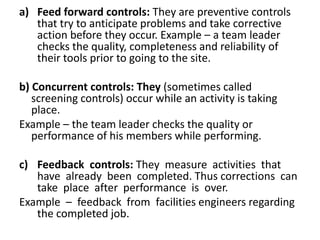

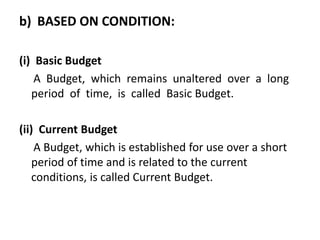

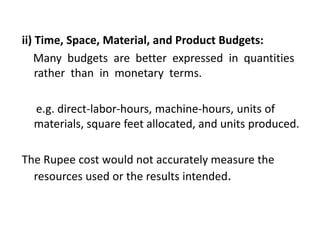

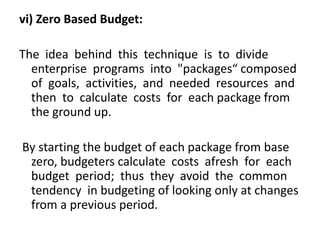

Control is the process of ensuring actual activities conform to plans by measuring performance and correcting deviations. It involves establishing standards, measuring performance, comparing to standards, and taking corrective actions if needed. There are three types of control systems - feed forward, concurrent, and feedback. Budgetary control compares actual spending to planned spending to see if plans need adjusting. It involves preparing budgets of different types based on factors like time period, conditions, capacity, and coverage area. Non-budgetary techniques like statistical data, break-even analysis, audits, and observation also aid managerial control.