Downloaded 82 times

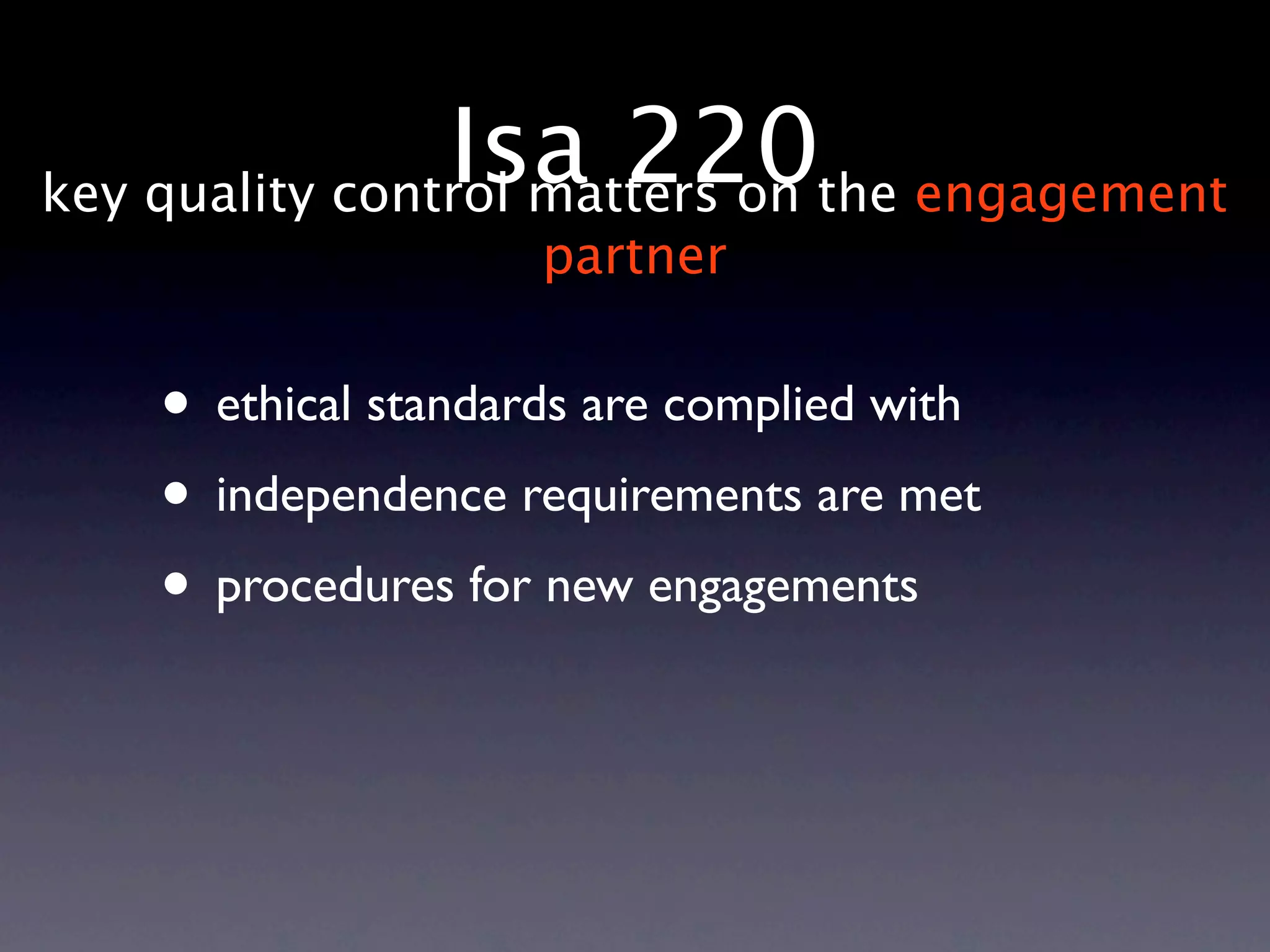

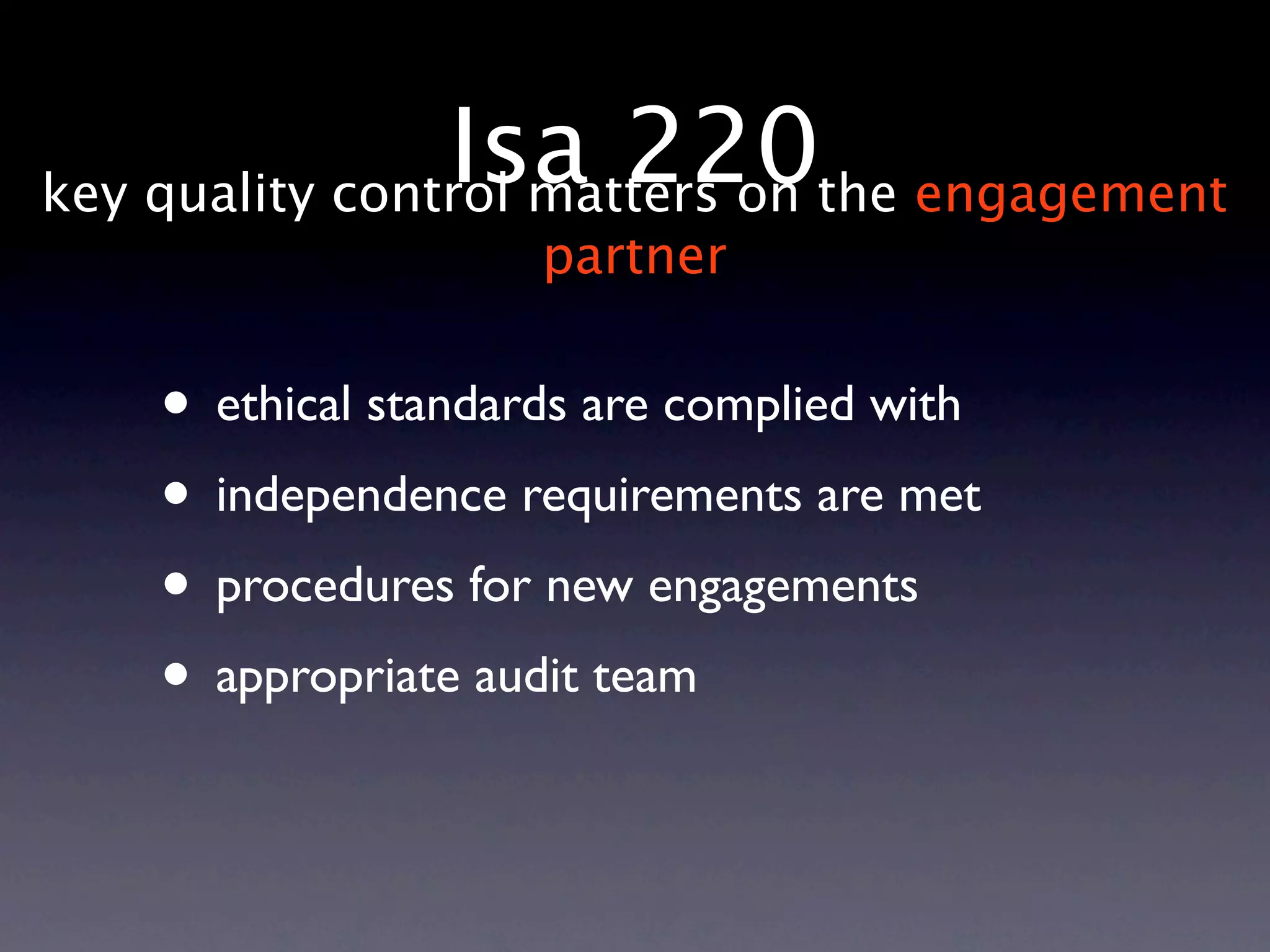

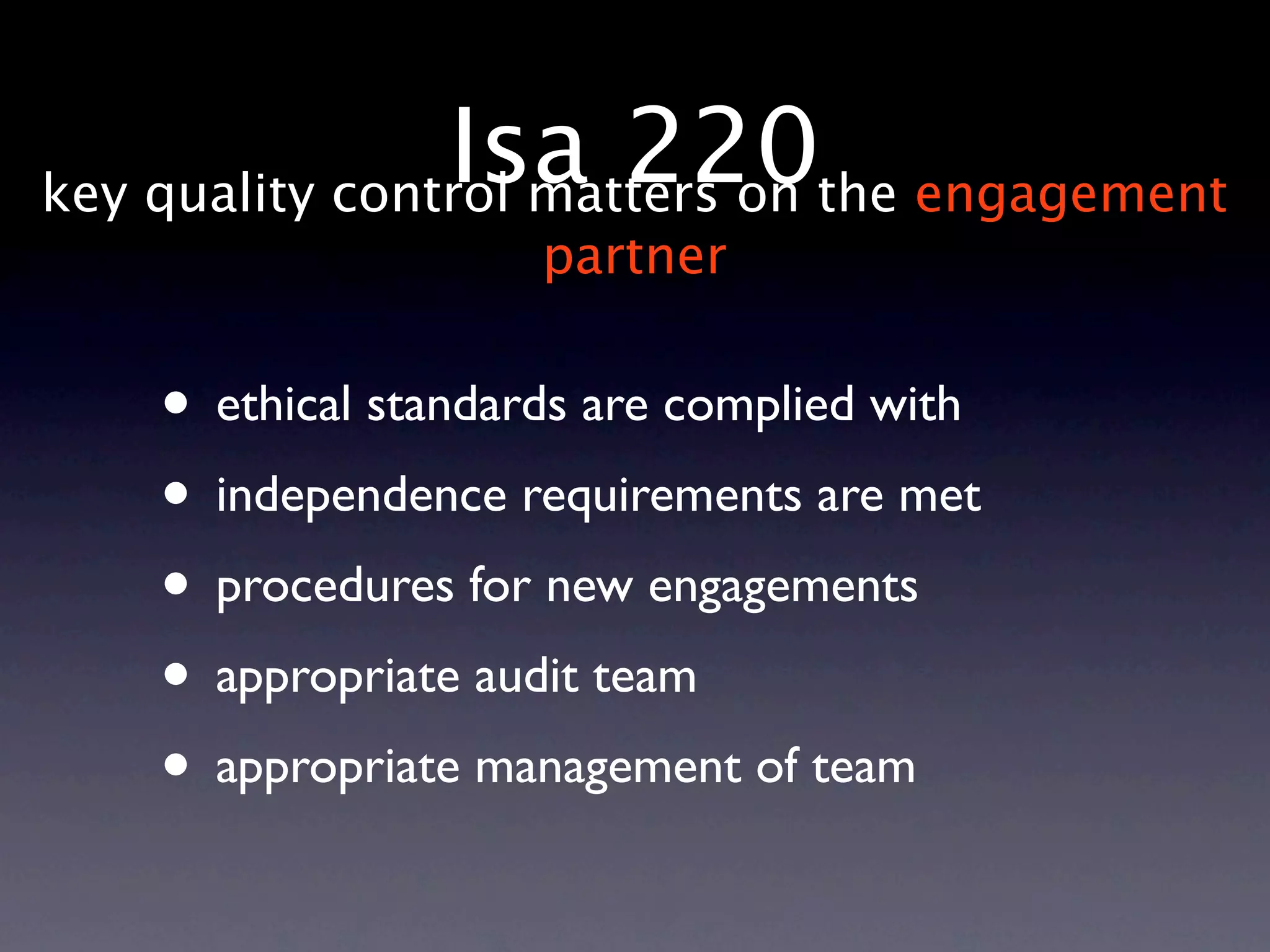

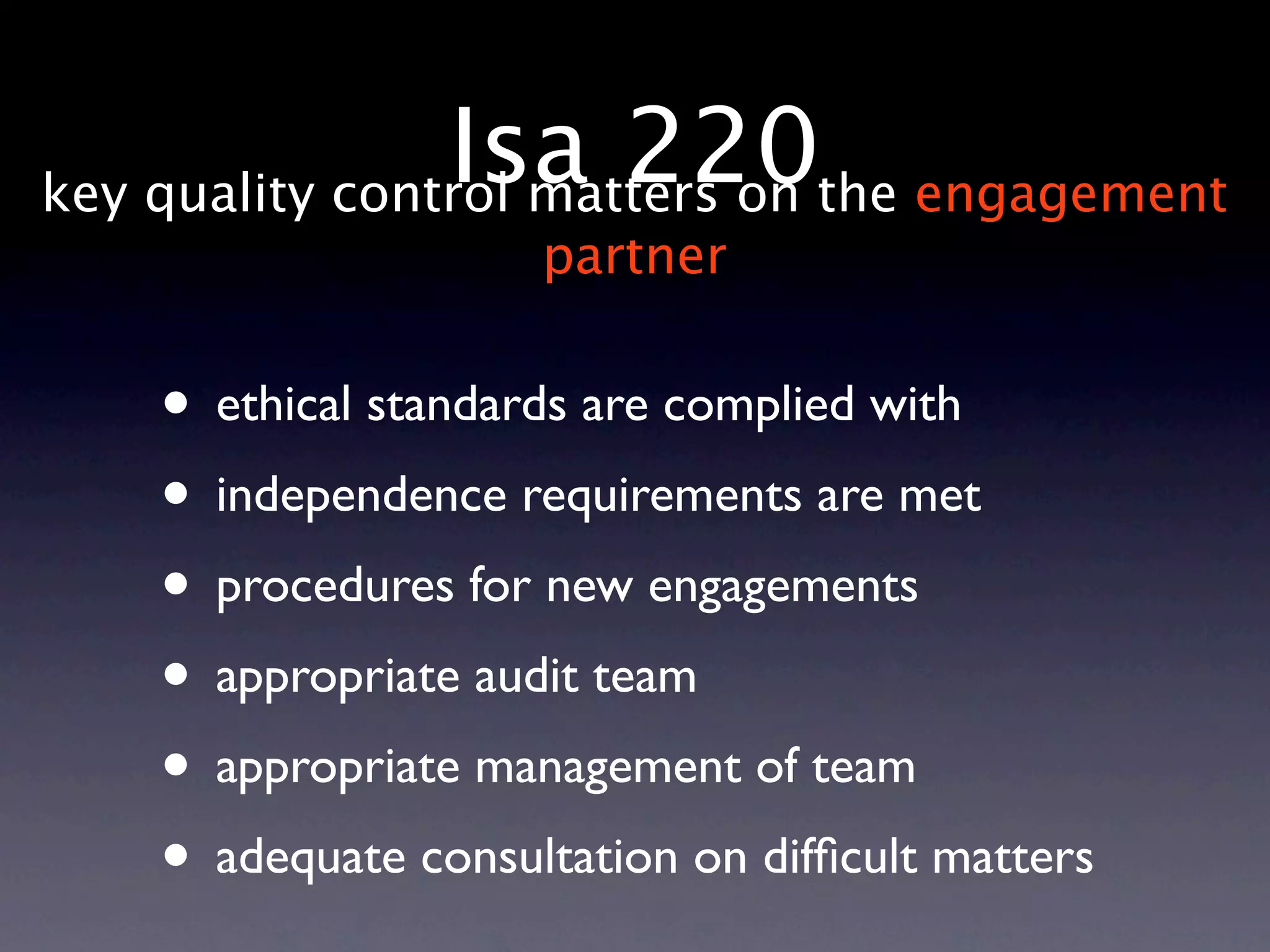

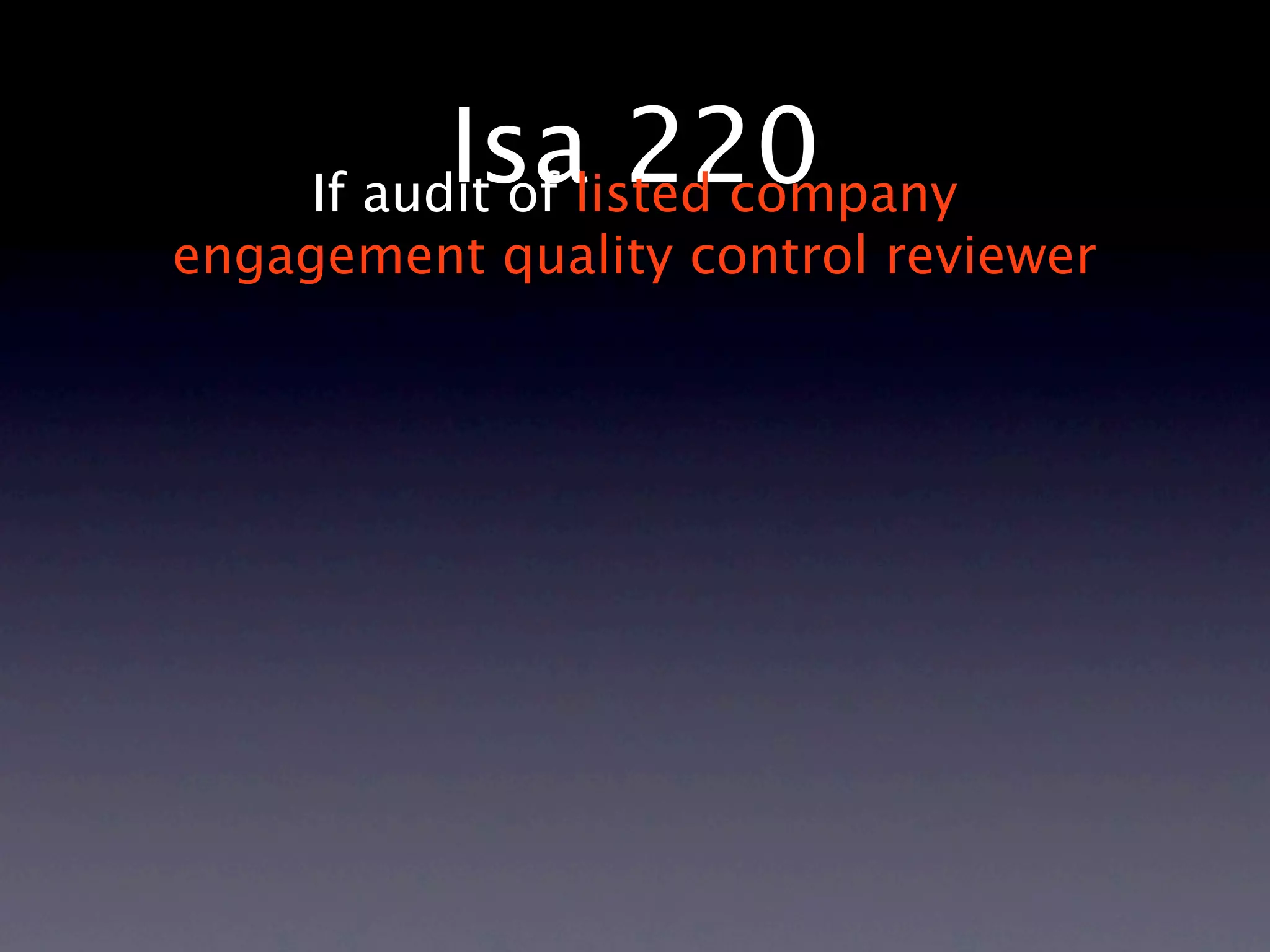

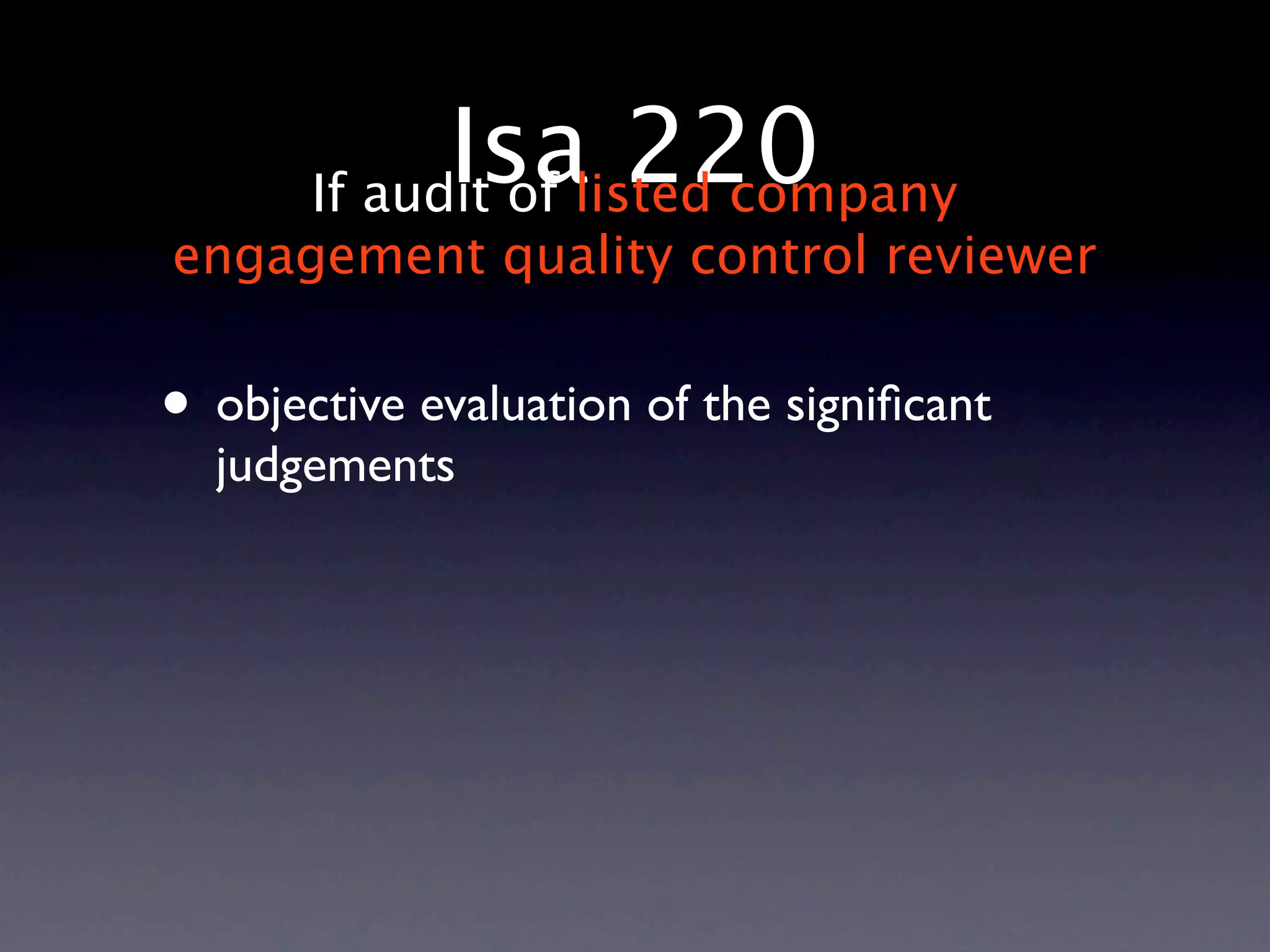

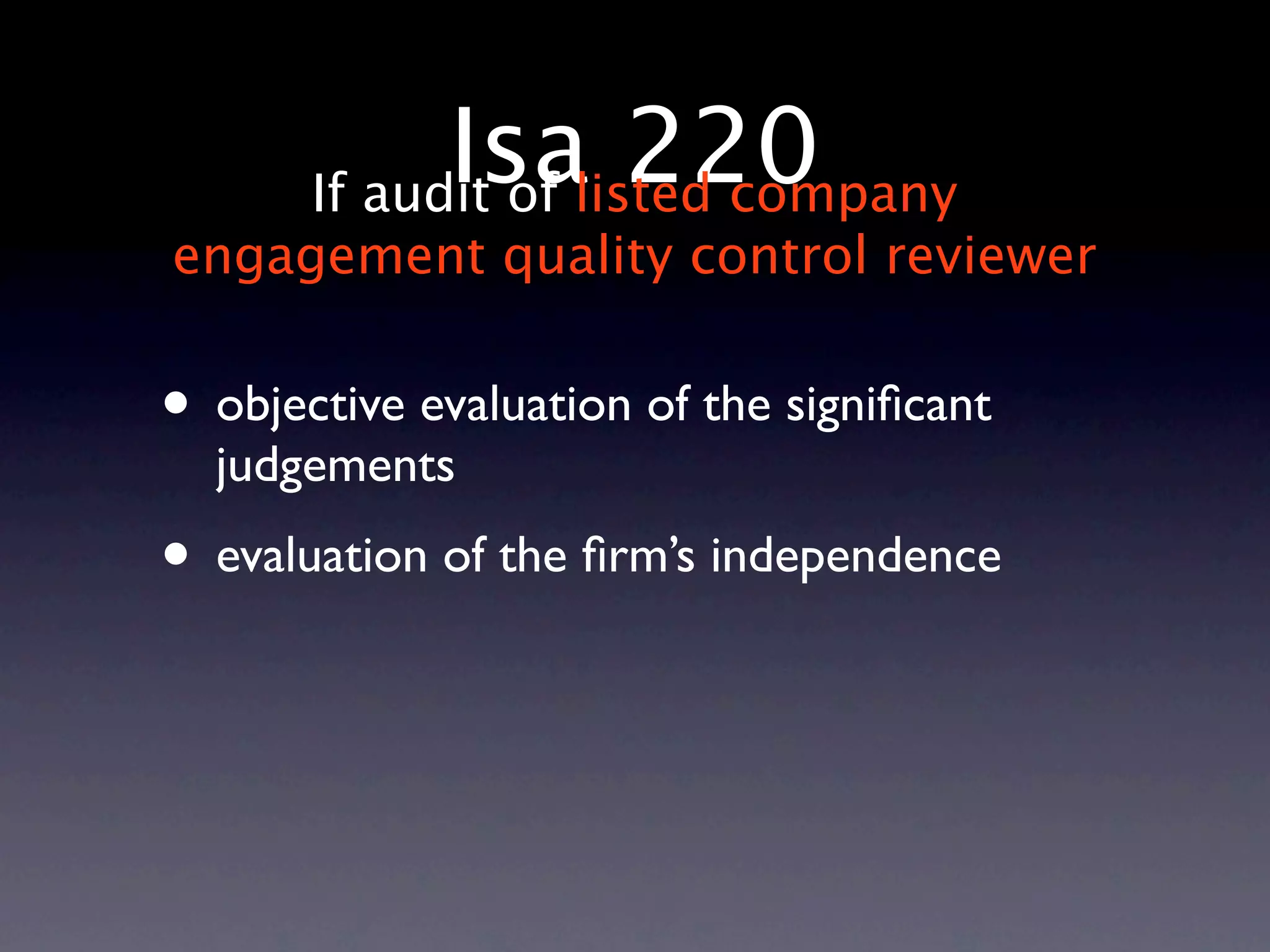

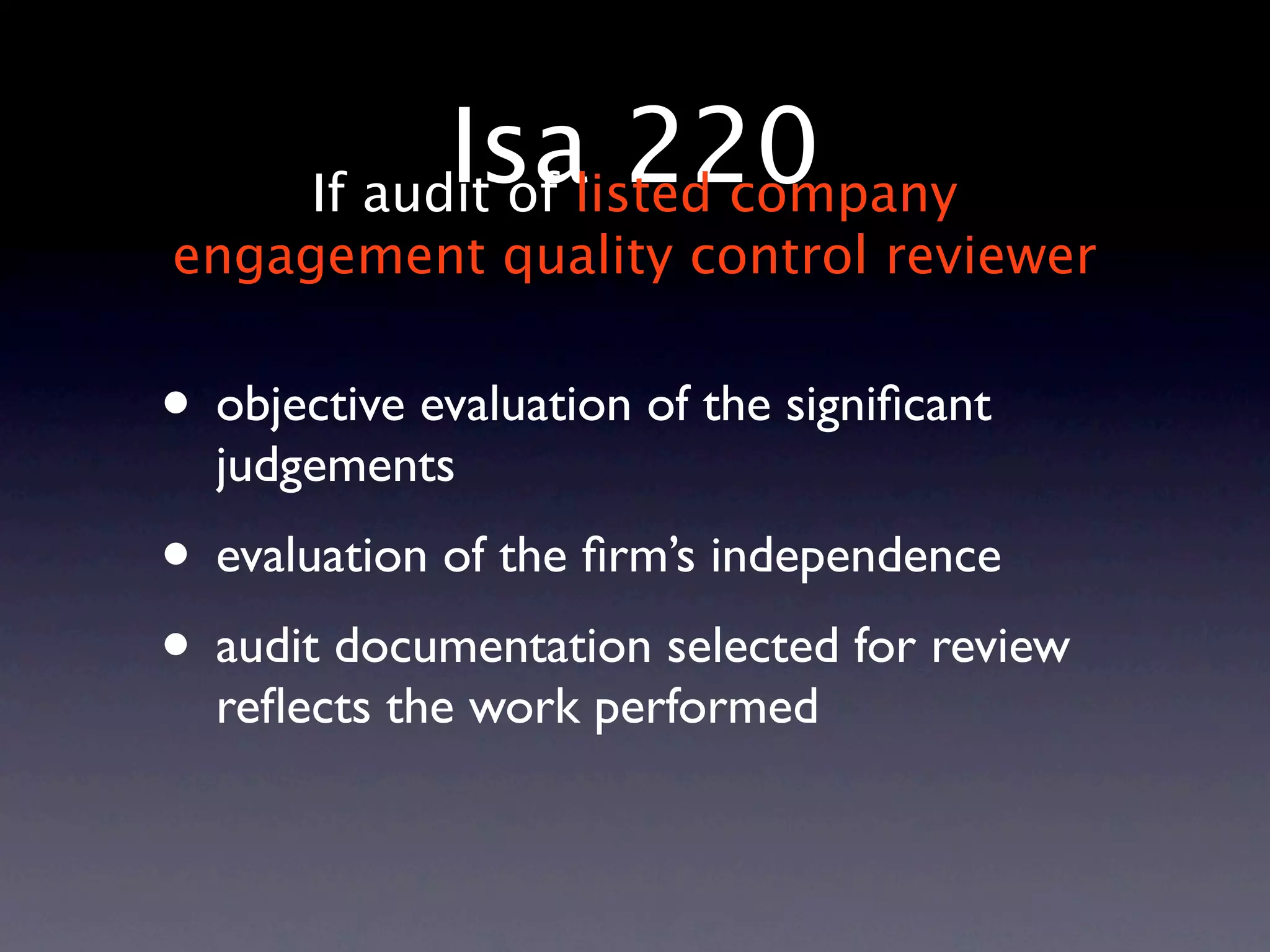

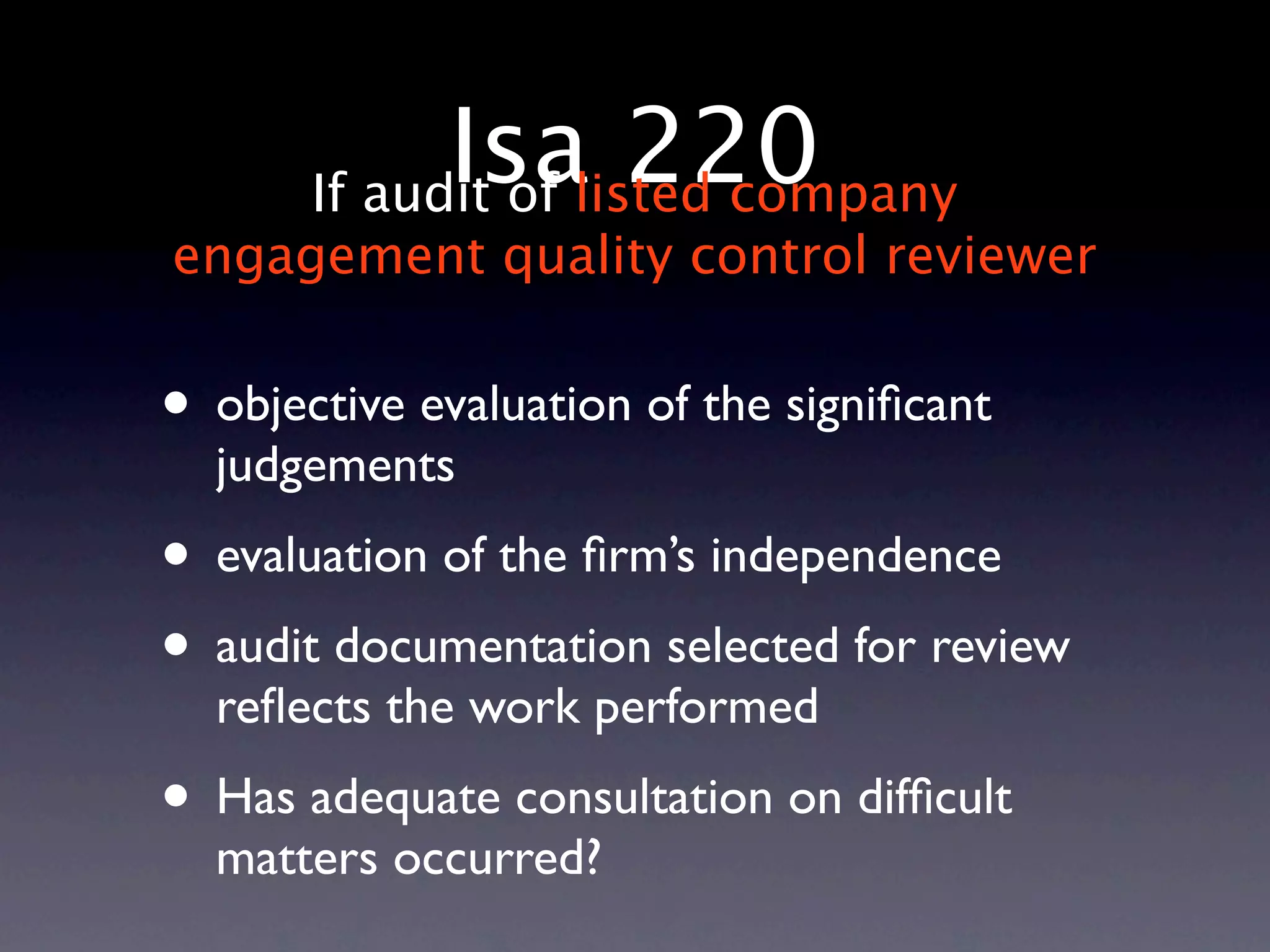

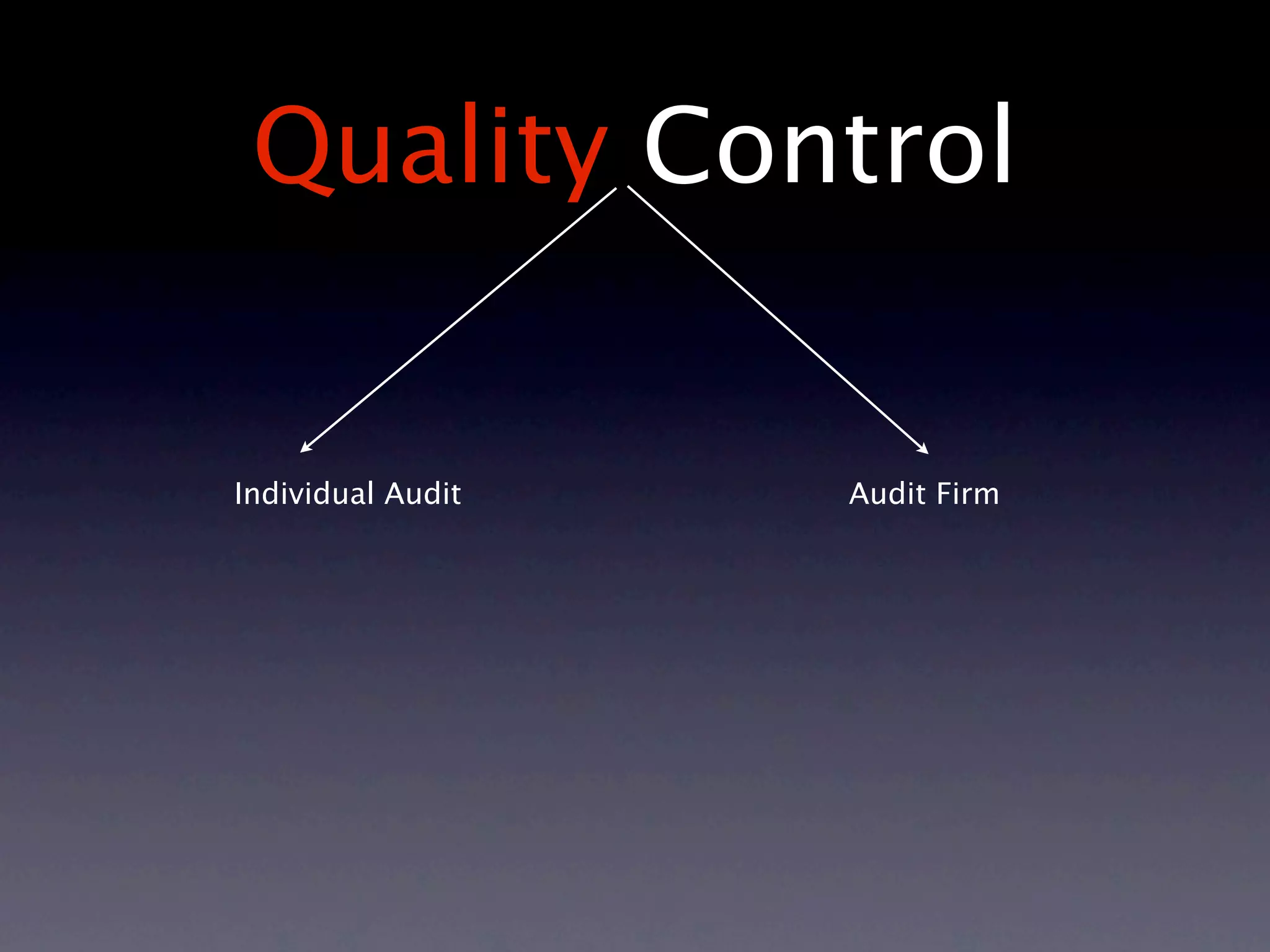

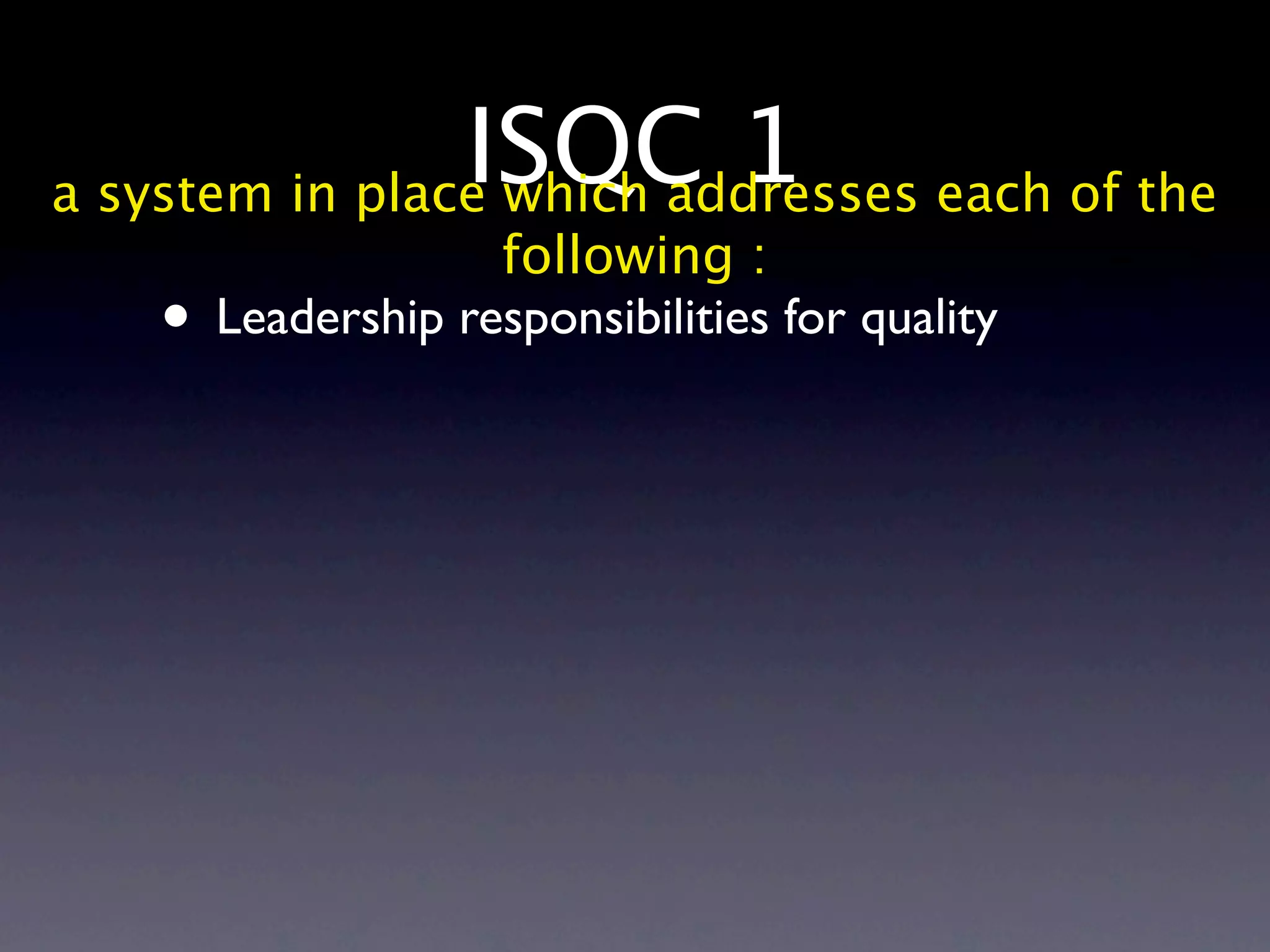

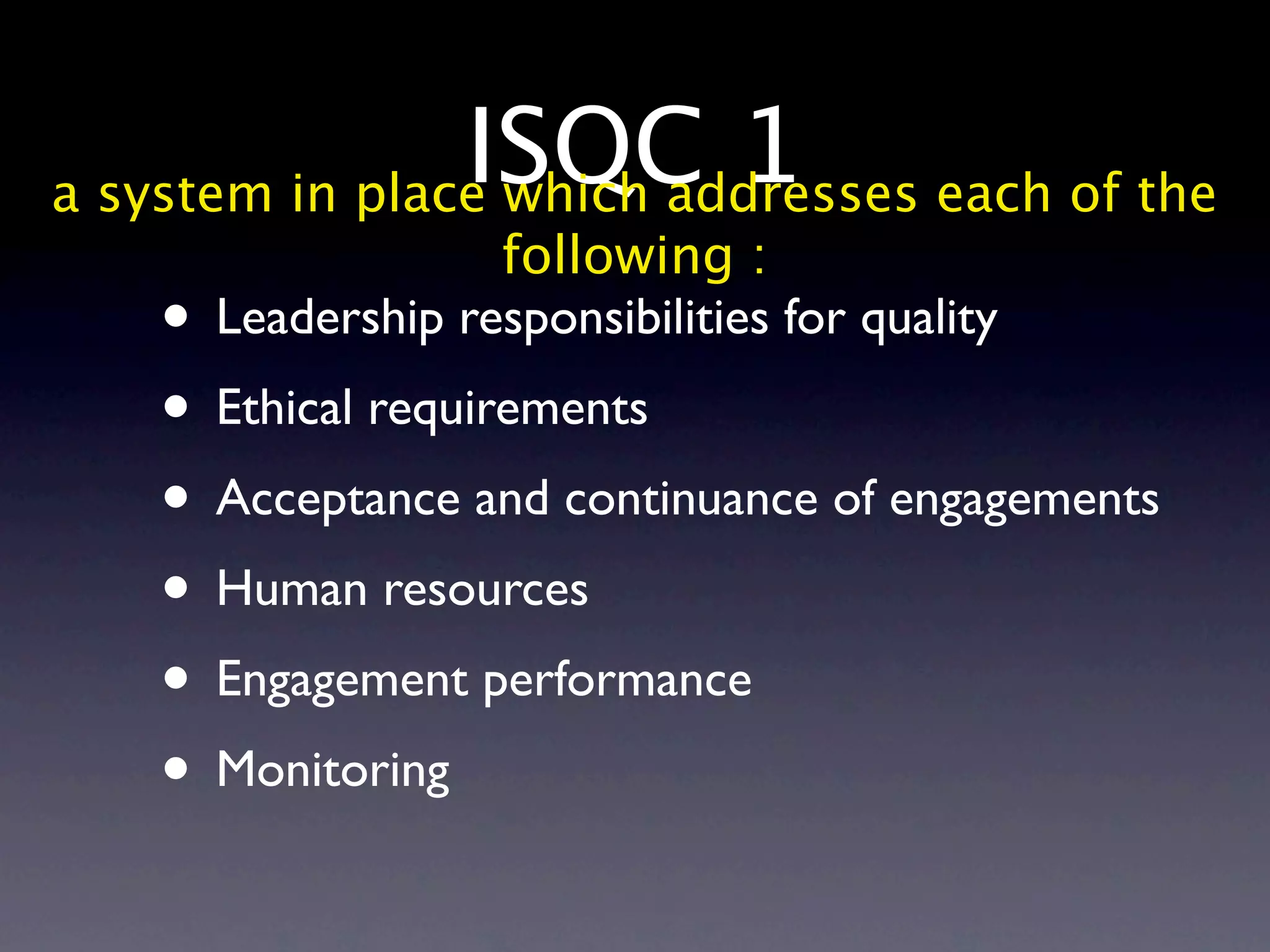

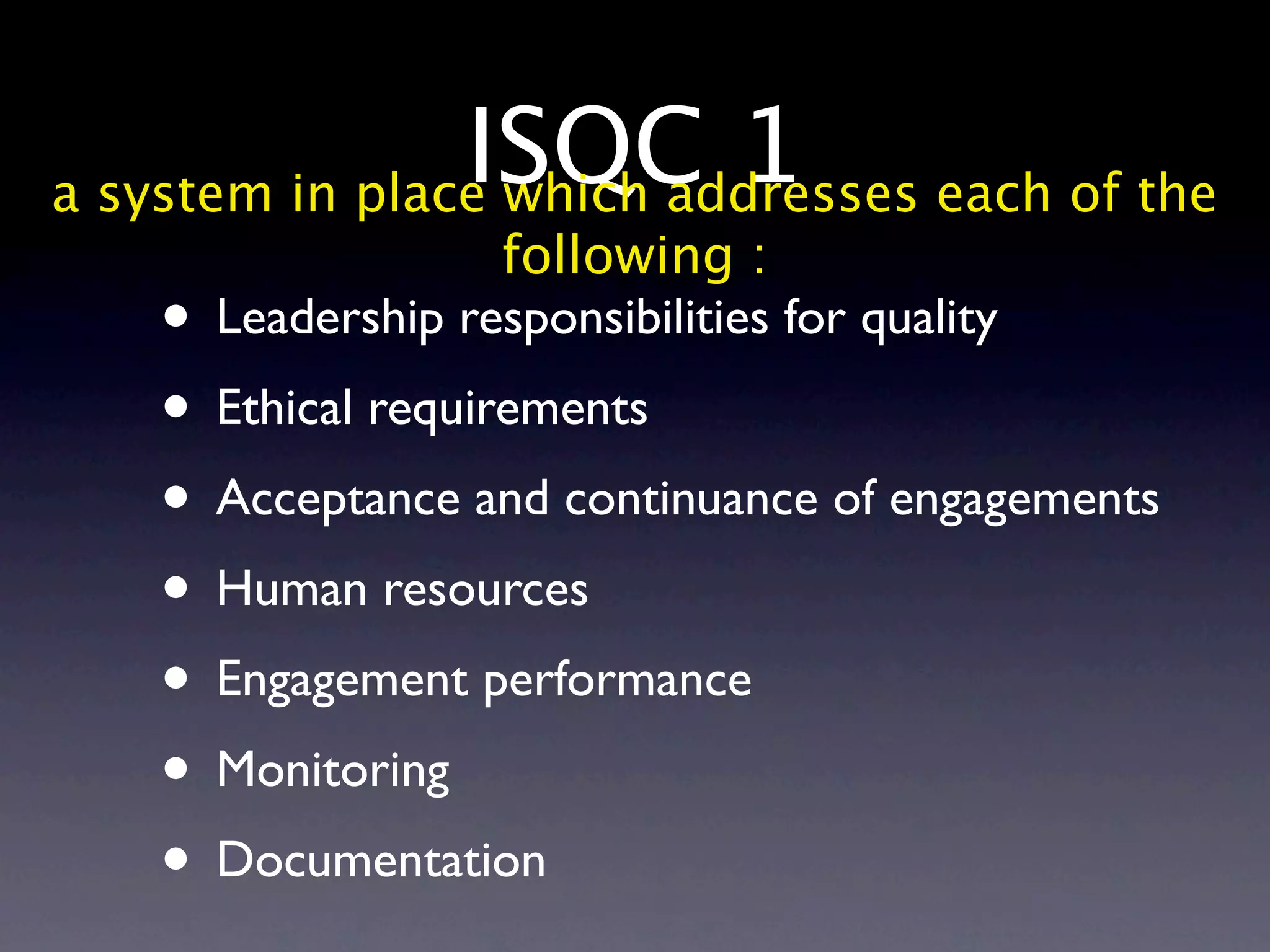

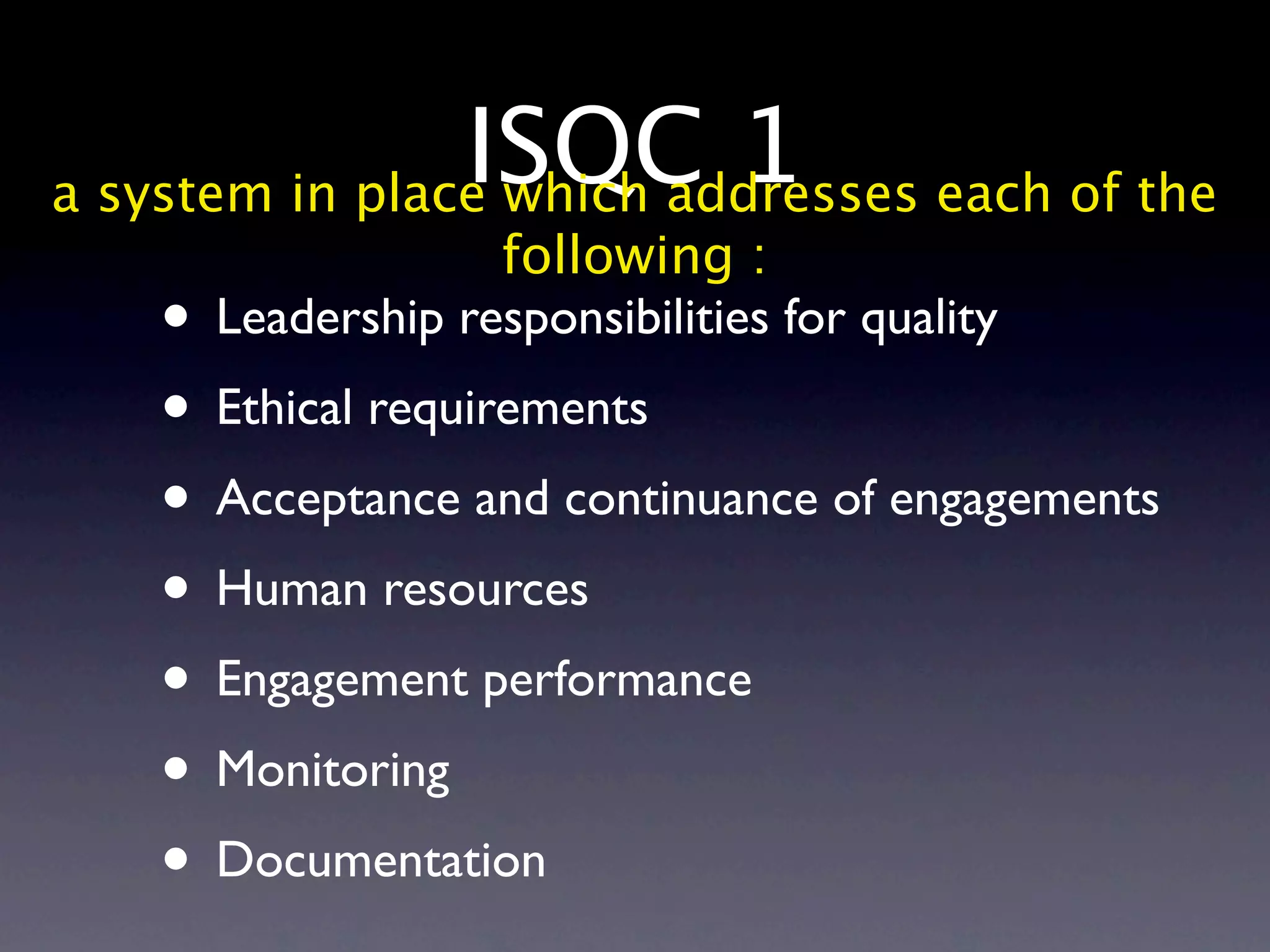

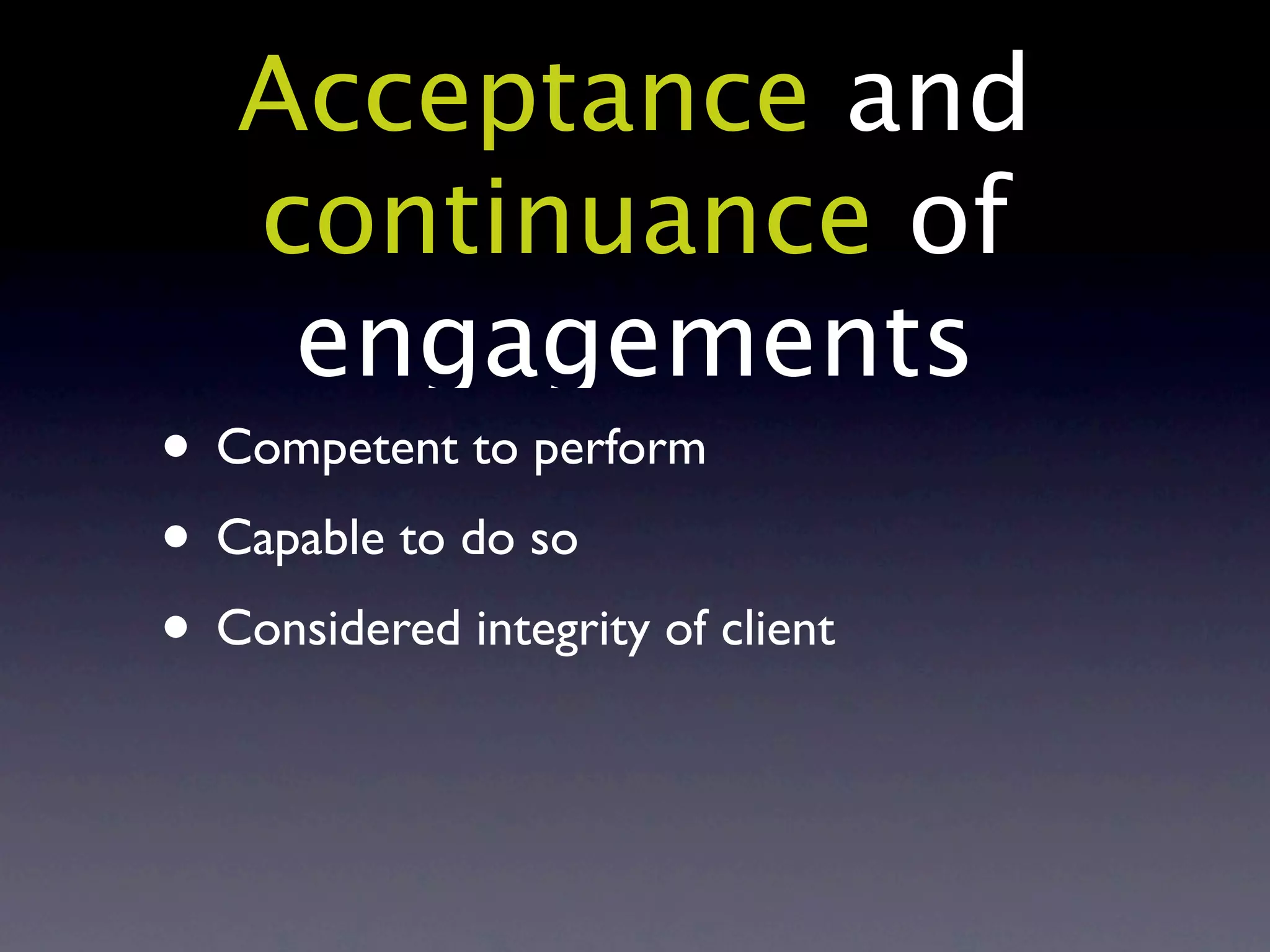

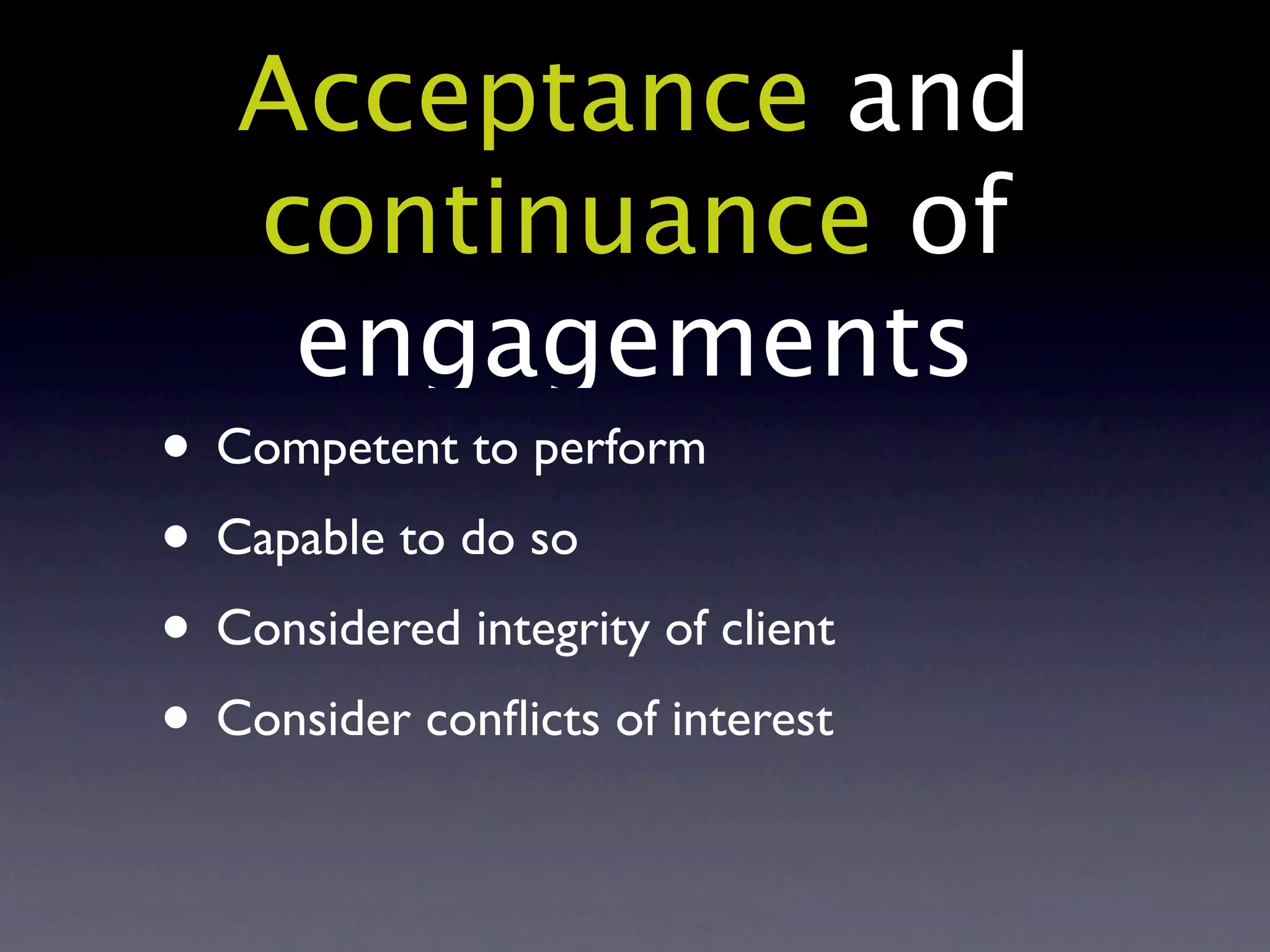

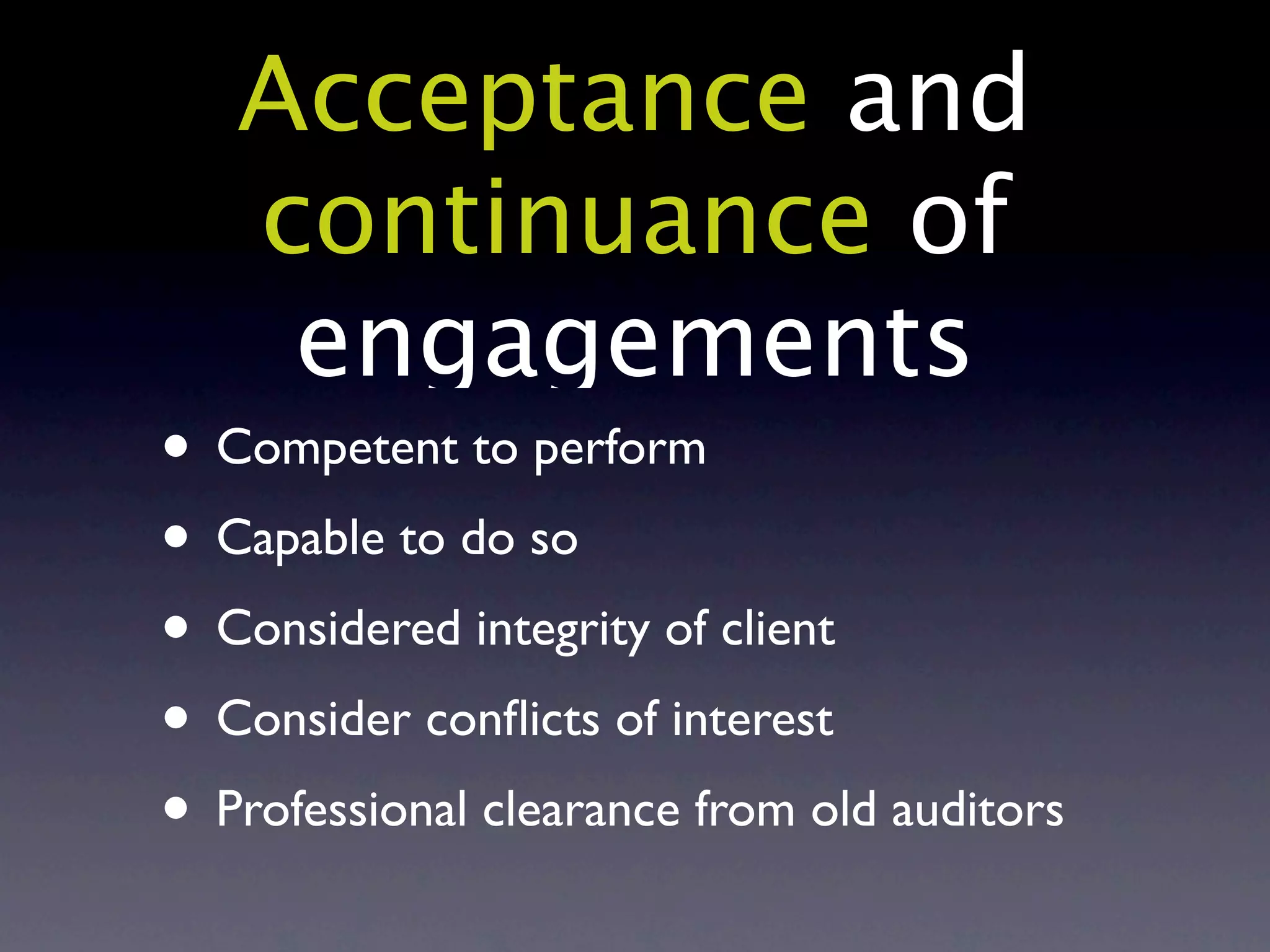

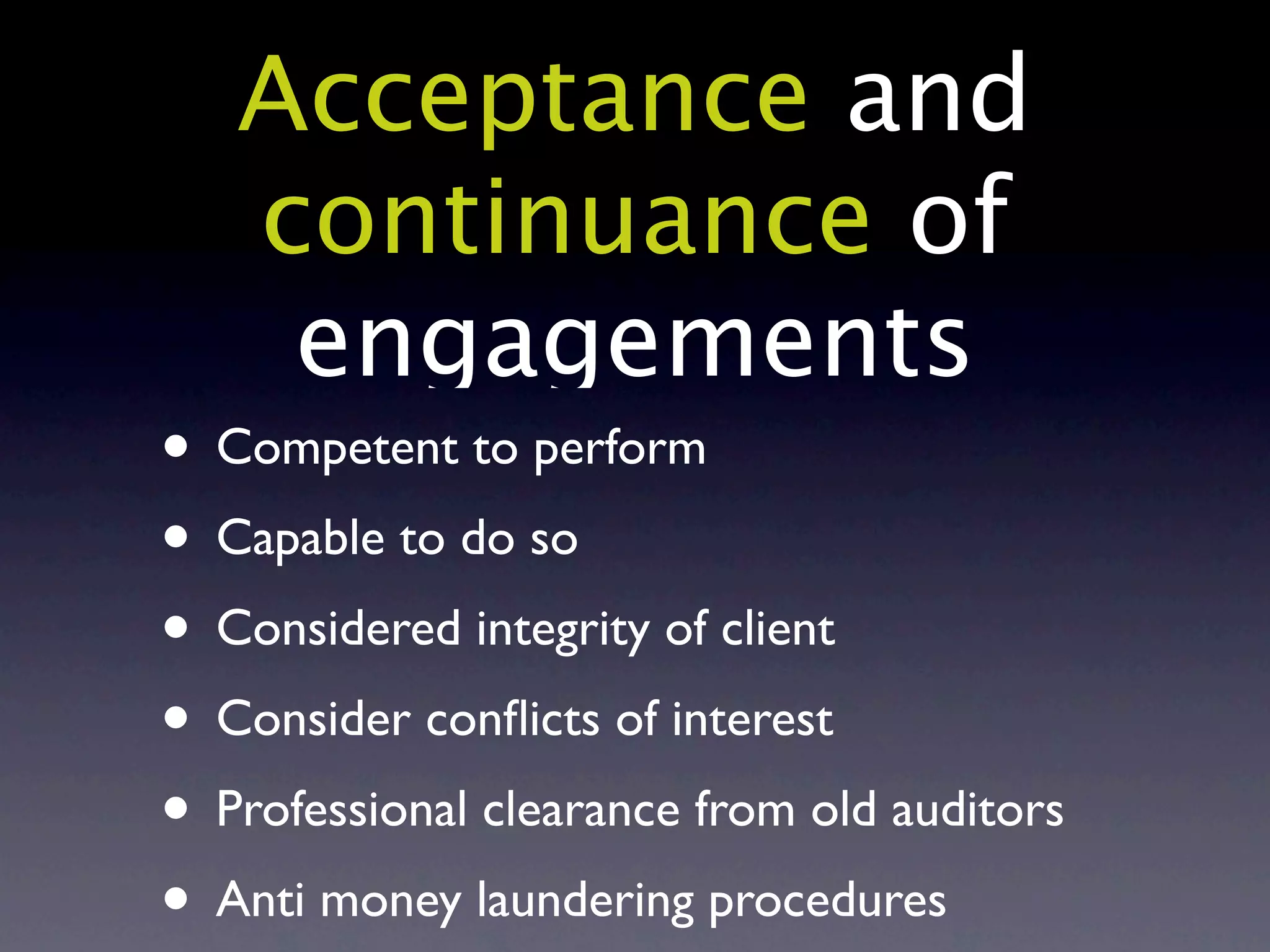

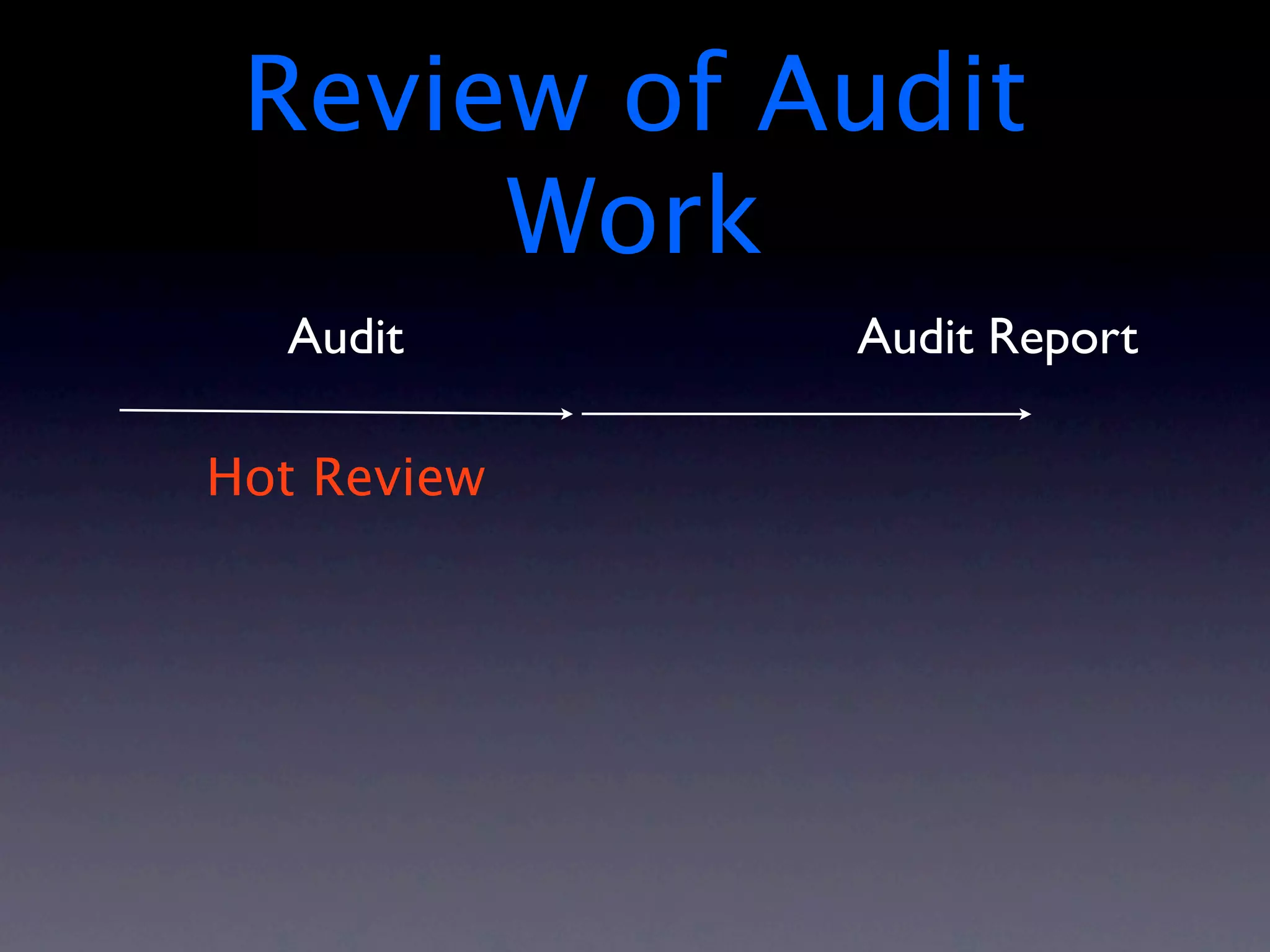

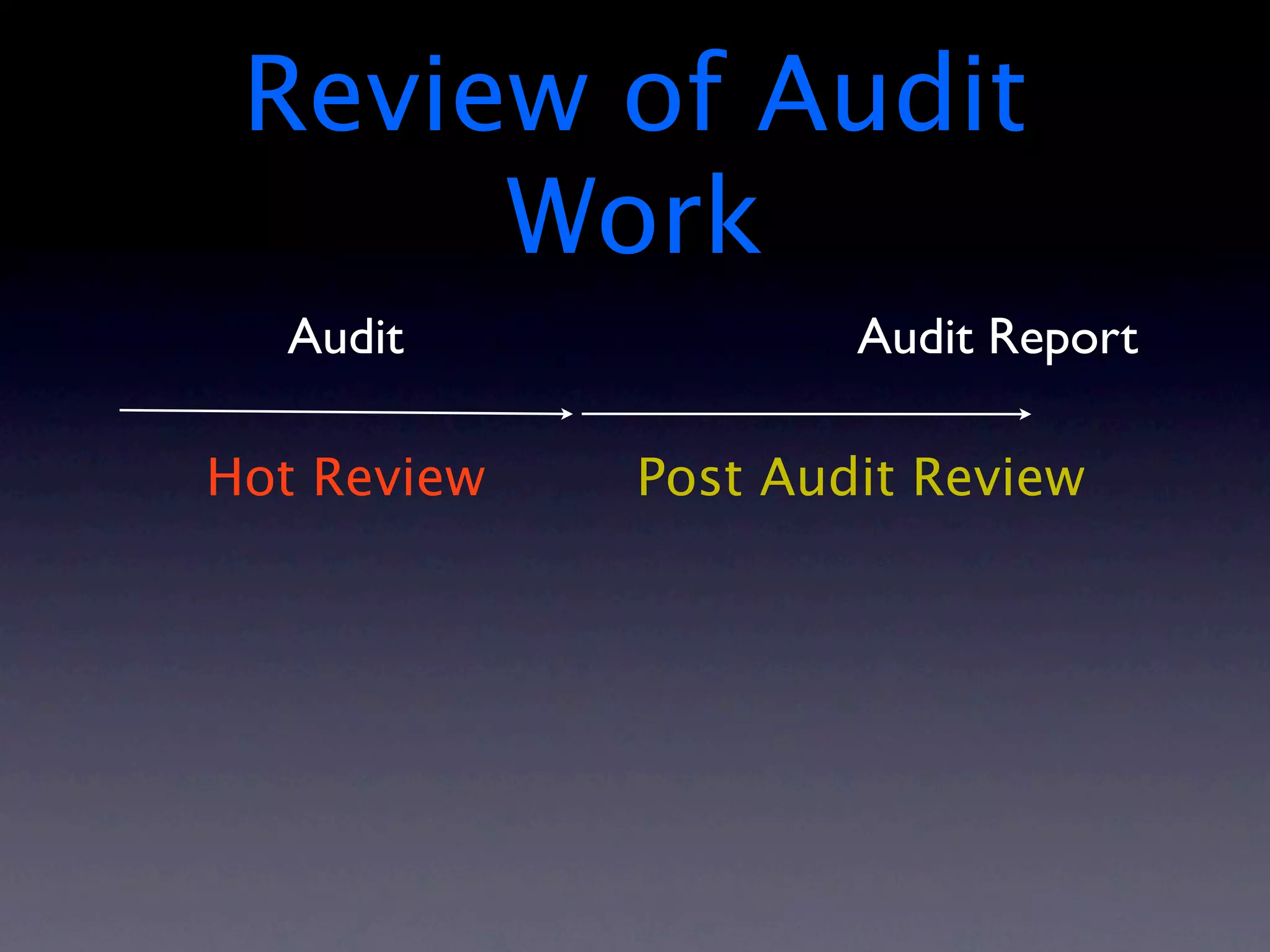

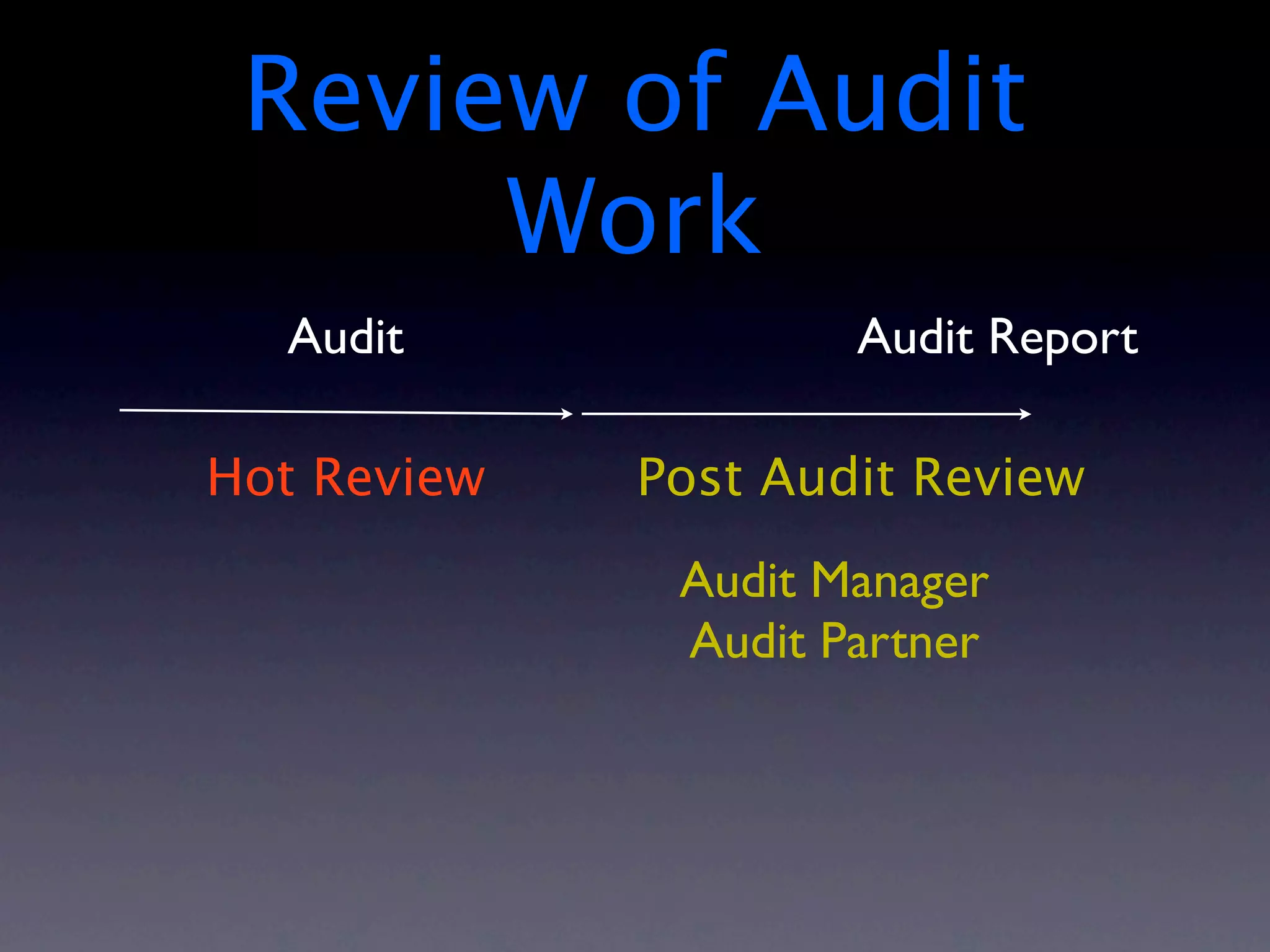

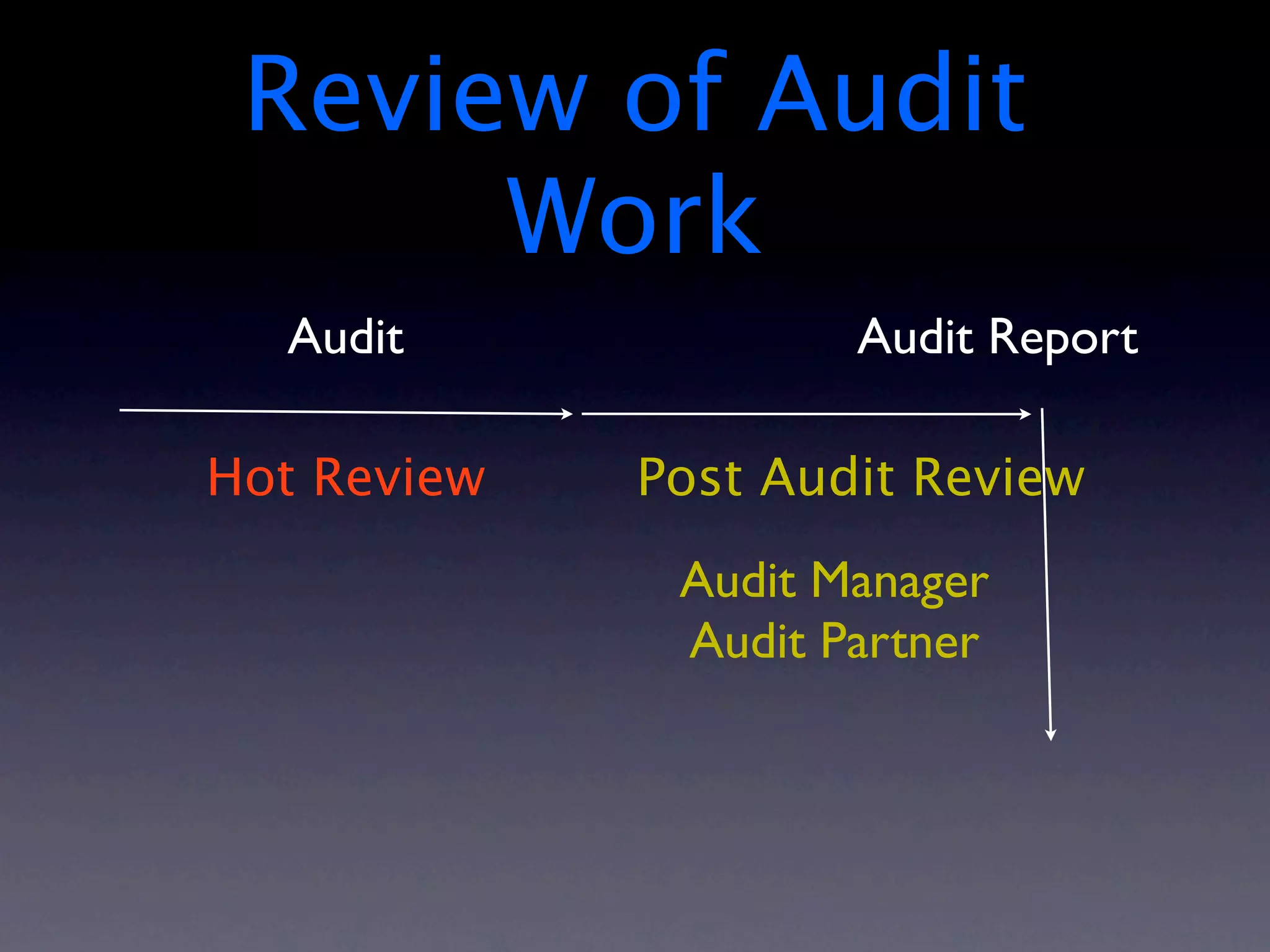

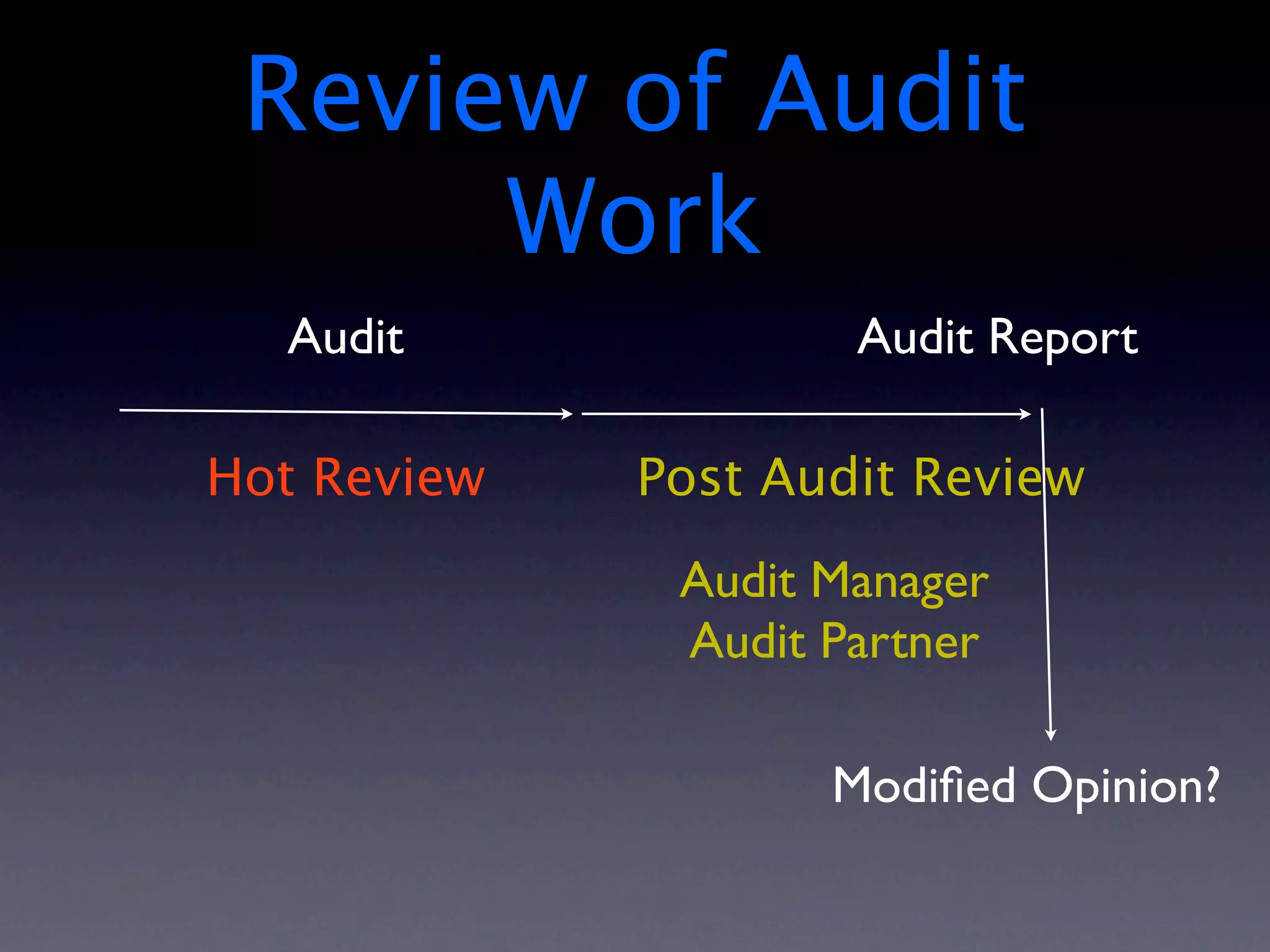

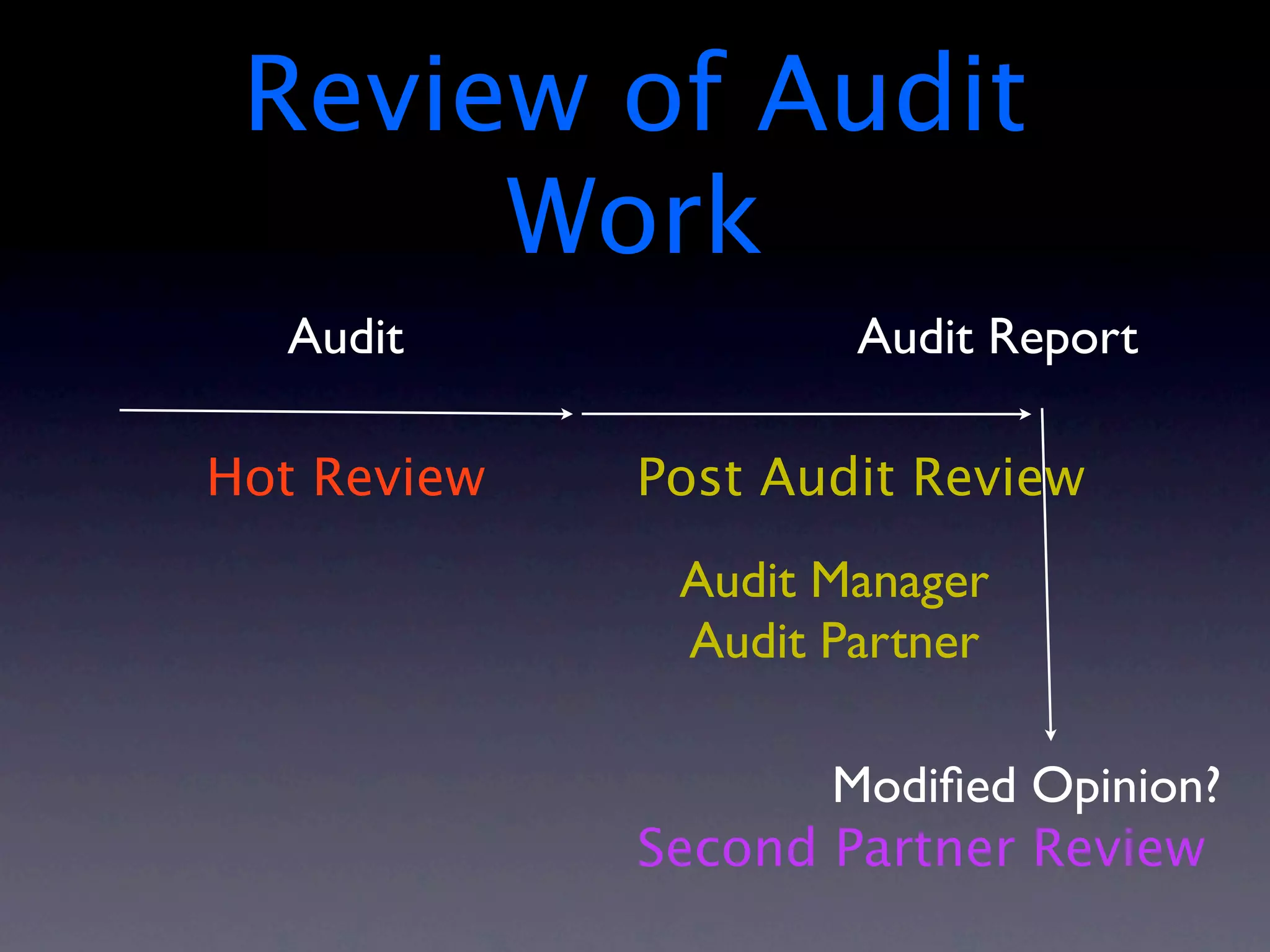

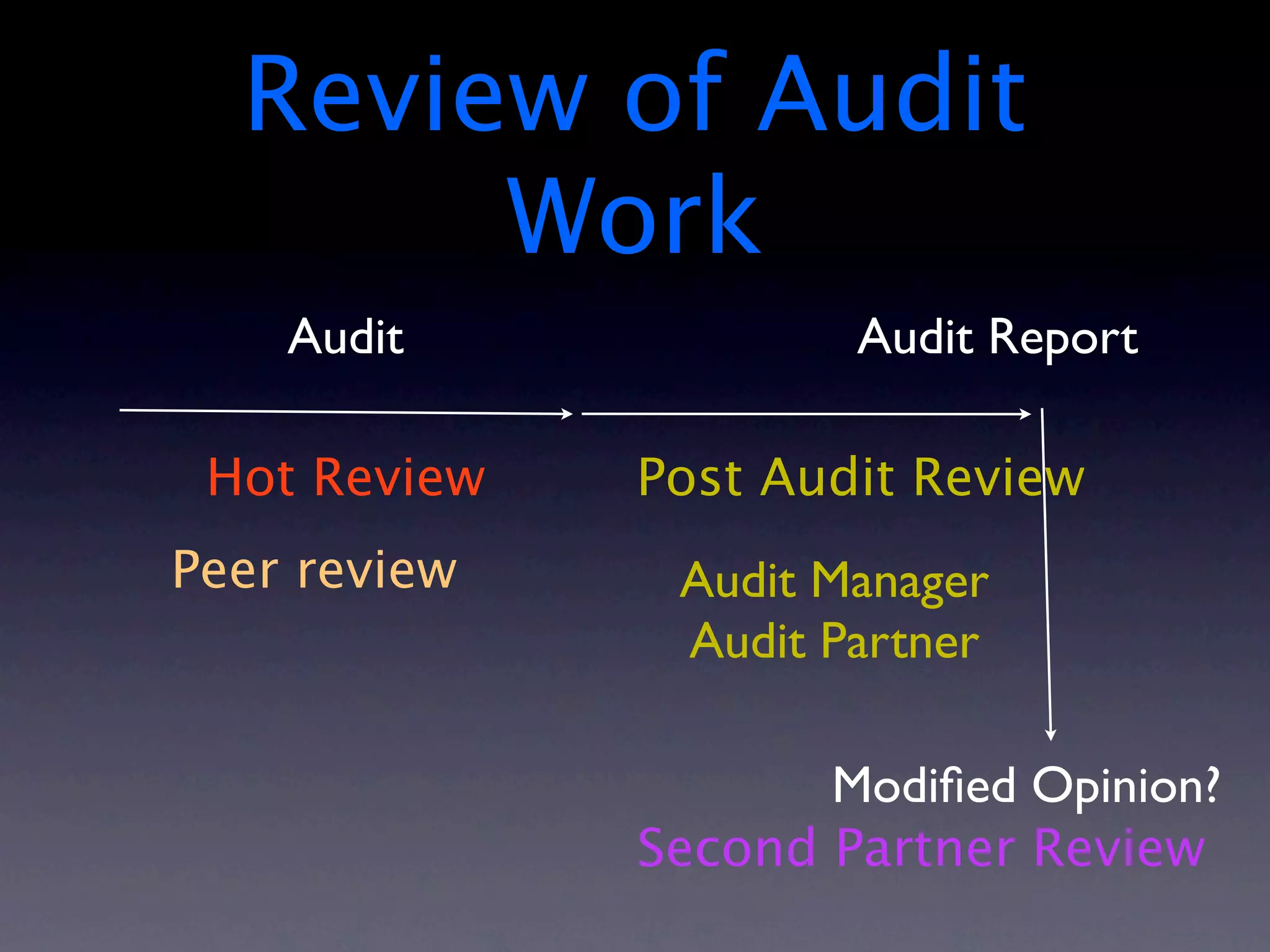

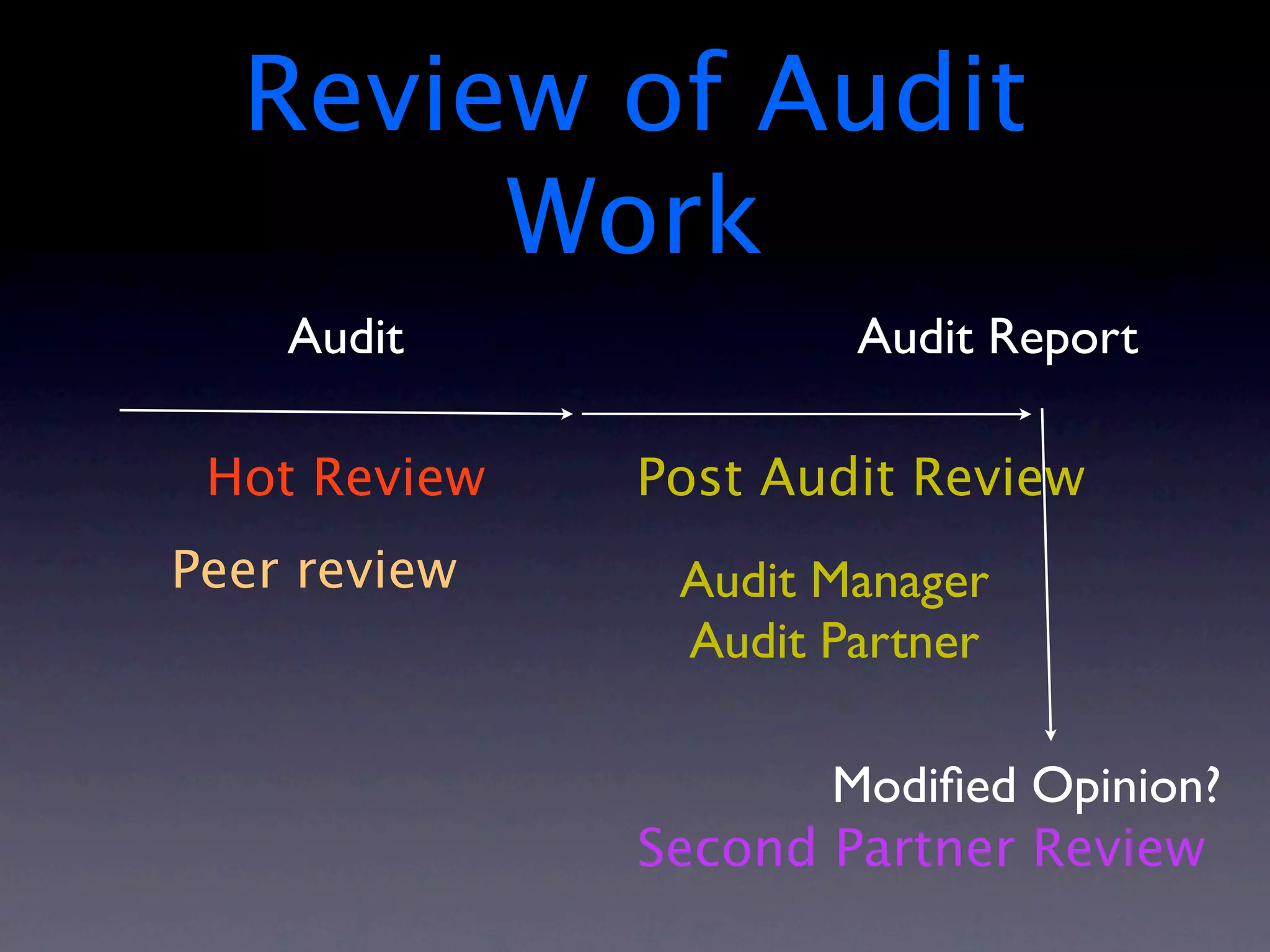

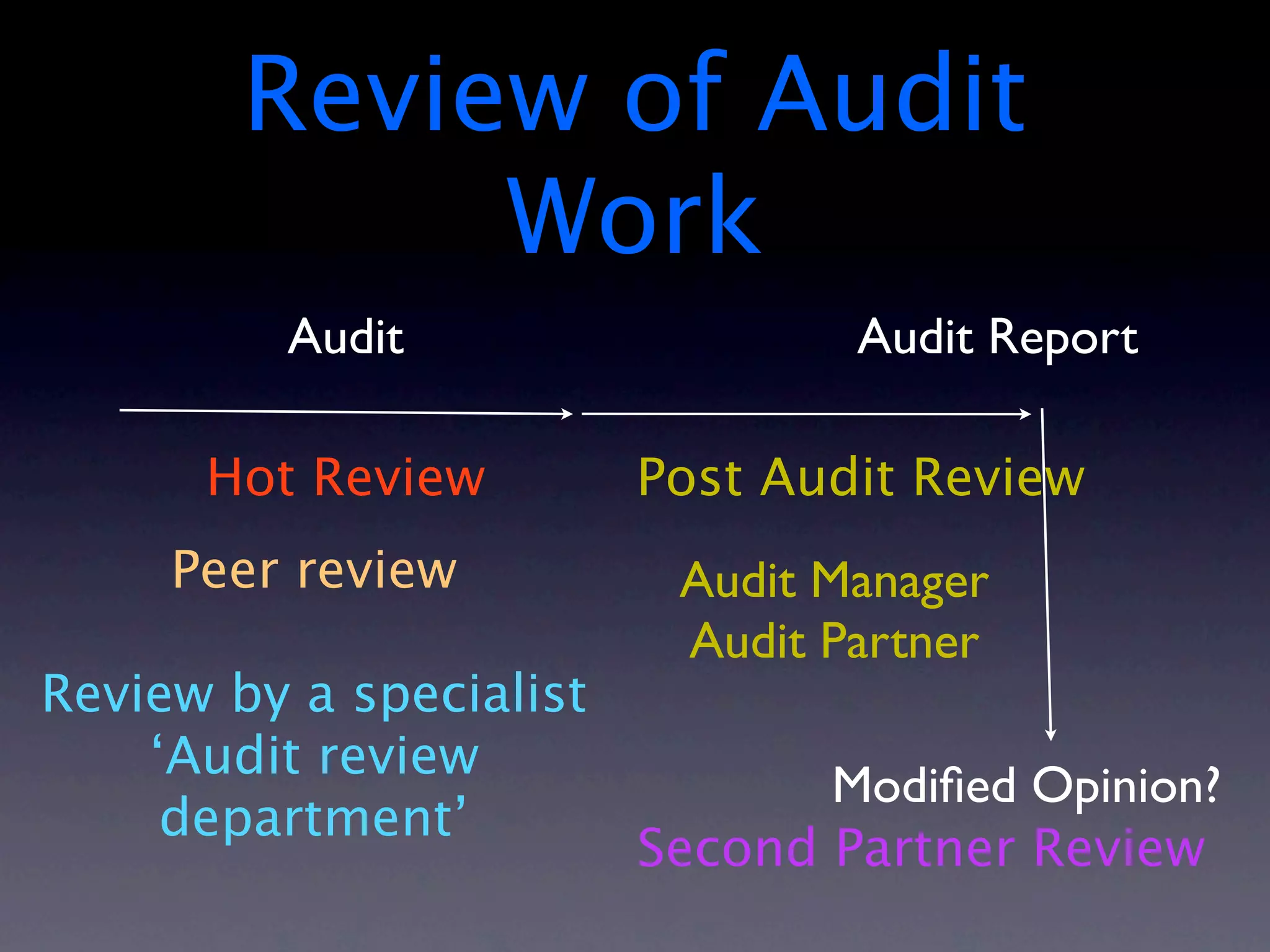

The document discusses quality control procedures for audit firms. It covers establishing a quality control system that addresses leadership responsibilities, ethical requirements, acceptance and continuance of engagements, human resources, engagement performance, monitoring, and documentation. It also discusses quality control procedures for individual audits, including direction of audit staff, hot reviews, post-audit reviews, and reviews by managers, partners and specialists.

![IRDA [Insurance Regulatory and Development Authority]](https://cdn.slidesharecdn.com/ss_thumbnails/ibegropu07-171025144708-thumbnail.jpg?width=640&height=640&fit=bounds)