Downloaded 209 times

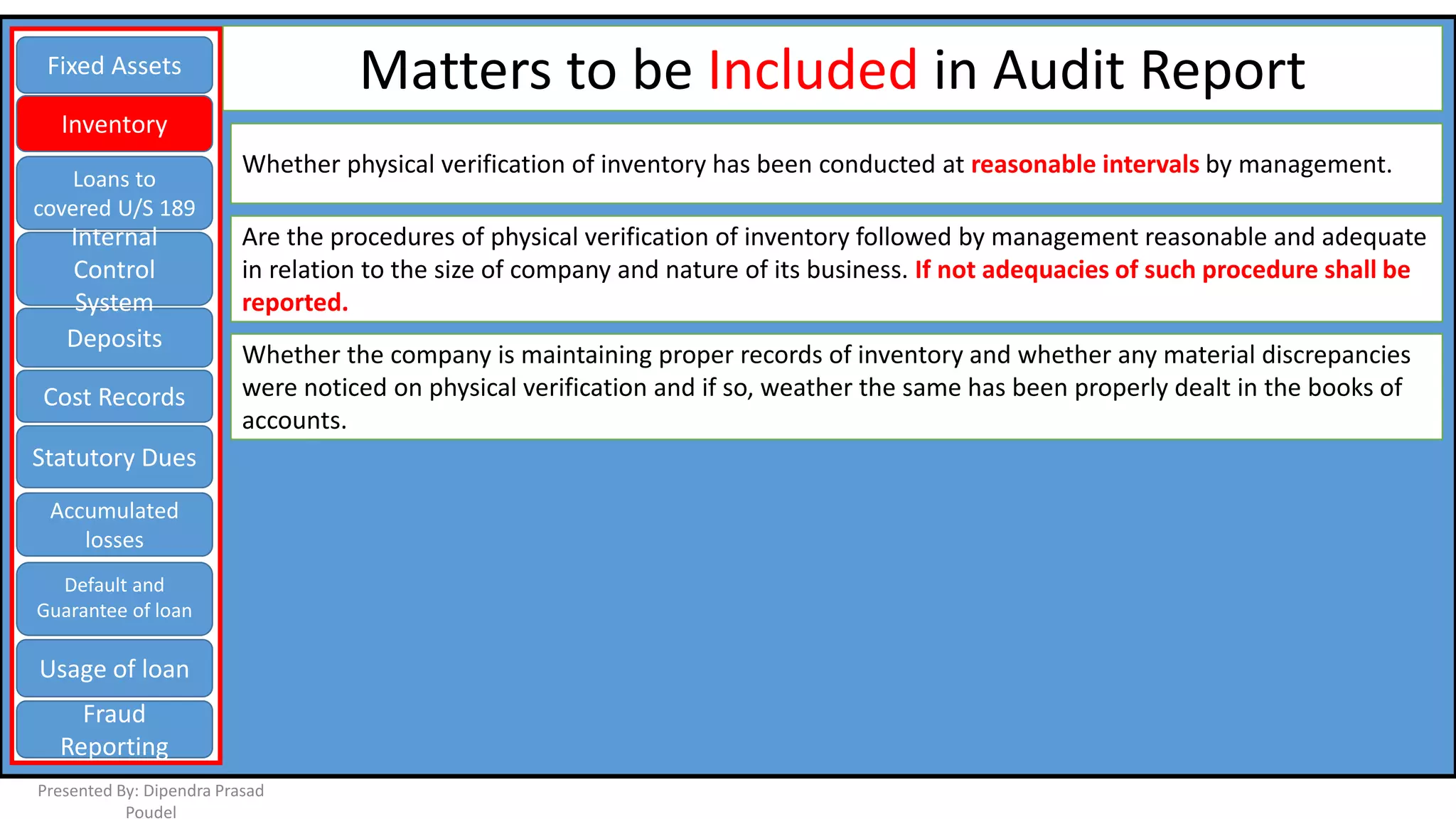

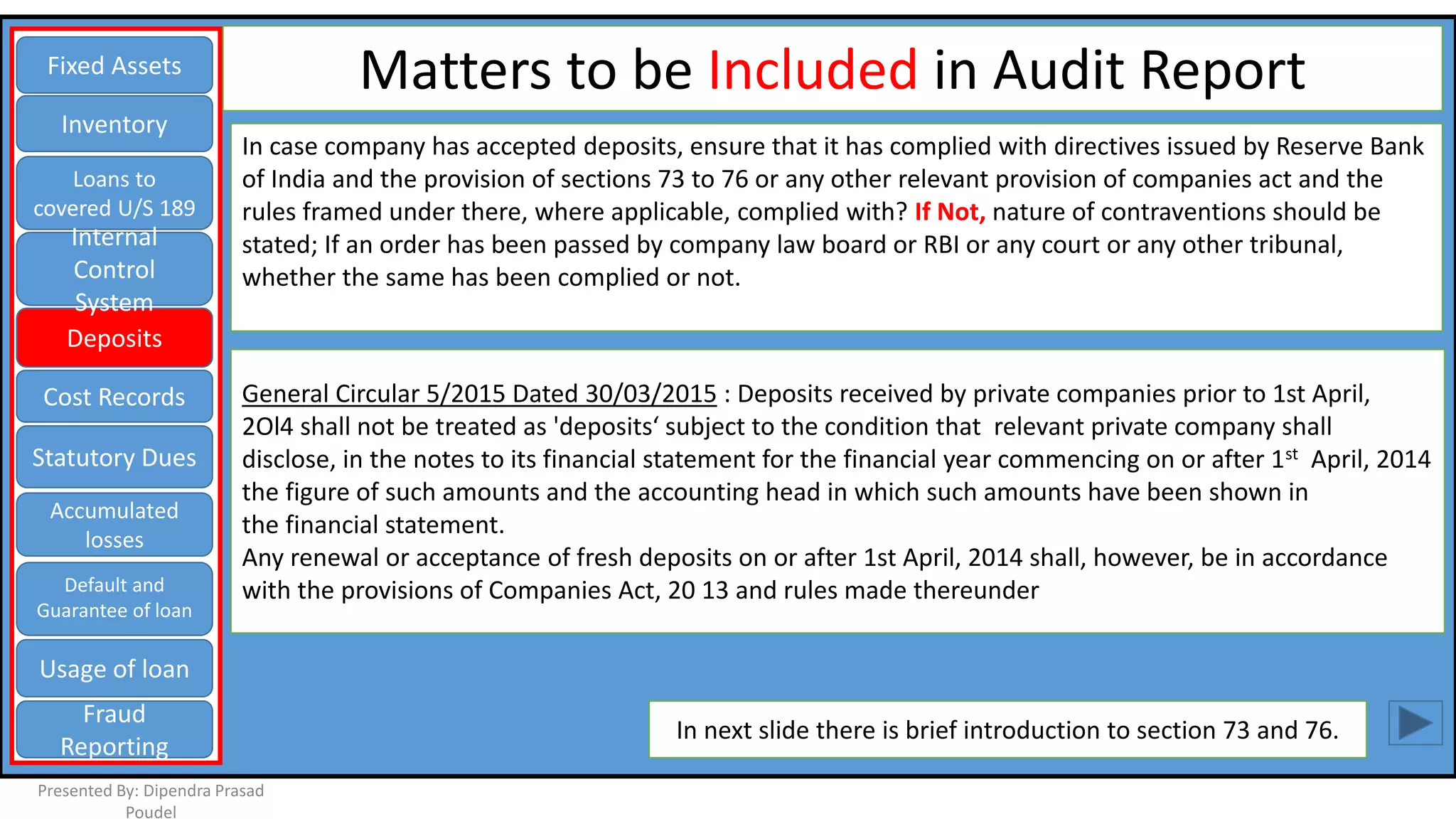

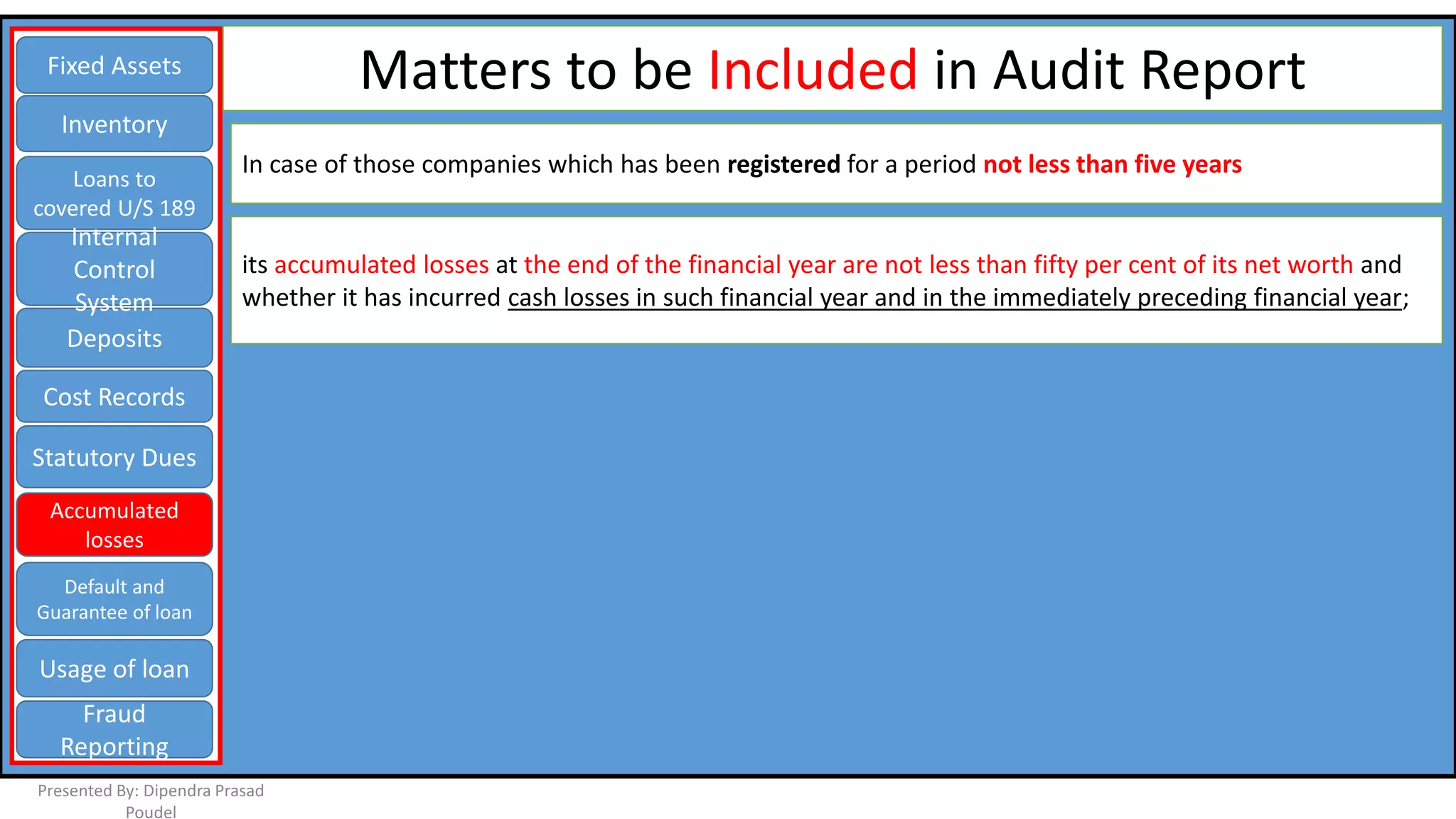

The document presents an auditor's report on Companies Act 2013 and CARO 2015, detailing the applicability and requirements for audit reports including fixed assets, inventory, loans, and fraud reporting. It outlines specific conditions under which companies and certain exceptions must comply, alongside statutory dues and internal control systems. The document serves as a comprehensive guide for auditors assessing compliance and reporting on corporate governance matters.