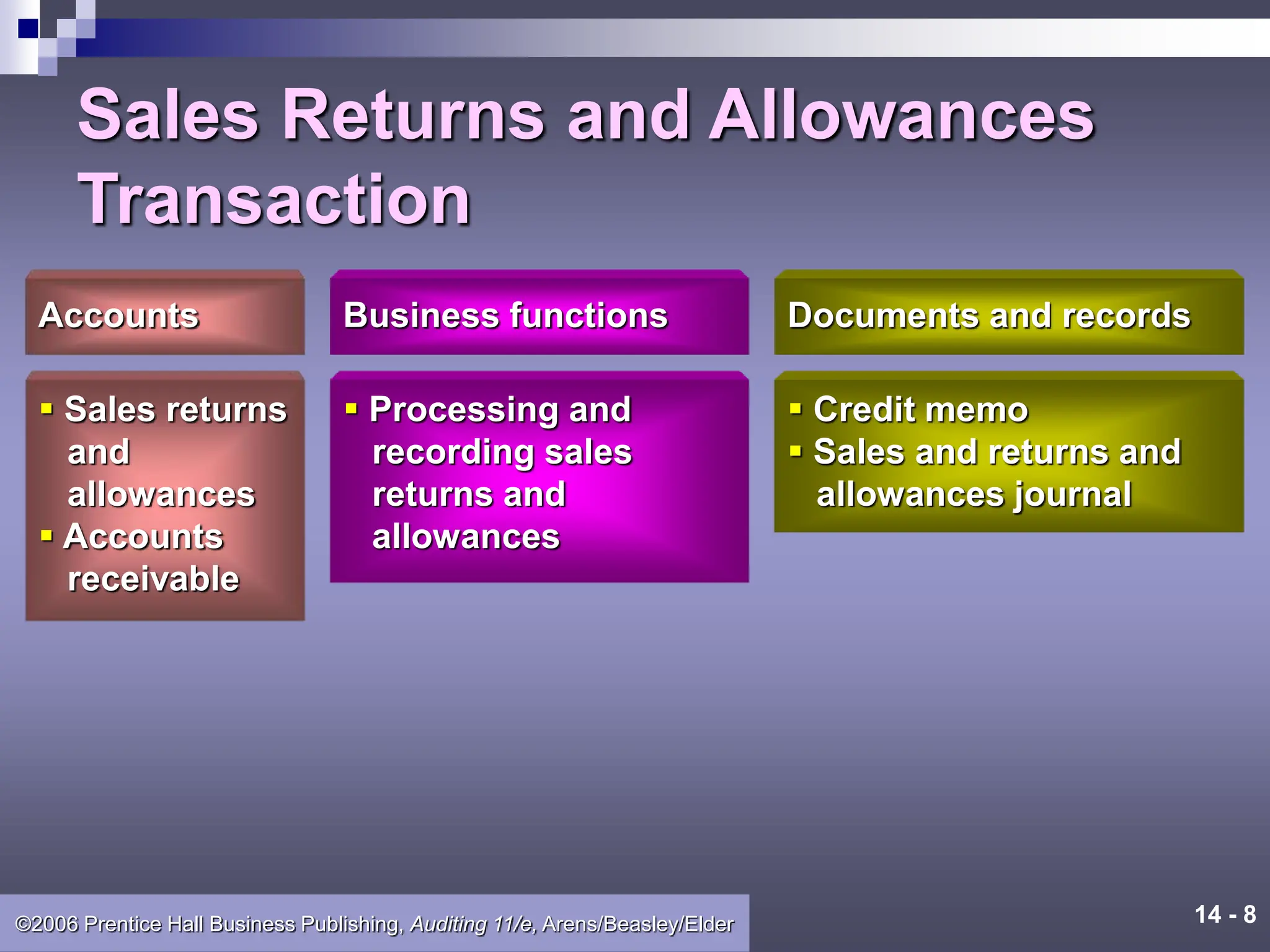

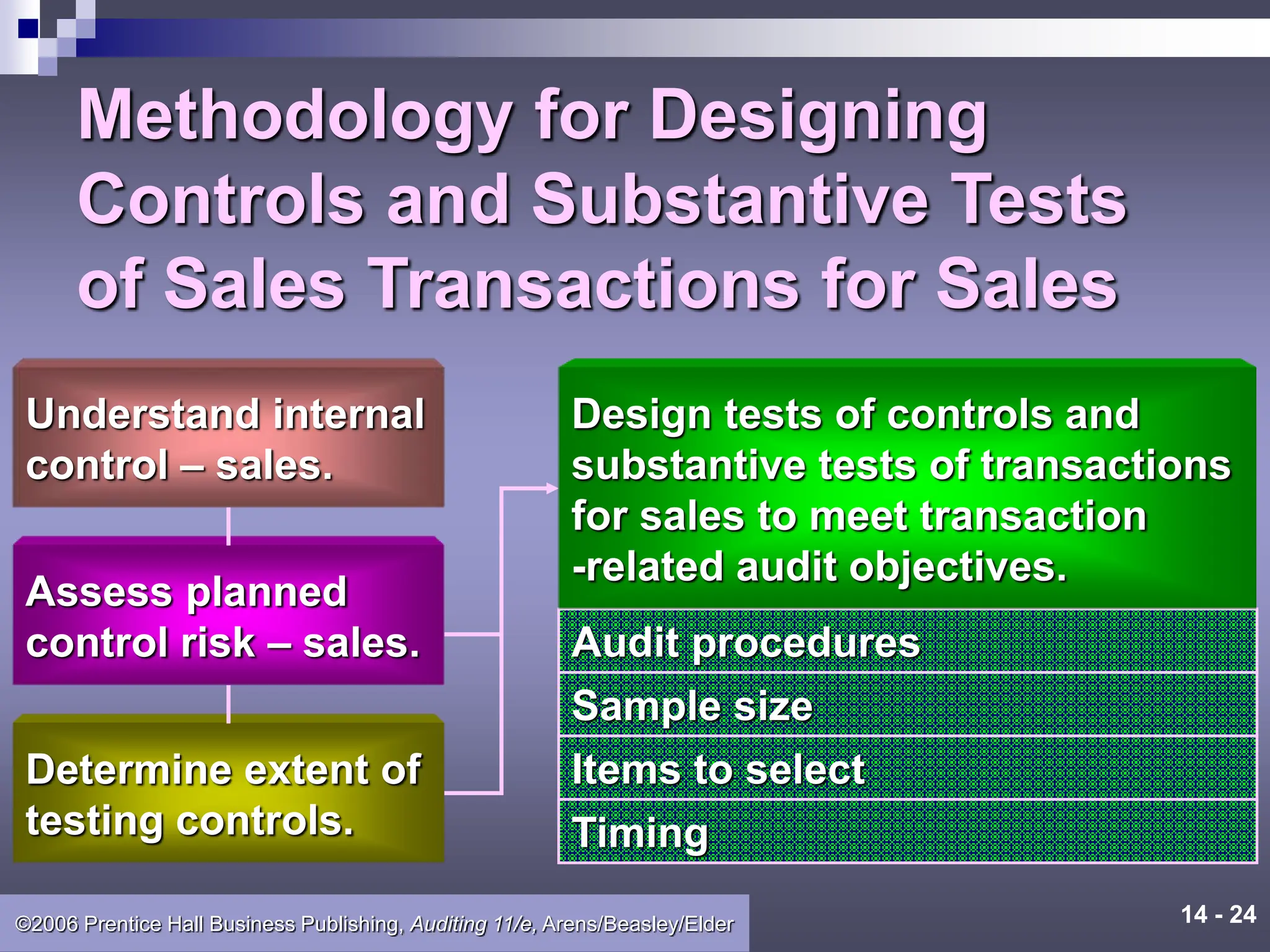

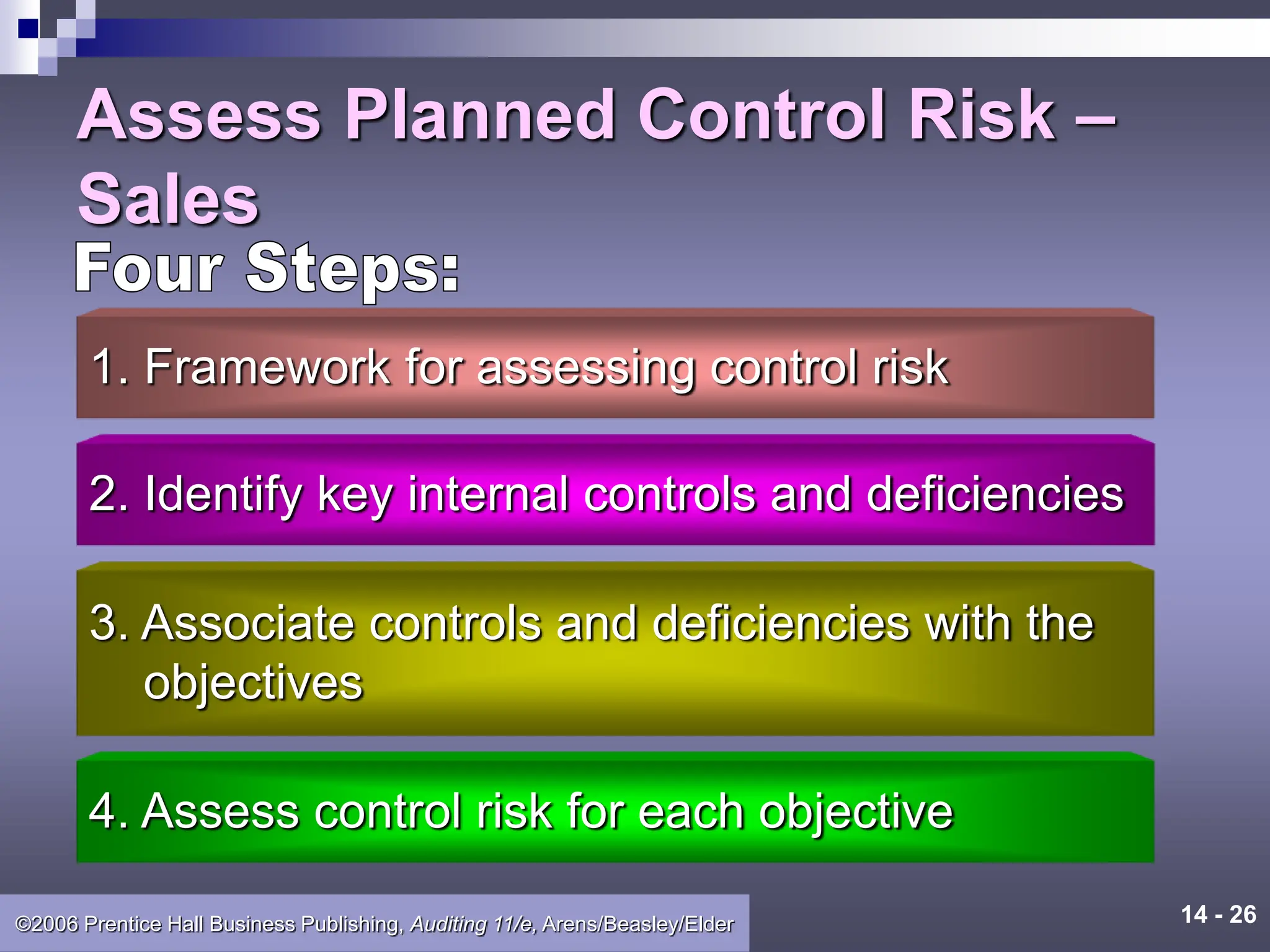

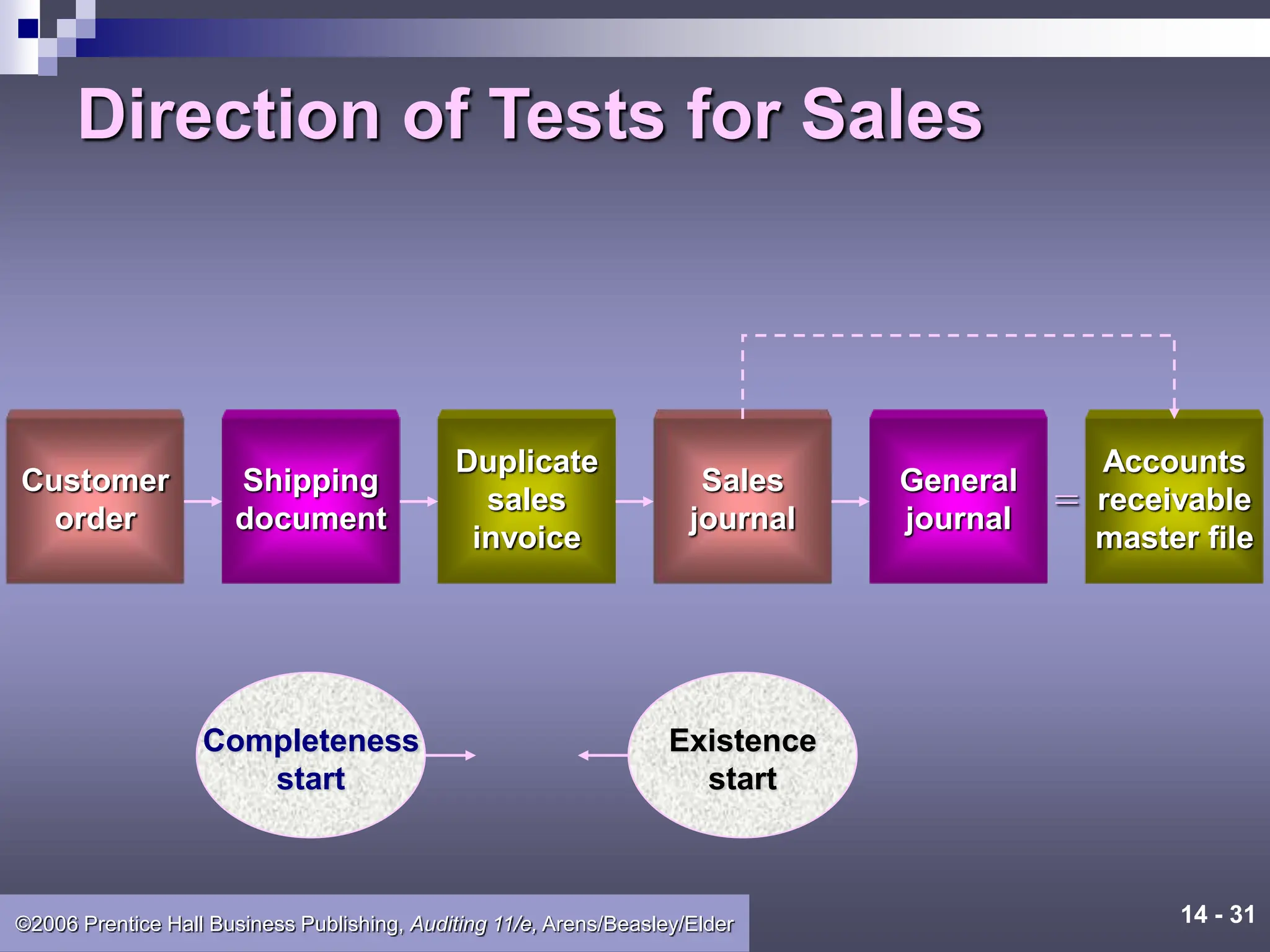

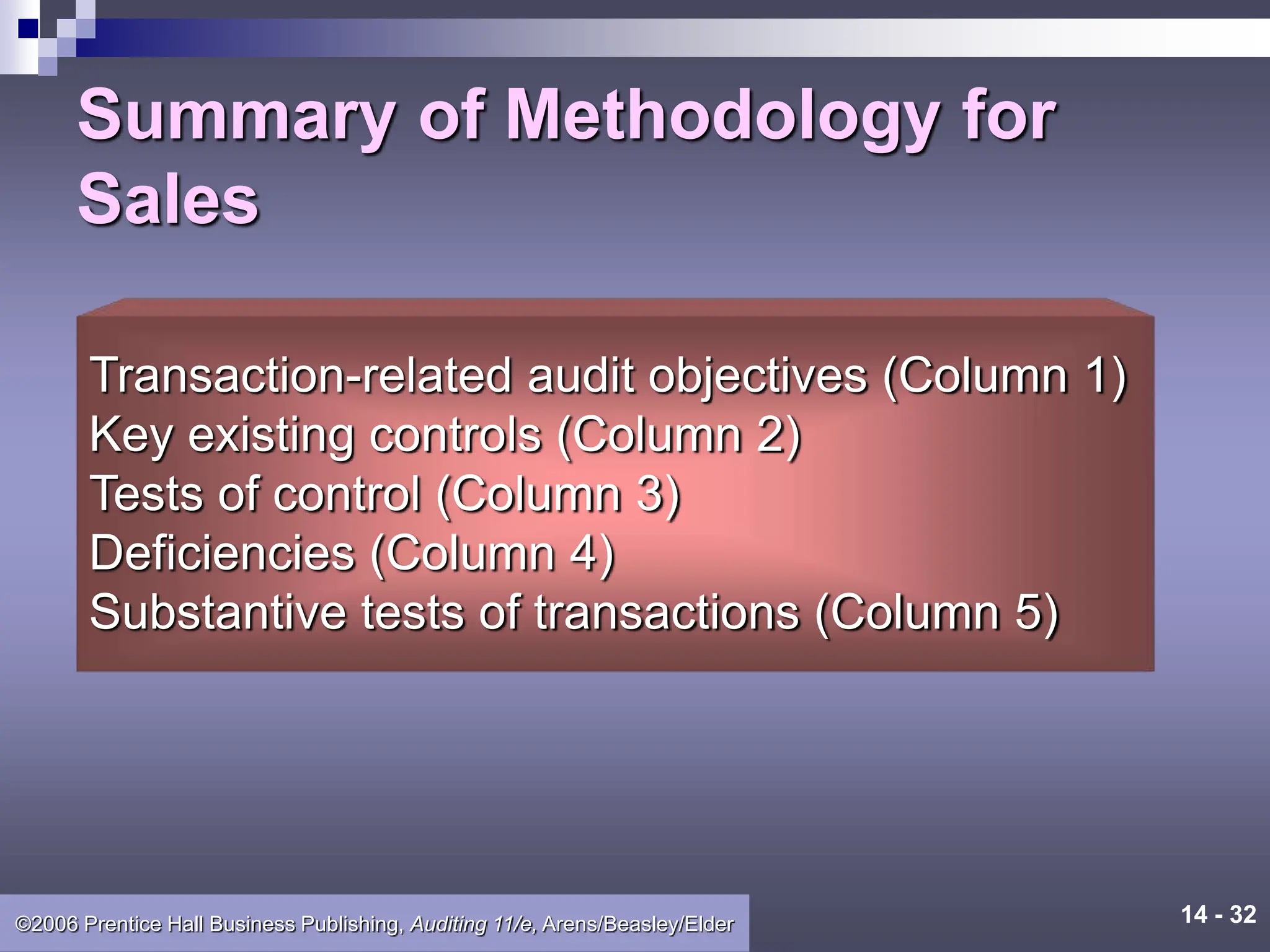

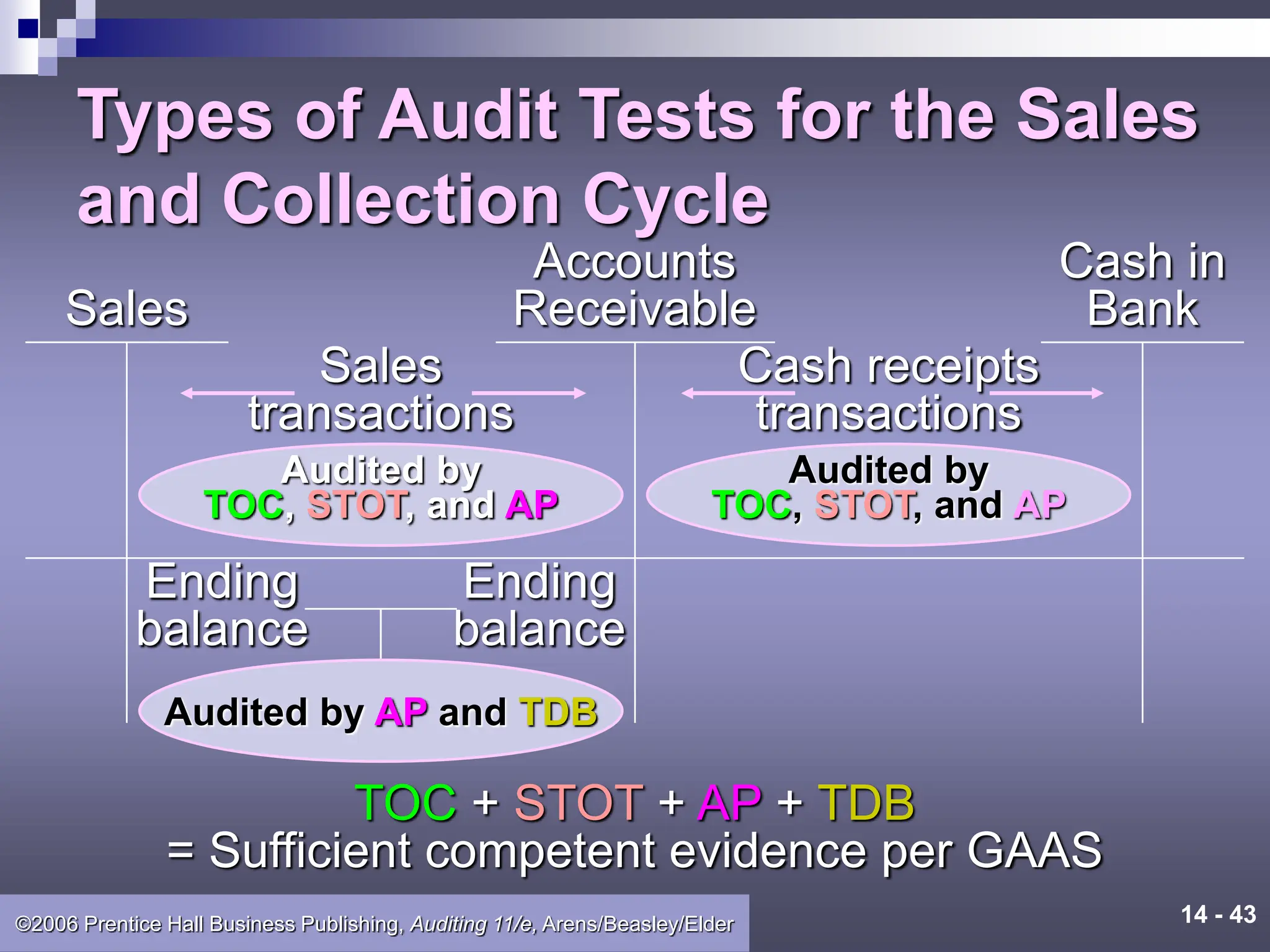

This document discusses auditing the sales and collection cycle. It covers the key accounts and transactions in the cycle, including sales, accounts receivable, cash receipts, returns and allowances, bad debts. The business functions like order processing, credit approval, billing, and cash receipt recording are described. Documentation used in the cycle like sales orders, invoices, and receipts are identified. The methodology for understanding controls, assessing control risk, and designing tests of controls and substantive transactions tests is presented. E-commerce impacts and testing approaches are also discussed.