Downloaded 14 times

![1. DEFINITION AND FACTS

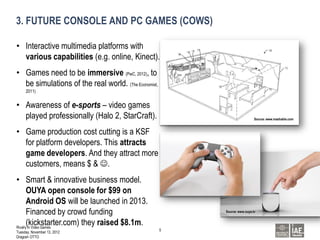

• Electronic game, also called computer game or 12

Source: PwC, 2012

video game, [is] any interactive game operated by 10 10,5 10,7

Average hours spent per week

computer circuit. (…) The term ‘video game’ (…) 8 8,9

can refer more specifically only to games played on

6 6,8

devices with video displays(…). (Britannica Online 6,3

Encyclopedia, 2012) 4 4,9

3,8

• Consoles are no longer the only game in town. 2 2,7

1,8 2

1 0,8

(The Economist, 2011) 0

Console Online on computer Wireless

(portable, phone, tablet)

• Online and wireless games will boost video games. Light Gamers Medium Gamers Heavy Gamers TOTAL

(PwC, 2011)

• Videogames market 2012 is $67bn, growing to

$82bn in 2017 [22% growth potential]. (David Cole, 120

Source: Gardner, 2012

112

DFC, 2012)

Gaming industry prognose in bn$

100

97

• Online games market $19bn in 2011 (…) to reach 80

74

$35bn by 2017 [84% growth potential]. (David Cole, 60

57

DFC, 2012) 51

40 45

• The ongoing economic weakness induced gamers 20 25 21

27 28

18

to shift to less expensive, online and wireless 0

12

options, cutting into the high-priced console game 2011 2013 2015

Gaming Software Gaming Hardware Online Gaming TOTAL

market. (PwC, 2011)

Rivalry in Video Games

3

Tuesday, November 13, 2012

Dragosh OTTO](https://image.slidesharecdn.com/20130223-managinginnovation-casestudy-videogames-slideshare-130223160135-phpapp01/85/RIVALRY-IN-VIDEO-GAMES-Dragosh-OTTO-3-320.jpg)

![4. FUTURE OF MOBILE, WIRELESS, AND SOCIAL GAMES (STARS)

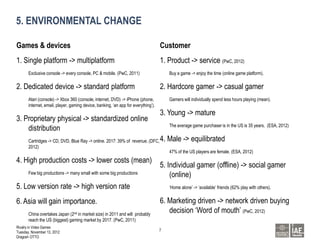

• Now the ever-increasing computing power of mobile 50

Source: PwC, 2012

phones has put the means of playing games. (…) 40

Far more computing power than the original

PlayStation. (The Economist, 2011) 30

Billion $

• Gaming is in fourth place (42 percent), and appears 20

more popular than checking the news (40 percent) 10

and listening to music (40 percent). (Gardner, 2012)

0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

• Price is much lower. Mostly for free. (Farmville)

Online/Wireless Console/PC

• Number of games on App Store and Co. are incomparable to consoles. E.g. App Store offers 128000 games, representing

18% (148Apps.biz, 2012) , Android Market 48244 games, representing about 15% (www.androlib.com, 2012).

• 64% of users who downloaded an [iOS] app in the past 30 days have downloaded a game. (Stan, 2012)

• 52% of all worldwide end user mobile sessions were spent in games. (Farago, 2012)

• “(…) the rules of competition have changed dramatically, arguably creating the most open, egalitarian market in the

history of video games”. (Farago, 2012)

• Purchase is easy. App Store 35bn, Play Store 30bn downloads in less then 5 years.

• Production costs for developers can be low. Focus on game player excitement.

Rivalry in Video Games

6

Tuesday, November 13, 2012

Dragosh OTTO](https://image.slidesharecdn.com/20130223-managinginnovation-casestudy-videogames-slideshare-130223160135-phpapp01/85/RIVALRY-IN-VIDEO-GAMES-Dragosh-OTTO-6-320.jpg)

The document discusses the evolution and current state of rivalry in the video game industry, emphasizing the shift from traditional consoles to online and mobile gaming. It highlights the market growth projections, the importance of immersive gameplay, and the influence of new entrants like mobile platforms on consumer behavior. Additionally, it addresses future trends such as multiplayer gaming and the need for innovative business models to attract both developers and players.