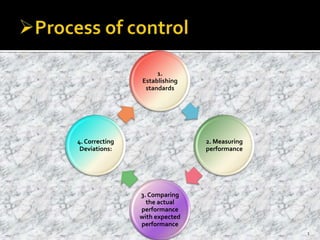

1. The document discusses the process of establishing performance standards, measuring actual performance against those standards, comparing the results, and taking corrective action for any deviations.

2. Key aspects of establishing standards include setting criteria for outputs, costs, profits, market share, and productivity. Performance is then measured using tools like ratio analysis, comparative statistics, and personal observation at control points.

3. The comparison process involves noting any deviations between standards and performance results. The causes and size of deviations are analyzed to determine appropriate corrective actions to implement during ongoing work.

Current trends in cost & management accountingTushar Sadhye

Cost & Management Accounting & Types of costs involvement.

Direct costing as an analysis tool & Cost volume profit analysis.

Target costing & Cost object analysis.

Process analysis & Zero base budgeting.

Cost reduction strategy & Compensation cost reduction.

Procurement cost reduction & Responsibility accounting.

Facilities cost reduction & Finance cost reduction.

Cost management is a form of management accounting.

Cost management is the process of planning and controlling the budget of a business which related to activities achieved by collecting, analyzing, evaluating and reporting cost information used for budgeting, estimating, forecasting, and monitoring costs.

this is presentation about costing system .in this presentation we know about 1)introduction.2)cost accounting in India.3)list of industries in which cost Accounting are there.4)some specfice terms related to cost.5)Importance of good cosing system.6) objectives of good costing system7)prerequisite of Installing good costing system.then at last conclusion we know about what we know about it ,as it is only a small slide share but but there is long process occured to us. If you like this powerpoint then share also.thank you.

Current trends in cost & management accountingTushar Sadhye

Cost & Management Accounting & Types of costs involvement.

Direct costing as an analysis tool & Cost volume profit analysis.

Target costing & Cost object analysis.

Process analysis & Zero base budgeting.

Cost reduction strategy & Compensation cost reduction.

Procurement cost reduction & Responsibility accounting.

Facilities cost reduction & Finance cost reduction.

Cost management is a form of management accounting.

Cost management is the process of planning and controlling the budget of a business which related to activities achieved by collecting, analyzing, evaluating and reporting cost information used for budgeting, estimating, forecasting, and monitoring costs.

this is presentation about costing system .in this presentation we know about 1)introduction.2)cost accounting in India.3)list of industries in which cost Accounting are there.4)some specfice terms related to cost.5)Importance of good cosing system.6) objectives of good costing system7)prerequisite of Installing good costing system.then at last conclusion we know about what we know about it ,as it is only a small slide share but but there is long process occured to us. If you like this powerpoint then share also.thank you.

What is job costing? What are its main characteristics?

Characteristics

Features

procedure involve in job order costing.

Applicability

What is BEP? List out the assumption of breakeven analysis

Assumption of BEP analysis

What is Profit Volume (P/V) Ratio

What is CVP analysis? How does it help the management?

What is process costing? What are its main characteristics? Name the industries where process costing can be applied.

Normal Loss

Abnormal Loss

Abnormal Gain

Job Costing & Process Costing

Accounting for losses in process costing

What do you mean by operating costing? Draw a specimen cost sheet for transport costing.

INDUSTRY AND CORRESPONDING COST UNIT

RECONCILIATION STATEMENT

ACtivItY BaSeD CostinG, Value ChAin AnalysiS, TargeT cosTing & Life Cycle Cos...Sonu Sah

It is the small presentation on the topic of activity based costing, value chain analysis, target costing and life cycle costing of the Cost and Management Accounting.

This presentation covers introduction,meaning,definition,characteristics,objectives,advantages,limitations,essential conditions for an effective system & methods of standard costing.

Introduction to cost managerial accountingVaradraj Bapat

Cost Accounting.

Cost Accounting Objectives.

Cost Accounting advantages.

what is cost?

Cost Classification:

By elements

By function

As direct and indirect

By variability

By controllability

By normality

By relevance

Elements of cost.

Throughput Accounting (Management Accounting and Finance)Kiran Hanjar

Throughput Accounting (TA) is a principle-based and simplified management accounting approach that provides managers with decision support information for enterprise profitability improvement

TA is relatively new in management accounting

It is an approach that identifies factors that limit an organization from reaching its goal, and then focuses on simple measures that drive behavior in key areas towards reaching organizational goals

Throughput Accounting is neither cost accounting nor costing

It is cash focused and does not allocate all costs (variable and fixed expenses, including overheads) to products and services sold or provided by an enterprise

This explain the steps in the control process. #the functions of management. It also covers the requirements for effective control.

Why would one need a good control system

What is job costing? What are its main characteristics?

Characteristics

Features

procedure involve in job order costing.

Applicability

What is BEP? List out the assumption of breakeven analysis

Assumption of BEP analysis

What is Profit Volume (P/V) Ratio

What is CVP analysis? How does it help the management?

What is process costing? What are its main characteristics? Name the industries where process costing can be applied.

Normal Loss

Abnormal Loss

Abnormal Gain

Job Costing & Process Costing

Accounting for losses in process costing

What do you mean by operating costing? Draw a specimen cost sheet for transport costing.

INDUSTRY AND CORRESPONDING COST UNIT

RECONCILIATION STATEMENT

ACtivItY BaSeD CostinG, Value ChAin AnalysiS, TargeT cosTing & Life Cycle Cos...Sonu Sah

It is the small presentation on the topic of activity based costing, value chain analysis, target costing and life cycle costing of the Cost and Management Accounting.

This presentation covers introduction,meaning,definition,characteristics,objectives,advantages,limitations,essential conditions for an effective system & methods of standard costing.

Introduction to cost managerial accountingVaradraj Bapat

Cost Accounting.

Cost Accounting Objectives.

Cost Accounting advantages.

what is cost?

Cost Classification:

By elements

By function

As direct and indirect

By variability

By controllability

By normality

By relevance

Elements of cost.

Throughput Accounting (Management Accounting and Finance)Kiran Hanjar

Throughput Accounting (TA) is a principle-based and simplified management accounting approach that provides managers with decision support information for enterprise profitability improvement

TA is relatively new in management accounting

It is an approach that identifies factors that limit an organization from reaching its goal, and then focuses on simple measures that drive behavior in key areas towards reaching organizational goals

Throughput Accounting is neither cost accounting nor costing

It is cash focused and does not allocate all costs (variable and fixed expenses, including overheads) to products and services sold or provided by an enterprise

This explain the steps in the control process. #the functions of management. It also covers the requirements for effective control.

Why would one need a good control system

Top 10 most important manufacturing performance indicators in 2019MRPeasy

mrpeasy.com

In manufacturing, there are many outside influencing factors, tracking the performance of an operation with KPI metrics means the difference between success and failure. Here are the most important manufacturing performance indicators.

UOP BUS 475 Capstone Final Examination Part 2 : Business Question And Answer...UOP E Help

Get without delay supply from specialists in fixing and offering understanding for BUS 475 Capstone Final Examination Part 2, BUS 475 Capstone Final Examination Part 2 Test Paper, UOP Business 475 Final Exam Solution, BUS 475 Capstone Final Examination Part 2 Questions and Answers, BUS 475 Complete Course, BUS 475 Complete Assignment for University Of Phoenix.

Memorandum Of Association Constitution of Company.pptseri bangash

www.seribangash.com

A Memorandum of Association (MOA) is a legal document that outlines the fundamental principles and objectives upon which a company operates. It serves as the company's charter or constitution and defines the scope of its activities. Here's a detailed note on the MOA:

Contents of Memorandum of Association:

Name Clause: This clause states the name of the company, which should end with words like "Limited" or "Ltd." for a public limited company and "Private Limited" or "Pvt. Ltd." for a private limited company.

https://seribangash.com/article-of-association-is-legal-doc-of-company/

Registered Office Clause: It specifies the location where the company's registered office is situated. This office is where all official communications and notices are sent.

Objective Clause: This clause delineates the main objectives for which the company is formed. It's important to define these objectives clearly, as the company cannot undertake activities beyond those mentioned in this clause.

www.seribangash.com

Liability Clause: It outlines the extent of liability of the company's members. In the case of companies limited by shares, the liability of members is limited to the amount unpaid on their shares. For companies limited by guarantee, members' liability is limited to the amount they undertake to contribute if the company is wound up.

https://seribangash.com/promotors-is-person-conceived-formation-company/

Capital Clause: This clause specifies the authorized capital of the company, i.e., the maximum amount of share capital the company is authorized to issue. It also mentions the division of this capital into shares and their respective nominal value.

Association Clause: It simply states that the subscribers wish to form a company and agree to become members of it, in accordance with the terms of the MOA.

Importance of Memorandum of Association:

Legal Requirement: The MOA is a legal requirement for the formation of a company. It must be filed with the Registrar of Companies during the incorporation process.

Constitutional Document: It serves as the company's constitutional document, defining its scope, powers, and limitations.

Protection of Members: It protects the interests of the company's members by clearly defining the objectives and limiting their liability.

External Communication: It provides clarity to external parties, such as investors, creditors, and regulatory authorities, regarding the company's objectives and powers.

https://seribangash.com/difference-public-and-private-company-law/

Binding Authority: The company and its members are bound by the provisions of the MOA. Any action taken beyond its scope may be considered ultra vires (beyond the powers) of the company and therefore void.

Amendment of MOA:

While the MOA lays down the company's fundamental principles, it is not entirely immutable. It can be amended, but only under specific circumstances and in compliance with legal procedures. Amendments typically require shareholder

Business Valuation Principles for EntrepreneursBen Wann

This insightful presentation is designed to equip entrepreneurs with the essential knowledge and tools needed to accurately value their businesses. Understanding business valuation is crucial for making informed decisions, whether you're seeking investment, planning to sell, or simply want to gauge your company's worth.

3.0 Project 2_ Developing My Brand Identity Kit.pptxtanyjahb

A personal brand exploration presentation summarizes an individual's unique qualities and goals, covering strengths, values, passions, and target audience. It helps individuals understand what makes them stand out, their desired image, and how they aim to achieve it.

Improving profitability for small businessBen Wann

In this comprehensive presentation, we will explore strategies and practical tips for enhancing profitability in small businesses. Tailored to meet the unique challenges faced by small enterprises, this session covers various aspects that directly impact the bottom line. Attendees will learn how to optimize operational efficiency, manage expenses, and increase revenue through innovative marketing and customer engagement techniques.

Personal Brand Statement:

As an Army veteran dedicated to lifelong learning, I bring a disciplined, strategic mindset to my pursuits. I am constantly expanding my knowledge to innovate and lead effectively. My journey is driven by a commitment to excellence, and to make a meaningful impact in the world.

"𝑩𝑬𝑮𝑼𝑵 𝑾𝑰𝑻𝑯 𝑻𝑱 𝑰𝑺 𝑯𝑨𝑳𝑭 𝑫𝑶𝑵𝑬"

𝐓𝐉 𝐂𝐨𝐦𝐬 (𝐓𝐉 𝐂𝐨𝐦𝐦𝐮𝐧𝐢𝐜𝐚𝐭𝐢𝐨𝐧𝐬) is a professional event agency that includes experts in the event-organizing market in Vietnam, Korea, and ASEAN countries. We provide unlimited types of events from Music concerts, Fan meetings, and Culture festivals to Corporate events, Internal company events, Golf tournaments, MICE events, and Exhibitions.

𝐓𝐉 𝐂𝐨𝐦𝐬 provides unlimited package services including such as Event organizing, Event planning, Event production, Manpower, PR marketing, Design 2D/3D, VIP protocols, Interpreter agency, etc.

Sports events - Golf competitions/billiards competitions/company sports events: dynamic and challenging

⭐ 𝐅𝐞𝐚𝐭𝐮𝐫𝐞𝐝 𝐩𝐫𝐨𝐣𝐞𝐜𝐭𝐬:

➢ 2024 BAEKHYUN [Lonsdaleite] IN HO CHI MINH

➢ SUPER JUNIOR-L.S.S. THE SHOW : Th3ee Guys in HO CHI MINH

➢FreenBecky 1st Fan Meeting in Vietnam

➢CHILDREN ART EXHIBITION 2024: BEYOND BARRIERS

➢ WOW K-Music Festival 2023

➢ Winner [CROSS] Tour in HCM

➢ Super Show 9 in HCM with Super Junior

➢ HCMC - Gyeongsangbuk-do Culture and Tourism Festival

➢ Korean Vietnam Partnership - Fair with LG

➢ Korean President visits Samsung Electronics R&D Center

➢ Vietnam Food Expo with Lotte Wellfood

"𝐄𝐯𝐞𝐫𝐲 𝐞𝐯𝐞𝐧𝐭 𝐢𝐬 𝐚 𝐬𝐭𝐨𝐫𝐲, 𝐚 𝐬𝐩𝐞𝐜𝐢𝐚𝐥 𝐣𝐨𝐮𝐫𝐧𝐞𝐲. 𝐖𝐞 𝐚𝐥𝐰𝐚𝐲𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞 𝐭𝐡𝐚𝐭 𝐬𝐡𝐨𝐫𝐭𝐥𝐲 𝐲𝐨𝐮 𝐰𝐢𝐥𝐥 𝐛𝐞 𝐚 𝐩𝐚𝐫𝐭 𝐨𝐟 𝐨𝐮𝐫 𝐬𝐭𝐨𝐫𝐢𝐞𝐬."

RMD24 | Debunking the non-endemic revenue myth Marvin Vacquier Droop | First ...BBPMedia1

Marvin neemt je in deze presentatie mee in de voordelen van non-endemic advertising op retail media netwerken. Hij brengt ook de uitdagingen in beeld die de markt op dit moment heeft op het gebied van retail media voor niet-leveranciers.

Retail media wordt gezien als het nieuwe advertising-medium en ook mediabureaus richten massaal retail media-afdelingen op. Merken die niet in de betreffende winkel liggen staan ook nog niet in de rij om op de retail media netwerken te adverteren. Marvin belicht de uitdagingen die er zijn om echt aansluiting te vinden op die markt van non-endemic advertising.

Taurus Zodiac Sign_ Personality Traits and Sign Dates.pptxmy Pandit

Explore the world of the Taurus zodiac sign. Learn about their stability, determination, and appreciation for beauty. Discover how Taureans' grounded nature and hardworking mindset define their unique personality.

Enterprise Excellence is Inclusive Excellence.pdfKaiNexus

Enterprise excellence and inclusive excellence are closely linked, and real-world challenges have shown that both are essential to the success of any organization. To achieve enterprise excellence, organizations must focus on improving their operations and processes while creating an inclusive environment that engages everyone. In this interactive session, the facilitator will highlight commonly established business practices and how they limit our ability to engage everyone every day. More importantly, though, participants will likely gain increased awareness of what we can do differently to maximize enterprise excellence through deliberate inclusion.

What is Enterprise Excellence?

Enterprise Excellence is a holistic approach that's aimed at achieving world-class performance across all aspects of the organization.

What might I learn?

A way to engage all in creating Inclusive Excellence. Lessons from the US military and their parallels to the story of Harry Potter. How belt systems and CI teams can destroy inclusive practices. How leadership language invites people to the party. There are three things leaders can do to engage everyone every day: maximizing psychological safety to create environments where folks learn, contribute, and challenge the status quo.

Who might benefit? Anyone and everyone leading folks from the shop floor to top floor.

Dr. William Harvey is a seasoned Operations Leader with extensive experience in chemical processing, manufacturing, and operations management. At Michelman, he currently oversees multiple sites, leading teams in strategic planning and coaching/practicing continuous improvement. William is set to start his eighth year of teaching at the University of Cincinnati where he teaches marketing, finance, and management. William holds various certifications in change management, quality, leadership, operational excellence, team building, and DiSC, among others.

Cracking the Workplace Discipline Code Main.pptxWorkforce Group

Cultivating and maintaining discipline within teams is a critical differentiator for successful organisations.

Forward-thinking leaders and business managers understand the impact that discipline has on organisational success. A disciplined workforce operates with clarity, focus, and a shared understanding of expectations, ultimately driving better results, optimising productivity, and facilitating seamless collaboration.

Although discipline is not a one-size-fits-all approach, it can help create a work environment that encourages personal growth and accountability rather than solely relying on punitive measures.

In this deck, you will learn the significance of workplace discipline for organisational success. You’ll also learn

• Four (4) workplace discipline methods you should consider

• The best and most practical approach to implementing workplace discipline.

• Three (3) key tips to maintain a disciplined workplace.

Skye Residences | Extended Stay Residences Near Toronto Airportmarketingjdass

Experience unparalleled EXTENDED STAY and comfort at Skye Residences located just minutes from Toronto Airport. Discover sophisticated accommodations tailored for discerning travelers.

Website Link :

https://skyeresidences.com/

https://skyeresidences.com/about-us/

https://skyeresidences.com/gallery/

https://skyeresidences.com/rooms/

https://skyeresidences.com/near-by-attractions/

https://skyeresidences.com/commute/

https://skyeresidences.com/contact/

https://skyeresidences.com/queen-suite-with-sofa-bed/

https://skyeresidences.com/queen-suite-with-sofa-bed-and-balcony/

https://skyeresidences.com/queen-suite-with-sofa-bed-accessible/

https://skyeresidences.com/2-bedroom-deluxe-queen-suite-with-sofa-bed/

https://skyeresidences.com/2-bedroom-deluxe-king-queen-suite-with-sofa-bed/

https://skyeresidences.com/2-bedroom-deluxe-queen-suite-with-sofa-bed-accessible/

#Skye Residences Etobicoke, #Skye Residences Near Toronto Airport, #Skye Residences Toronto, #Skye Hotel Toronto, #Skye Hotel Near Toronto Airport, #Hotel Near Toronto Airport, #Near Toronto Airport Accommodation, #Suites Near Toronto Airport, #Etobicoke Suites Near Airport, #Hotel Near Toronto Pearson International Airport, #Toronto Airport Suite Rentals, #Pearson Airport Hotel Suites

India Orthopedic Devices Market: Unlocking Growth Secrets, Trends and Develop...Kumar Satyam

According to TechSci Research report, “India Orthopedic Devices Market -Industry Size, Share, Trends, Competition Forecast & Opportunities, 2030”, the India Orthopedic Devices Market stood at USD 1,280.54 Million in 2024 and is anticipated to grow with a CAGR of 7.84% in the forecast period, 2026-2030F. The India Orthopedic Devices Market is being driven by several factors. The most prominent ones include an increase in the elderly population, who are more prone to orthopedic conditions such as osteoporosis and arthritis. Moreover, the rise in sports injuries and road accidents are also contributing to the demand for orthopedic devices. Advances in technology and the introduction of innovative implants and prosthetics have further propelled the market growth. Additionally, government initiatives aimed at improving healthcare infrastructure and the increasing prevalence of lifestyle diseases have led to an upward trend in orthopedic surgeries, thereby fueling the market demand for these devices.

2. Standards are criteria against which results

are measured.

They are norms to achieve the goals.

Standards are usually measured in terms of

output.

They can also be measured in non-monetary

terms like loyalty, customer attraction,

goodwill etc. Some of the standards are as.

2

3. Time standards:

The goal will be set on the basis of time lapse in

performing a task.

Cost standards:

These indicate the financial expenditures

involved per unit, e.g. material cost per unit, cost

per person, etc.

Income standards:

These relate to financial rewards received due to

a particular activity like sales volume per month,

year etc.

3

4. Market share:

This relates to the share of the company's

product in the market.

Productivity:

Productivity can be measured on the basis of

units produced per man hour etc.

Profitability:

These goals will be set with the consideration

of cost per unit, market share, etc.

4

5. Measurement involves comparison between

what is accomplished and what was intended to

be accomplished.

The measurement of actual performance must

be in the units similar to those of pre-

determined criterion.

The units which are chosen must be clear, well-

defined and easily identified, and should be

uniform and homogenous throughout the

measurement process.

5

6. The performance can be measured by the

following steps:

a) Strategic control points:

b) measuring devices:

c) Ratio analysis:

d) Comparative statistical analysis:

e) Personal observation:

6

7. It is not possible to check everything that is

being done. So it is necessary to pick

strategic control points for measurement.

Some of these points are:

Continue…

7

8. (i) Income:

It is a significant control point and must be as

much per unit of time as was expected. If the

income is significantly off form the expectation

then the reasons should be investigated and a

corrective action taken.

(ii) Expenses:

Total and operational cost per unit must be

computed and must be adhered to. Key expense

data must be reviewed periodically.

8

9. (iii) Inventory:

Some minimum inventory of both the finished

product as well as raw materials must be kept in

stock as a buffer. Any change in inventory level

would determine whether the production is to

be increased or decreased.

(iv) Quality of the product:

Standards of established quality must be

maintained especially in food processing, drug

manufacturing, automobiles, etc.The process

should be continuously observed for any

deviations.

9

10. (v) Absenteeism:

Excessive absenteeism of personnel is a

serious reflection on the environment and

working conditions.Absenteeism in excess of

chance expectations must be seriously

investigated.

10

11. This involves a wide variant of technical

instruments used for measurement of

machine operations, product "quality for size

and ingredients and production processes.

These instruments may be mechanical,

electronic or chemical in nature.

11

12. Ratio analysis is one of the most important

management tools. It describes the

relationship of one business variable to

another.

The following are some of the important

ratios

Continue….

12

13. i) Net sales to working capital:

The working capital must be utilised adequately.

If the inventory turnover is rapid then the same

working capital can be used again and again.

Hence for perishable goods, this ratio is high.

Any change in ratio will signal a deviation from

the norm.

ii) Net sales to inventory:

The greater the turnover of inventory, generally,

the higher the profit on investment.

Continue….

13

14. iii) Current ratio:

This is the ratio of current asset to current liabilities, and is

used to determine a firm's ability to pay the short term

debts.

iv) Net profits to net sale:

This ratio measures the short-run profitability of a business.

v) Collection period on credit sales:

The collection period should be as short as possible. Any

deviation from established collection period should be

promptly investigated.

14

15. vi) Net profits to tangible net worth:

Net worth is the difference between tangible

assets and total liabilities.This ratio of net

worth is used to measure profitability over a

long period.

vii) Net profits to net working capital:

The net-working capital is the operating

capital at hand.This would determine the

ability of the business to finance day-to-day

operations.

15

16. The operations of one company can be

usefully compared with similar operations of

another company or with industry averages.

It is a very useful performance measuring

device.

16

17. Personal observation both formal and

informal can be used in certain situation as a

measuring device for performances, specially,

the performance of the personnel.

The informal observation is generally a day-

to-day routine type. A manager may walk

through a store to have a general idea about

how people are working.

17

18. This is the active principle of the process.

The previous two, setting the goals and the

measurement format are the preparatory

parts of the process. It is the responsibility of

the management to compare the actual

performance against the standards

established.

Continue….

18

19. This comparison is less complicate if the

measurement units for the standards set and

the performance measured are the same and

quantified.The comparison becomes more

difficult when these require subjective

evaluations

There are four phases in comparison steps

which are given below

Continue….

19

21. At the third phase, deviations if any are noted

between standards and performance. If clear

cut deviations are there, then management

must study the:-

(i) Causes for deviation

(ii) Effect of deviation

(iii) Size of deviation

(iv) Positive or negative deviation.

21

22. The final element in the process is the taking

corrective action.

Measuring and comparing performance, detecting

shortcomings, failures or deviations, from plans etc…

Thus controlling to be effective, should involve not

only the detection of lapses but also probe into the

failure spots, fixation of responsibility for the failures

at the right quarters, recommendation of the best

possible steps to correct them.

These corrective actions must be applied when the

work is in progress.The primary objective should be

avoidance of such failures

22