Download as PDF, PPTX

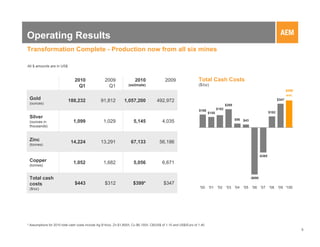

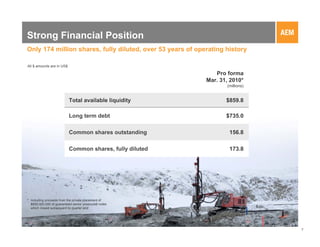

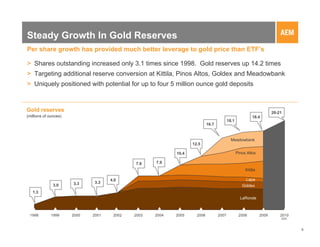

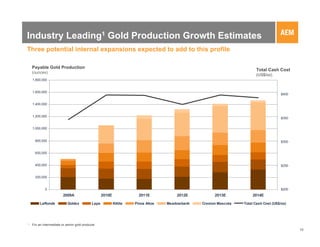

- Agnico-Eagle Mines Limited provided a corporate update in May 2010, outlining its strategy, operating results, and strong financial position. - The company's strategy focuses on increasing gold production, growing gold reserves through acquisitions like Comaplex Minerals Corp, being a low-cost leader, and maintaining a solid financial profile with $860 million in available liquidity. - In Q1 2010 the company produced over 188,000 ounces of gold, exceeding Q1 2009 production, and estimates 2010 full year gold production around 1.057 million ounces at a total cash cost of $399 per ounce. Revenues increased to $237.6 million in Q1 2010.