Standard costing is a cost control method aimed at reducing expenses while maintaining product quality by setting predetermined cost targets against which actual costs are measured. It involves analyzing variances between standard and actual costs to improve efficiency and reduce wastage. While it has advantages like improved managerial control and cost reduction, it also faces limitations such as the difficulty in establishing appropriate standards and the risk of outdated or rigid benchmarks.

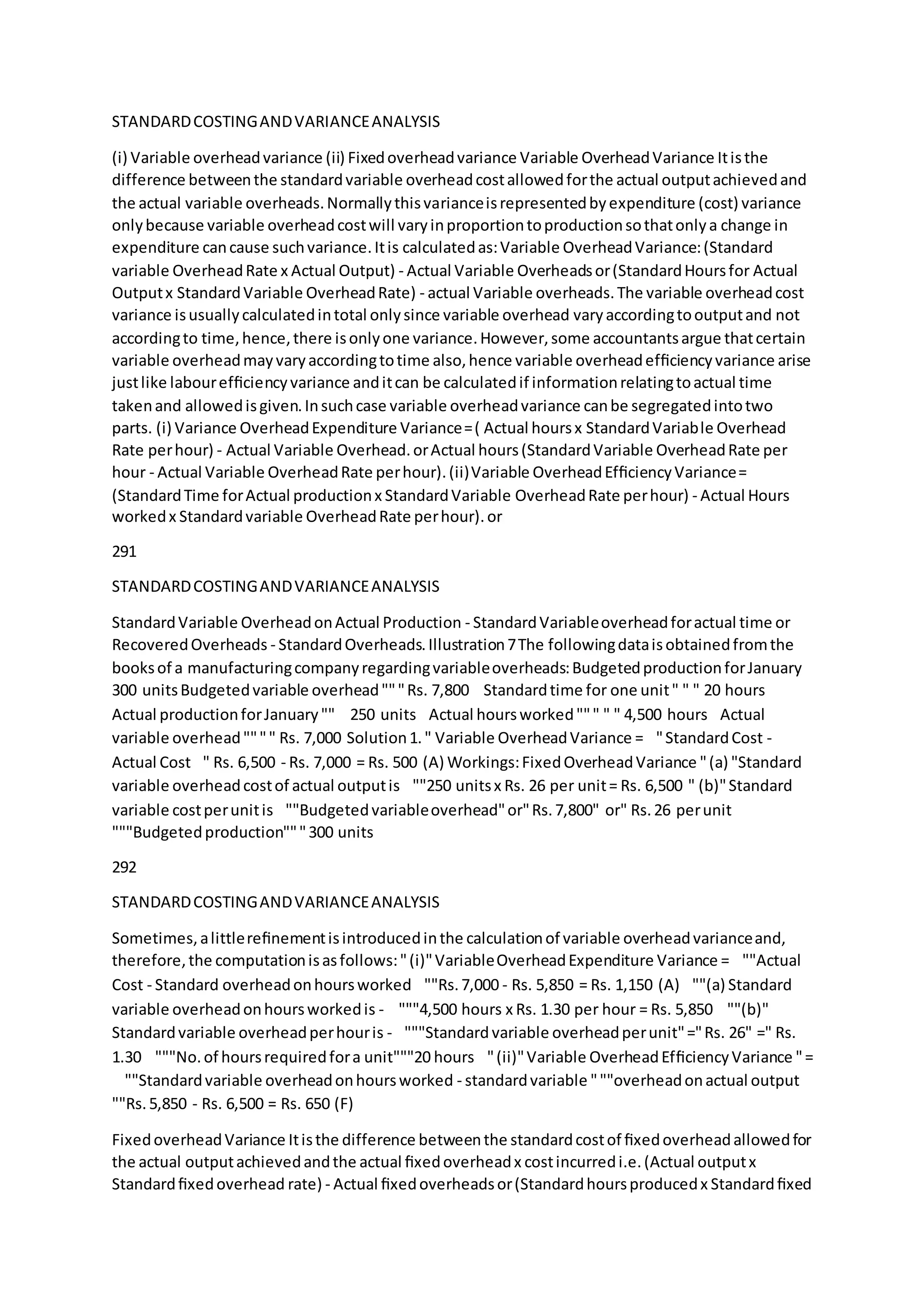

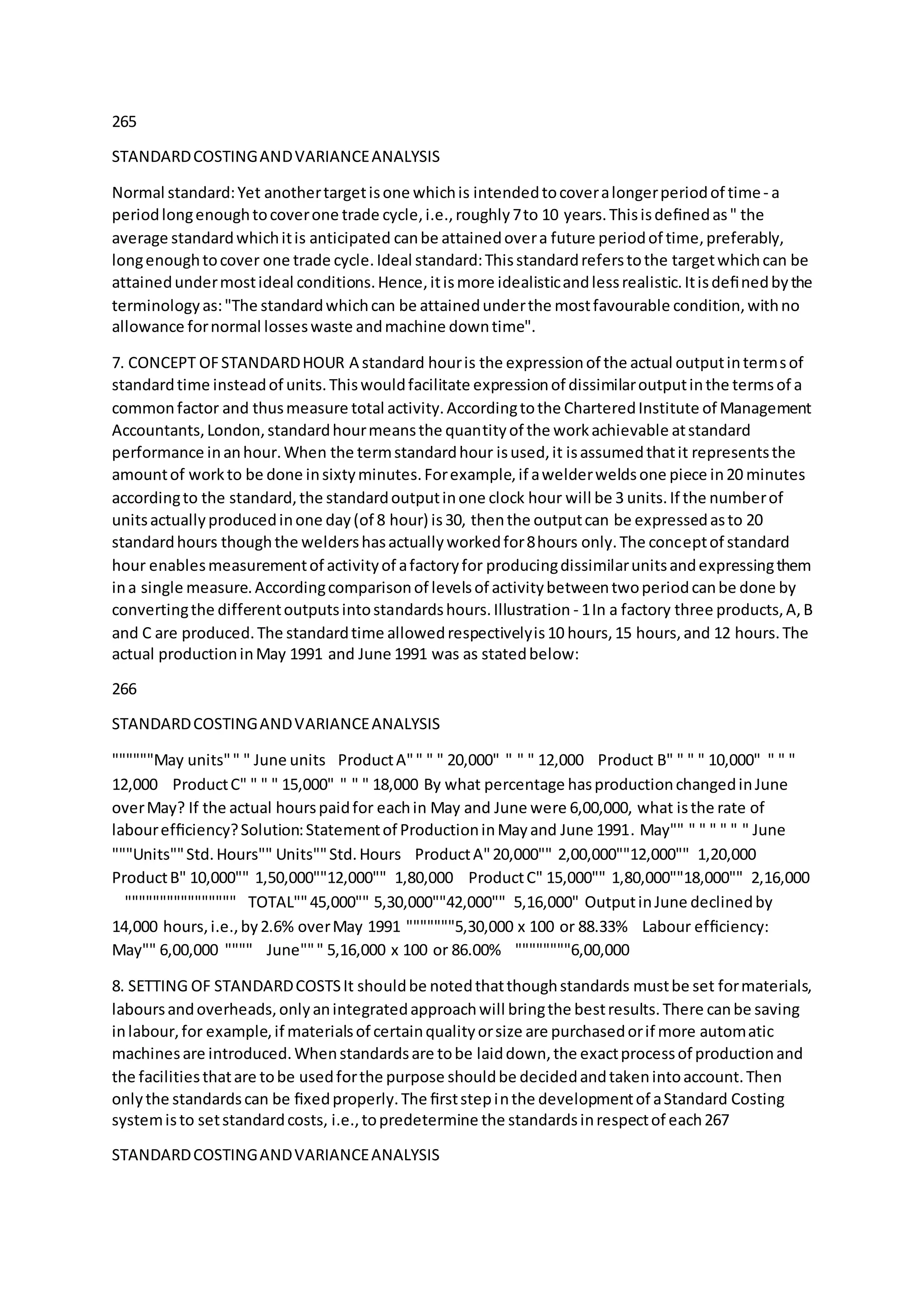

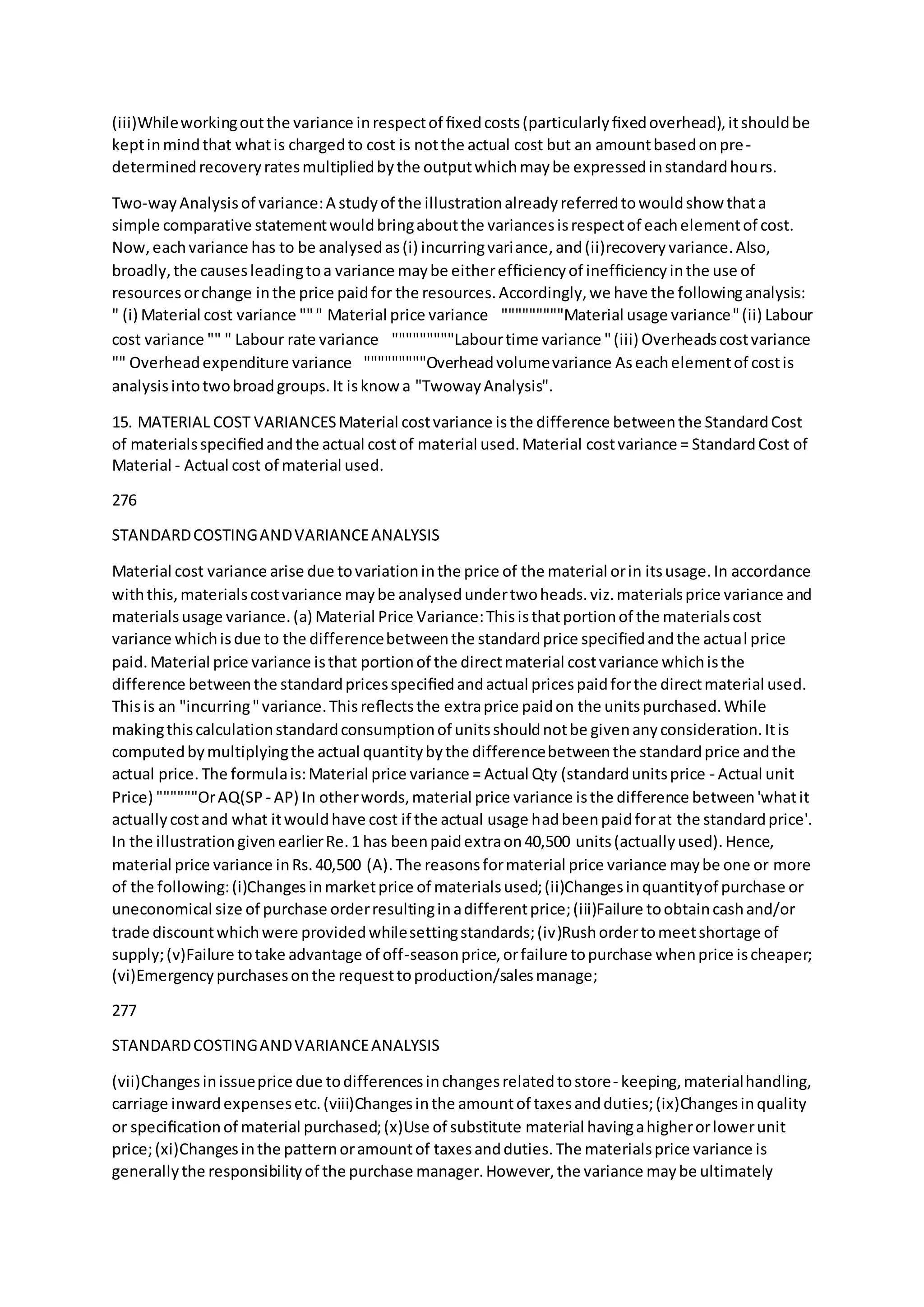

![""""Material B 5 kg.@ Rs.6"" 30.00"" 55.00 the total cost has risen;thisisthe nature of the mix

variance.Itis calculatedbycomparing(revised) standardmix atstandardpricesandthe actual mix

at standard prices.Revised""=Total of actual quantitiesx Standardquantityof anyone material

standardMix" of all material"" Total of standard quantityof all types of material See the

illustrationgivenbelow:Illustration3:Forproducingone unitof a product,the material standardis:

Material X: 6 kg.@ Rs.8 per kgand

Material Y: 4 kg.@ Rs.10 perkg In a week,1,000 unitswere

producedthe actual consumptionof materialswas:Material X:5,900 kg. @ Rs. 9 perkg and

Material Y: 4,800 kg. @ Rs. 9.50 per kg Compute the variousvariances.

280

STANDARDCOSTINGANDVARIANCEANALYSIS

Solution:Standardcostof material of 1,000 units:"""""""""""Rs.

Material X:6,000 kg.@ Rs.8 per

kg" " " 48,000

Material Y: 4,000 kg.@ Rs. 10 perkg"" " 40,000

" Total"""""""""88,000

Actual cost: " Material X: 5,900 kg. @ Rs. 9 per kg" " " 53,100

Material Y: 4,800 kg.@ Rs.9.50 per

kg"" 45,600

" Total"""""""""98,700 Total material costvariance"" " " " 10,700 (A) AnalysisMaterial

Price Variance:Actual Quantity(StandardPrice - Actual Price)

X=5900 (Rs. 8 - Rs. 9)" " " = Rs. 5,900

(A)

Y = 4800 (Rs.10 - Rs. 9.50)"" = Rs. 2,400 (F)

"""""""" Rs. 3,500 (A) Material Usage Variance:

StandardPrice (StandardQuantity - Actual Quantity)

X= Rs. 8 (6,000 - 5900)" " " = Rs. 800 (F)

Y =

Rs. 10 (4000 - 4800)"" " = Rs. 8,000 (A)

"""""""" Rs. 7,200 (A) Material Cost Variance = "" Material

price variance [Rs.3500(A)]

""[Rs.10,700(A)]""Plusmaterialusagesvariance (Rs.7,200(A)]

Material Mix Variance:

Revusedstandardmix (total actual quantity10,700 kg.)

Material X - 10,700

x 6 " " " = 6,420kg.

"""""10

281

STANDARDCOSTINGANDVARIANCEANALYSIS

" Y - 10,700 x 4 " " " = 4,280 kg.

""""10 Standardcost of revisedstandardmix:"""""""Rs."""" Rs.

X

6,420 kg.@ Rs.8"" " 51,360"

Y 4,280 kg.@ Rs. 10""42,800" " " 94,160 Standardcost of actual mix:

X 5,900 kg.@ Rs.8"" " 48,200"

Y 4,800 kg.@ Rs.10""48,000" " " 95,200

Material mix variance

(Difference)"""" 1,040(A)

The net usage variance will be Rs.7,200 lessRs.1,040 or Rs. 6,160 as provedbelow:"""""""Rs.

X

(6,420 - 6,000) x Rs. 8"" 3,360 (A)

Y(4,280 - 4,000) x Rs. 10" 2,800 (A)

"""""""6,160 (A)

(ii) Material YieldVariance:Yieldvarianceisthe differencebetweenthe standardyieldspecificand

the actual yieldobtained.Inotherwords,the difference betweenactual yieldof material in

manufacture andthe standard yield(i.e.expectedyieldfrom agivenstandardinput) valuedat

standardoutputprice is knowas material yieldvariance.Thisvariance isof greatsignificance in

processingindustries,inwhichthe outputof one processbecomesthe inputof the nextprocesstill

the finishedproductis obtainedatthe final stage.The analysisof thisvariance helpseffective

control overusage.A lowactual yieldisunfavourableyieldvariance whichindicatesthat

consumptionof materialswasmore thanthe standard.A high actual yieldindicatesefficiency,buta

constanthighyieldisa pointerforthe revisionof the standard.

282](https://image.slidesharecdn.com/standardcostingandvarianceanalysis-170924162415/75/Standard-costing-and-variance-analysis-13-2048.jpg)

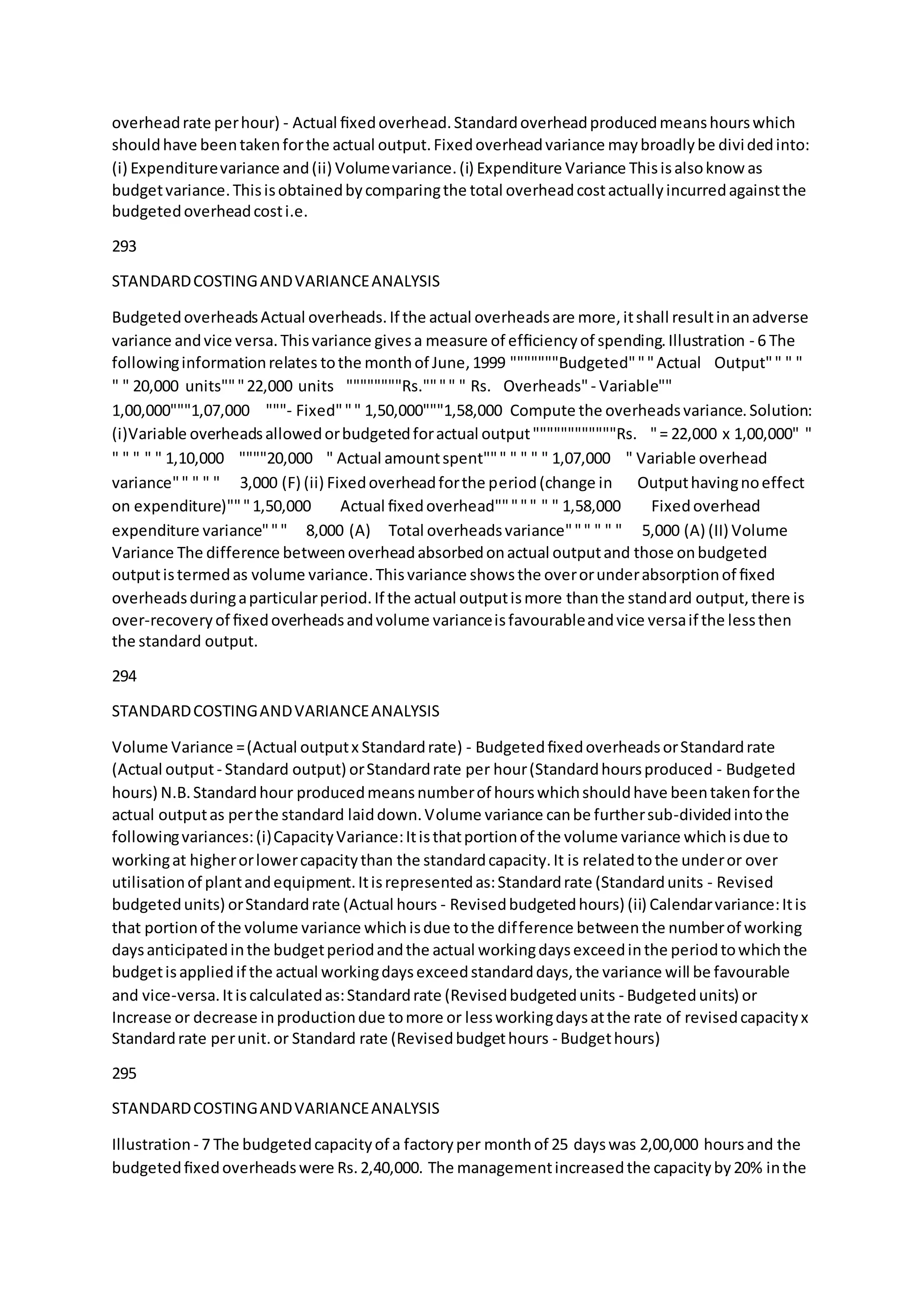

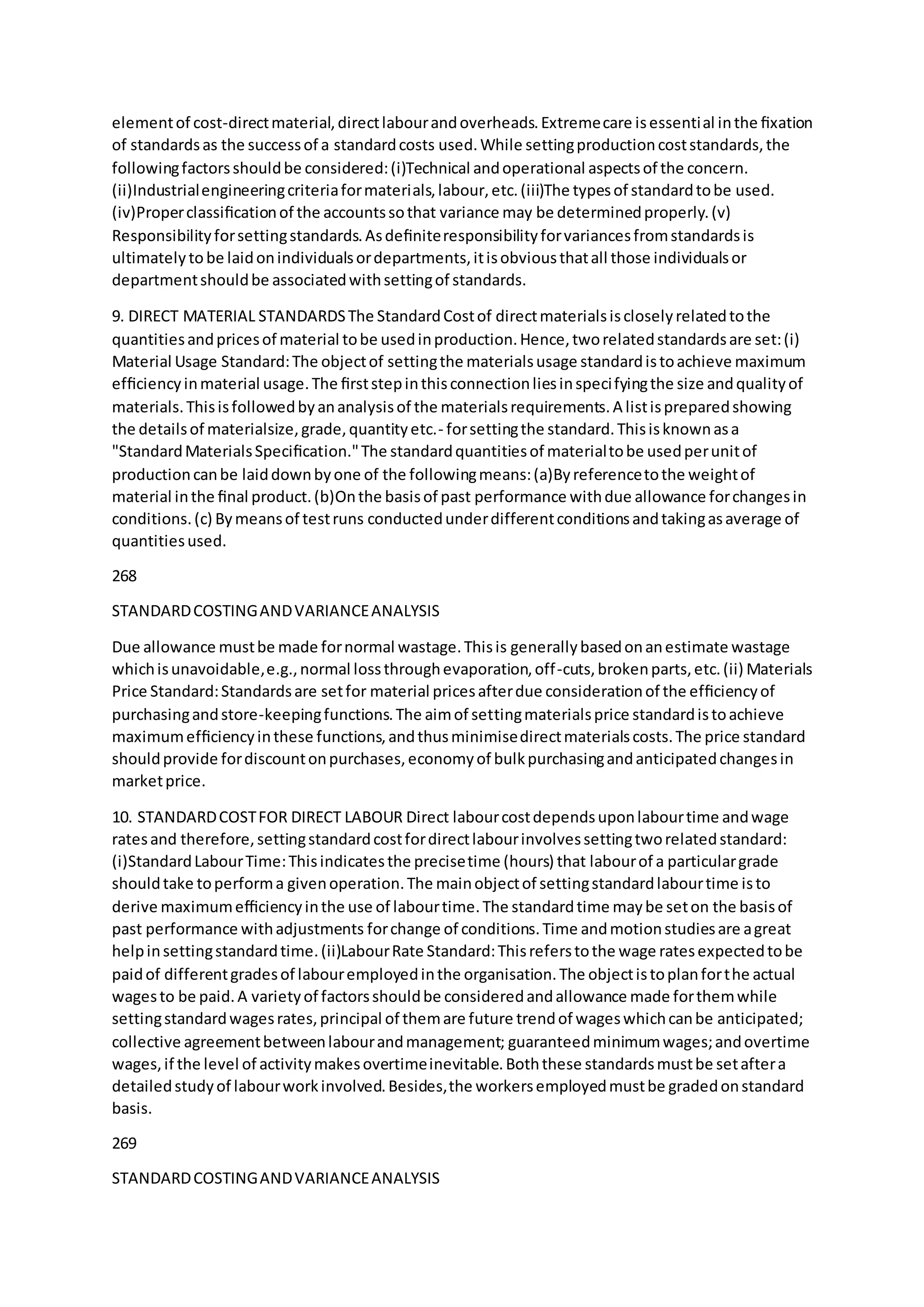

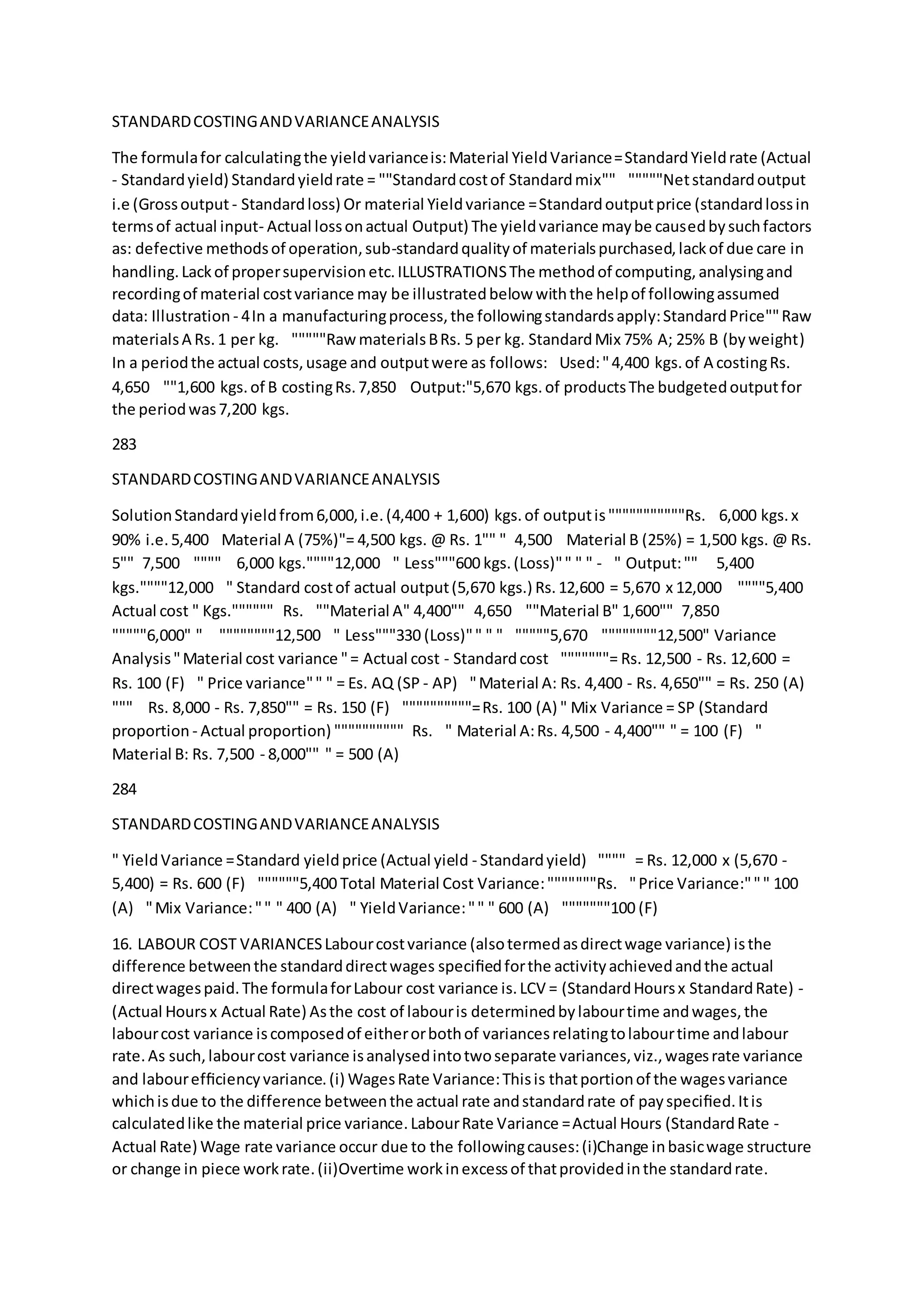

![The formulafor computinglabourmix-variance is:"(Actual hoursatstandardrate of actual gang "

Actual hoursat standardrate of standardgang.) " or " Standardrate ( Revisedstandardlabourhours

- Actual labourhours) " Revisedlabour=" Total of actual hoursx Standardhours""""""Total of

standardhours The calculationisjustlike thatof materials.Itisincludedinthe efficiencyortime

variance discussedabove.LabourYieldVariance:Thisisdue tothe difference inthe standardoutput

specifiedandthe actual outputobtained.Thisiscomputedasfollows:Labouryieldvariance =

Standardcost (Actual output - standard output) """""or(Standardlossof actual total input - Actual

loss) ´ Average standardrate perunit.If the actual outputis more than standard output,itis

favourable variance andvice versa.Illustration - 5A factory,workingfor50 hoursa week,employs

100 workersona job work.The standardrate isRe. 1 an hour and standardoutputis 200 unitsper

gang hour.Duringa weekinJune,tenemployeeswerepaidat80 p. an hourand five at Re. 1.20 an

hour.Rest of the employeeswere paidatthe standardrate.Actual numberof unitsproducedwas

10,200 Calculate labourcostvariances.

288

STANDARDCOSTINGANDVARIANCEANALYSIS

Solution:(i) Costvariance "standardCost - Actual Cost " Rs. 5,100 - Rs. 4,950 = Rs. 150 (F) Workings

(ii) Rate variance:"(a) Calculationof Actual Cost:""""""Rs.""15 workersfor50 hours @ Re. 1 per

hour""="" 4,250

""10 workersfor50 hours@ 80 p. perhour "" =" " 400

""5 workersfor50

hours@ Rs.1.20 perhour" ="" 300

""""""""Total Actual Cost""" " 4,950 " (b) Calculationof

StandardRate:

""Standardcost (pergang hour)

""StandardProduction(perganghour)

"""100 x

Re.1

""=" 200 units"""Rs.100"= 50 per units

""="200 units" (c) Calculationof StandardCost:

""Actual productionx Standardrate

""10,200 unitsx 50 p.per unit= Rs. 5,100 Asthe actual wage

rate hasdeviatedfromthe standardinrespectof only15 workerfromout of a total of 100 workers,

wagesrate variance wouldbe calculatedonlyinrespectof these 15 workers.(iii)EfficiencyVariance:

" Actual Hours (standardrate - Actual Rate) " Therefore,

"500 Hours (Re.1 - 80 p.)""= Rs.100(F)

"

250 Hours(Re.1 - Rs. 1.20)" = Rs. 50(A)

" thus,the total rate variance isRs. 50 (F)

289

STANDARDCOSTINGANDVARIANCEANALYSIS

efficiencyvariance isindicatedbythe factthat,as comparedwithstandardproductionof 10,000

units(200 units´ 50 hours),the actual productionis10,200 unitsStandard Rate ( StandardHours -

Actual Hours) Re. 1 (5,100) = Rs.100 favourable.Calculationof StandardHours:""Actual

production""""x " No.of workers

""Standardproductionperhour""10,200 units" x " 100 = 5,100

hours

""200 units(iv) YieldVariance:"StandardLabour cost perunitof output(SY-AY)

"0.50

(10,000_10,200) = Rs. 100 (F) " verification:"CostVariance + EfficiencyVariance

"Rs.150 (F) = 50

(F) + Rs.100 (F)

17. OVERHEADCOST VARIANCESThe total overheadcostvariance is the difference betweenthe

StandardCost of overheadallowedforthe actual outputachievedandthe actual overheadcost

incurred.Inotherwords,overheadcostvariance isthe underor overabsorptionof overheads.

Overheadcostvariance iscalculatedas follows:[Actual outputx Standardoverheadrate perunit] -

Actual overheadcost"""""or[Standardhoursfor actual outputx Standard overheadrate perhour] -

Actual overheadcostOverheadcostvariancescanbe classifiedas:

290](https://image.slidesharecdn.com/standardcostingandvarianceanalysis-170924162415/75/Standard-costing-and-variance-analysis-16-2048.jpg)