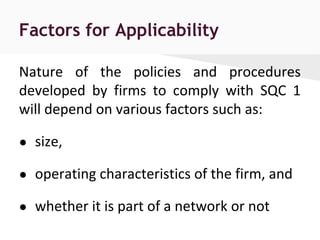

![Other Assurance

Services

Framework of Assurance

Engagement

Related

Services

Assurance

Services

SQC

Standards on

Quality Control

[1 to 90]

Assurance

Services

Audit & Review of Historical

Financial Information

SA

Standards on

Auditing

[100 to 900]

SAE

Standards on

Assurance

Engagements

[3000 to 3699]

SRS

Standards on

Related

services

[4000 to 4699]

Related

Services

Structure of Standards issued by AASB

Other Assurance

Services

SRE

Standards on

Review

Engagement

[2000 to 2699]

Framework of Assurance

Engagement](https://image.slidesharecdn.com/standardonqualitycontrolsqc-peerreview-150309131130-conversion-gate01/85/Standard-on-quality-control-sqc-peer-review-2-320.jpg)

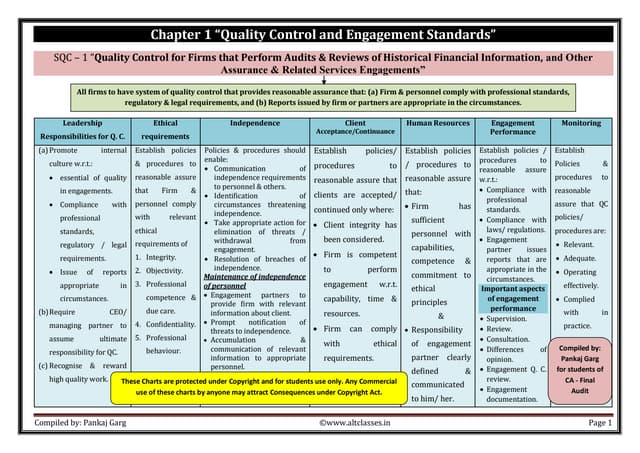

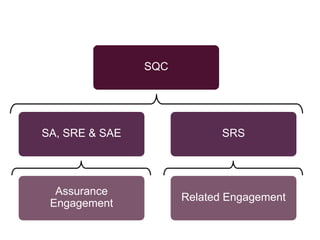

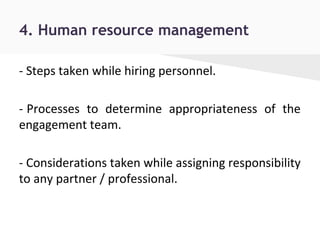

The document discusses Standard on Quality Control (SQC) 1, which applies to all firms that perform audits, reviews, and other assurance and related services engagements. SQC 1 requires firms to establish a system of quality control with six key elements: leadership responsibilities, ethical requirements including independence, client acceptance and continuance, human resource management, engagement performance, and monitoring. It describes the policies and procedures firms must implement under each element to maintain quality in service engagements. The document also briefly outlines the peer review process where another professional evaluates a firm's quality control system and attestation work.