Downloaded 13 times

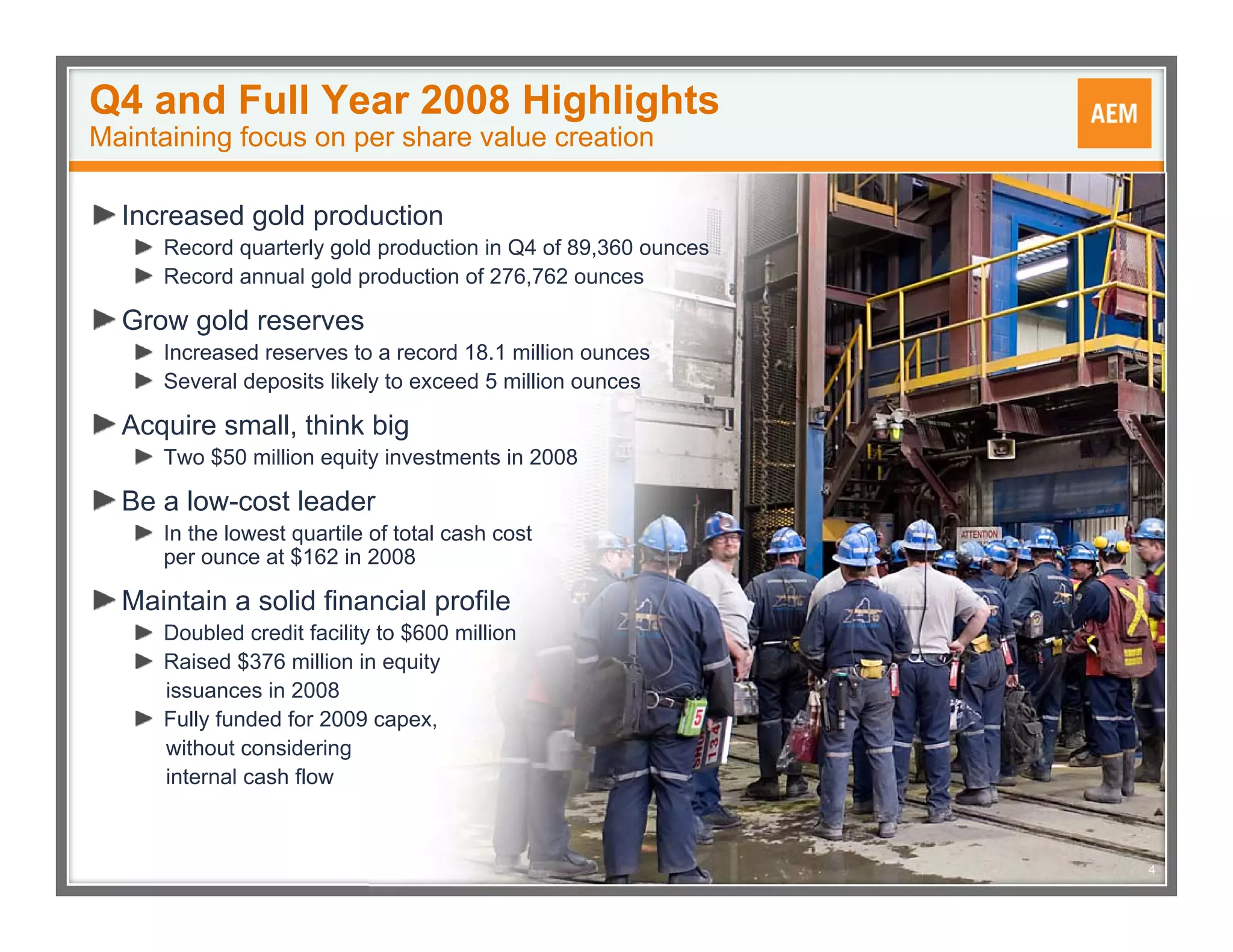

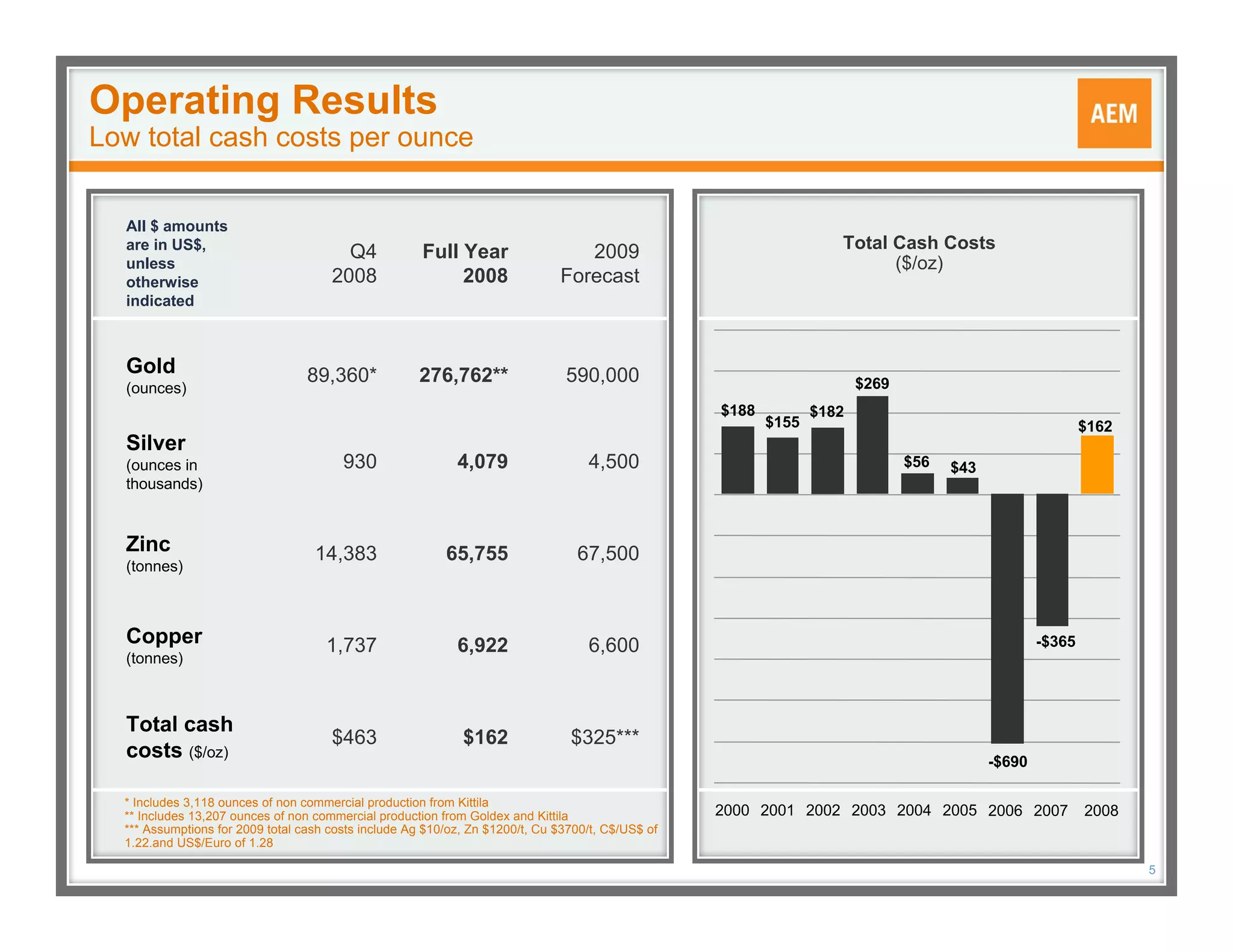

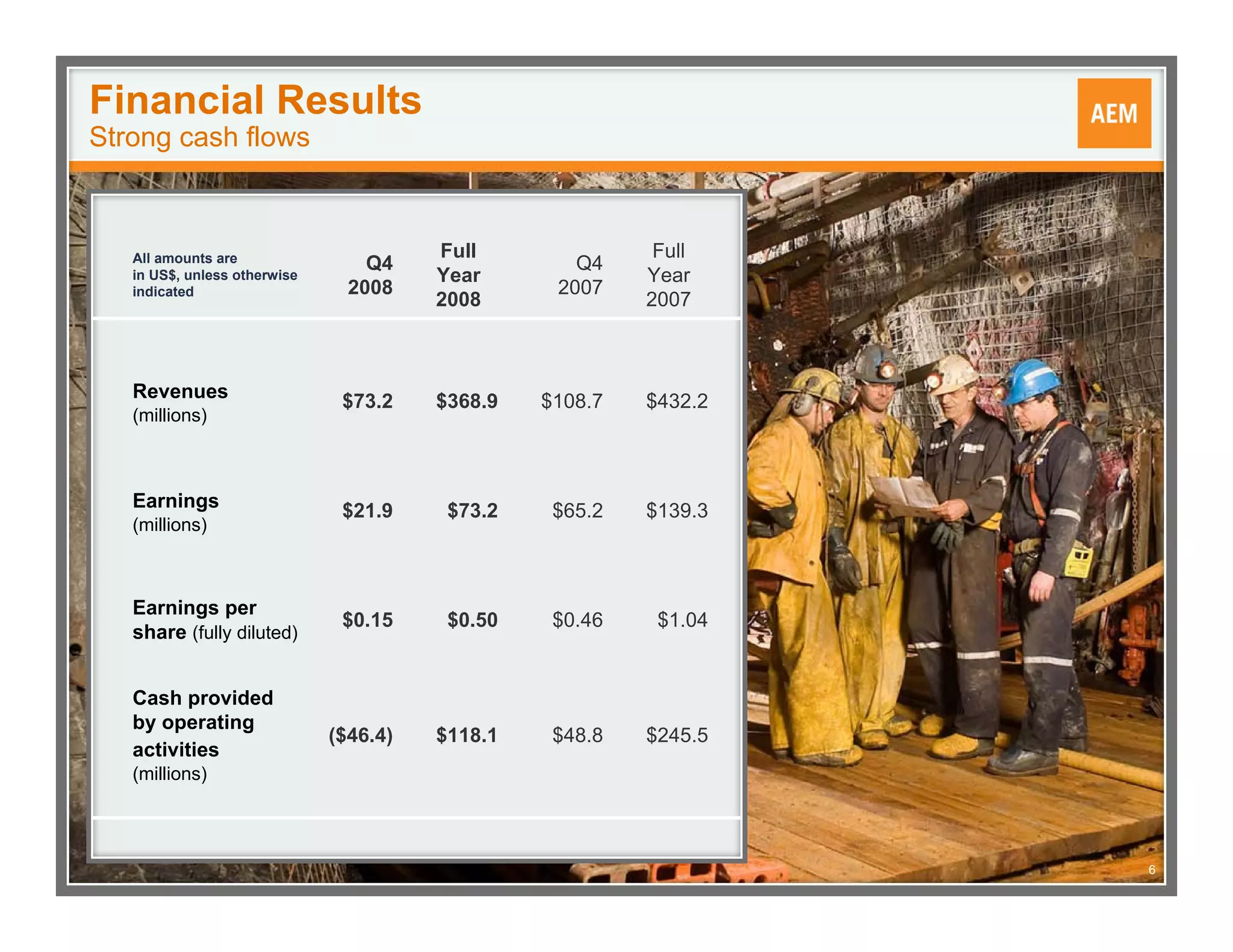

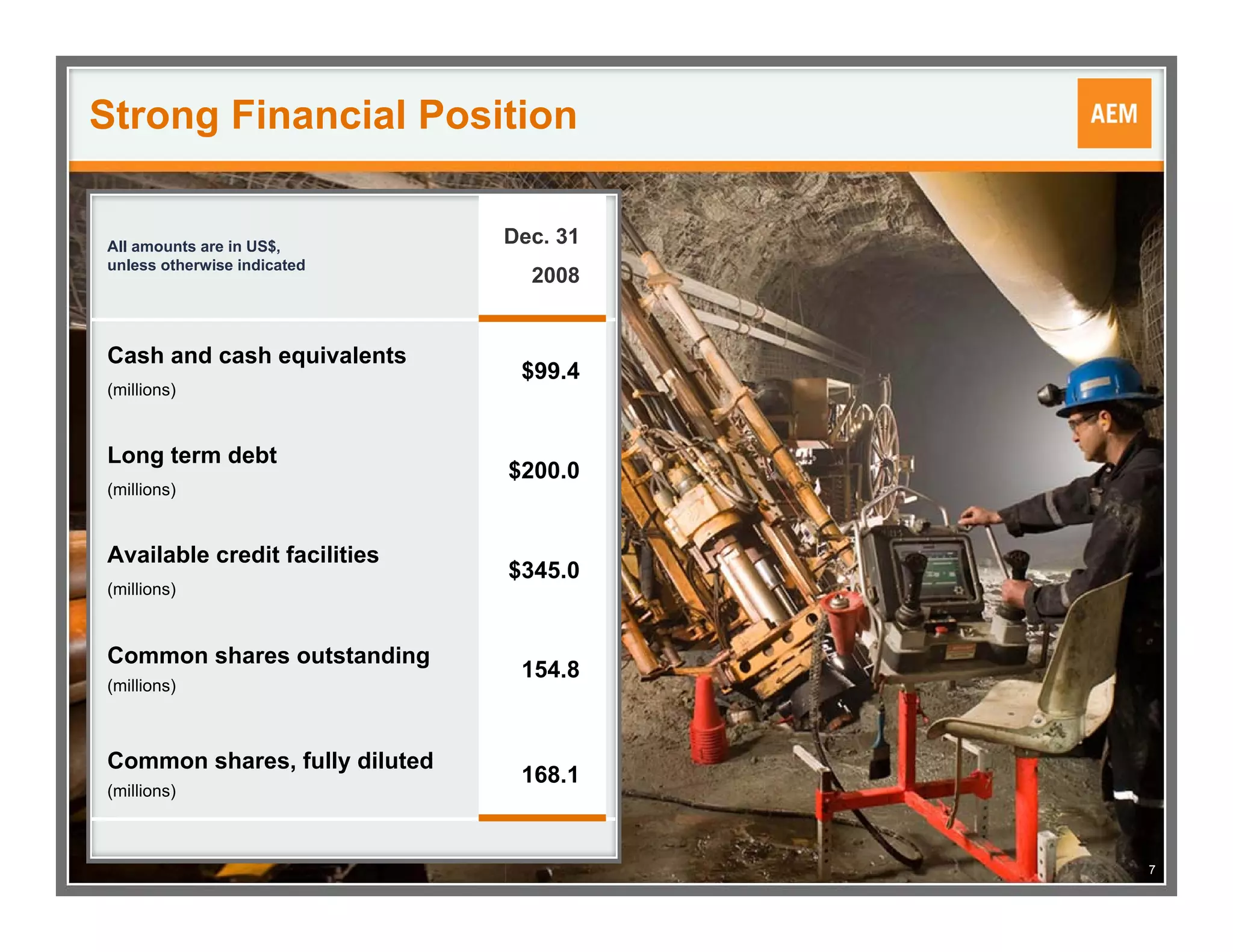

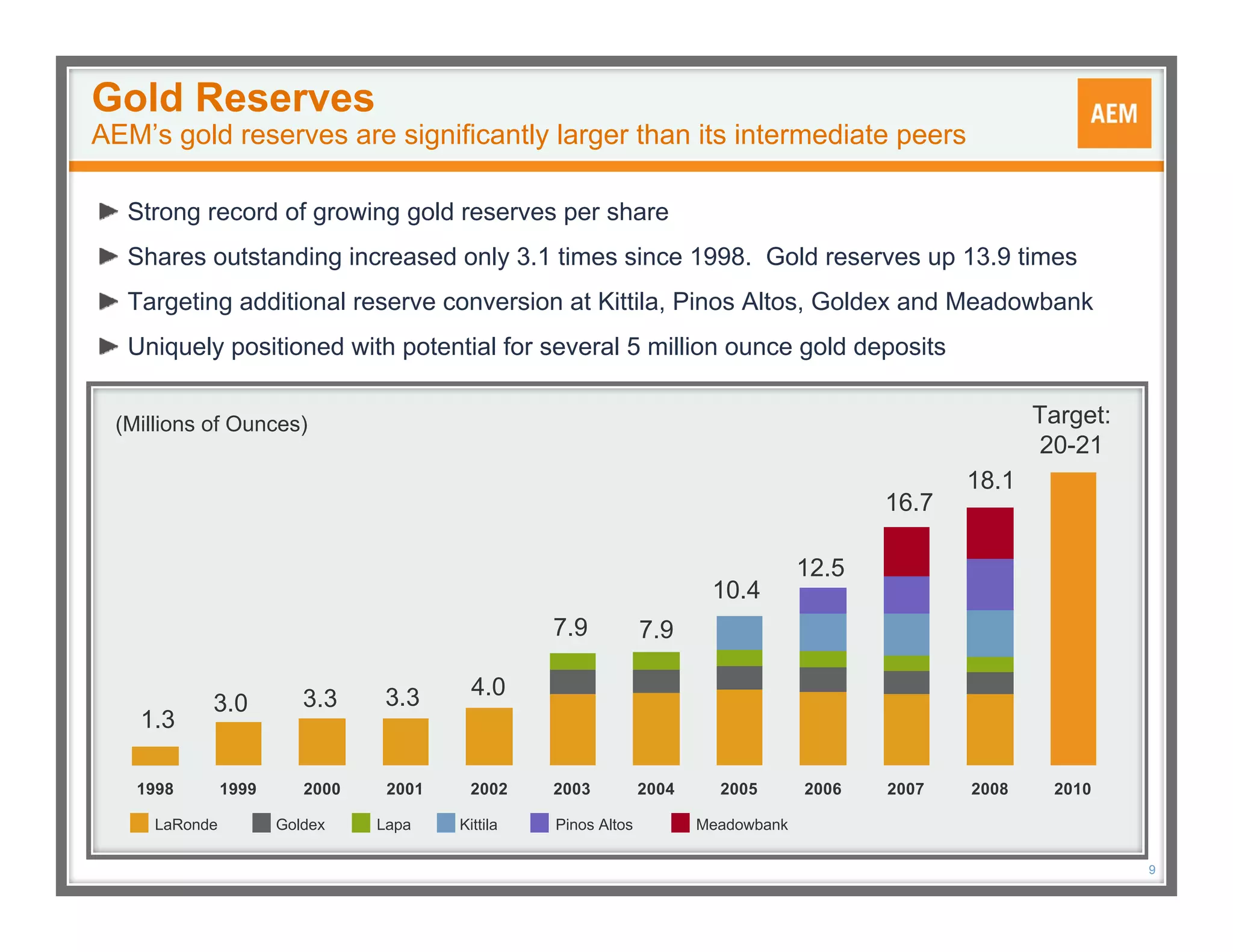

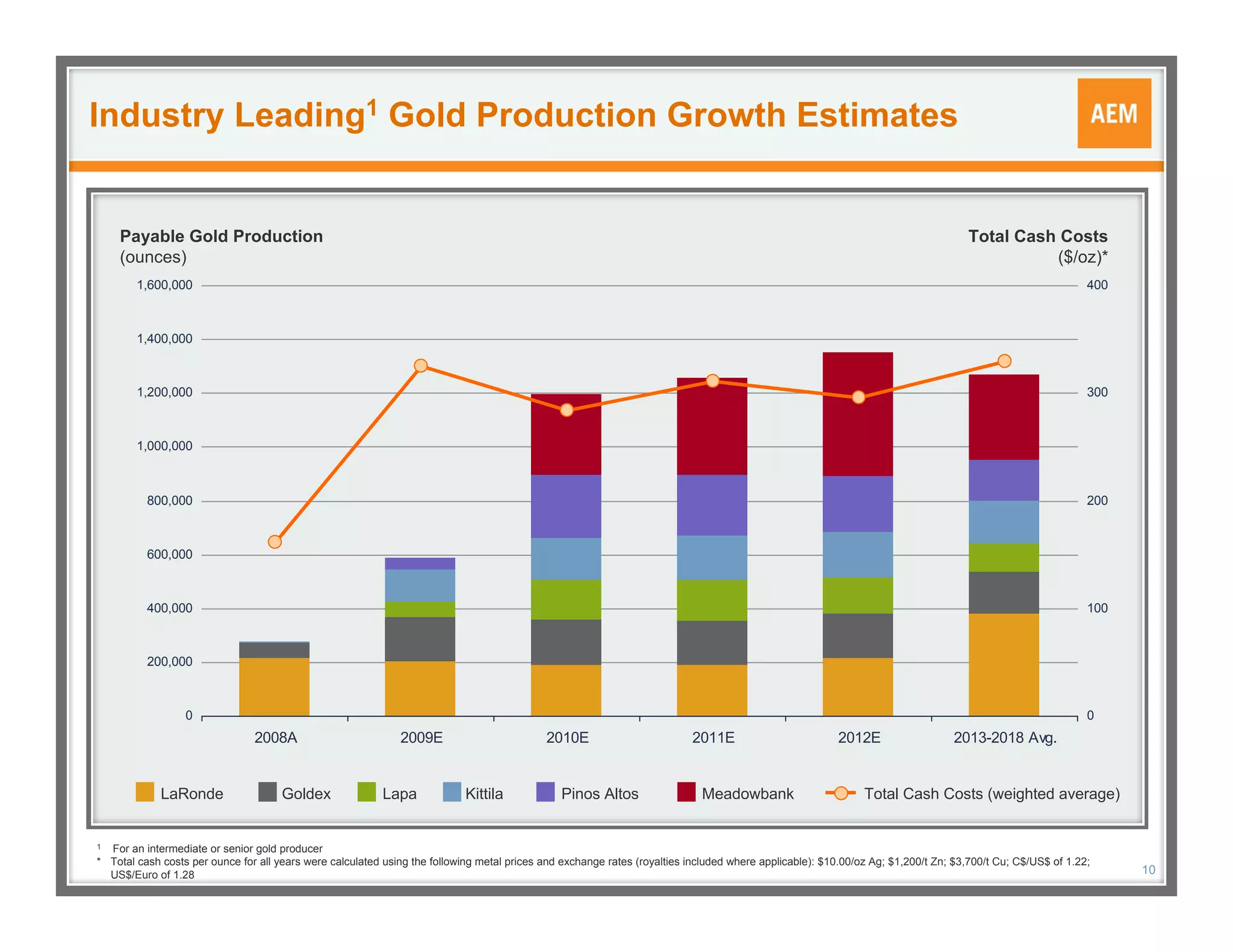

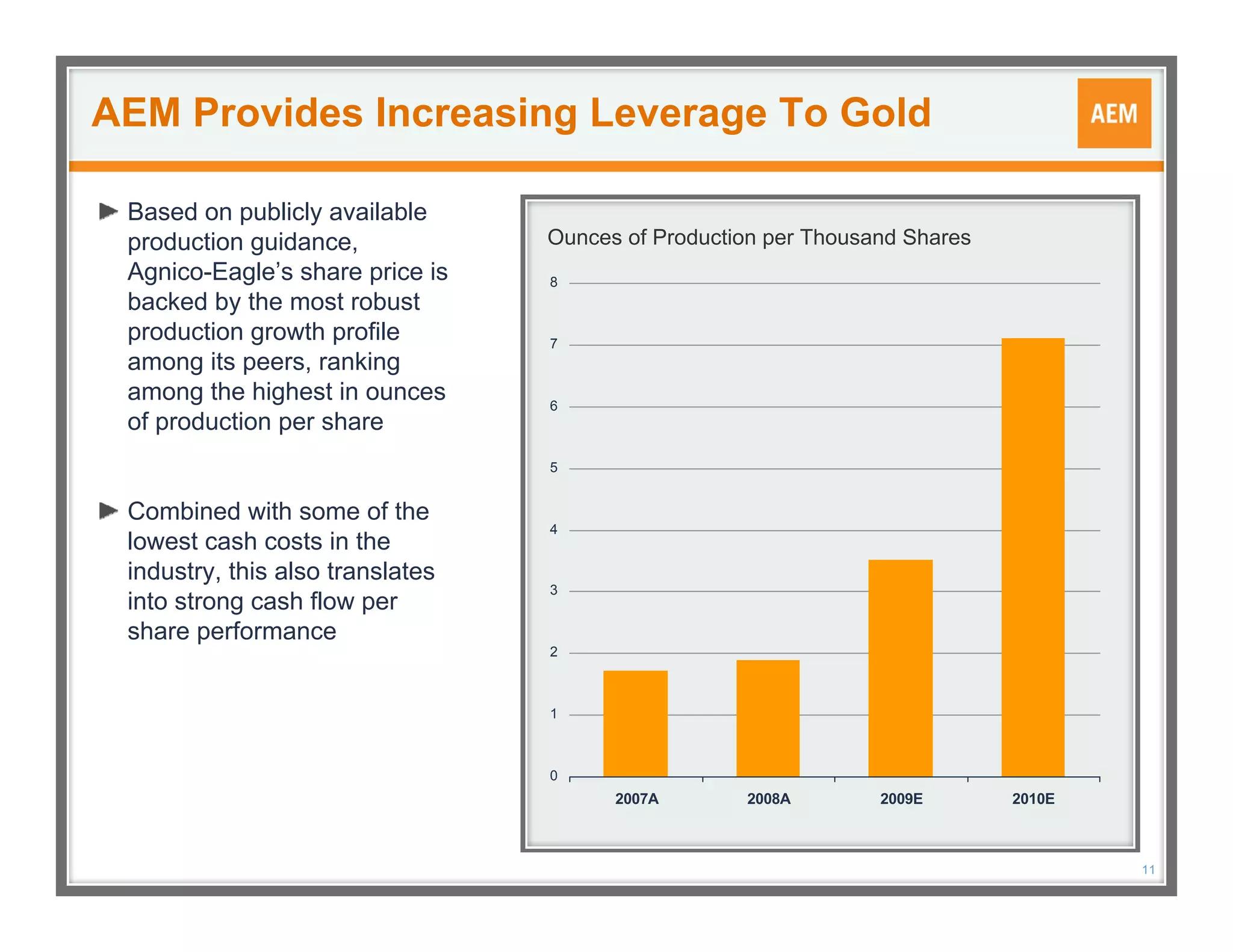

This document provides a corporate update from Agnico-Eagle Mines Limited for February 2009. It summarizes the company's operating and financial results for Q4 and full year 2008, highlights its strong gold reserves which are larger than its peers, and outlines its global growth strategy with three operating mines and three new mines under construction. It also previews upcoming news in 2009 regarding expansion studies at several of its projects which could further increase production.