Downloaded 41 times

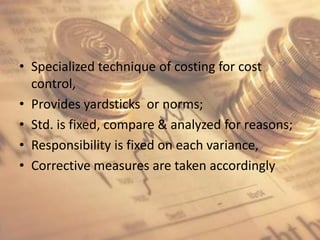

Standard costing is a specialized costing technique used for cost control that establishes predetermined costs known as standards that are used as benchmarks to measure performance and control costs. Variances between actual and standard costs are analyzed to identify reasons for differences and assign responsibility so corrective measures can be taken. Standard costing is useful for decision making, production planning, policy formulation, and proper budgeting as it provides feedback on performance.