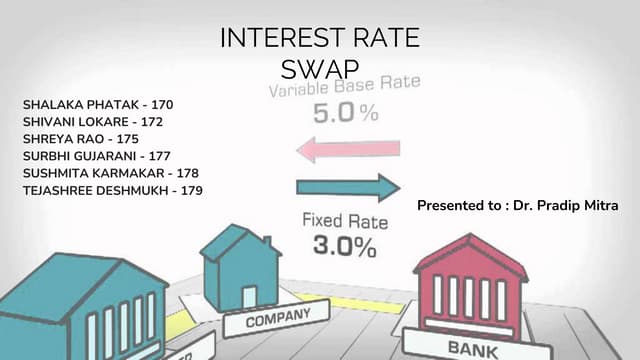

A currency swap involves exchanging interest payments on loans denominated in different currencies. Party A borrows in one currency like INR and pays interest in another currency like USD, while Party B does the opposite. Currency risk can arise if a company's cash flows don't match the currency of its swap payments. Currency swaps are used to hedge currency risk and reduce funding costs. An interest rate swap exchanges a fixed rate loan for a floating rate loan. The interest payments are swapped periodically to allow parties to borrow at lower rates. Interest rate swaps are used for hedging, reducing costs, and speculating on interest rate movements.