Downloaded 182 times

![Audit report to state

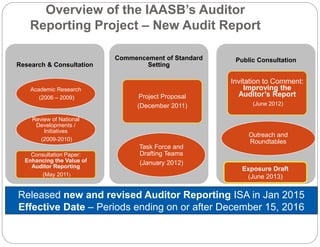

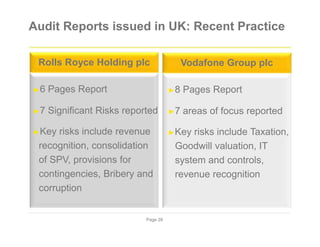

Other information [ annexed in annual report ]

Management is responsible for the other information. The other

information comprises the director’s report, analysis etc……………..

Our opinion on the financial statements does not cover the other

information and we do not express any form of assurance conclusion

thereon.

In connection with our audit of the financial statements, our

responsibility is to read the other information and, in doing so,

consider whether the other information is materially inconsistent

with the financial statements or our knowledge obtained in the audit or

otherwise appears to be materially misstated. If, based on the work we

have performed, we conclude that there is a material misstatement of

this other information, we are required to report that fact.[We have

nothing to report in this regard [or a statement that describes any

material misstatement of the other information]].

Page 10](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-12-320.jpg)

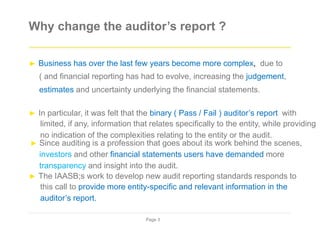

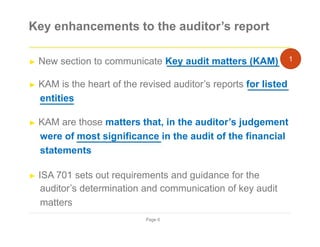

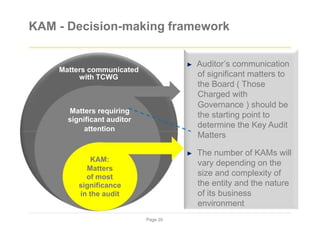

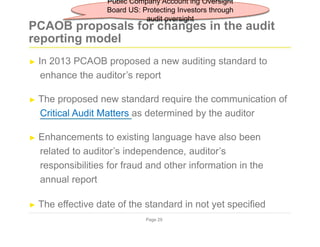

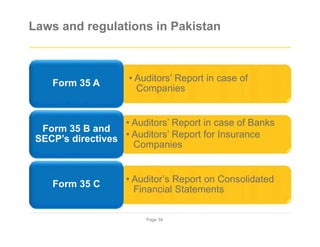

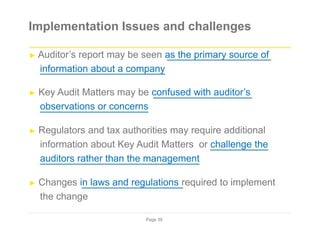

![Form of Audit Report under revised

standards vs. Current Audit Report

Independent Auditors’ Report

Current Audit Report

► Report on the Audit of the Financial

Statements

► Opinion

► Basis for Opinion

► Material Uncertainty Related to Going

Concern (if applicable)

► Emphasis of Matter (if applicable)

► Key Audit Matters

► Other Matters (if any)

► Other Information (if applicable)

► Responsibilities of Management and TCWG

for the Financial Statements

► Auditors’ Responsibilities for the Audit of

Financial Statements

► Report on Other Legal and Regulatory

Requirements

► The engagement partner on the audit [name].

► Signature, Address and Date

► Identification of

financial

statements audited

► Management’s

responsibilities

► Description of audit

scope

► Audit opinion

Page 12](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-14-320.jpg)

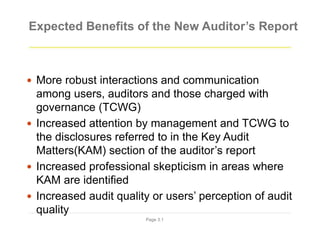

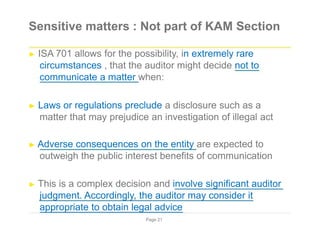

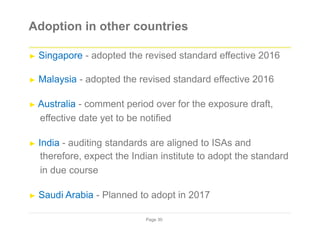

![The new auditor’s report

(Extracted from ISA 700 (Revised) - Forming an Opinion and Reporting on Financial Statements)

INDEPENDENT AUDITOR’S REPORT

To the Shareholders of ABC Company [or Other Appropriate Addressee]

Report on the audit of the financial statements

Opinion

We have audited the financial statements of ABC Company (the Company), which comprise the statement of

financial position as at December 31 20X1, and the statement of comprehensive income, statement of changes in

equity and statement of cash flows for the year then ended, and notes to the financial statements, including a

summary of significant accounting policies.

In our opinion, the accompanying financial statements present fairly, in all material respects, (or give a true and fair

view of) the financial position of the Company as at 31 December 20X1 and (of) its financial performance and its cash

flows for the year then ended in accordance with International Financial Reporting Standards.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under

those standards are further described in the Auditor’s responsibilities for the audit of the financial statements section

of our report. We are independent of the Company in accordance with the ethical requirements that are relevant to

our audit of the financial statements in [Country], and we have fulfilled our other ethical responsibilities in accordance

with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide

a basis for our opinion.

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the

financial statements of the current period. These matters were addressed in the context of our audit of the financial

statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these

matters.

Enhancements to

the auditor’s report

Opinion first. The auditor’s opinion - the

“pass/fail” statement that users have said

they continue to value - is required to be

positioned at the beginning of the report,

followed by the Basis for Opinion.

Required Basis for Opinion section.

Currently required only when the auditor’s

opinion was modified.

New affirmative statement about the

auditor’s fulfillment of independence and

other relevant ethical responsibilities

requirements.

The new KAM section is the centerpiece

of the revised auditor’s report.

Required for audits of listed entities,

but may be applied voluntarily to other

audits.

[Description of each key audit matter in accordance with ISA 701.]

Page 14](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-16-320.jpg)

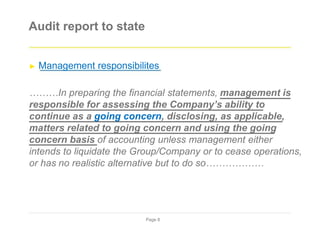

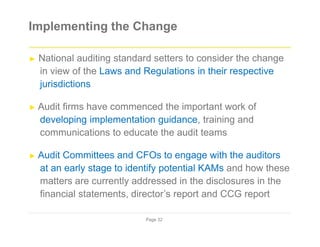

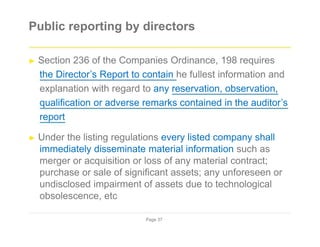

![The new auditor’s report

Other information [ annexed in annual reports]

Management is responsible for the other information. The other information comprises the [information included in the

Annual Report, but does not include the financial statements and our auditor’s report thereon.]

Our opinion on the financial statements does not cover the other information and we do not express any form of

assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing

so, consider whether the other information is materially inconsistent with the financial statements or our knowledge

obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we

conclude that there is a material misstatement of this other information, we are required to report that fact. [We have

nothing to report in this regard [or a statement that describes any material misstatement of the other information]].

New descriptions of management’s

responsibilities relating to going

Responsibilities of management [and those

charged with governance] for the financial

statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with

IFRSs, and for such internal control as management determines is necessary to enable the preparation of financial

statement that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a

going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of

accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic

alternative but to do so.

[Those charged with governance] are responsible for overseeing the Company’s financial reporting process.]

concern. Intended to reflect the

requirements of the applicable financial

reporting framework.

Identification of TCWG is required

when a separate body exists that is

responsible for the oversight of the

financial reporting process (in many

cases, the audit committee).

When individuals responsible for such

oversight are also responsible for the

preparation of the financial statements,

no reference to oversight

responsibilities Is required.

Page 15](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-17-320.jpg)

![The new auditor’s report

Auditor’s responsibilities for the audit of the

financial statements (continued)

Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit

evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the

Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw

attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to

modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However,

future events or conditions may cause the Company to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the

financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

[[For group audits] Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business

activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction,

supervision and performance of the group audit. We remain solely responsible for our audit opinion.]

We communicate with [those charged with governance] regarding, among other matters, the planned scope and timing of the audit

and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide [those charged with governance] with a statement that we have complied with relevant ethical requirements regarding

independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our

independence, and where applicable, related safeguards.

From the matters communicated with [those charged with governance], we determine those matters that were of most significance in

the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our

auditor’s report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we

determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably

be expected to outweigh the public interest benefits of such communication.

Report on other legal and regulatory requirements

[The form and content of this section of the auditor’s report would vary depending on the nature of the auditor’s other reporting

responsibilities prescribed by local law or regulation]

The partner in charge of the audit resulting in this independent auditor’s report is [name].

[Signature]

[Auditor address]

[Date]

New descriptions of responsibilities

relating to going concern. Reflects

responsibilities under ISA 570, which

are required regardless of the

applicable framework.

A separate section (when applicable)

relating to other information in an

annual report.

More information will be shared on the

revised auditor’s responsibilities,

including its new reporting

requirements, when ISA 720 The

Auditor’s Responsibilities Relating to

Other Information.

Disclosure of the name of the

engagement partner for audits of listed

entities.

Already common practice in many

jurisdictions, the name of the

engagement partner is now included in

auditor’s reports under the ISAs, but is

only required for audits of listed

entities.

Page 17](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-19-320.jpg)

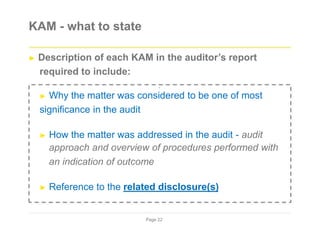

![Key audit matters - an illustration

Goodwill

[Why a matter was determined to be a KAM]

Under IFRSs, the Group is required to annually test the amount of goodwill for impairment.

This annual impairment test was significant to our audit because the balance of XX as of 31

December 20X6 is material to the financial statements. In addition, management’s

assessment process is complex and highly judgmental and is based on assumptions,

specifically [describe certain assumptions], which are affected by expected future market or

economic conditions, particularly those in [name of country or geographic area].

[How a KAM was addressed in the audit]

Our audit procedures included, among others, using a valuation expert to assist us in

evaluating the assumptions and methodologies used by the Group, in particular those

relating to the forecasted revenue growth and profit margins for [name of business line]. We

also focused on the adequacy of the Group’s disclosures about those assumptions to which

the outcome of the impairment test is most sensitive, that is, those that have the most

significant effect on the determination of the recoverable amount of goodwill.

[Refer to the related disclosures]

The Company’s disclosures about goodwill are included in Note X, which specifically

explains that small changes in the key assumptions used could give rise to an impairment

of the goodwill balance in the future.

Page 26](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-28-320.jpg)

![Suggested Approach to Change in the legal

forms relating to the auditor’s report

Independent Auditors’ Report

► Report on the Audit of the Financial

Statements

► Opinion

► Basis for Opinion

► Material Uncertainty Related to Going

Concern (if applicable)

► Emphasis of Matter (if applicable)

► Key Audit Matters

► Other Matters (if any)

► Other Information (if applicable)

► Responsibilities of Management and TCWG

for the Financial Statements

► Auditors’ Responsibilities for the Audit of

Financial Statements

► Report on Other Legal and Regulatory

Requirements

► The engagement partner on the audit [name].

► Signature, Address and Date

Opinions required

by the Companies

Ordinance, 1984

in addition to the

opinion on the

financial

statements (true

& fair view) may

be reported under

a separate

section of the

report in

accordance with

the ISAs

Page 35](https://image.slidesharecdn.com/e2851f17-d55c-49de-a246-7e2cc4269a27-160814212807/85/Presentation-on-New-Auditor-Report-37-320.jpg)

The document discusses the new auditor's report requirements that will take effect for audits ending on or after December 15, 2016. Key changes include adding a new section to communicate key audit matters, revising descriptions of management and auditor responsibilities related to going concern, and enhancing descriptions of the audit performed and auditor responsibilities. The new requirements are aimed at making auditor's reports more informative and relevant to financial statement users. The document provides an overview of the new requirements and compares the format of reports under the revised standards versus the current format. An illustrative example of the new auditor's report is also included.