Downloaded 211 times

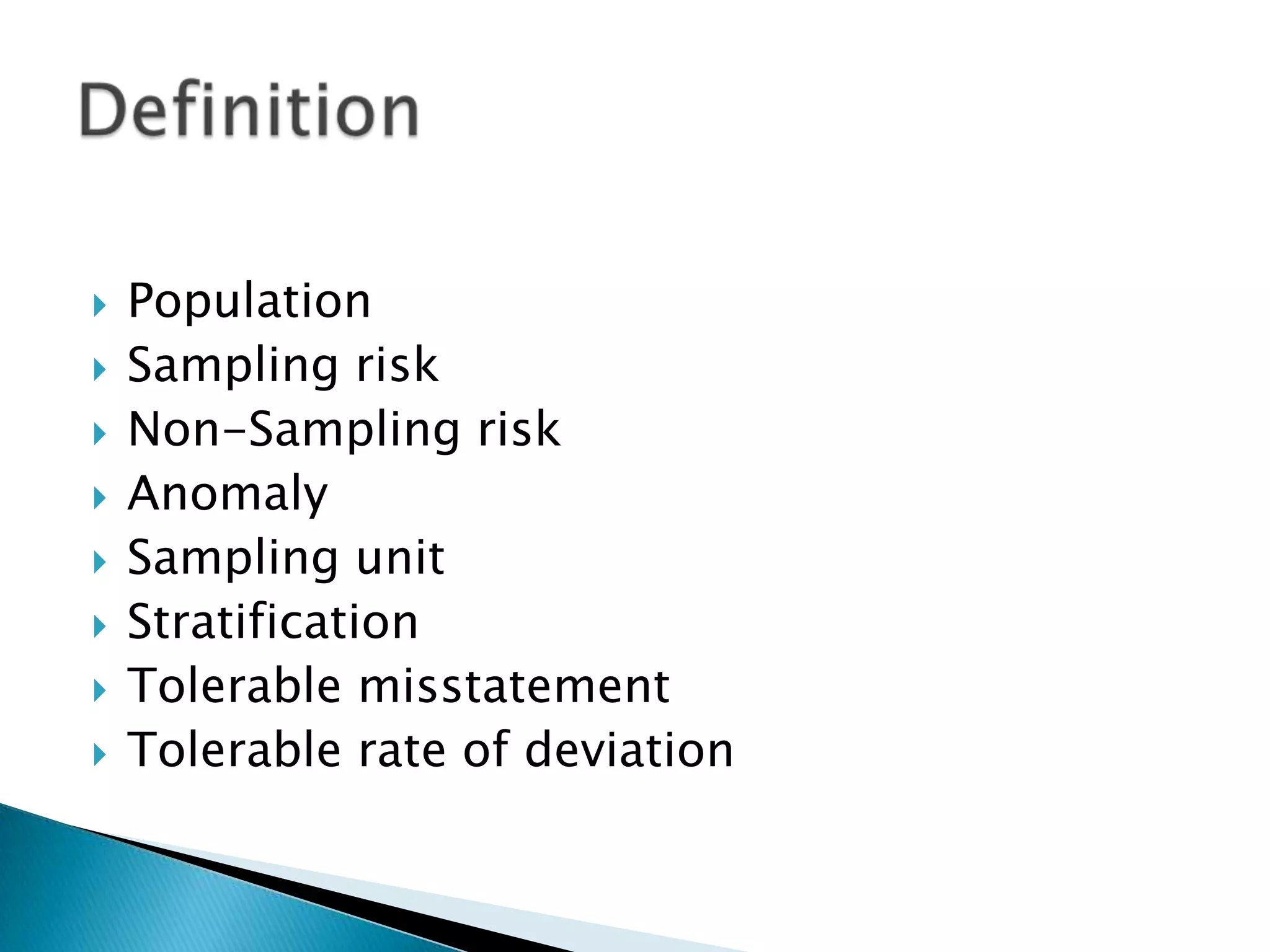

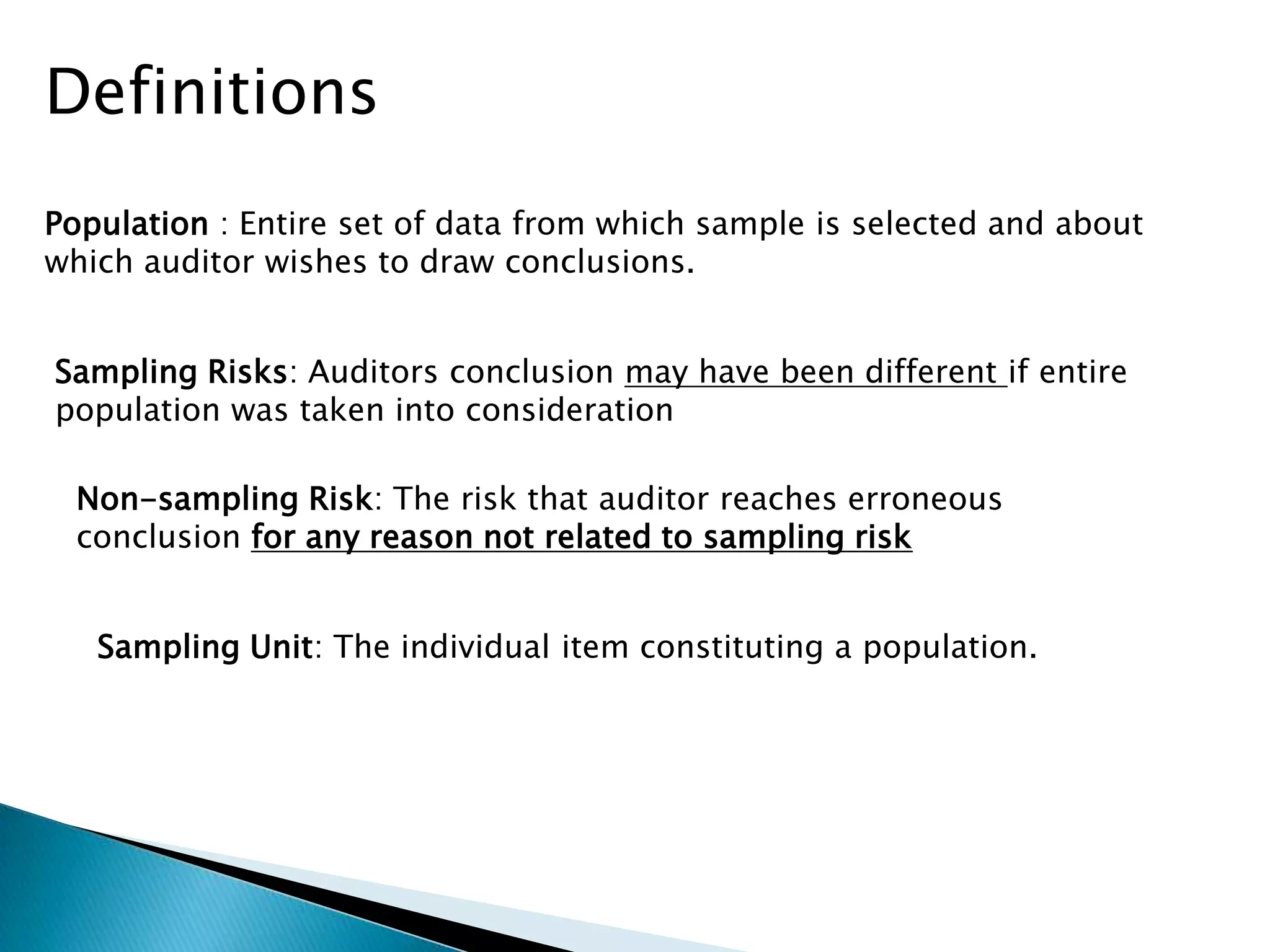

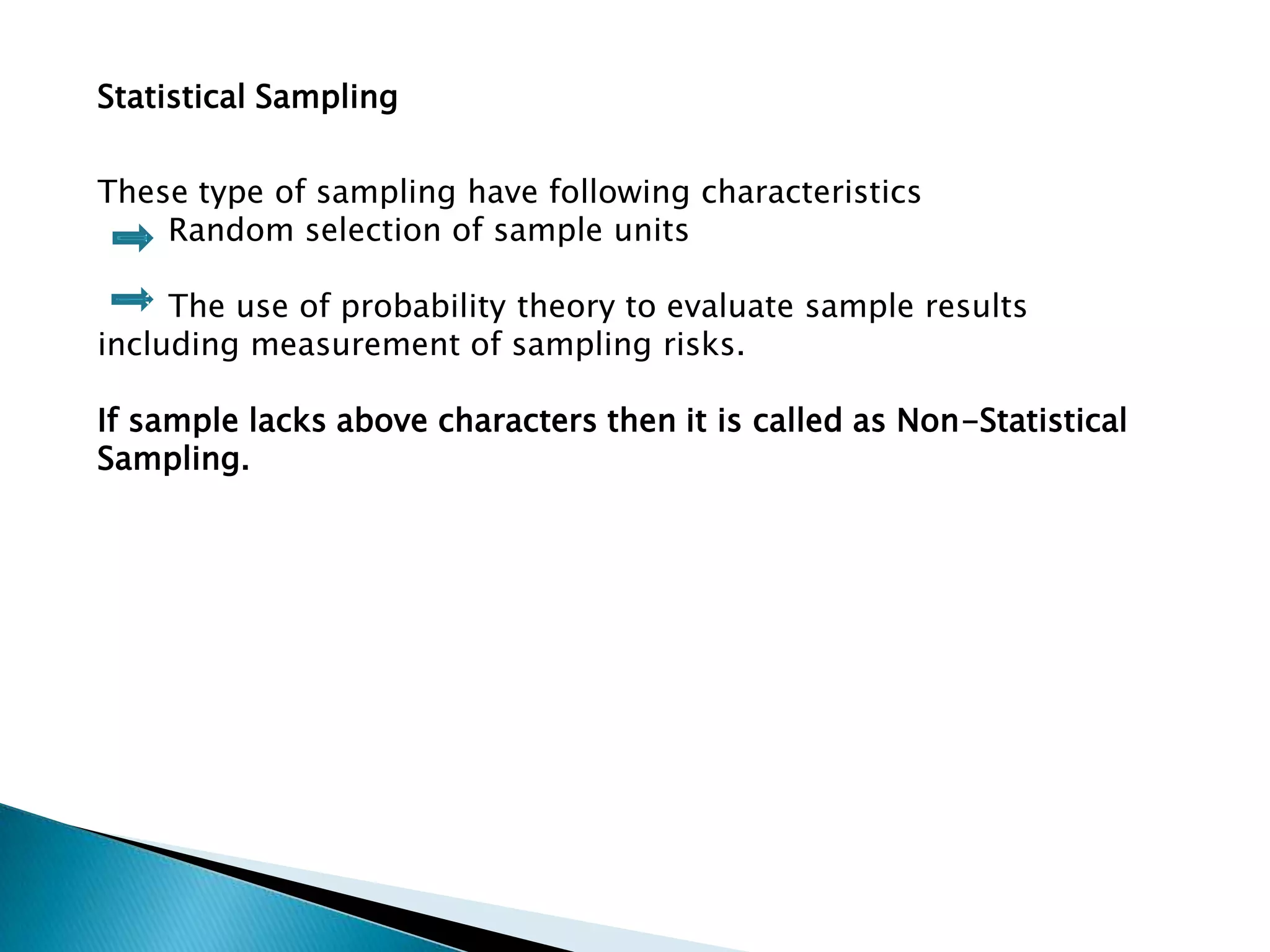

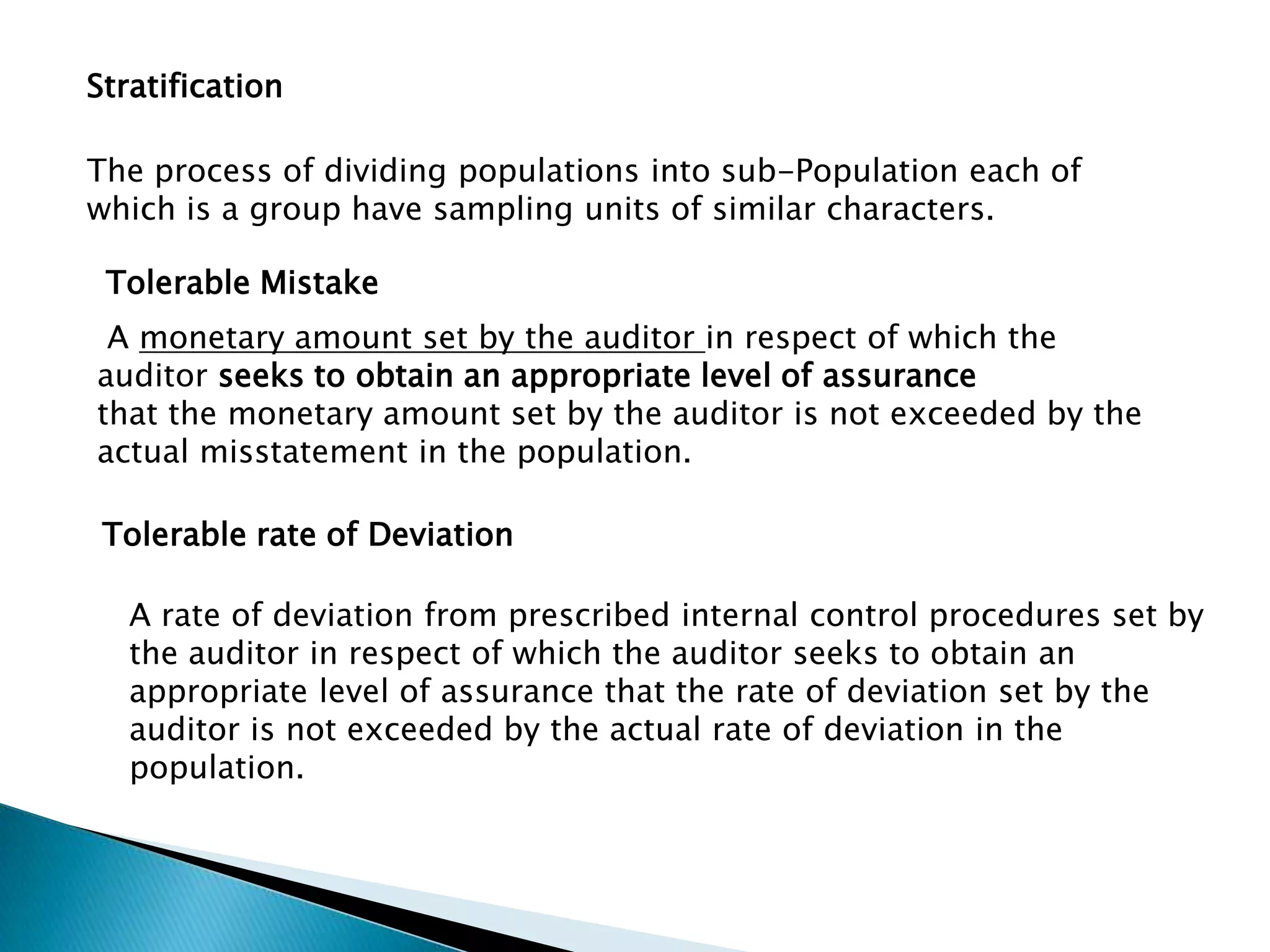

The document outlines the principles and methods of audit sampling, emphasizing the importance of selection techniques to achieve reliable conclusions about a population based on a sample. It discusses statistical and non-statistical sampling approaches, definitions of sampling risks, and the need for stratification to ensure representative samples. The document aims to guide auditors in reducing sampling risks and ensuring accurate evaluation of financial statements.