Downloaded 257 times

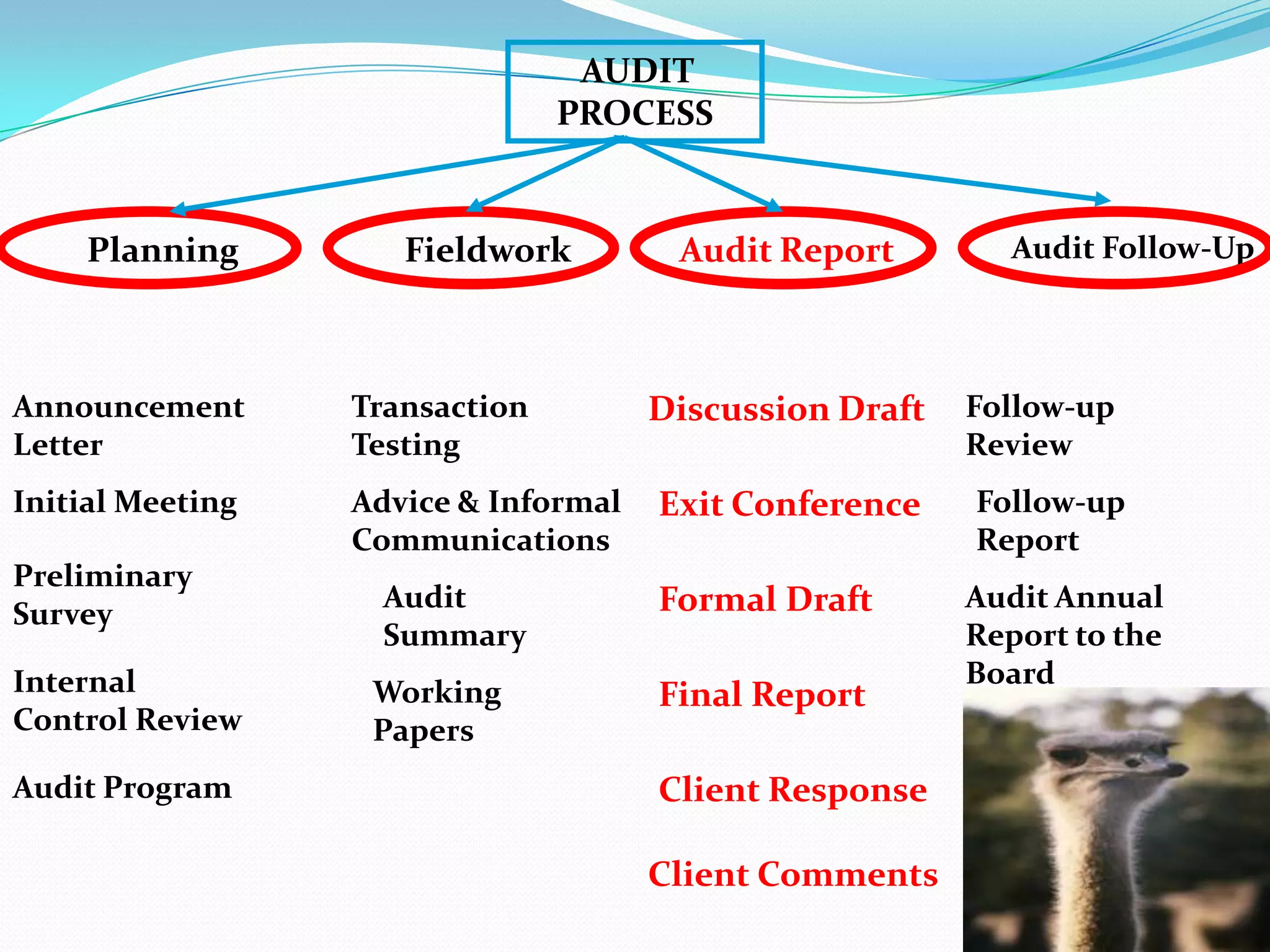

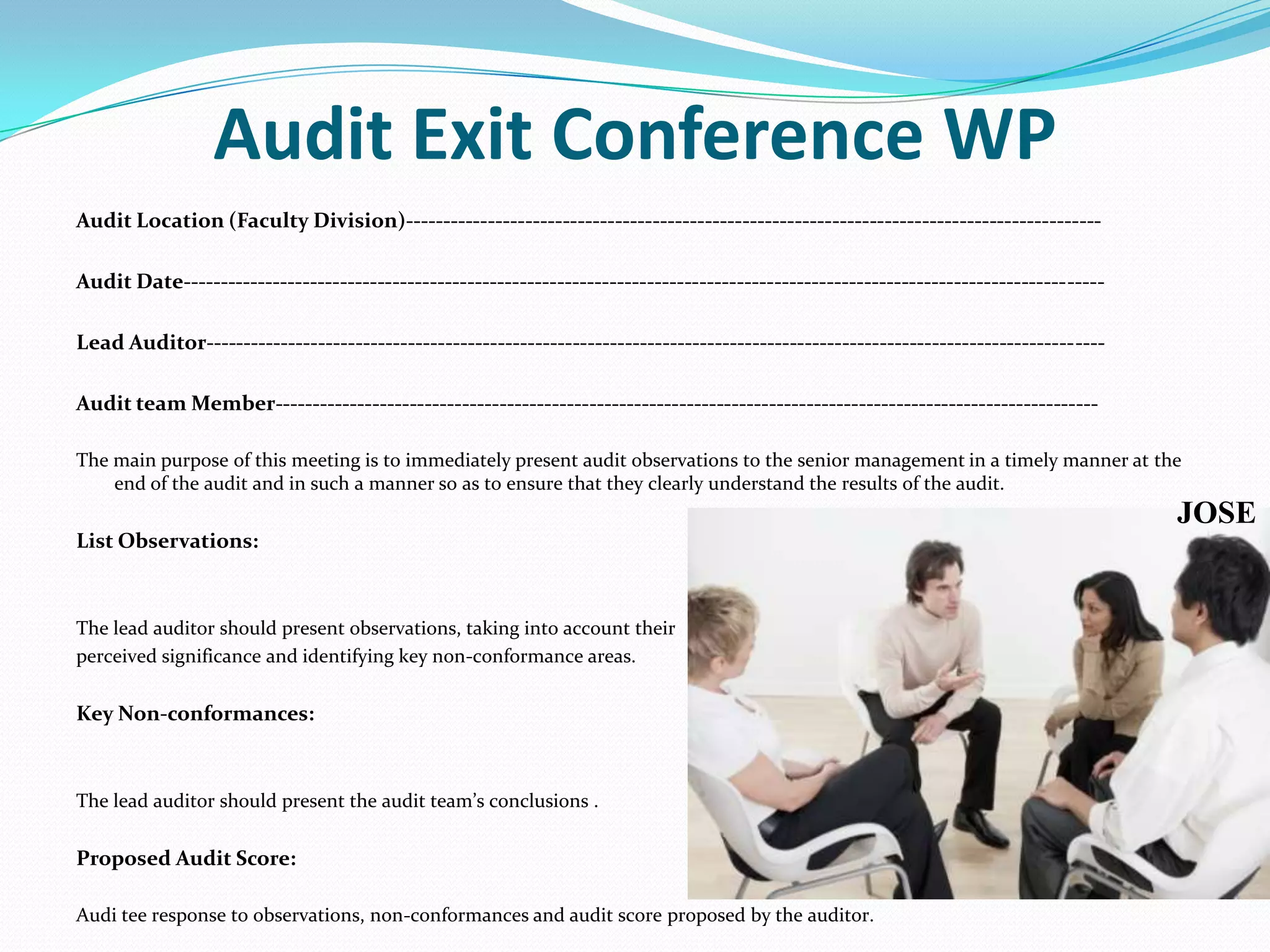

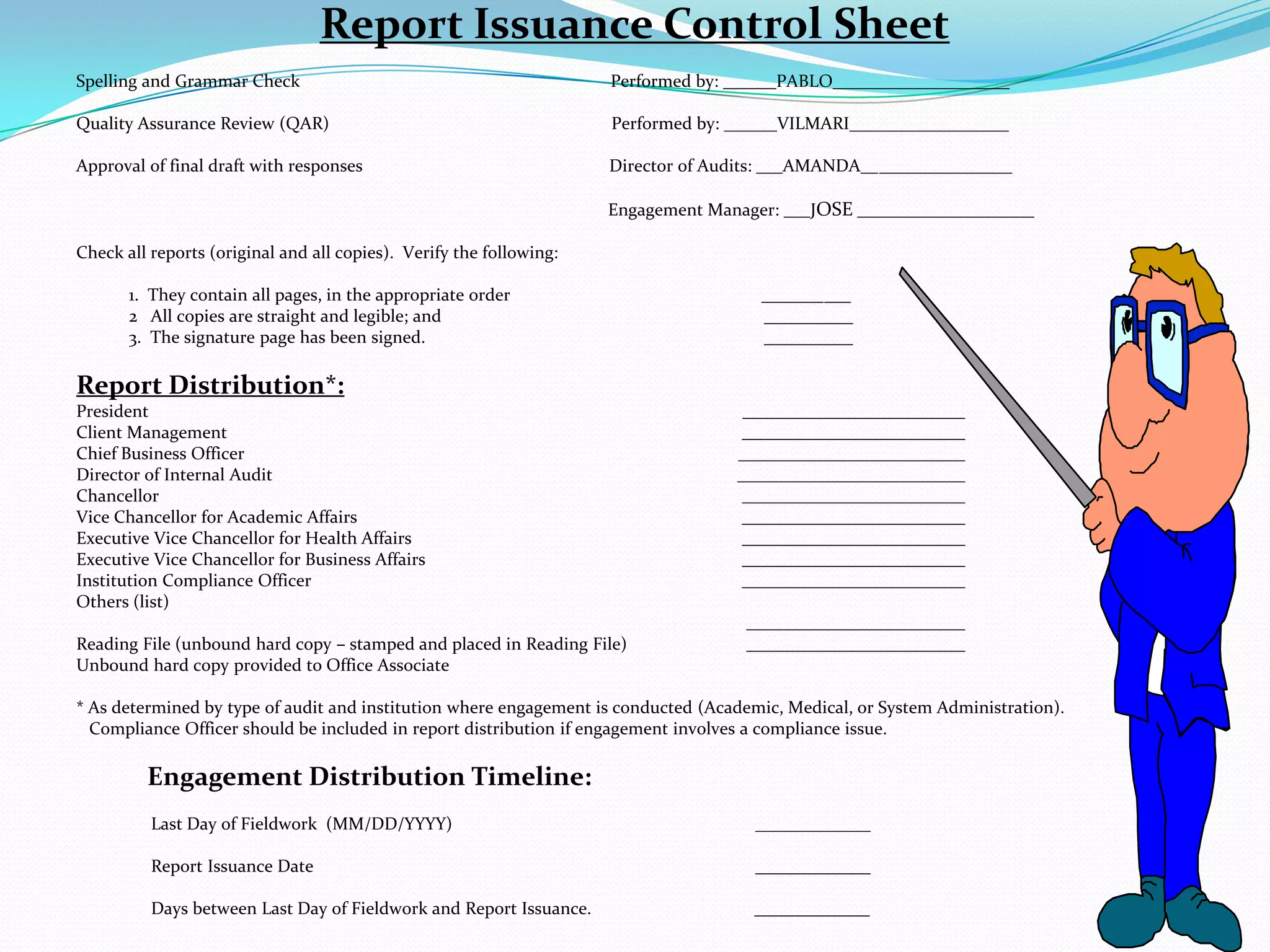

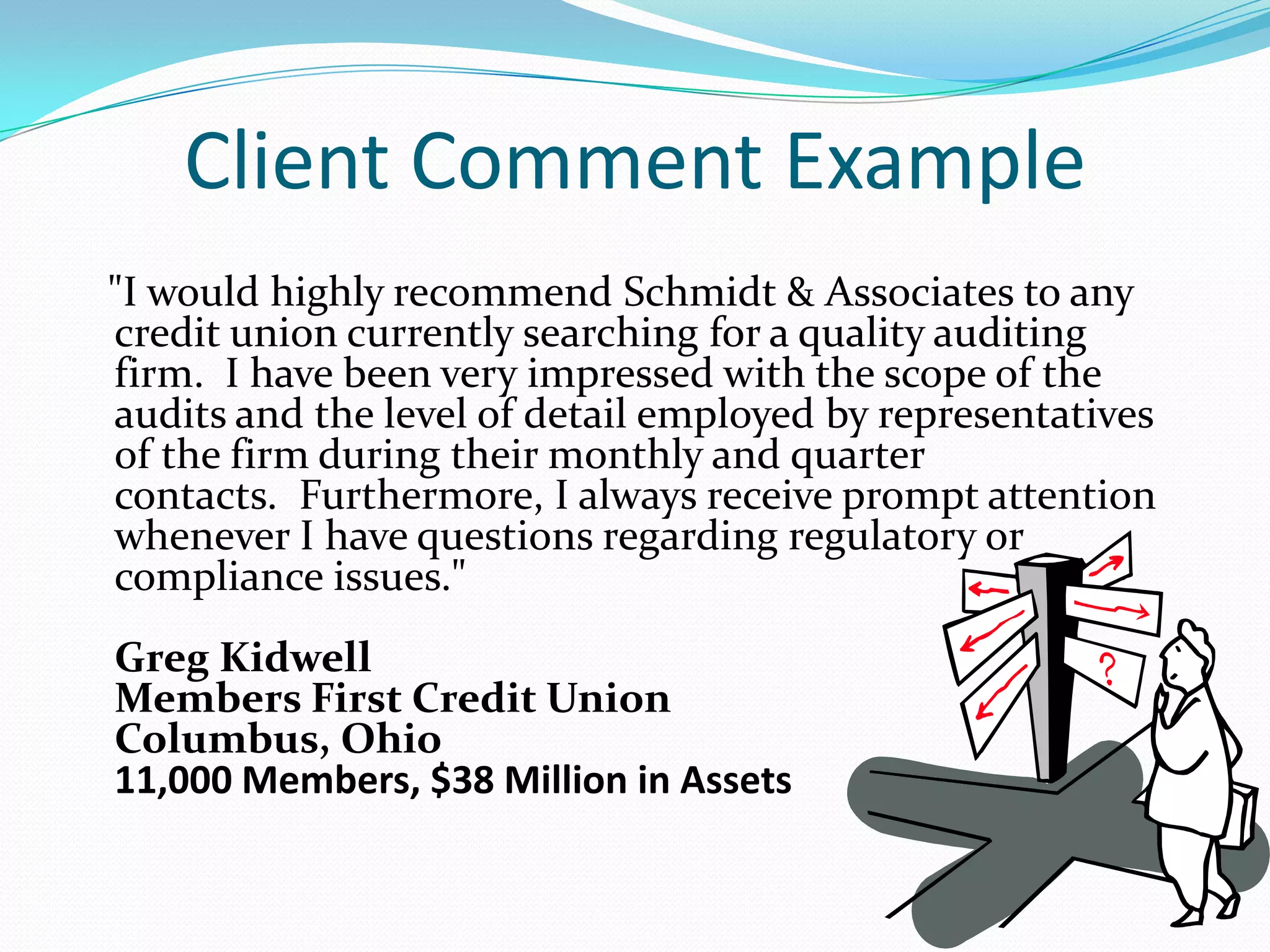

The document outlines the audit process, detailing stages such as planning, fieldwork, reporting, and follow-up, emphasizing client involvement at each stage. It explains internal control reviews, exit conferences, and the importance of addressing audit findings with proposed recommendations. The final audit report is issued after client feedback and is considered public information, with follow-up reviews conducted to ensure resolution of findings.