Download to read offline

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

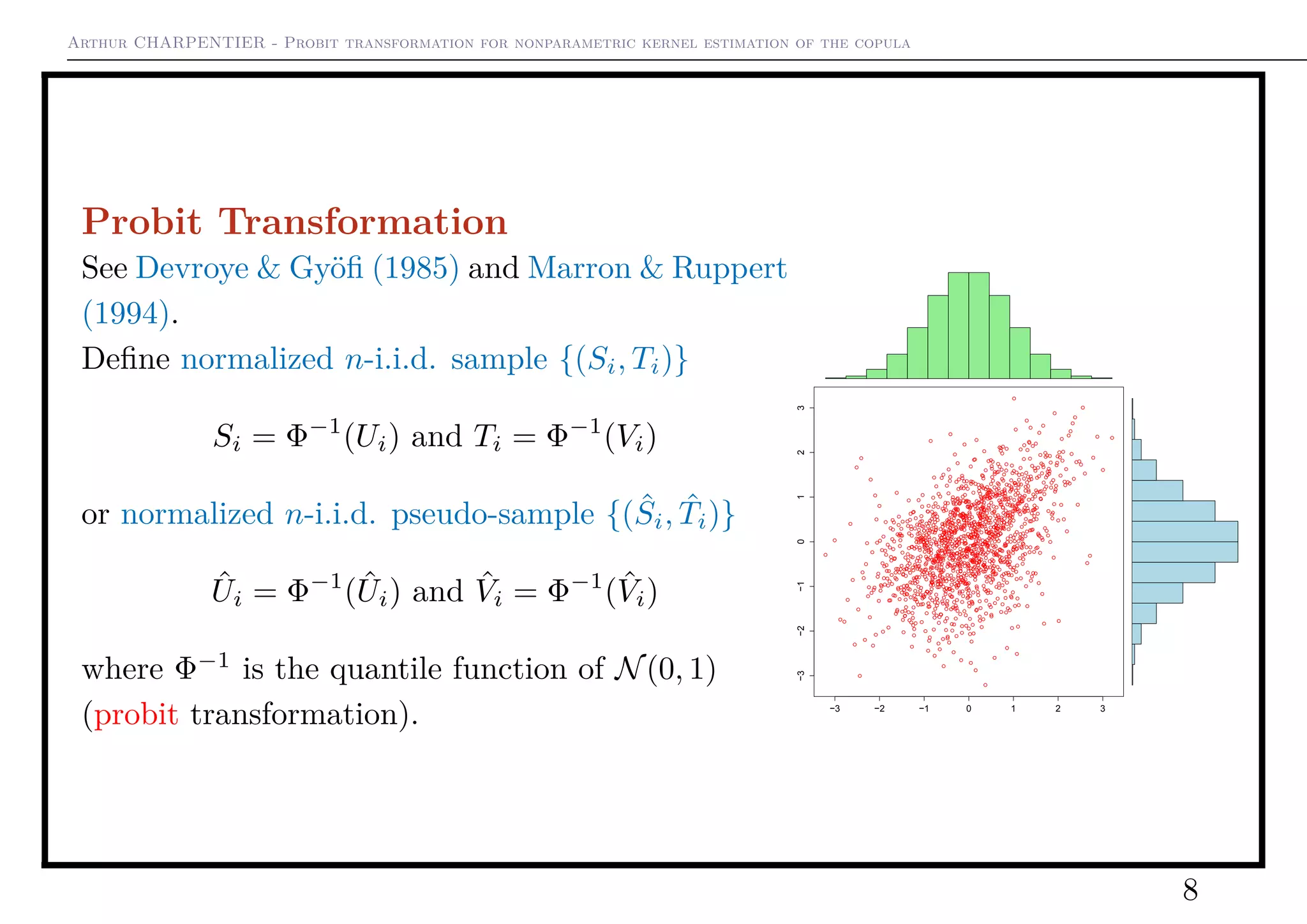

Motivation

Consider some n-i.i.d. sample {(Xi, Yi)} with cu-

mulative distribution function FXY and joint den-

sity fXY . Let FX and FY denote the marginal

distributions, and C the copula,

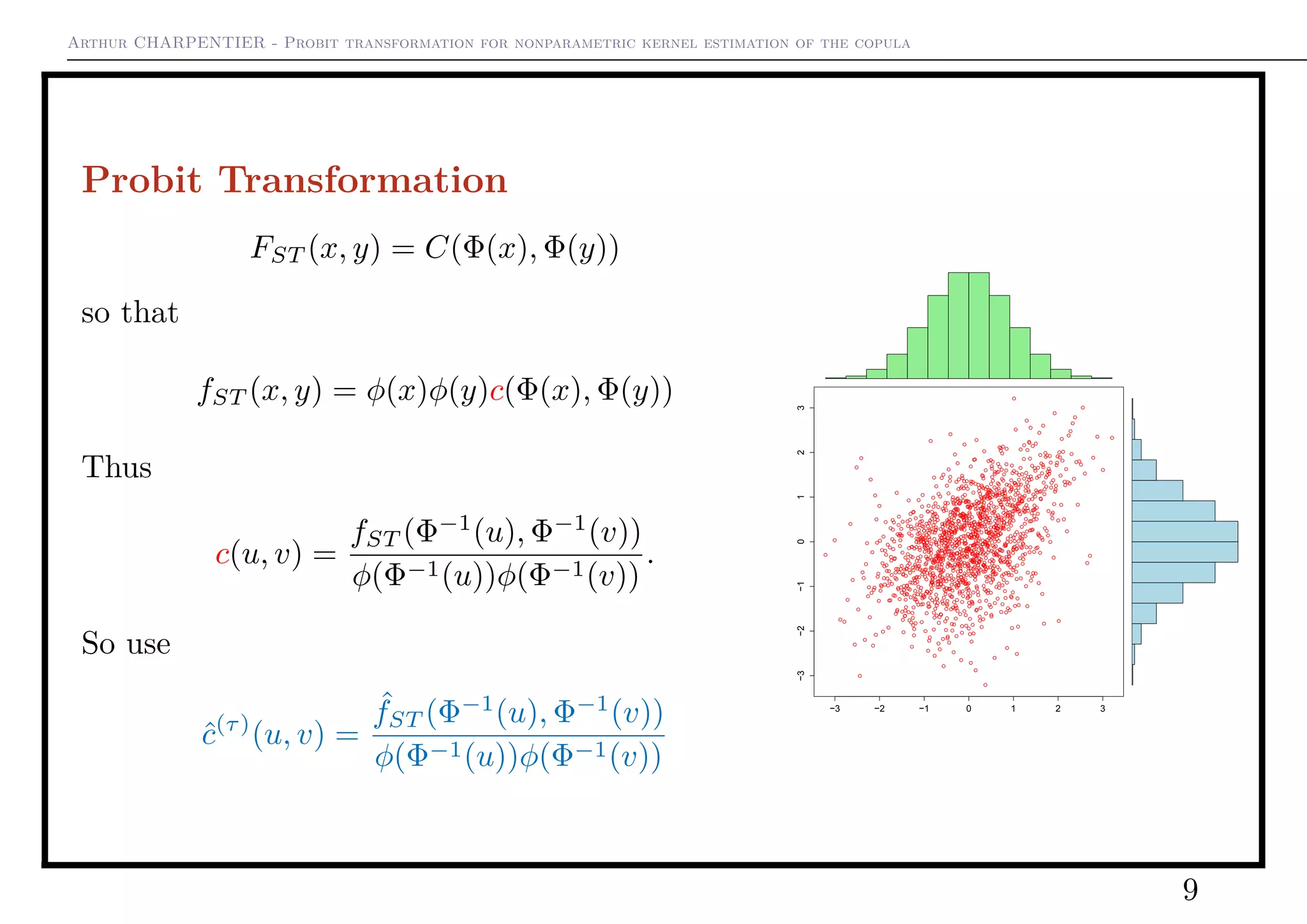

FXY (x, y) = C(FX(x), FY (y))

so that

fXY (x, y) = fX(x)fY (y)c(FX(x), FY (y))

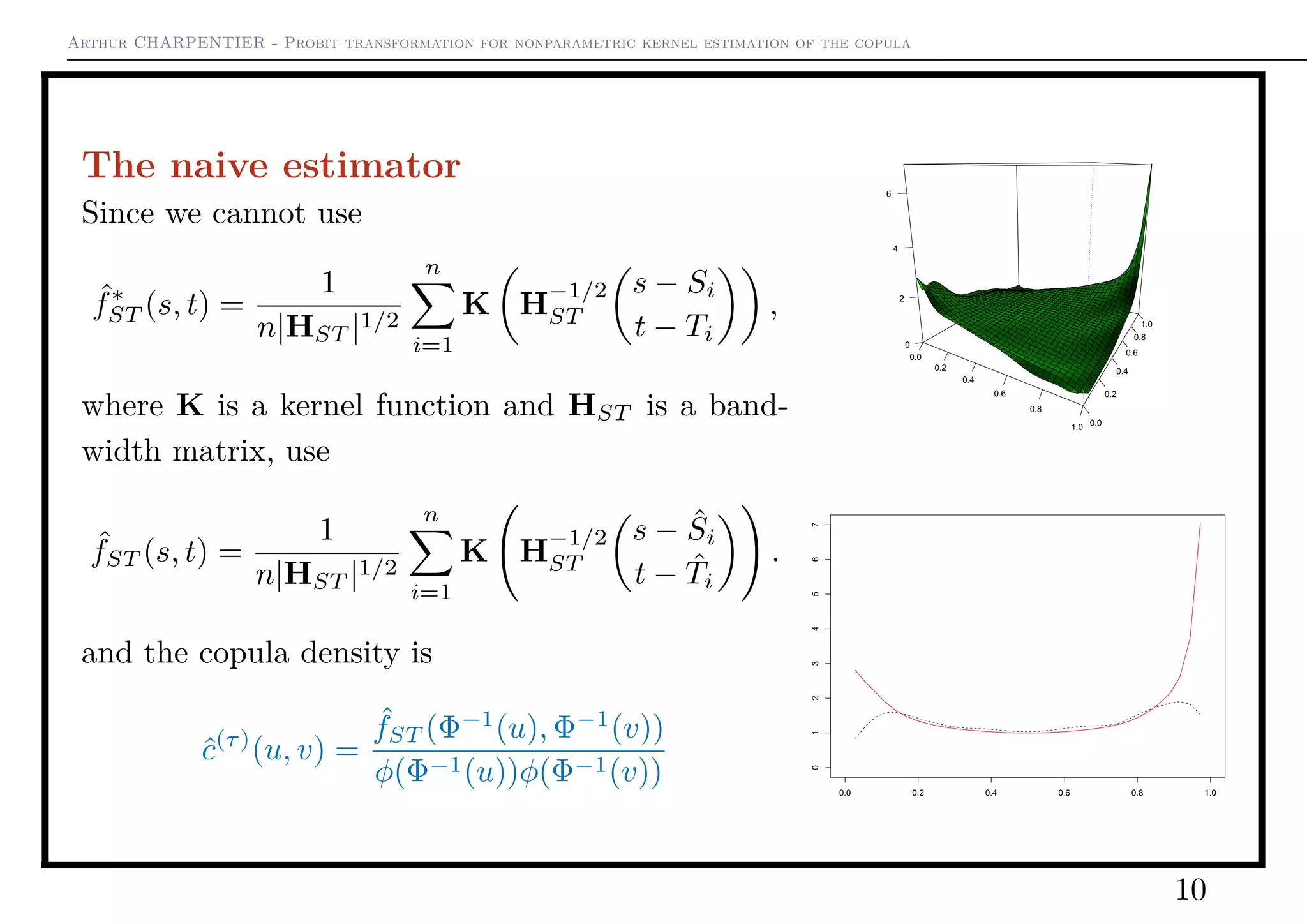

We want a nonparametric estimate of c on [0, 1]2

. 1e+01 1e+03 1e+05

1e+011e+021e+031e+041e+05

2](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-2-2048.jpg)

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

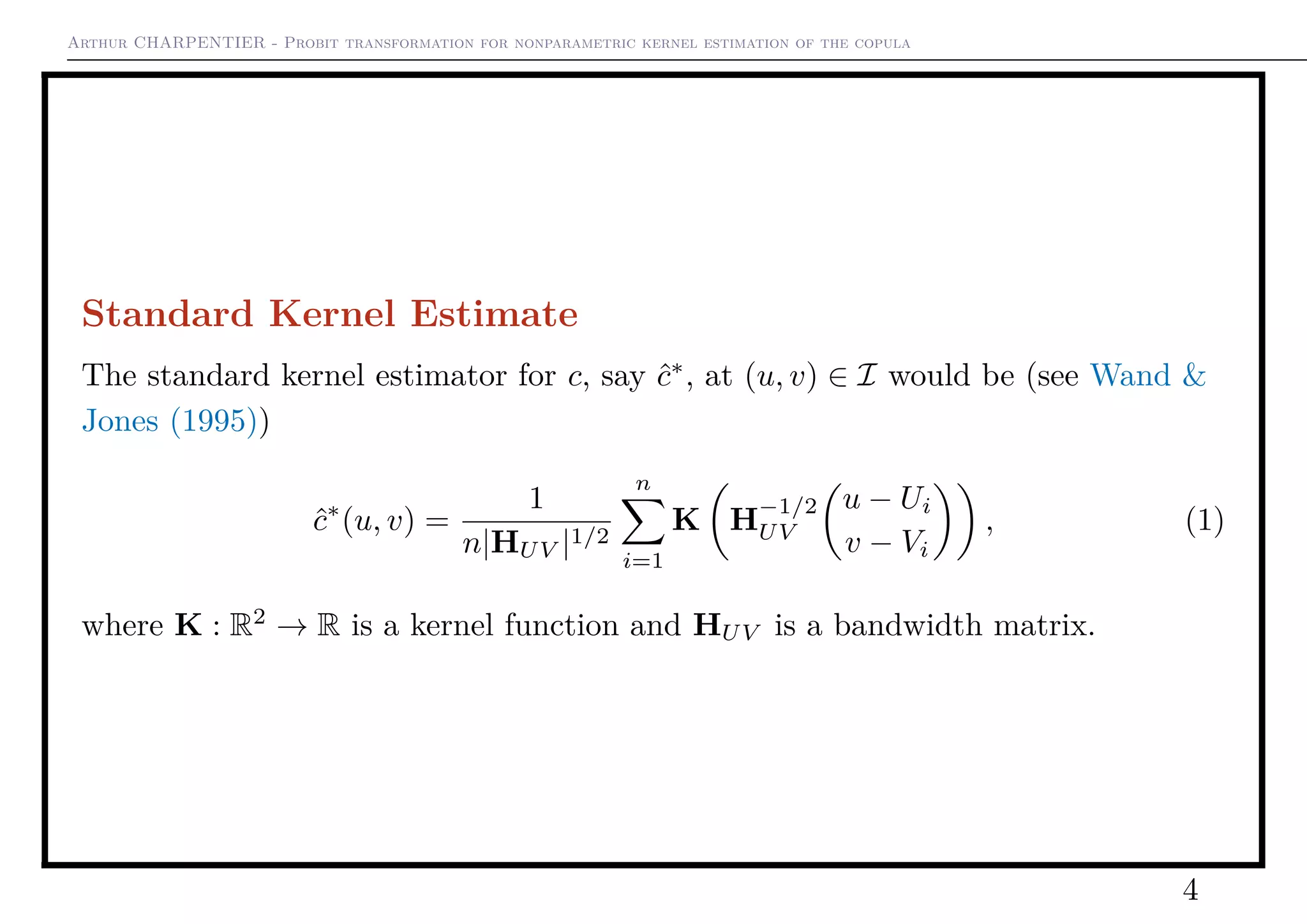

Standard Kernel Estimate

However, this estimator is not consistent along

boundaries of [0, 1]2

E(ˆc∗

(u, v)) =

1

4

c(u, v) + O(h) at corners

E(ˆc∗

(u, v)) =

1

2

c(u, v) + O(h) on the borders

if K is symmetric and HUV symmetric.

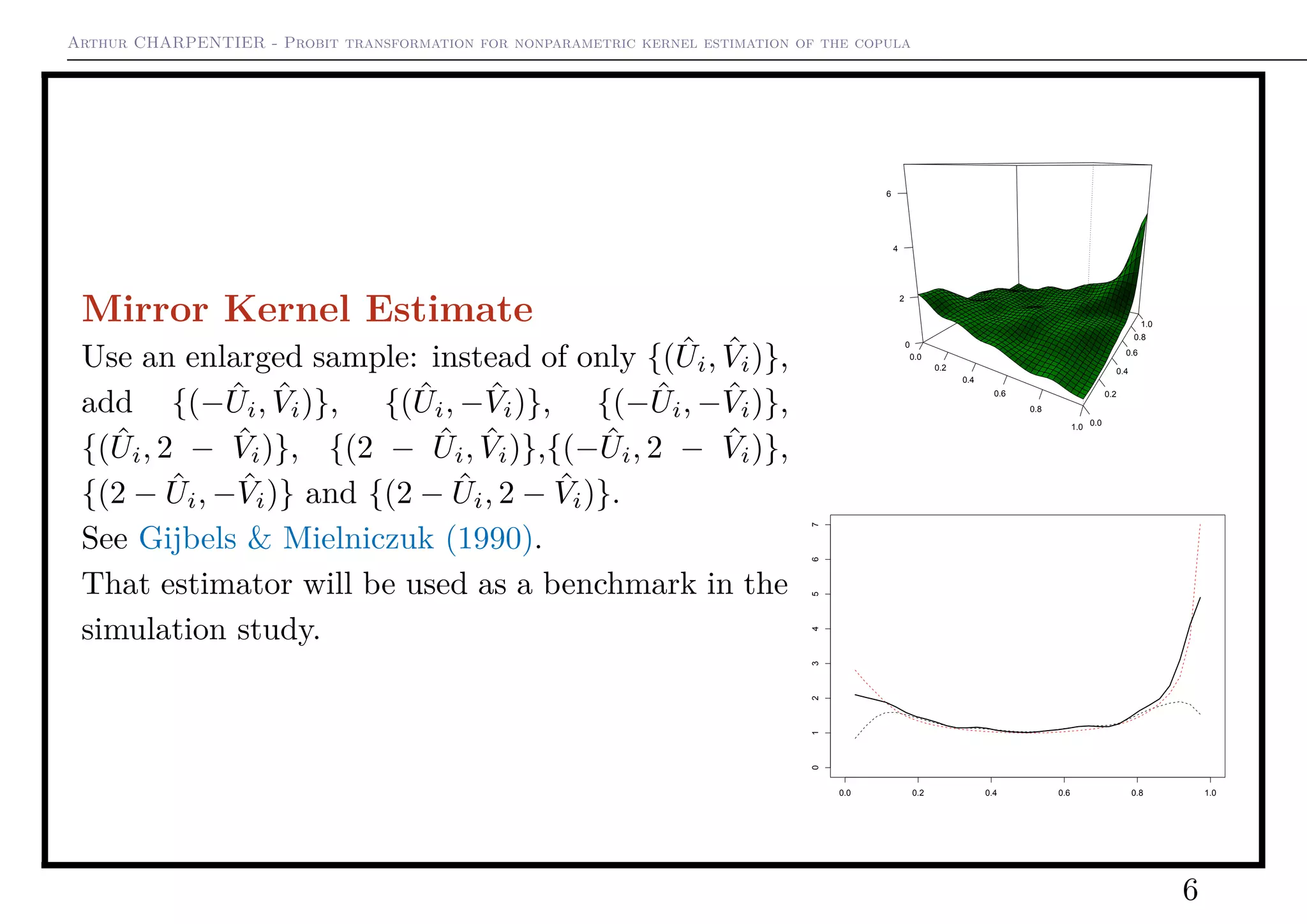

Corrections have been proposed, e.g. mirror reflec-

tion Gijbels (1990) or the usage of boundary kernels

Chen (2007), but with mixed results.

Remark: the graph on the bottom is ˆc∗

on the

(first) diagonal.

0.0

0.2

0.4

0.6

0.8

1.0 0.0

0.2

0.4

0.6

0.8

1.0

0

2

4

6

0.0 0.2 0.4 0.6 0.8 1.0

01234567

5](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-5-2048.jpg)

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

Using Beta Kernels

Use a Kernel which is a product of beta kernels

Kxi

(u)) ∝ u

x1,i

b

1 [1 − u1]

x1,i

b · u

x2,i

b

2 [1 − u2]

x2,i

b

See Chen (1999).

0.0

0.2

0.4

0.6

0.8

1.0 0.0

0.2

0.4

0.6

0.8

1.0

0

2

4

6

0.0 0.2 0.4 0.6 0.8 1.0

01234567

7](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-7-2048.jpg)

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

Asymptotic properties

A2. The copula C of FXY is such that (∂C/∂u)(u, v) and (∂2

C/∂u2

)(u, v) exist

and are continuous on {(u, v) : u ∈ (0, 1), v ∈ [0, 1]}, and (∂C/∂v)(u, v) and

(∂2

C/∂v2

)(u, v) exist and are continuous on {(u, v) : u ∈ [0, 1], v ∈ (0, 1)}. In

addition, there are constants K1 and K2 such that

∂2

C

∂u2

(u, v) ≤

K1

u(1 − u)

for (u, v) ∈ (0, 1) × [0, 1];

∂2

C

∂v2

(u, v) ≤

K2

v(1 − v)

for (u, v) ∈ [0, 1] × (0, 1);

A3. The density c of C exists, is positive and admits continuous second-order

partial derivatives on the interior of the unit square I. In addition, there is a

constant K00 such that

c(u, v) ≤ K00 min

1

u(1 − u)

,

1

v(1 − v)

∀(u, v) ∈ (0, 1)2

.

see Segers (2012).

17](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-17-2048.jpg)

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

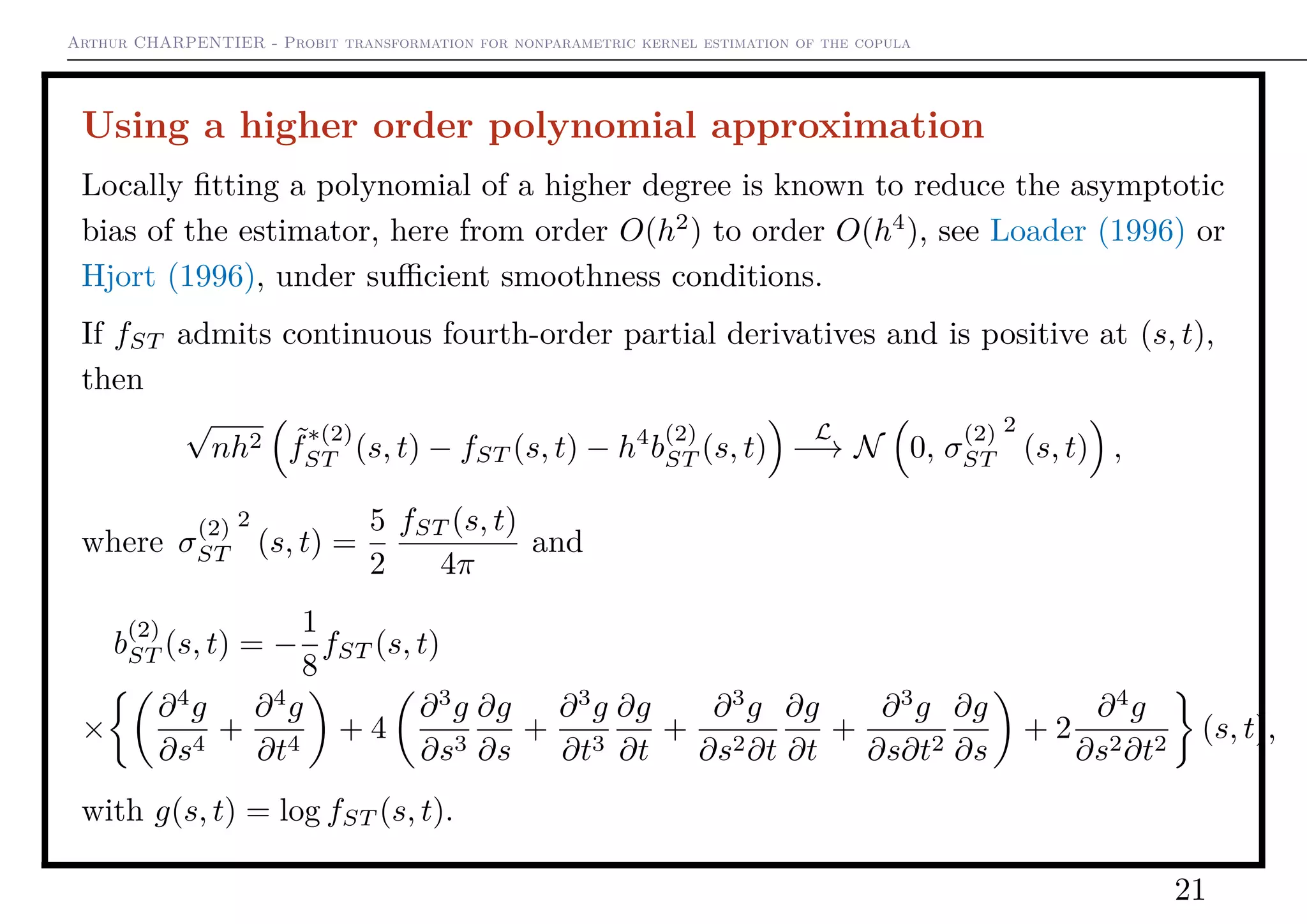

Using a higher order polynomial approximation

A4. The copula density c(u, v) = (∂2

C/∂u∂v)(u, v) admits continuous

fourth-order partial derivatives on the interior of the unit square [0, 1]2

.

Then

√

nh2 ˜c∗(τ,2)

(u, v) − c(u, v) − h4 b(2)

(u, v)

φ(Φ−1(u))φ(Φ−1(v))

L

−→ N 0, σ(2) 2

(u, v)

where σ(2) 2

(u, v) =

5

2

c(u, v)

4πφ(Φ−1(u))φ(Φ−1(v))

22](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-22-2048.jpg)

![Arthur CHARPENTIER - Probit transformation for nonparametric kernel estimation of the copula

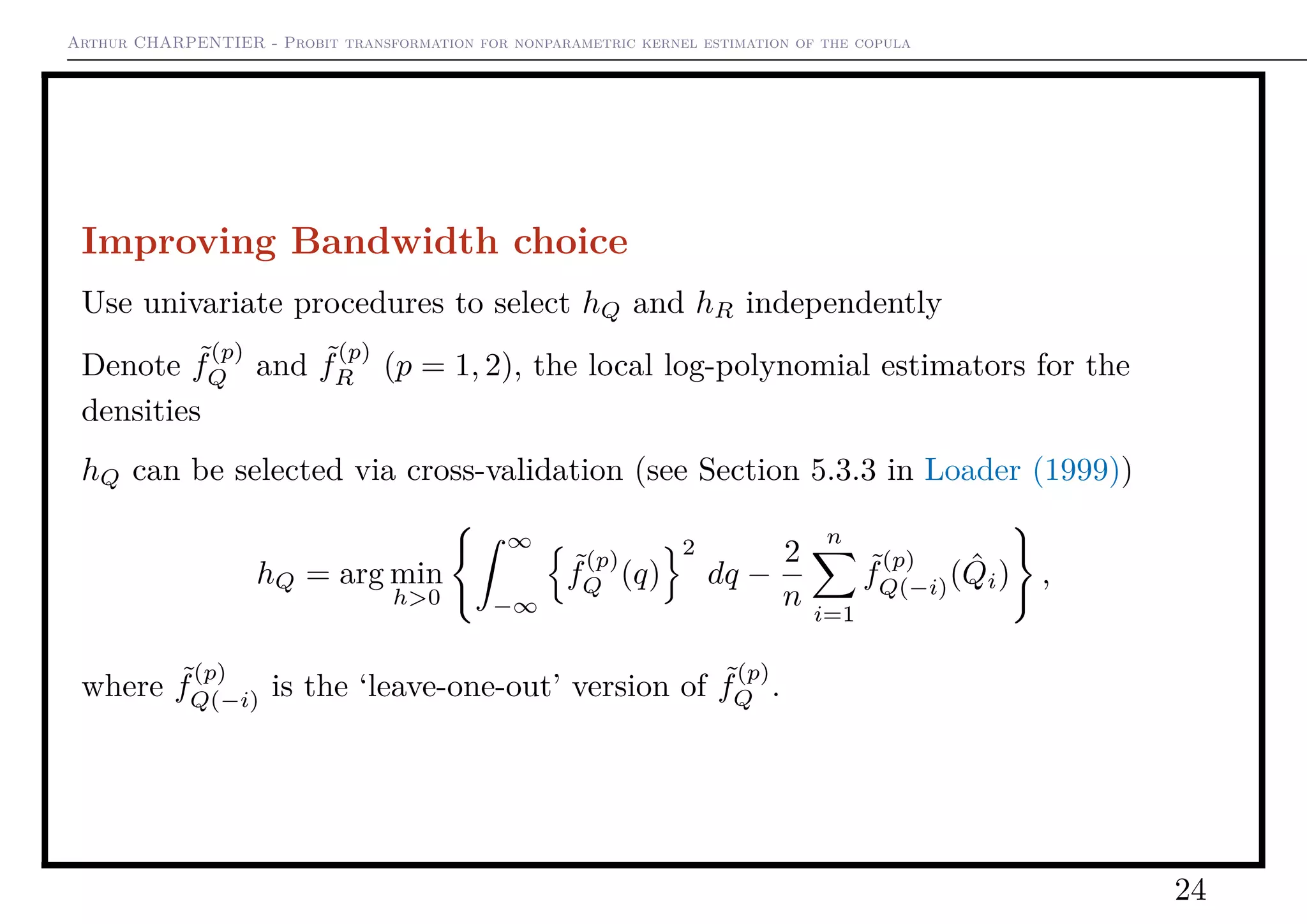

Improving Bandwidth choice

Consider the principal components decomposition of the (n × 2) matrix

[ˆS, ˆT ] = M.

Let W1 = (W11, W12)T

and W2 = (W21, W22)T

be the eigenvectors of MT

M. Set

Q

R

=

W11 W12

W21 W22

S

T

= W

S

T

which is only a linear reparametrization of R2

, so

an estimate of fST can be readily obtained from an

estimate of the density of (Q, R)

Since { ˆQi} and { ˆRi} are empirically uncorrelated,

consider a diagonal bandwidth matrix HQR =

diag(h2

Q, h2

R).

−4 −2 0 2 4

−3−2−1012

23](https://image.slidesharecdn.com/slides-cirm-2016-light-160208151543/75/slides-CIRM-copulas-extremes-and-actuarial-science-23-2048.jpg)

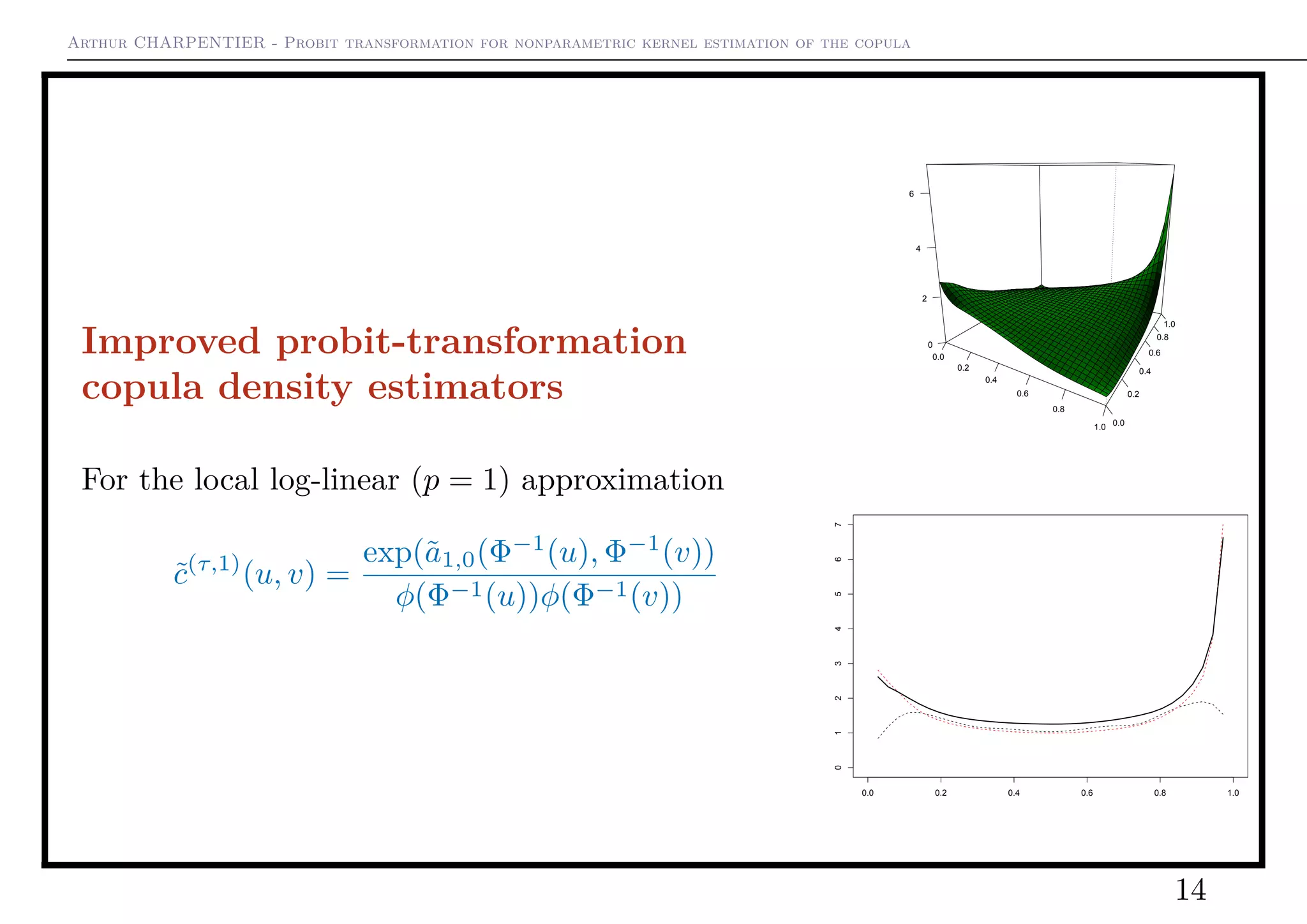

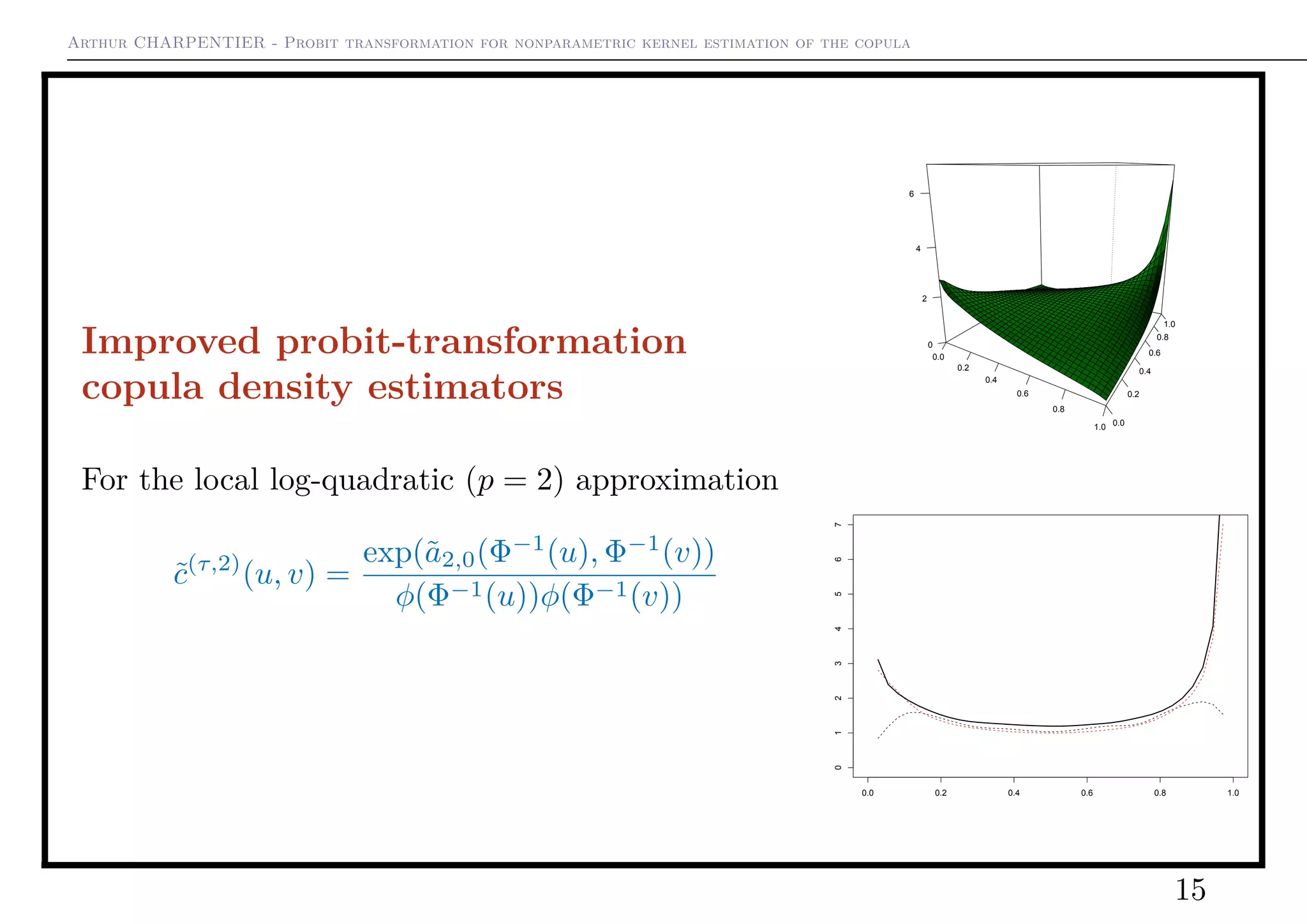

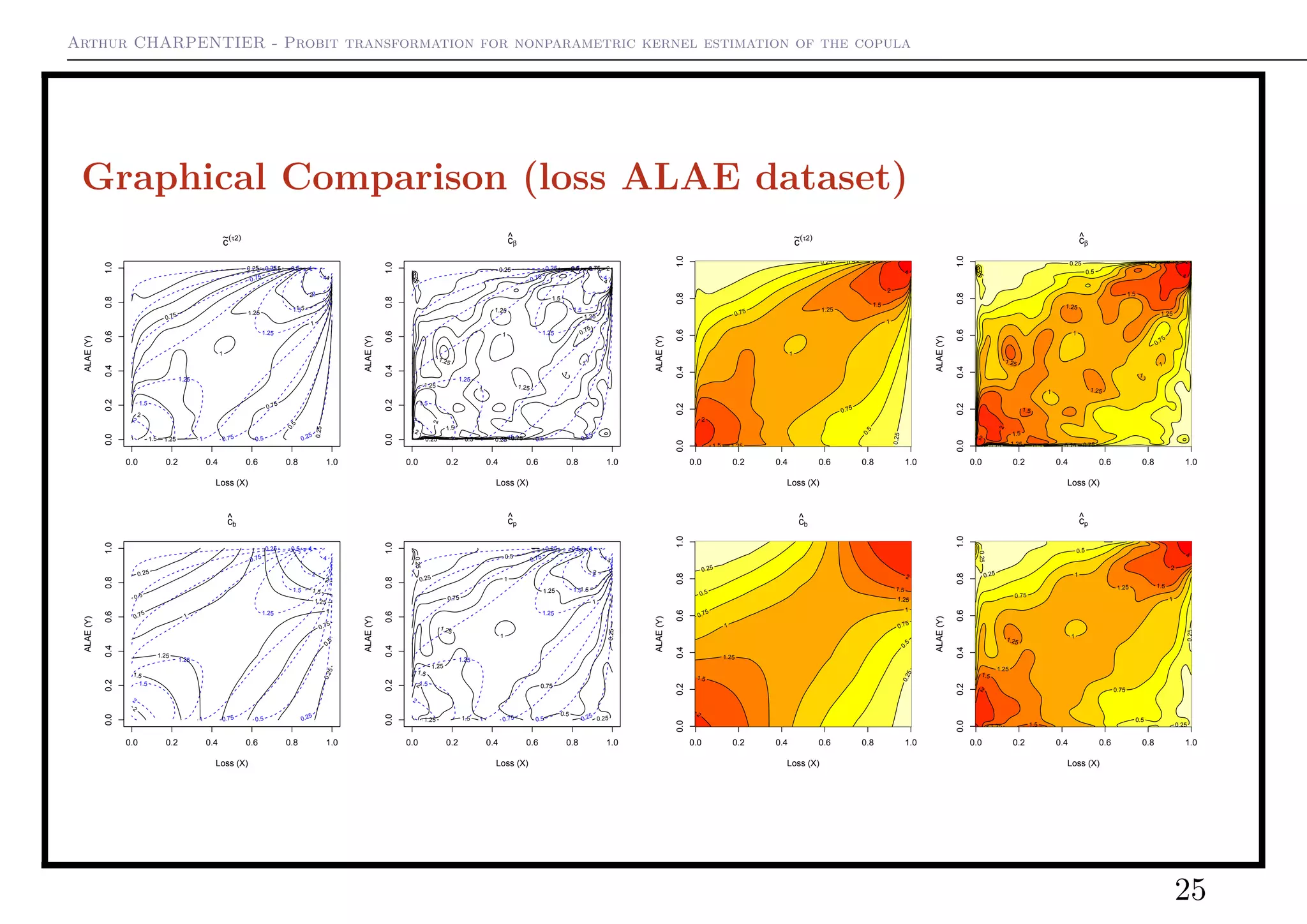

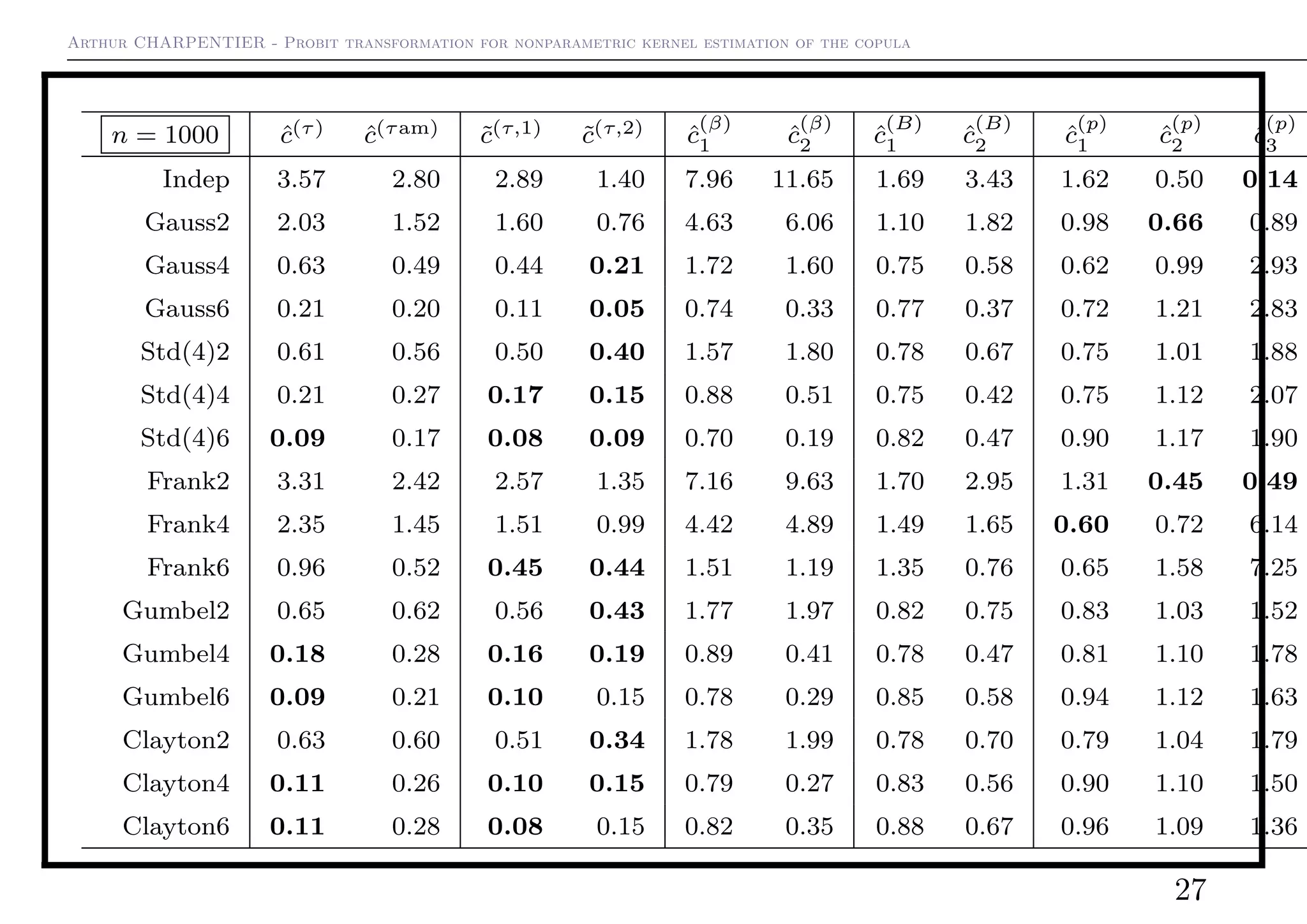

1) The document discusses probit transformation for nonparametric kernel estimation of copulas. It introduces a standard kernel estimator for copulas that is inconsistent on boundaries. 2) It then presents a "naive" probit transformation kernel copula density estimator that transforms data to standard normal using the probit function to address boundary issues. 3) It further improves upon this by introducing local log-linear and log-quadratic approximations for the transformed density, yielding two new estimators with better asymptotic properties.

![[DSC Europe 25] Dragana Ilic - AI for Big Data in Astronomy.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/8palya86qaatvjhva1ms-2-dragana-ilic-ai-ilic-251208151906-652b819c-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Marija Vlajkovic & Andrea Radonjanin - Integration of AI tool...](https://cdn.slidesharecdn.com/ss_thumbnails/qf1jrglttoc3bm8s3aop-final-integration-of-ai-tools-251208151905-394f3a6a-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Andy Cotgreave - Nothing is new in analytics.pptx](https://cdn.slidesharecdn.com/ss_thumbnails/mba4vzcurvoh5lfrd5zw-6-251205194645-341bbbbe-thumbnail.jpg?width=640&height=640&fit=bounds)

![[DSC Europe 25] Vid Stimac - Policy Parsimony: Between Oversimplifying and Ov...](https://cdn.slidesharecdn.com/ss_thumbnails/eqlepagzqp2rhg3gbluh-dsc-stimac-251120-251205090438-059e7f54-thumbnail.jpg?width=640&height=640&fit=bounds)