Downloaded 90 times

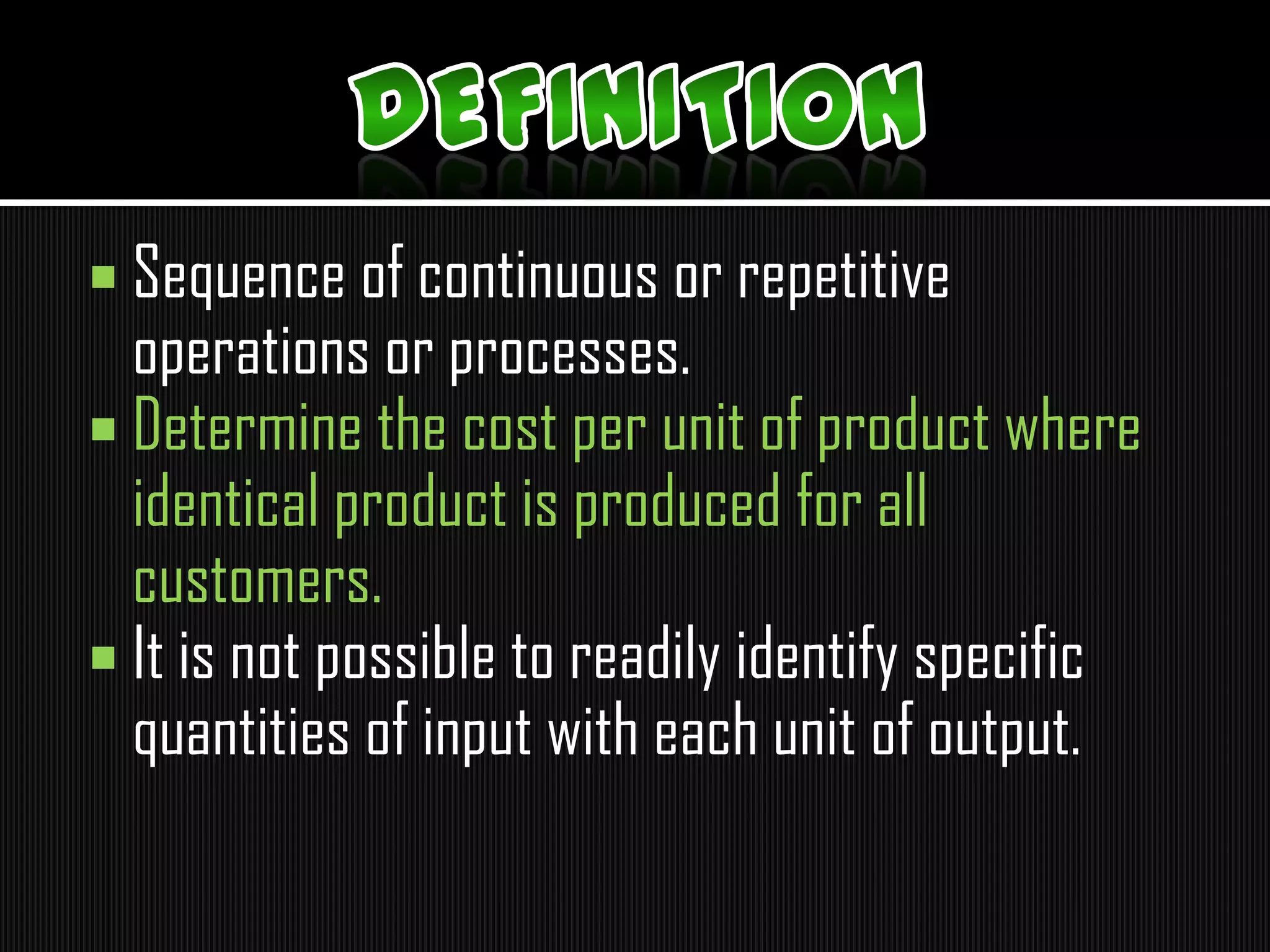

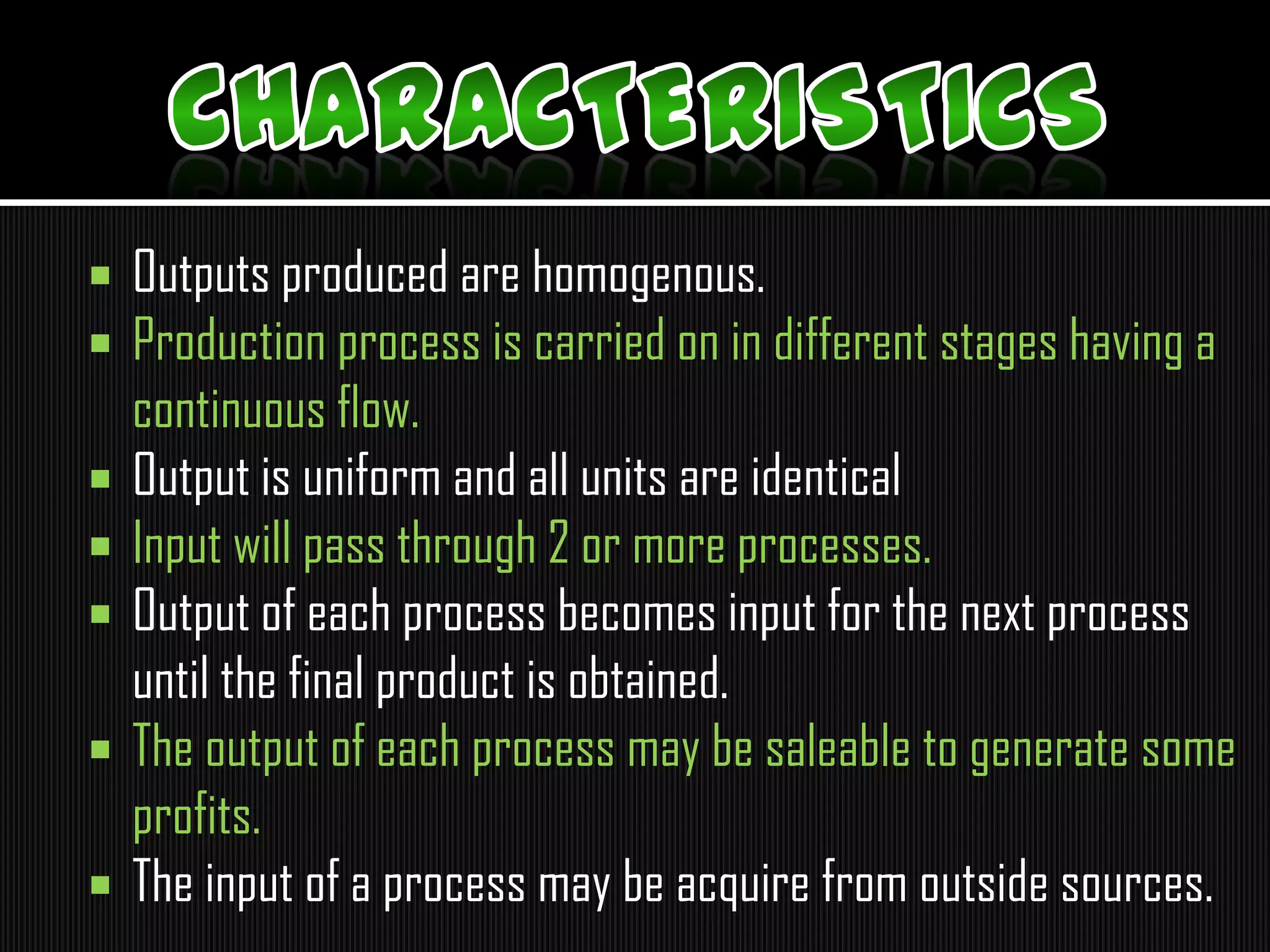

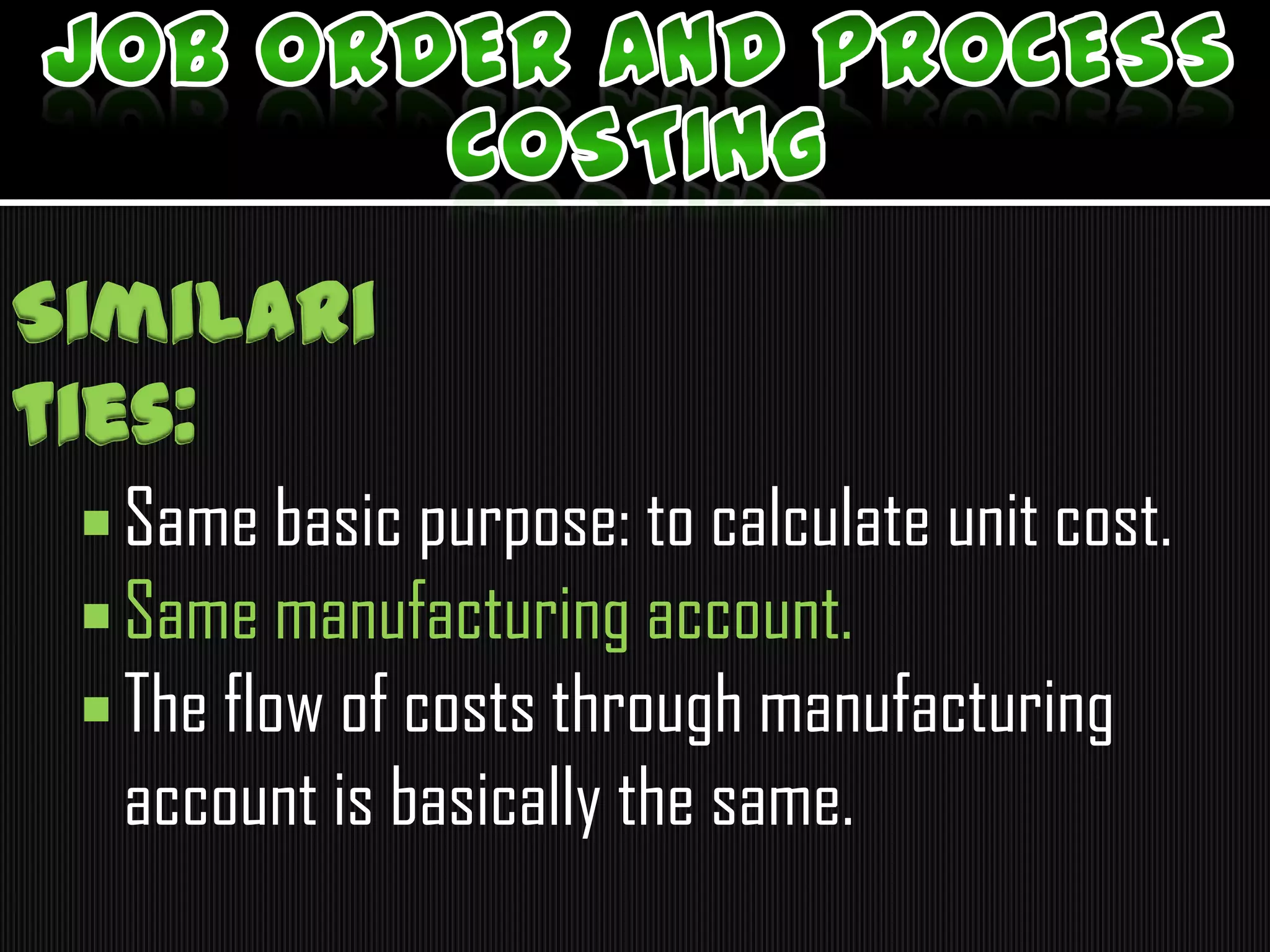

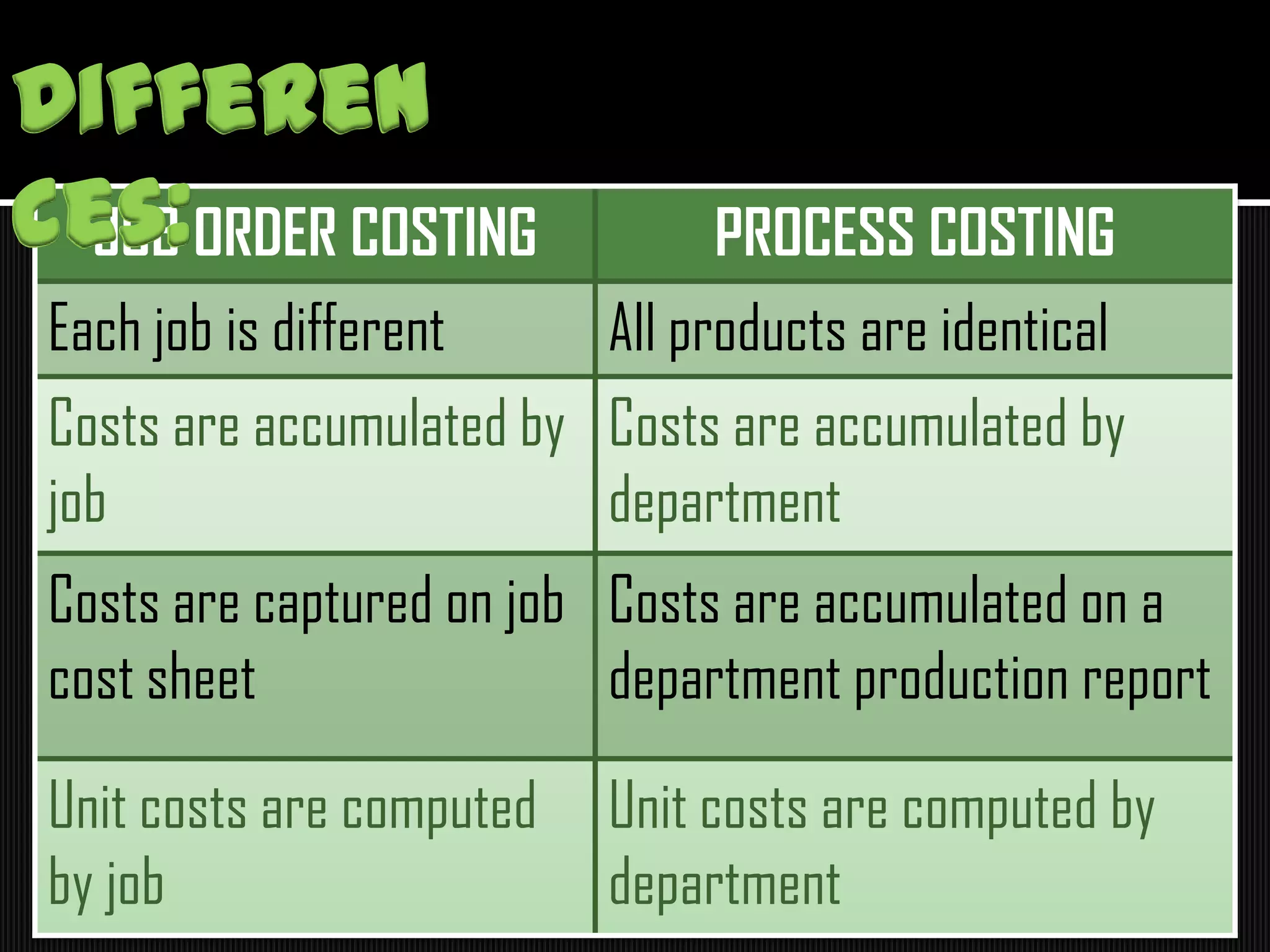

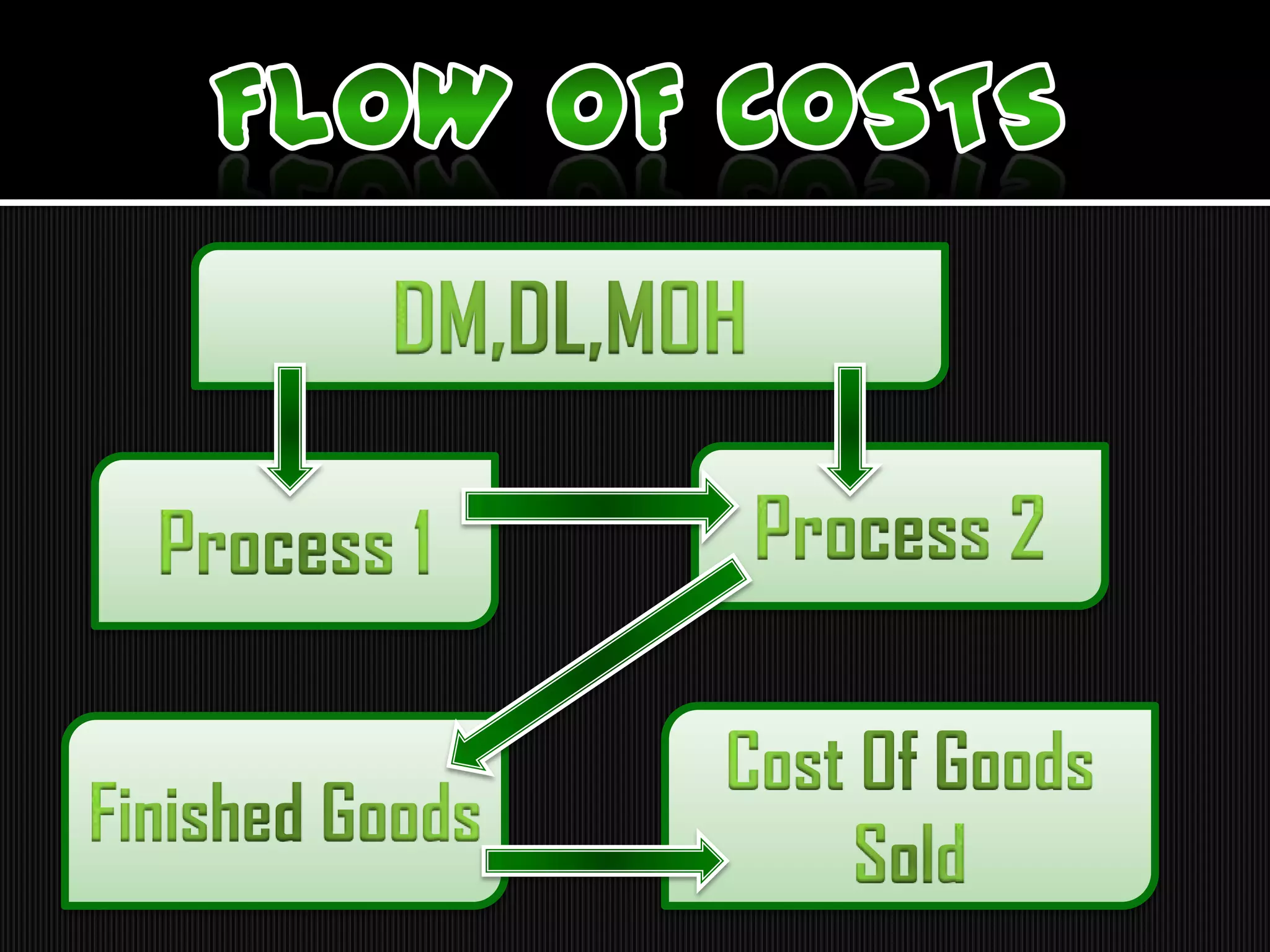

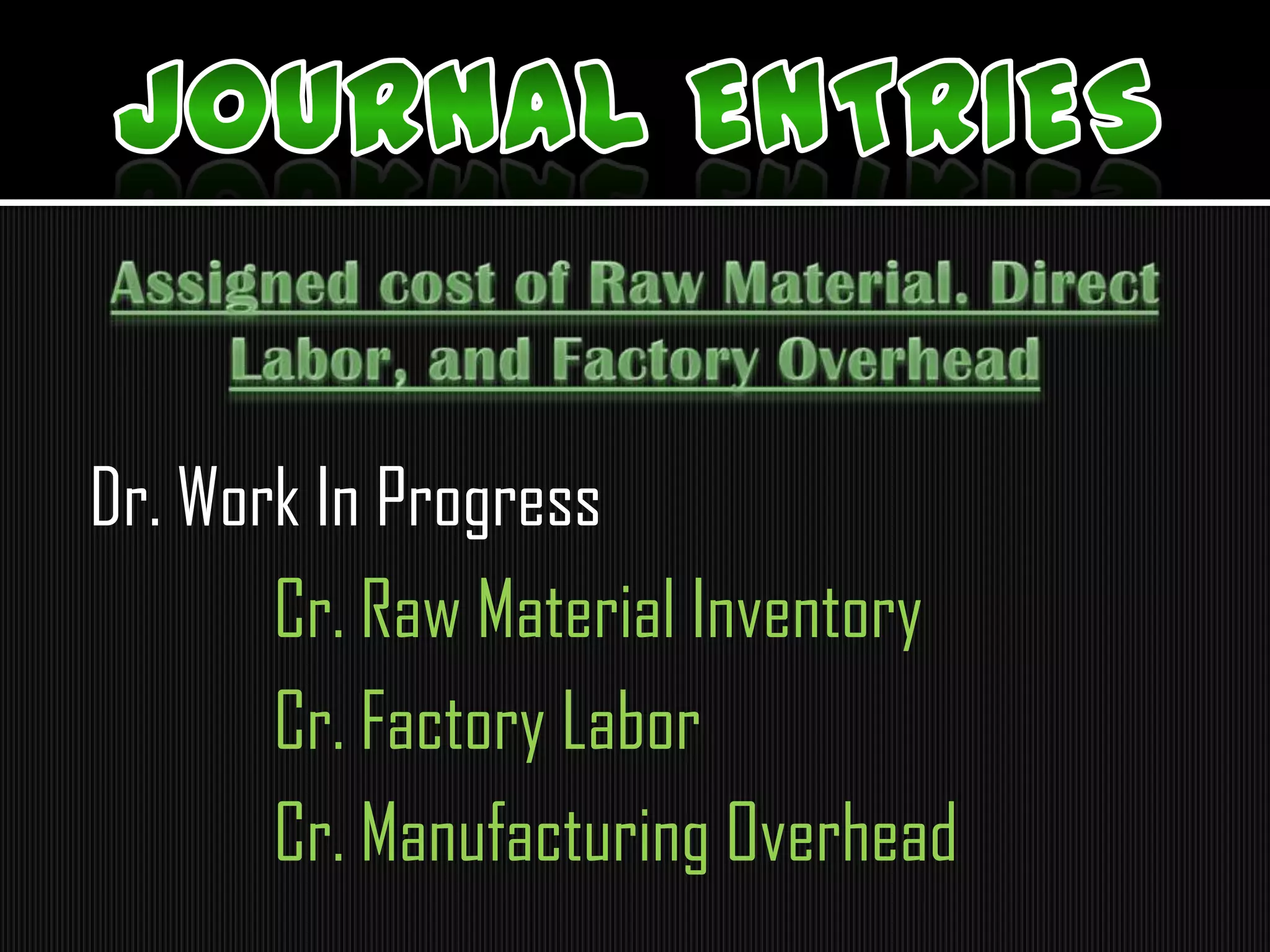

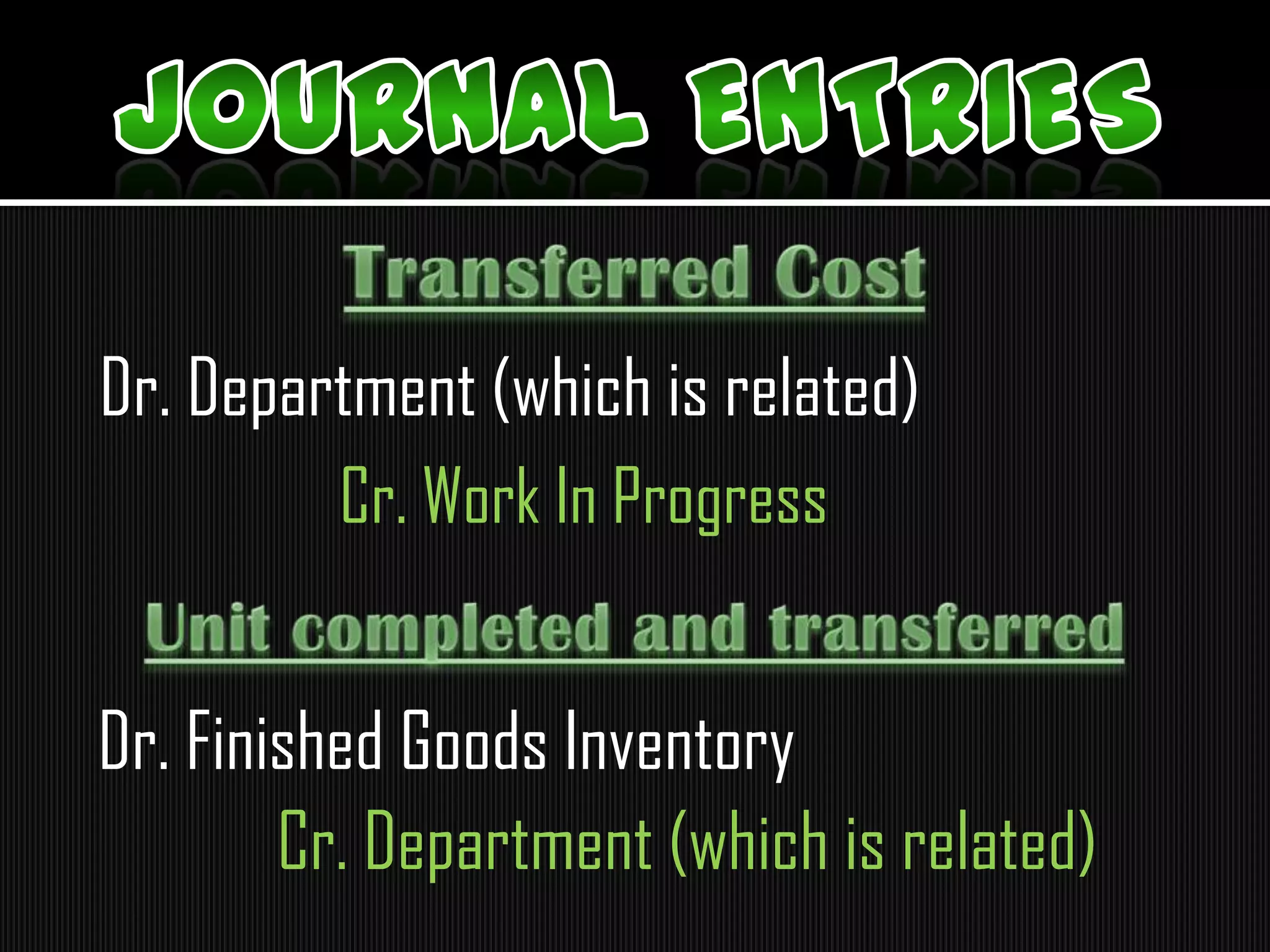

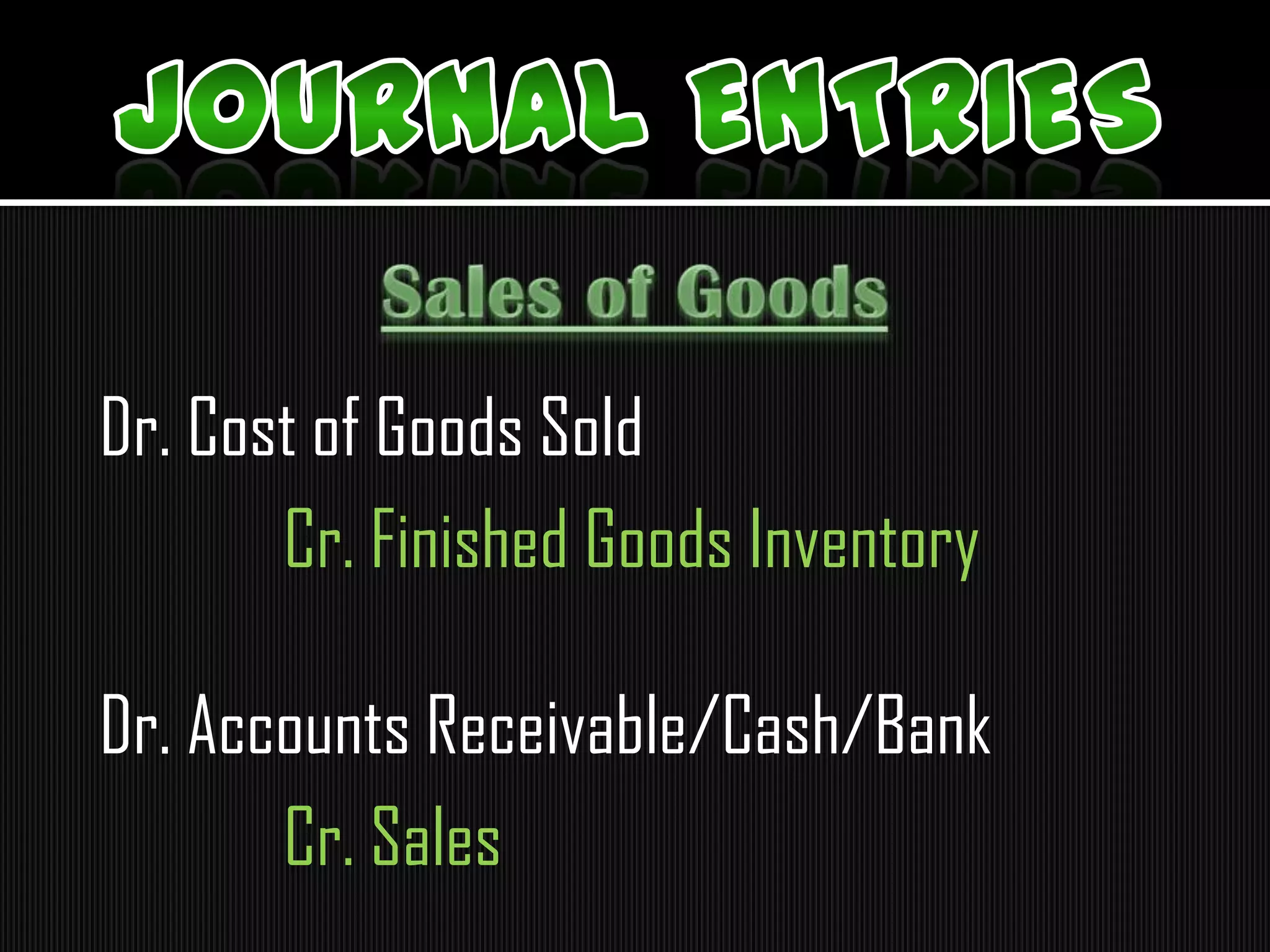

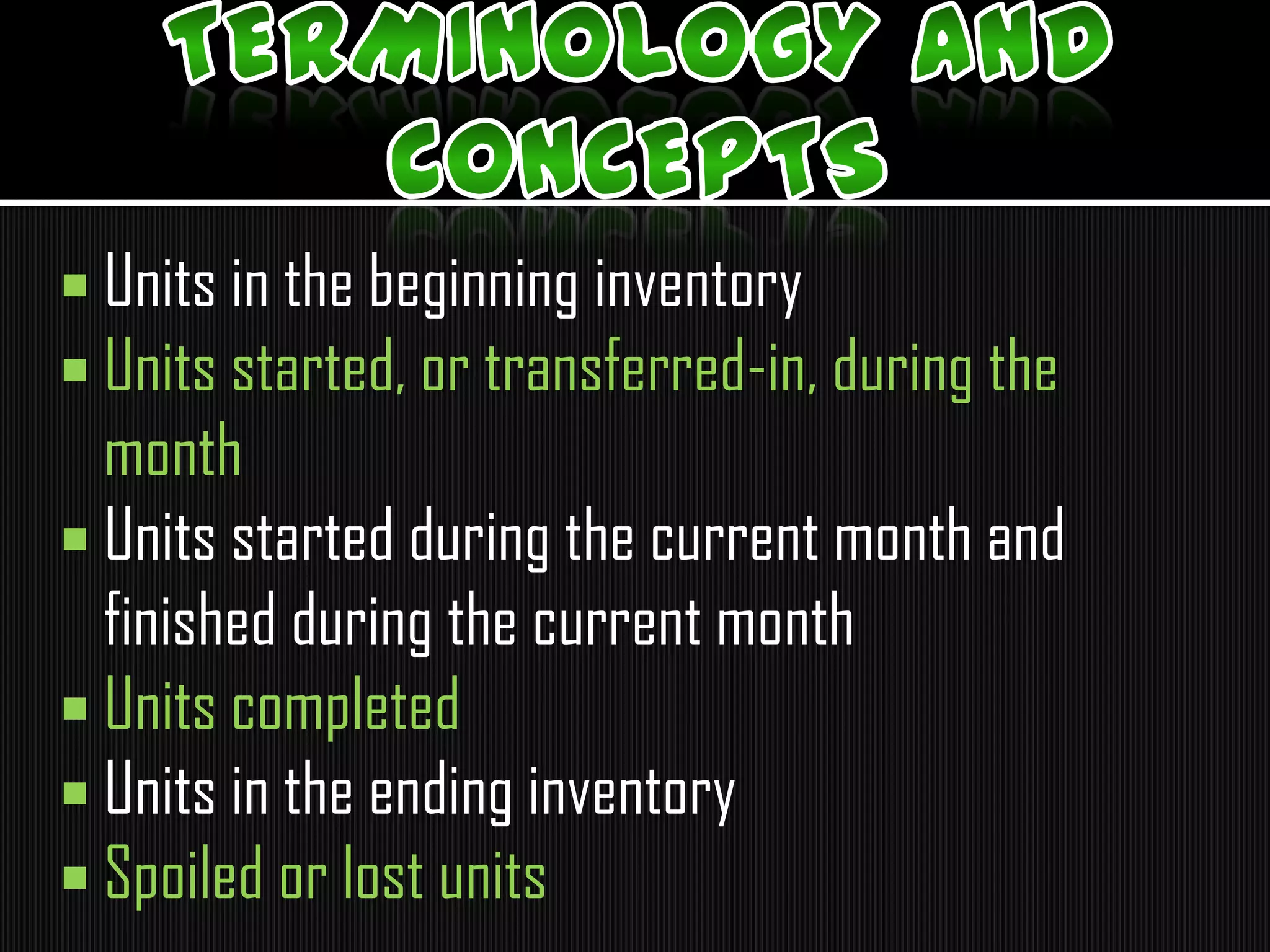

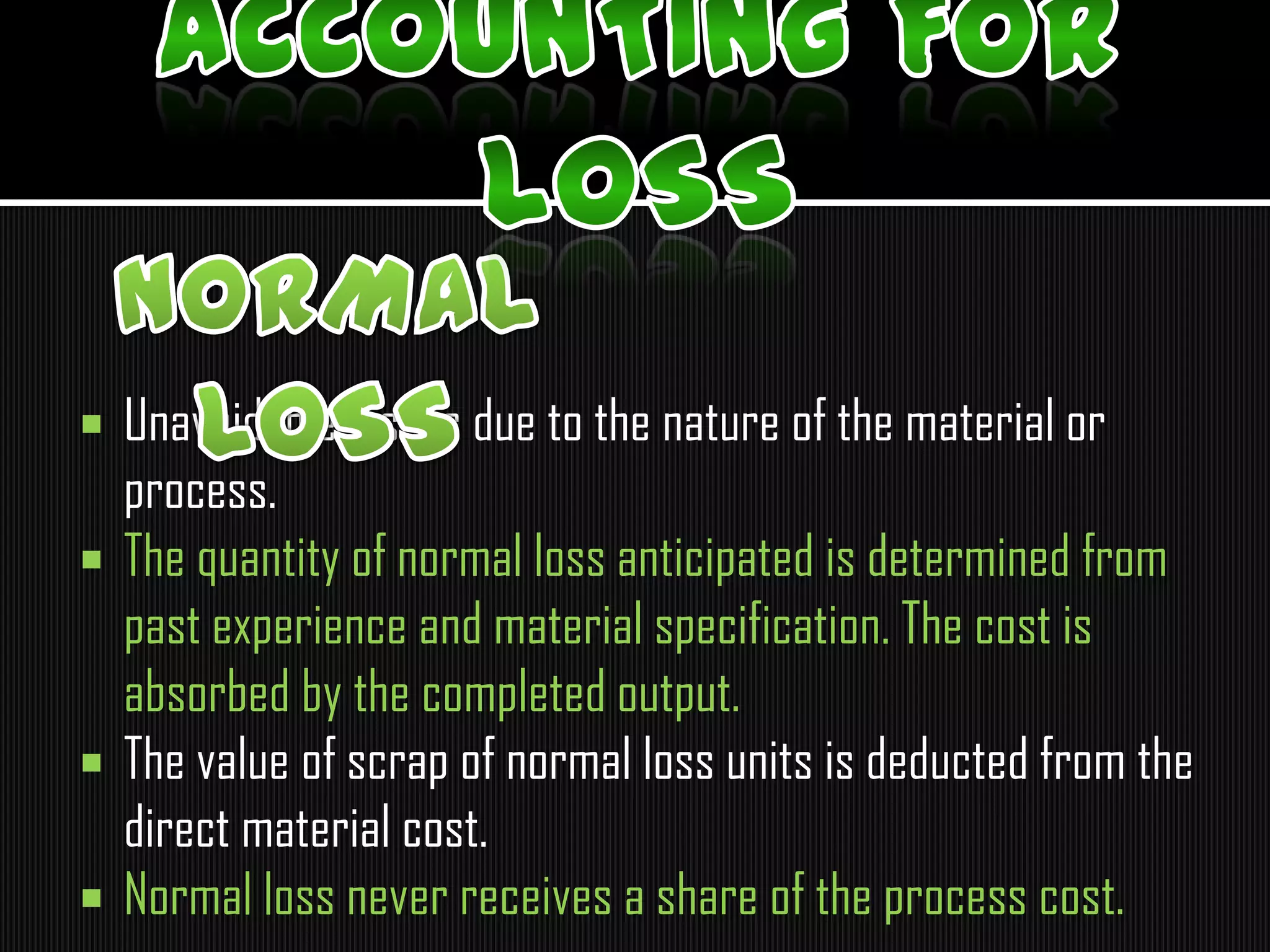

The document discusses key aspects of process costing, including: - Process costing is used when identical products are produced continuously through multiple stages. Costs are accumulated by department rather than by individual job. - Units are tracked as they move through each department/process, including beginning inventory, units started/transferred, finished, and ending inventory. - Normal losses that occur due to the production process are estimated and their costs are absorbed into finished units, while abnormal losses are treated as expenses.