Cost and management accounting techniques are essential tools for effective decision making. Some key techniques discussed are:

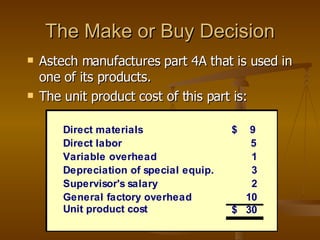

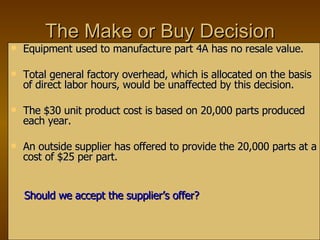

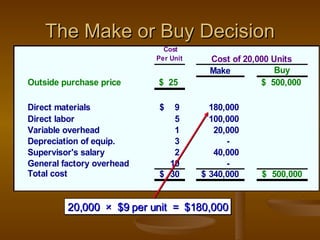

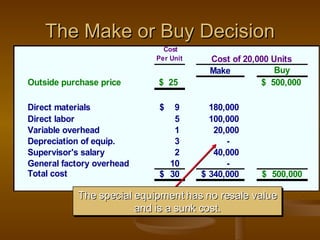

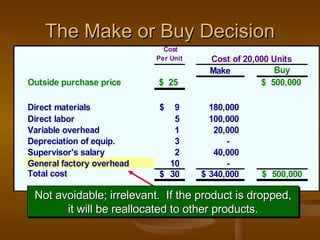

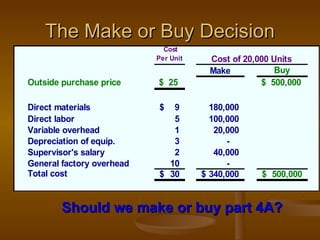

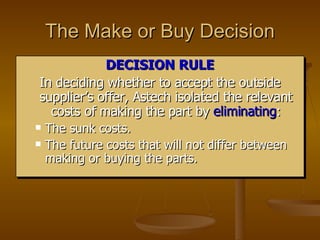

1) Make or buy analysis which helps decide whether to produce an item internally or purchase it based on relevant costs like variable production costs and supplier prices.

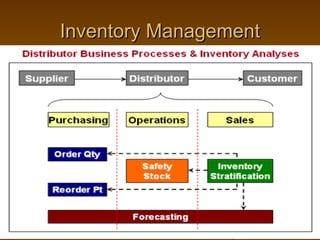

2) Inventory management techniques like just-in-time and economic order quantity which aim to reduce inventory costs.

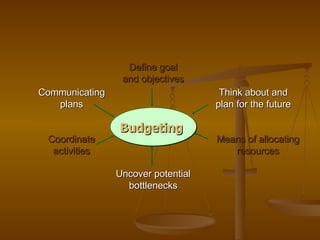

3) Budgeting allows defining goals, coordinating activities, and allocating resources.

4) Variance analysis identifies reasons for deviations from budgets.

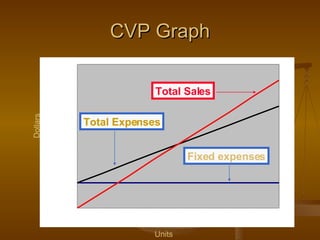

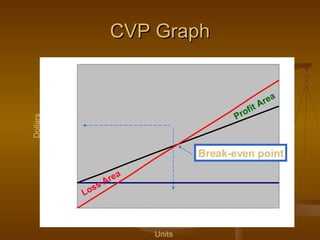

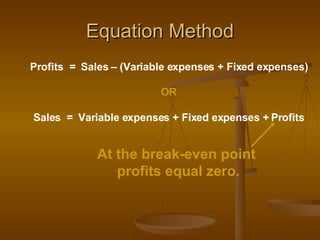

5) Cost-volume-profit analysis uses graphs and equations to understand break-even points and profit/loss areas.

6) Activity based costing allocates overhead costs based on