Downloaded 62 times

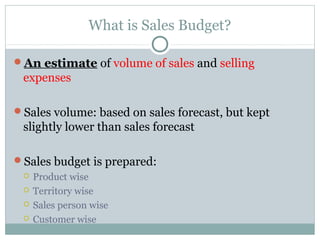

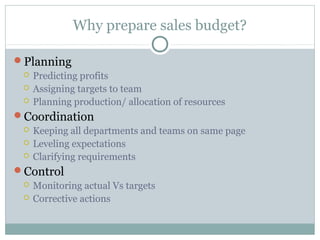

This document discusses key concepts related to sales budgets, quotas, territories, and control. It defines a sales budget as an estimate of sales volume and expenses set slightly lower than forecasts. Sales budgets are prepared by product, territory, salesperson, and customer. Quotas and territories are used to set performance standards, control results, and motivate teams. Territories assign exclusive areas to sales teams to reduce conflict and efficiently allocate resources. Control processes compare actual performance to targets and analyze expenses to ensure budget and objective achievement.