Downloaded 47 times

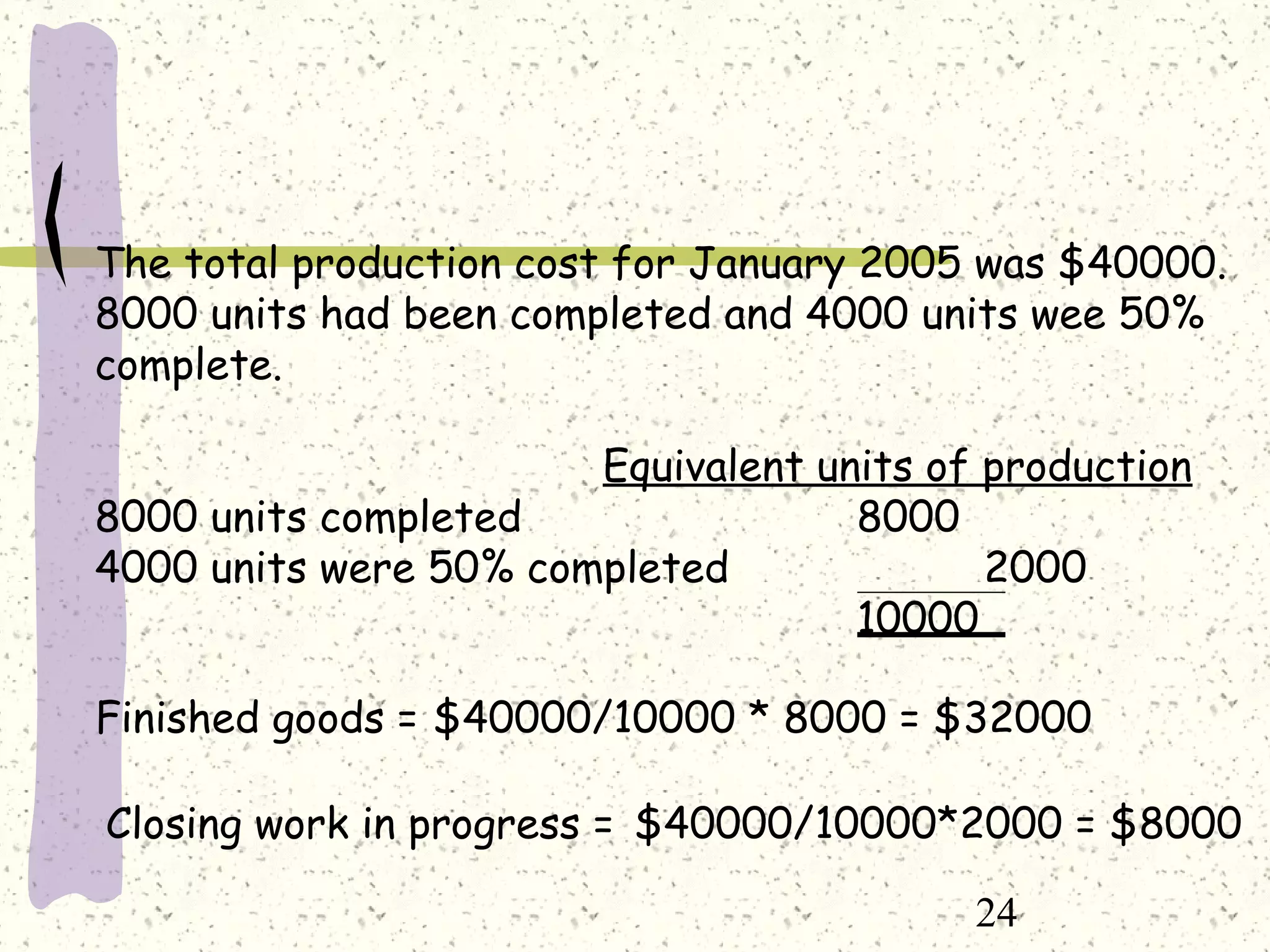

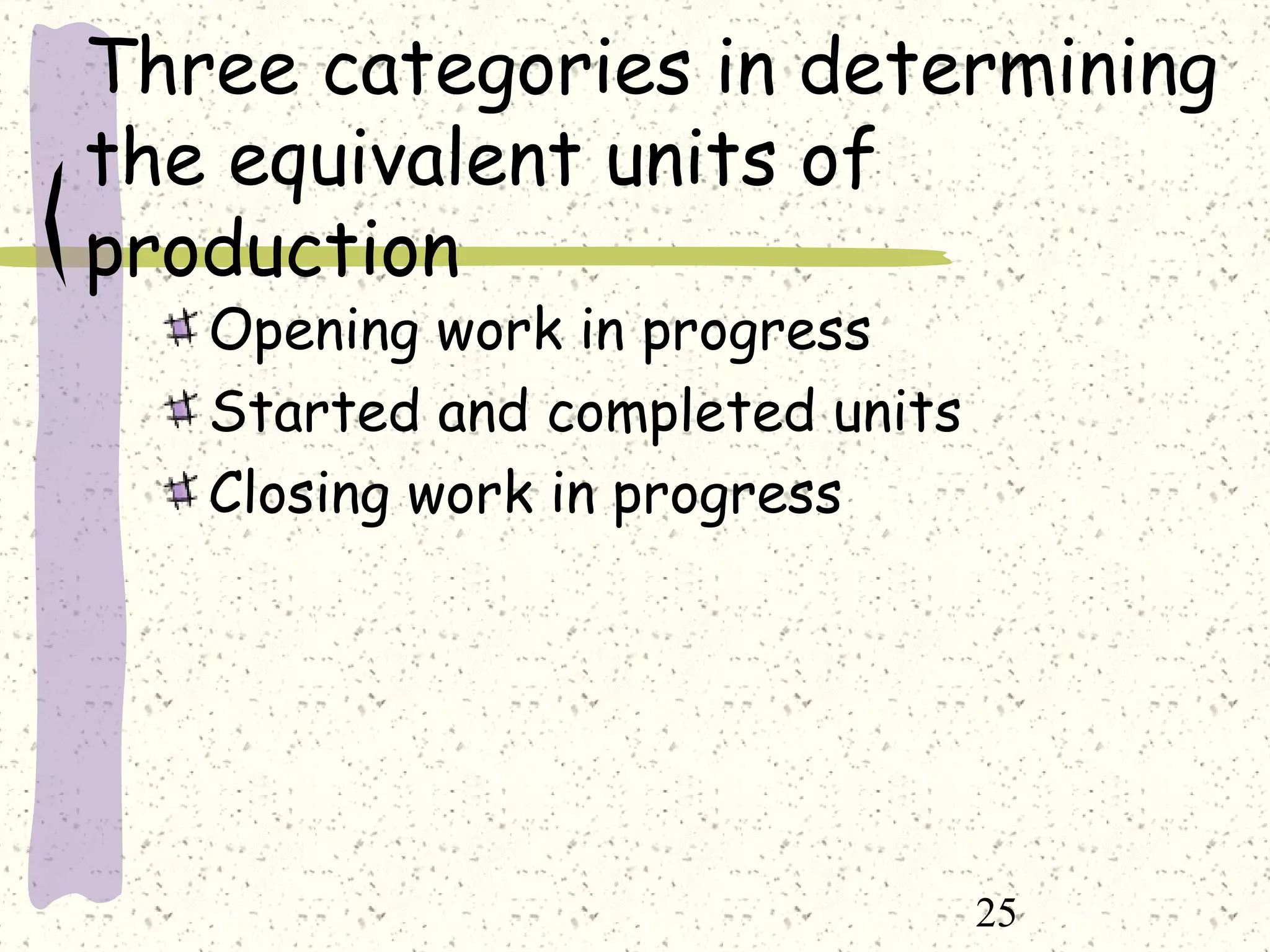

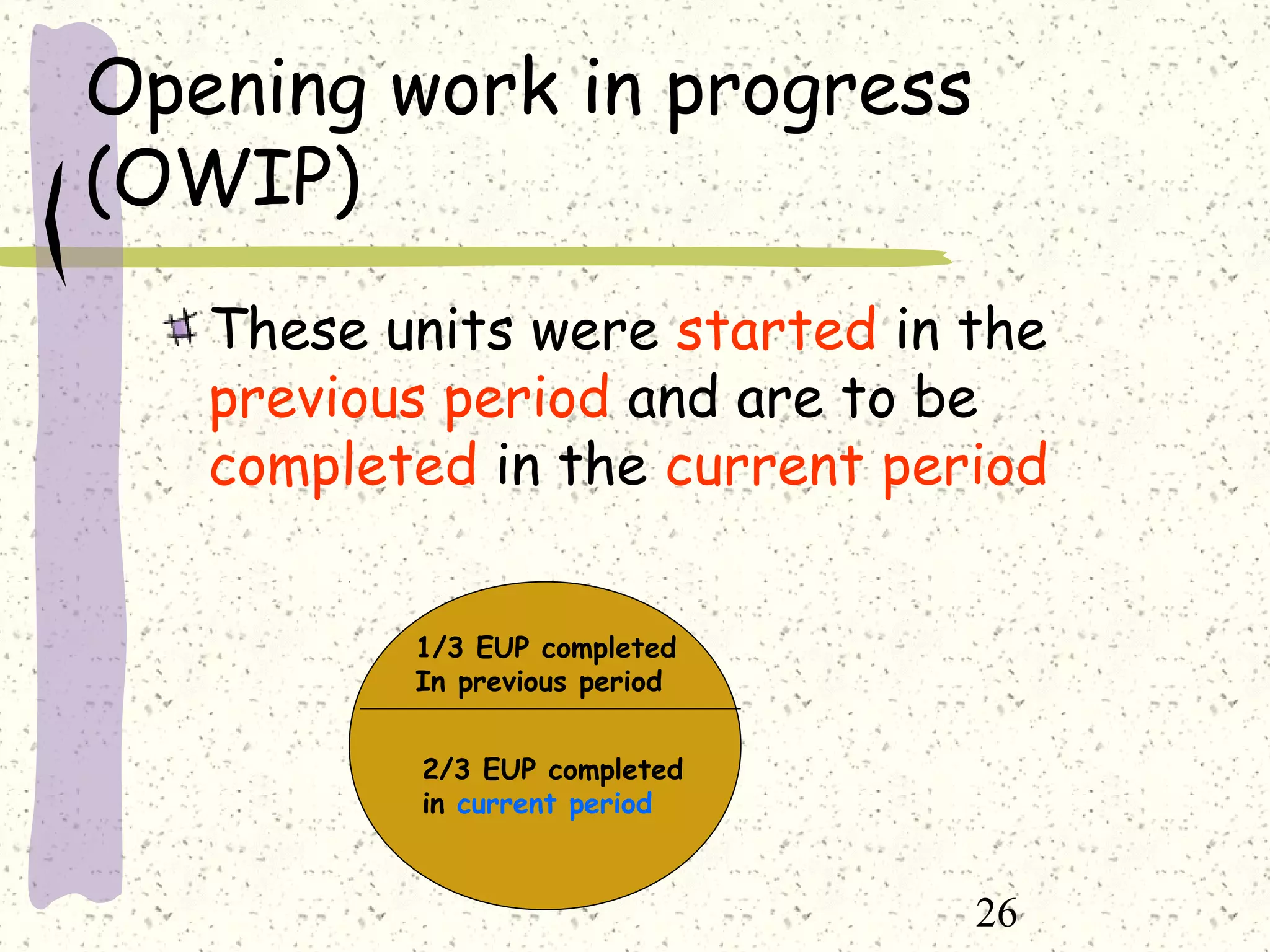

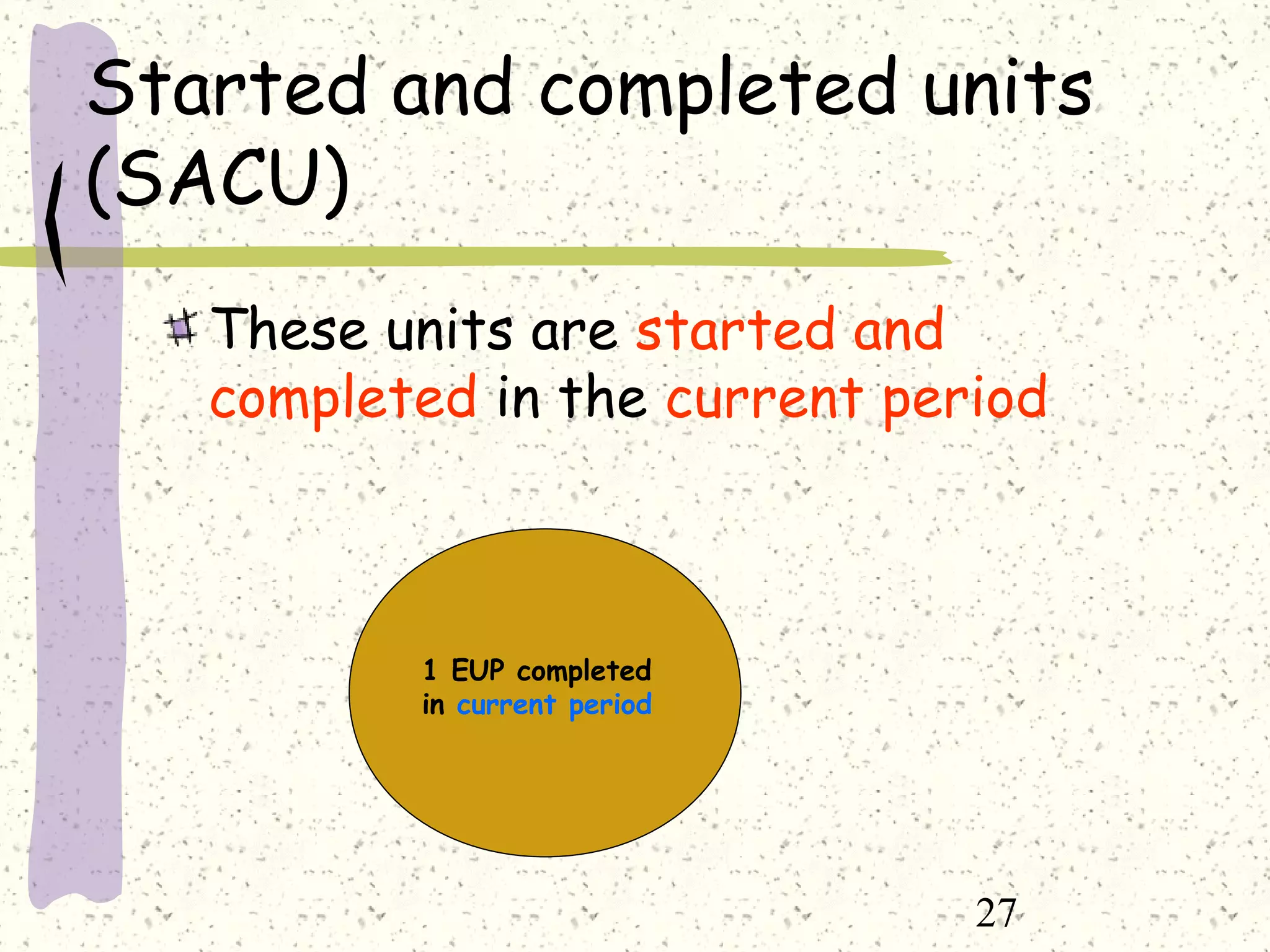

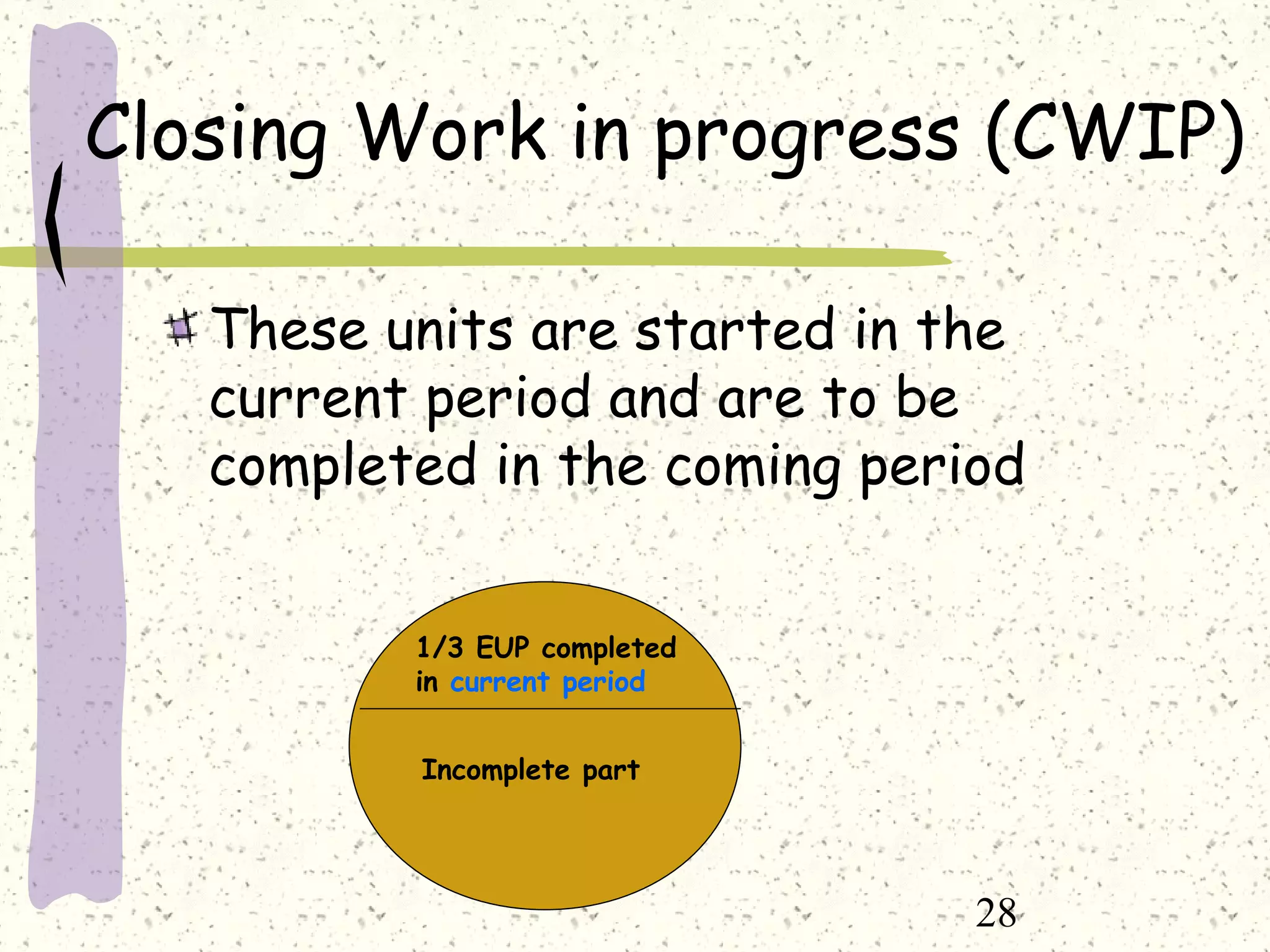

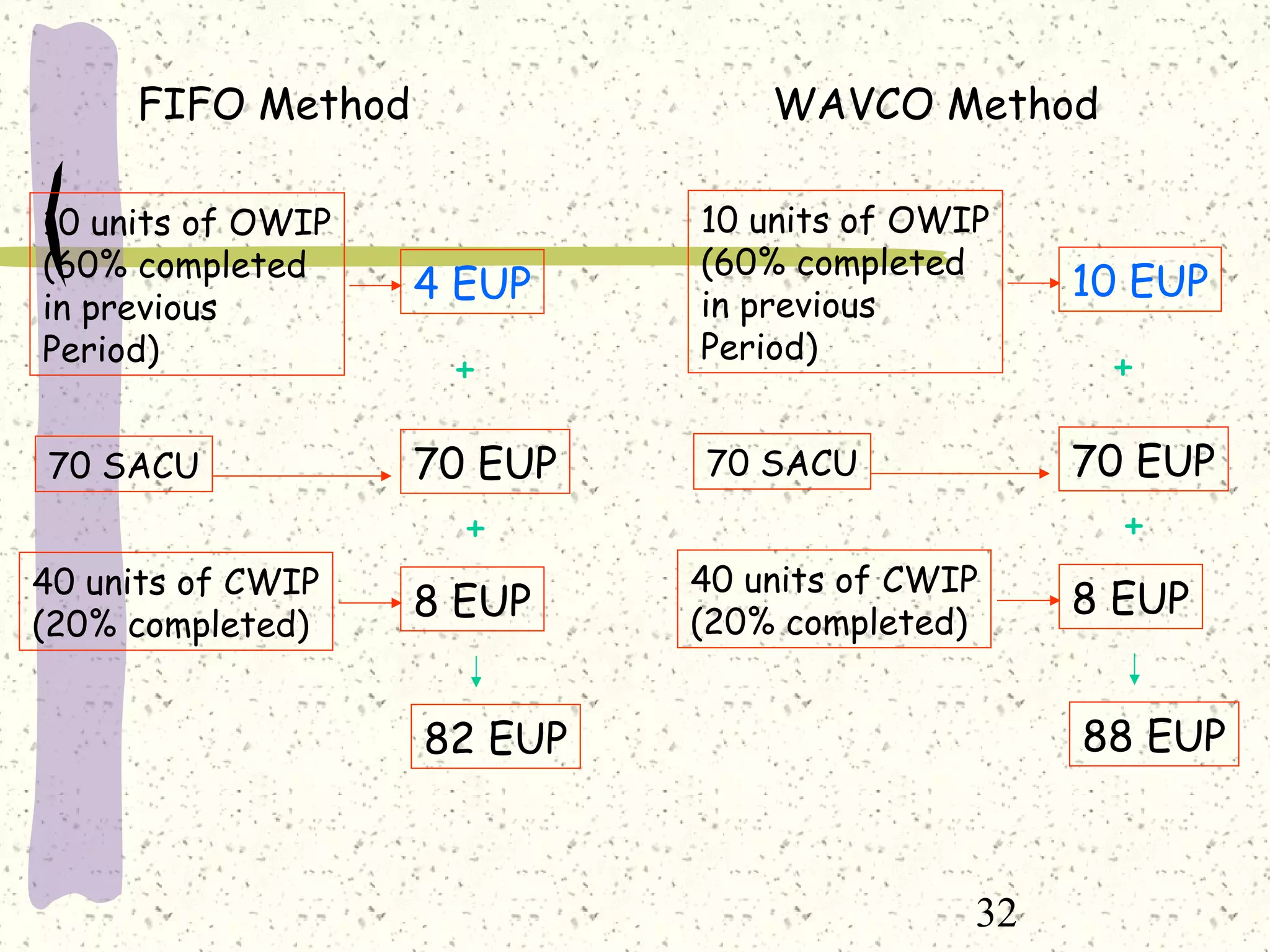

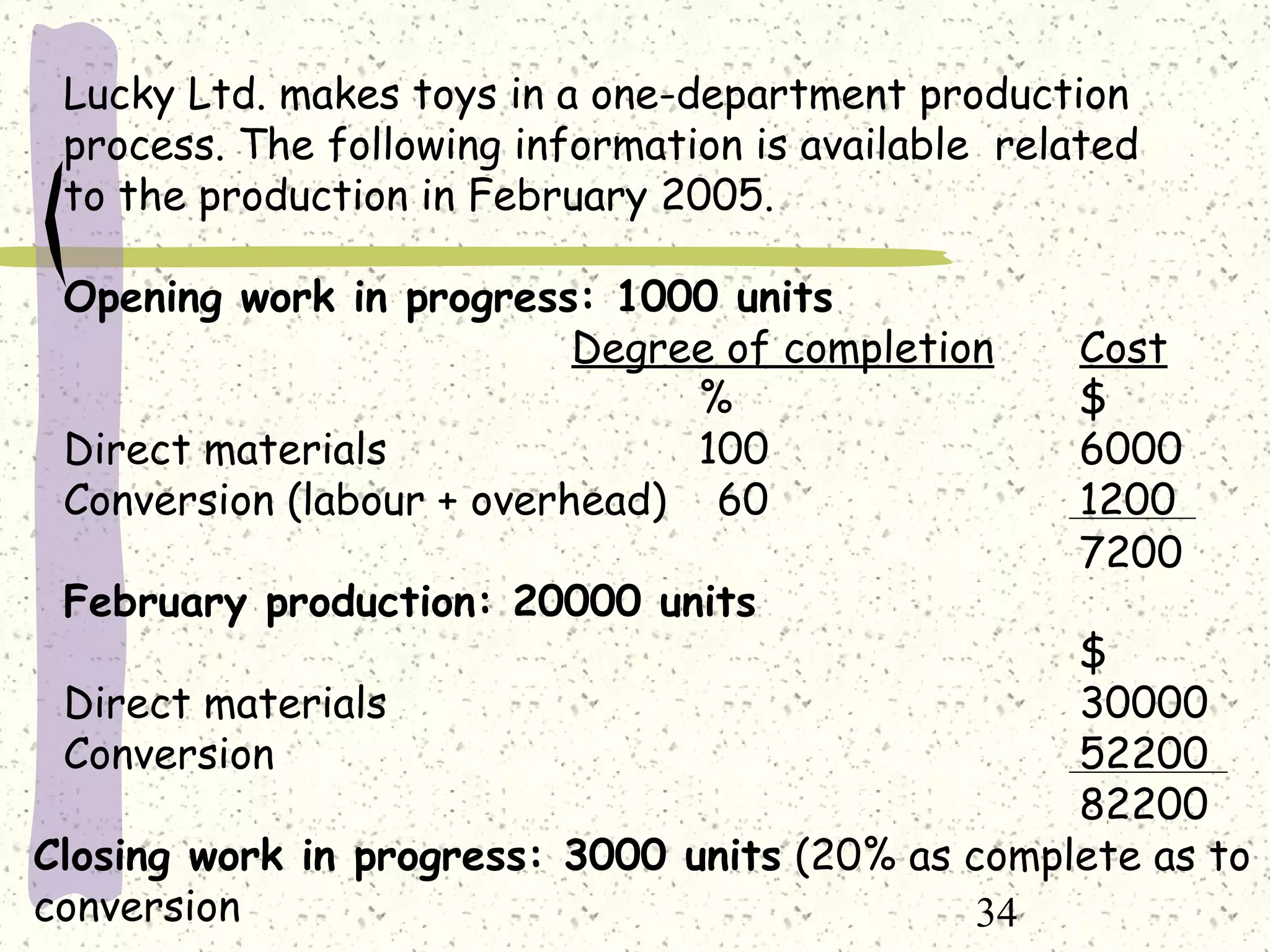

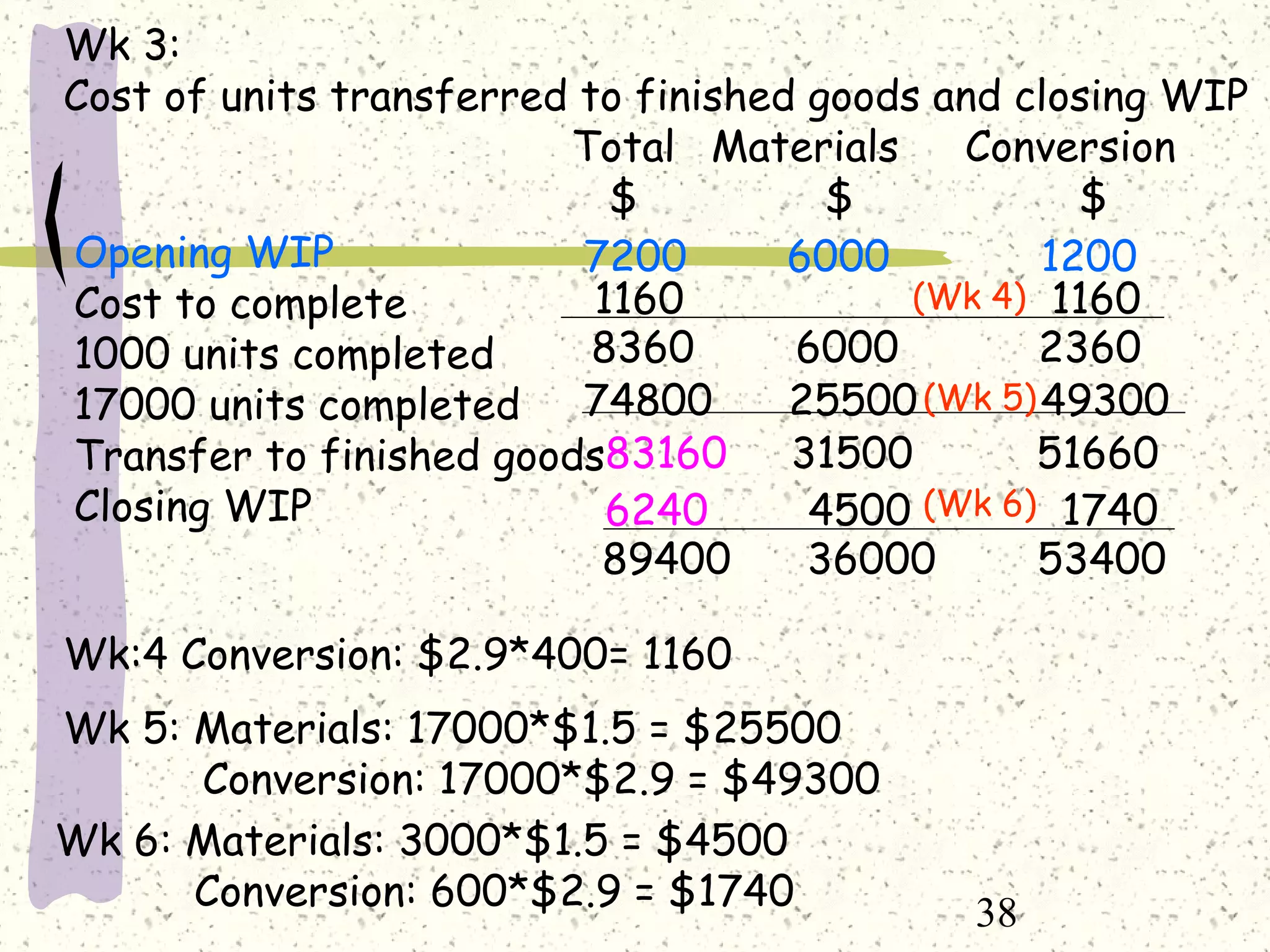

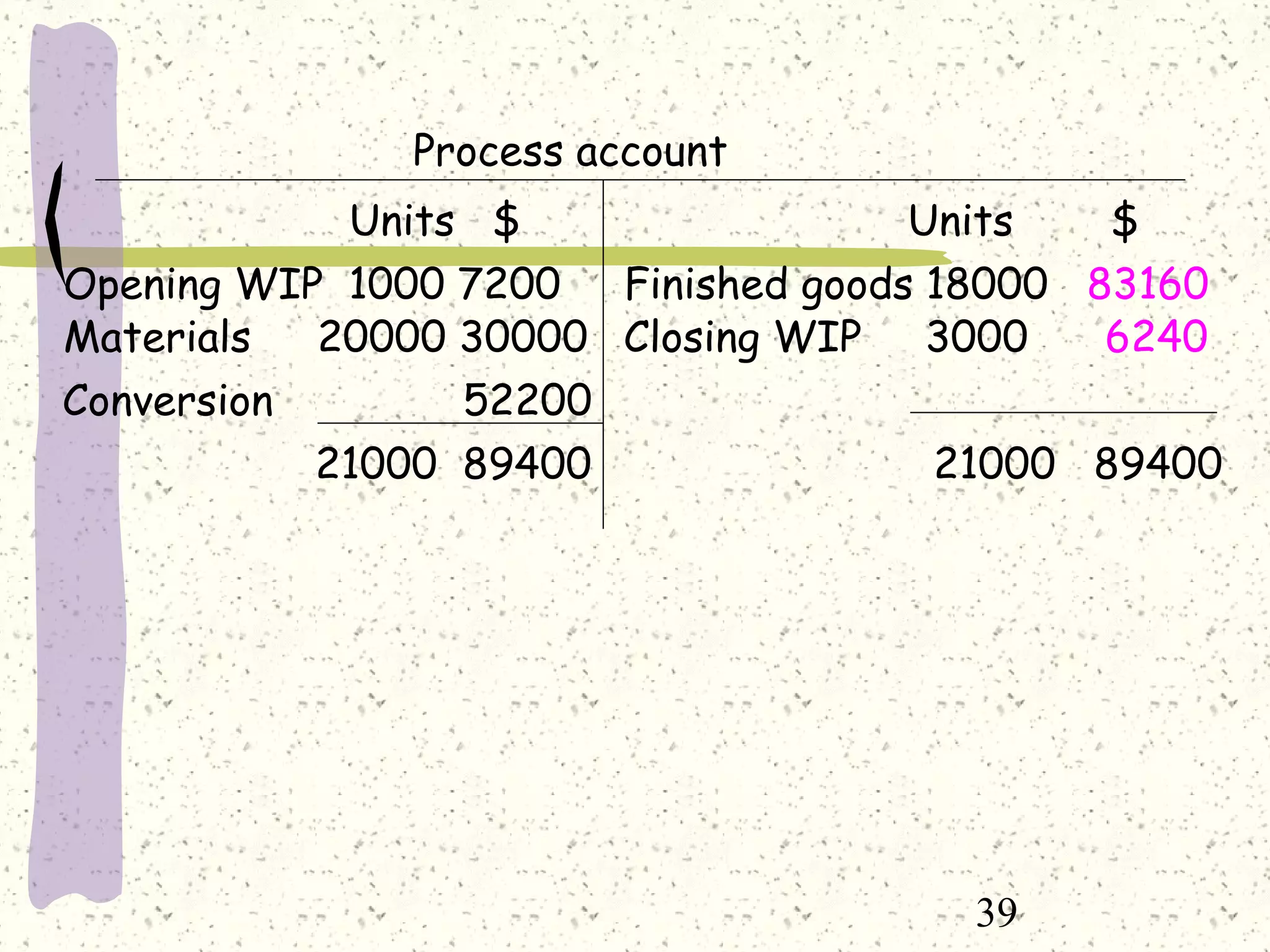

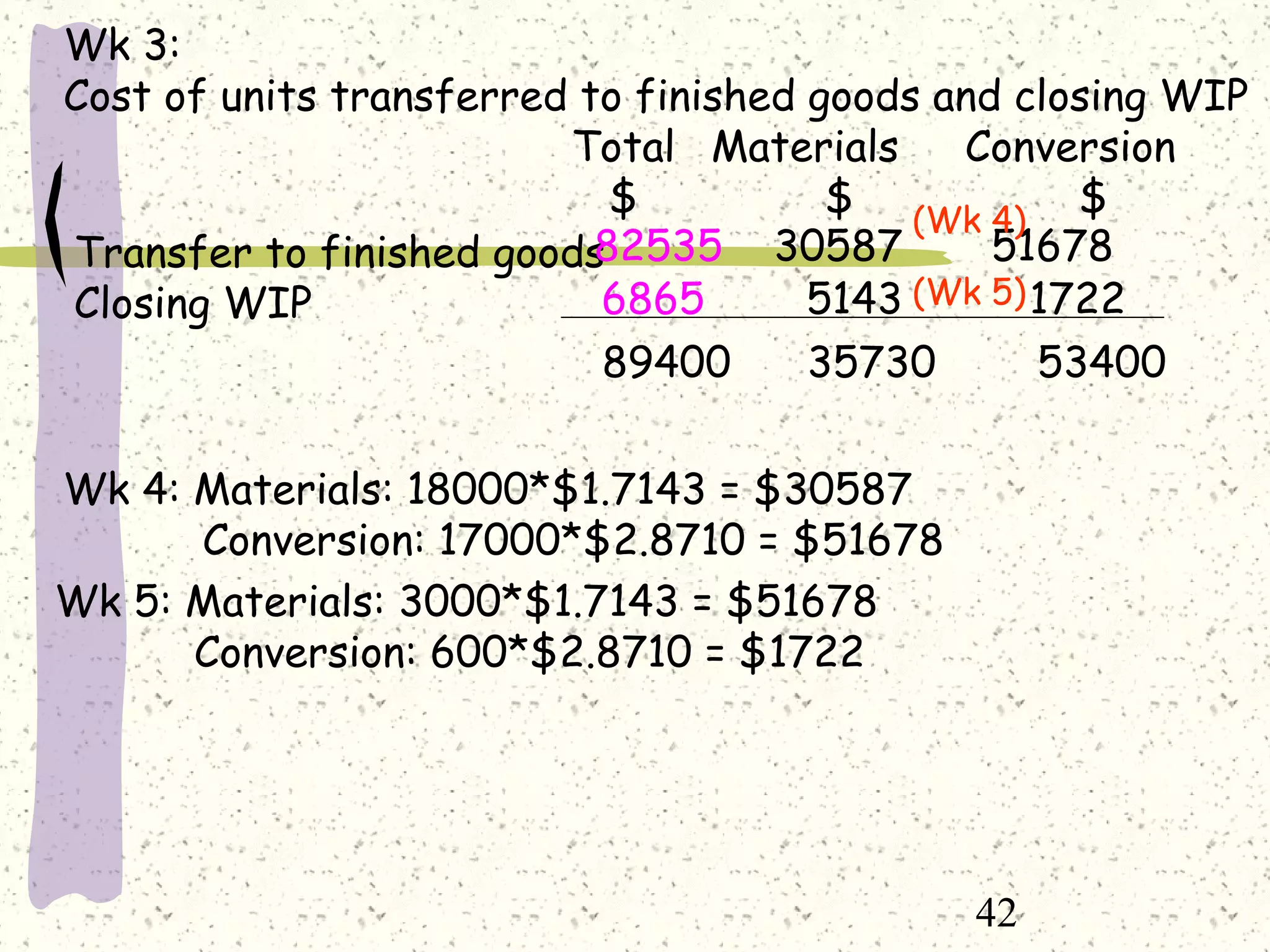

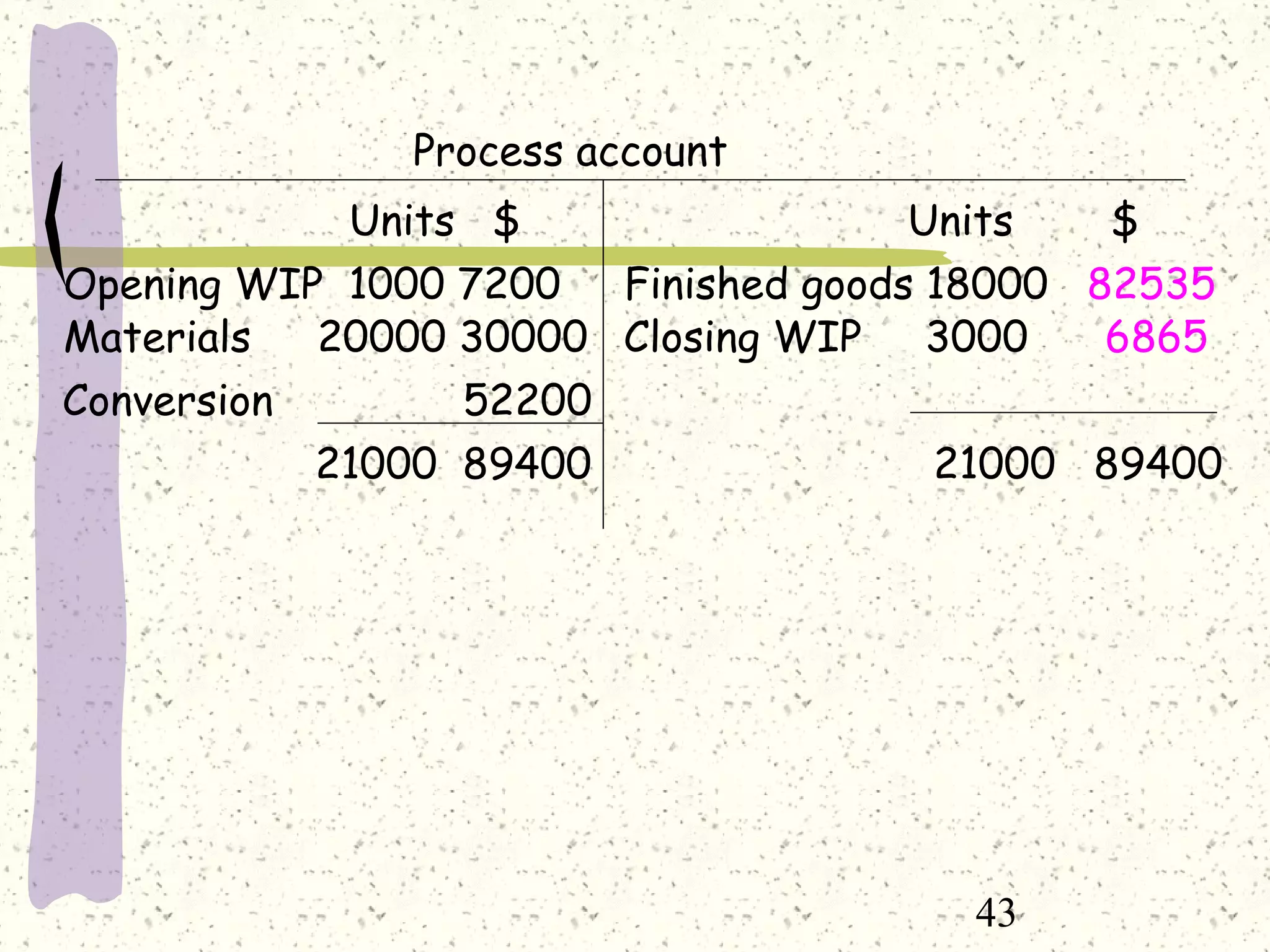

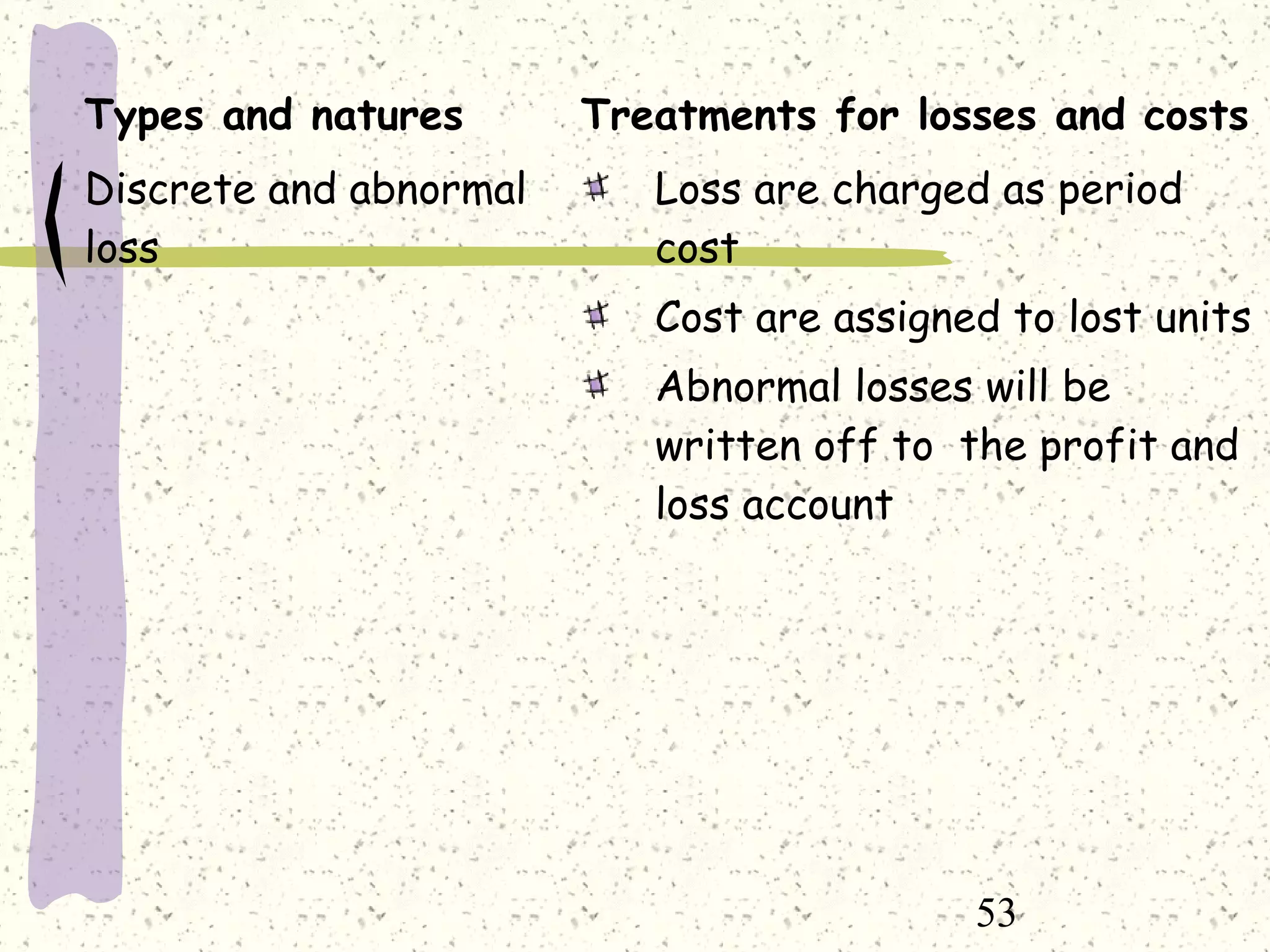

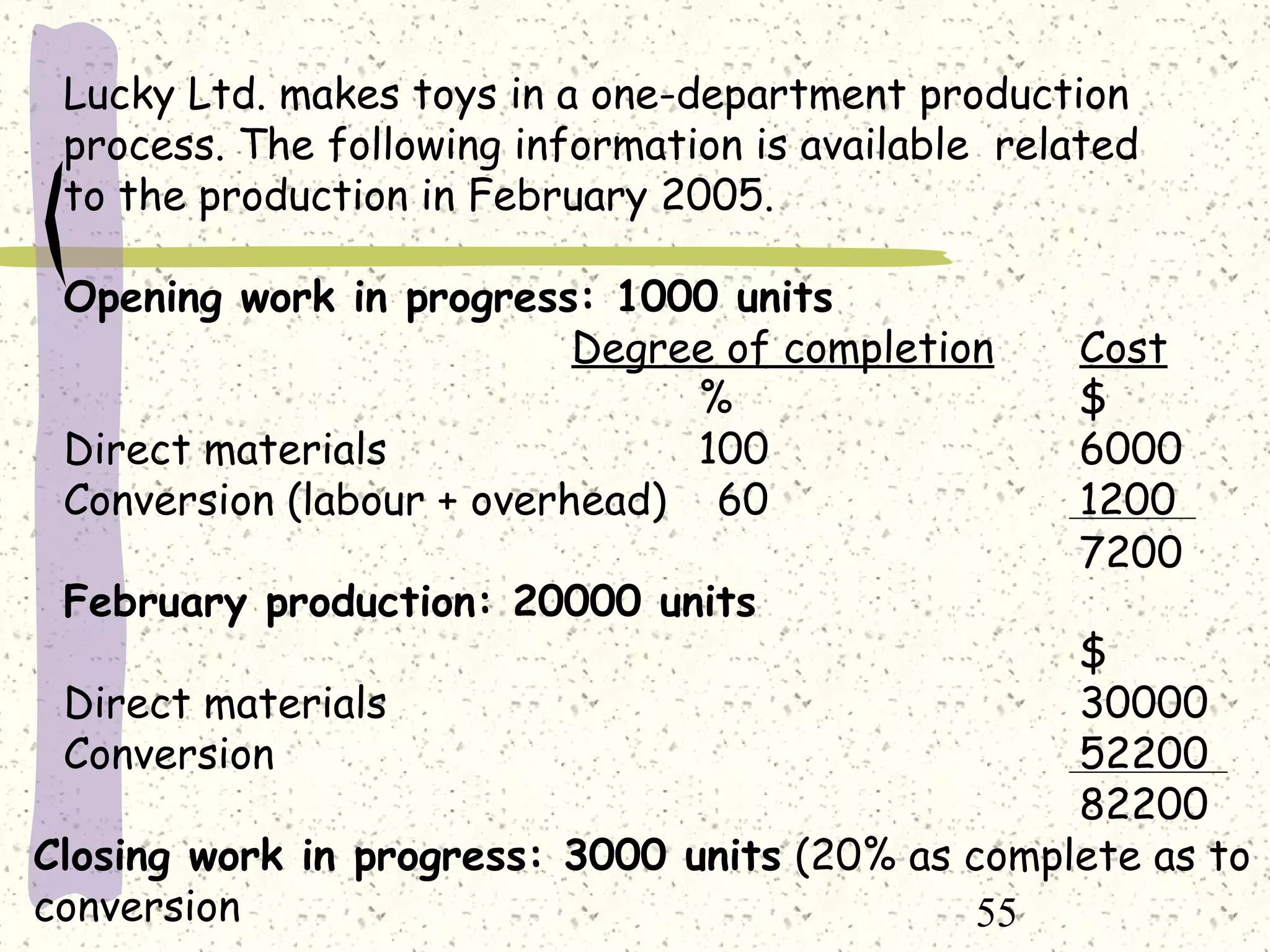

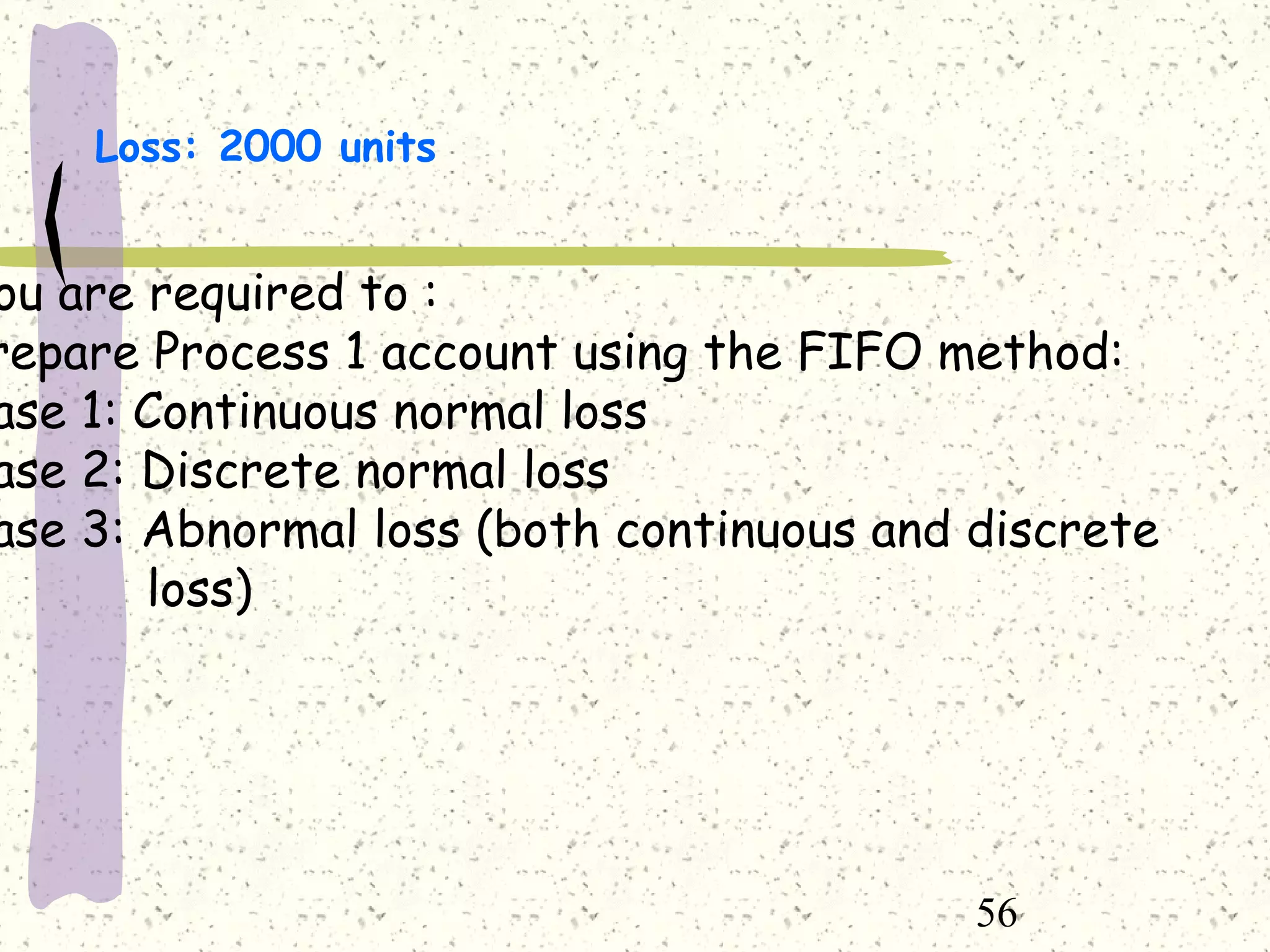

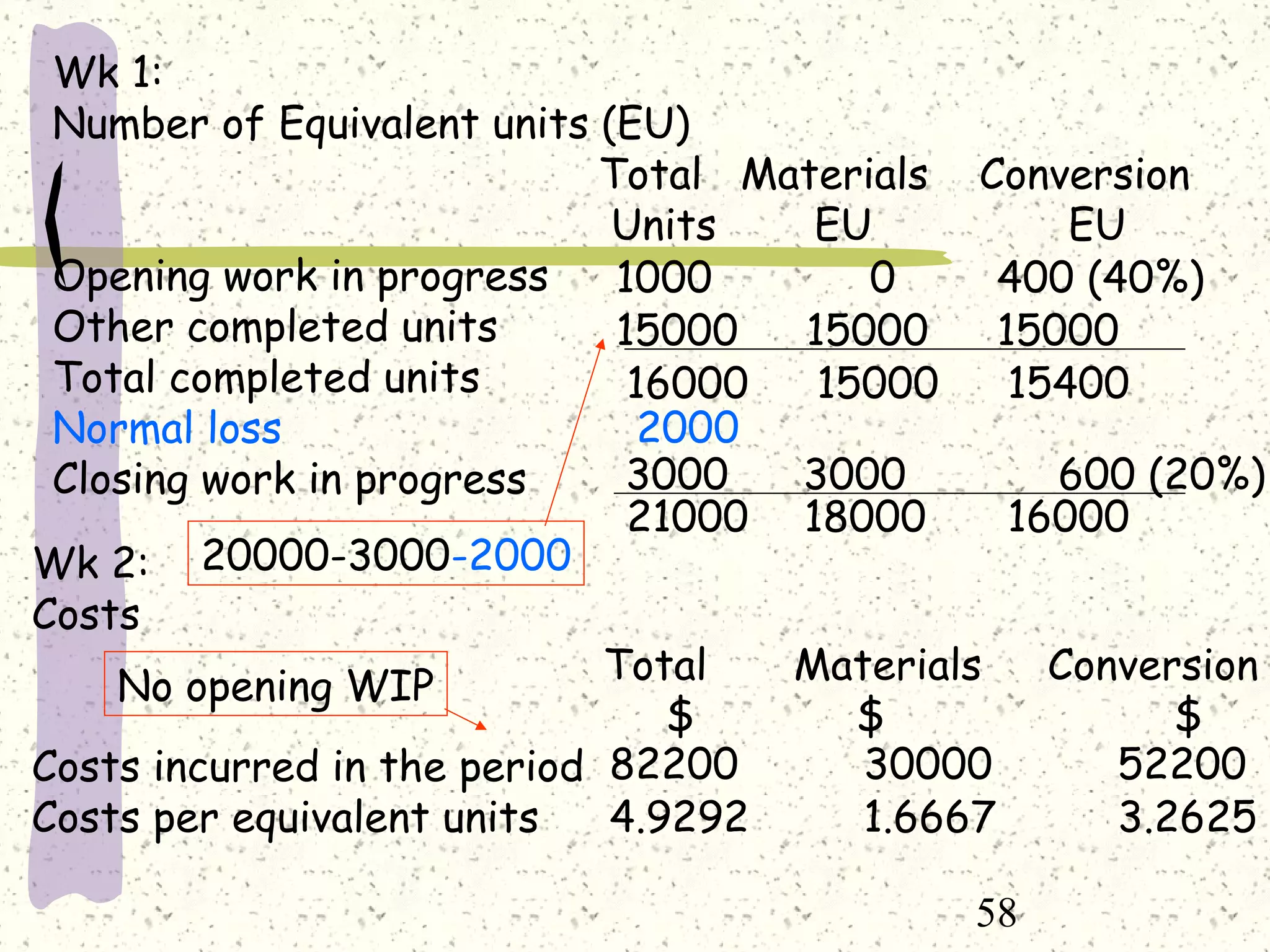

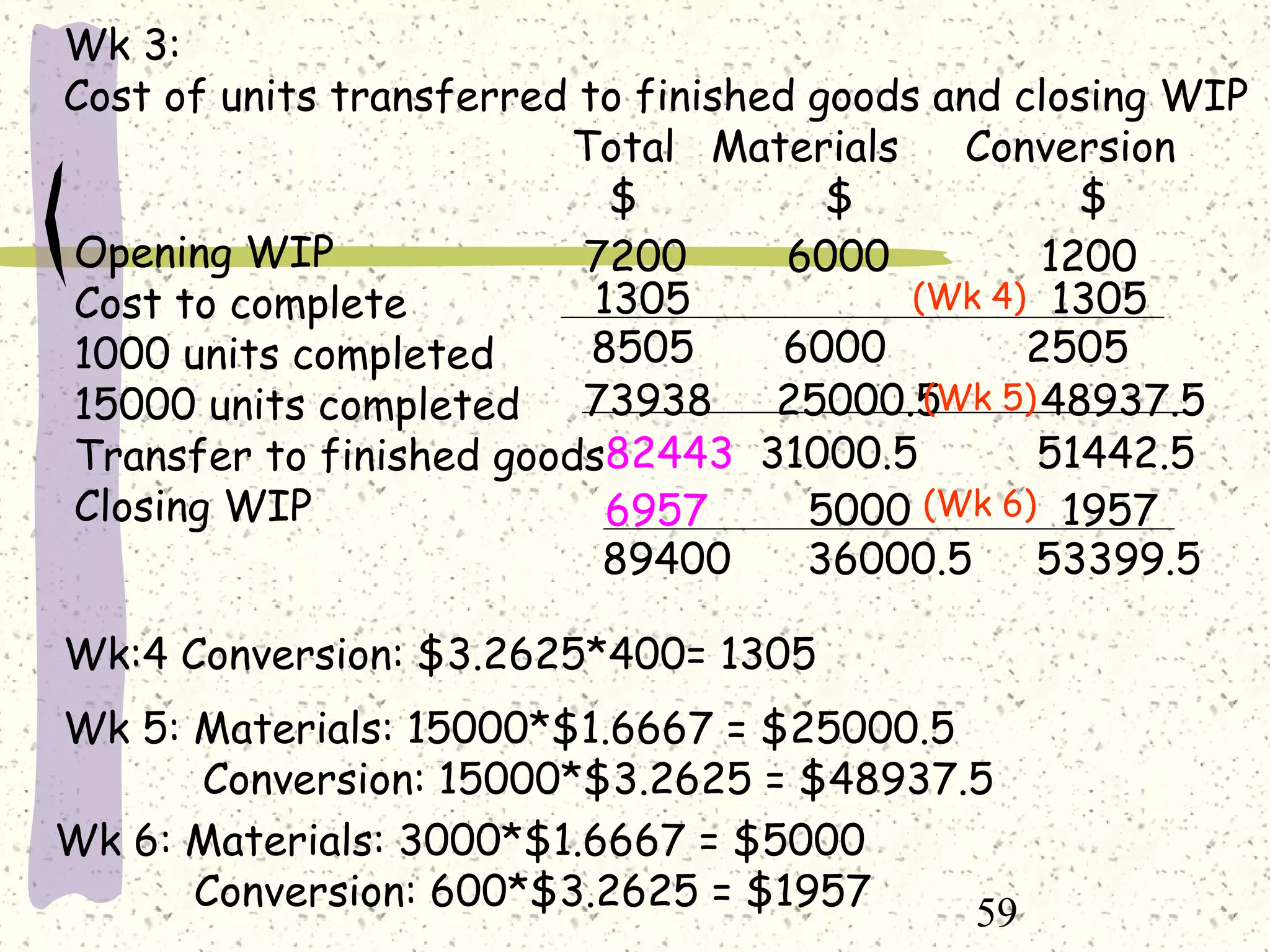

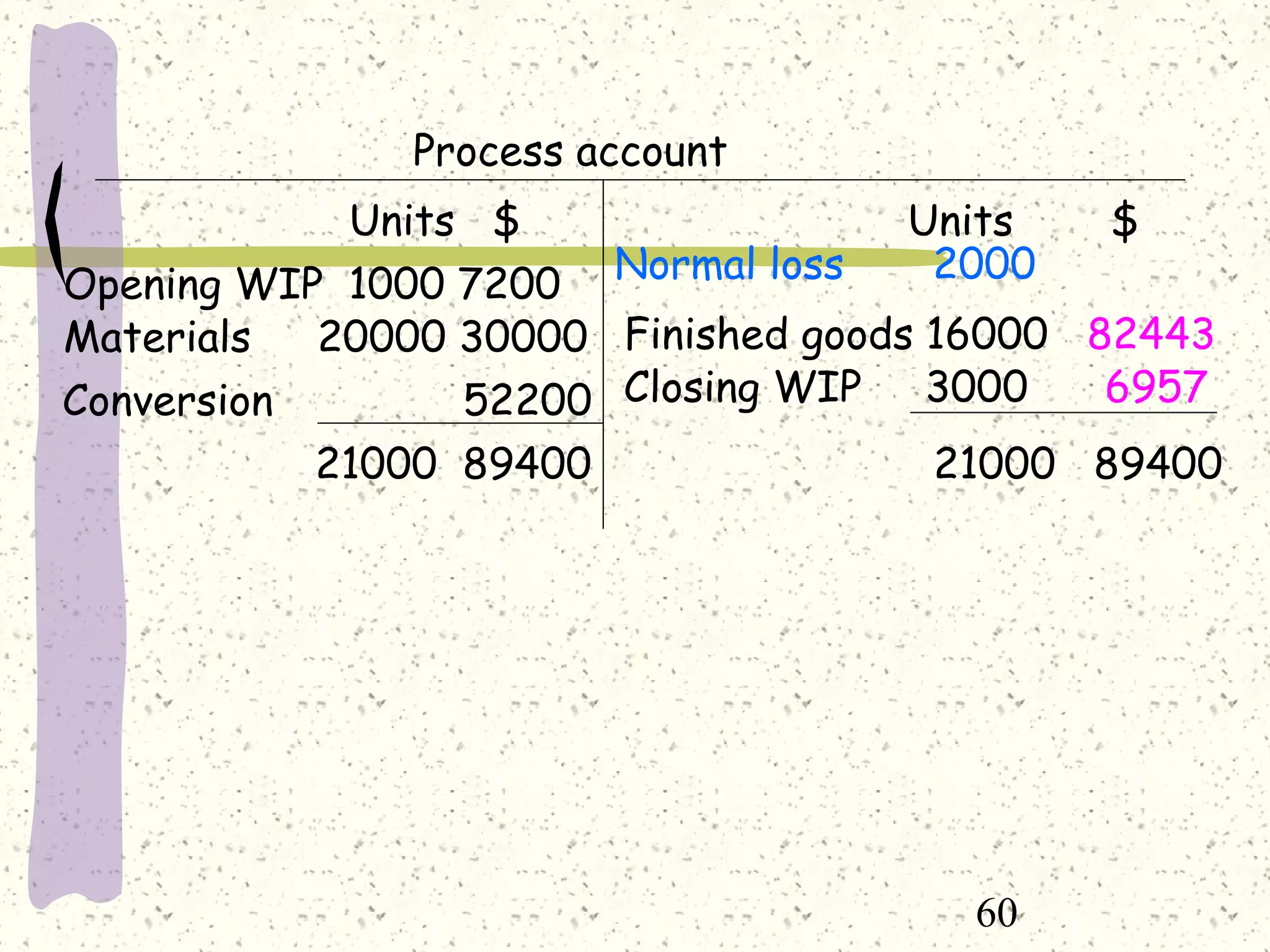

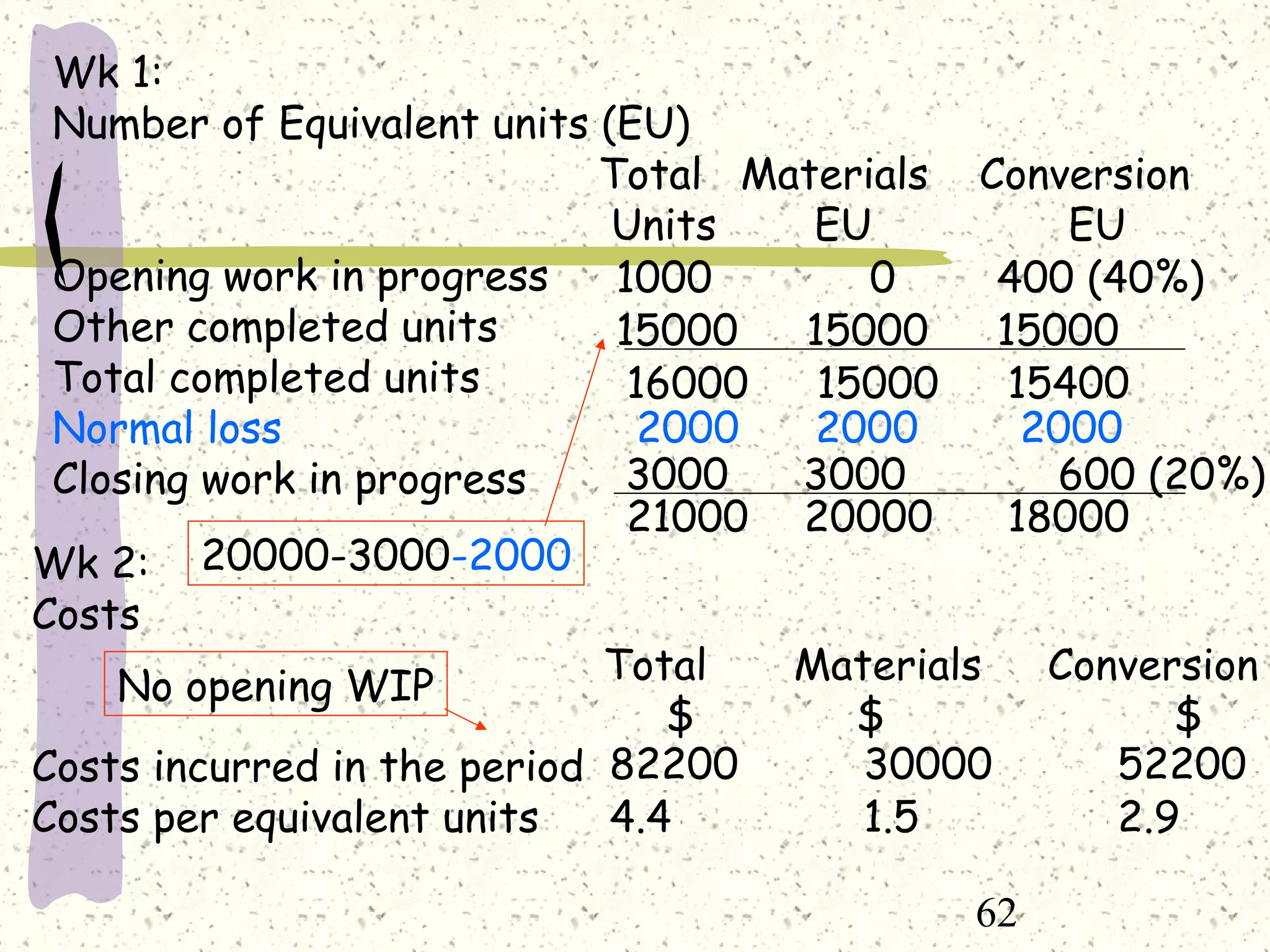

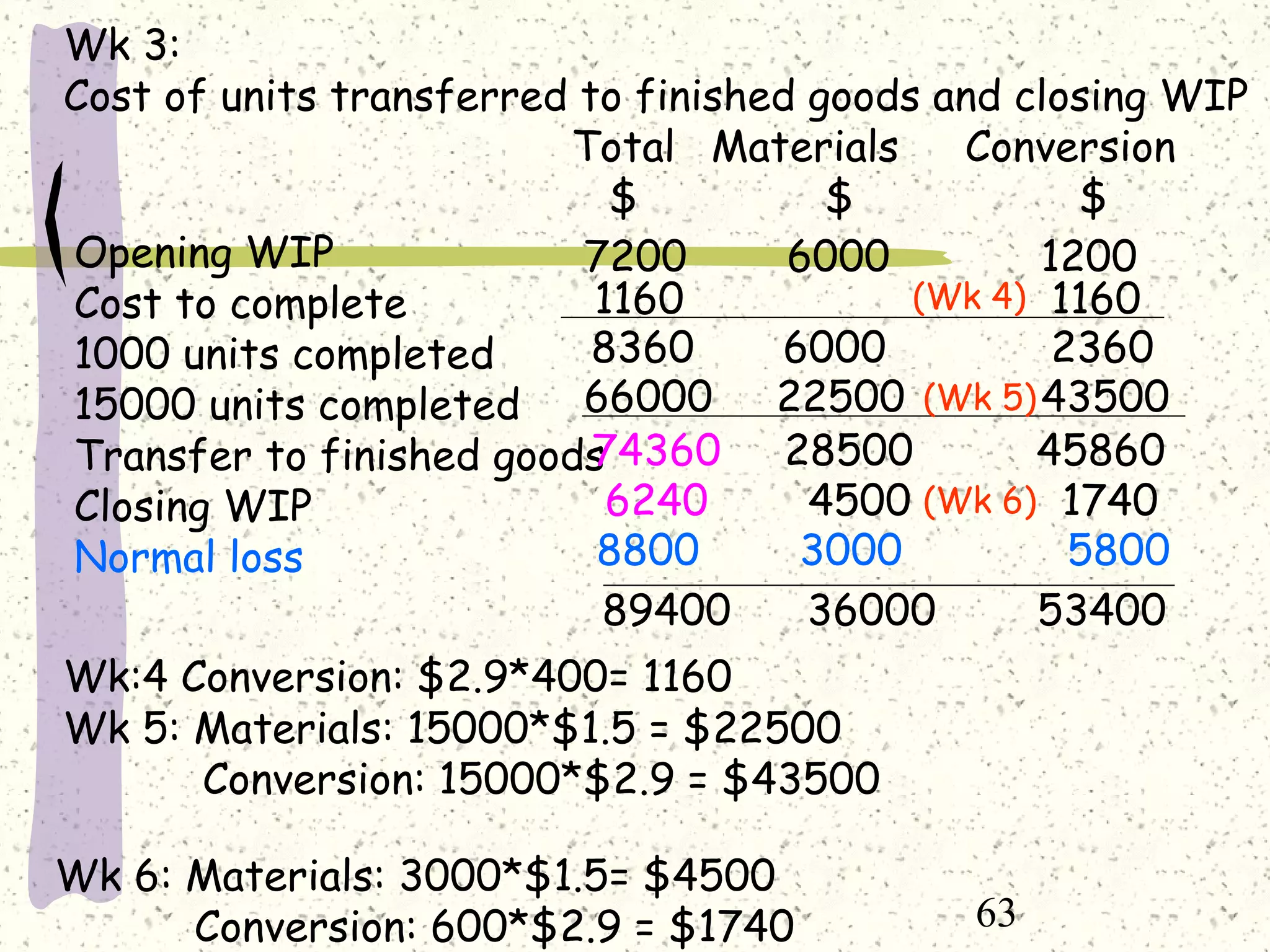

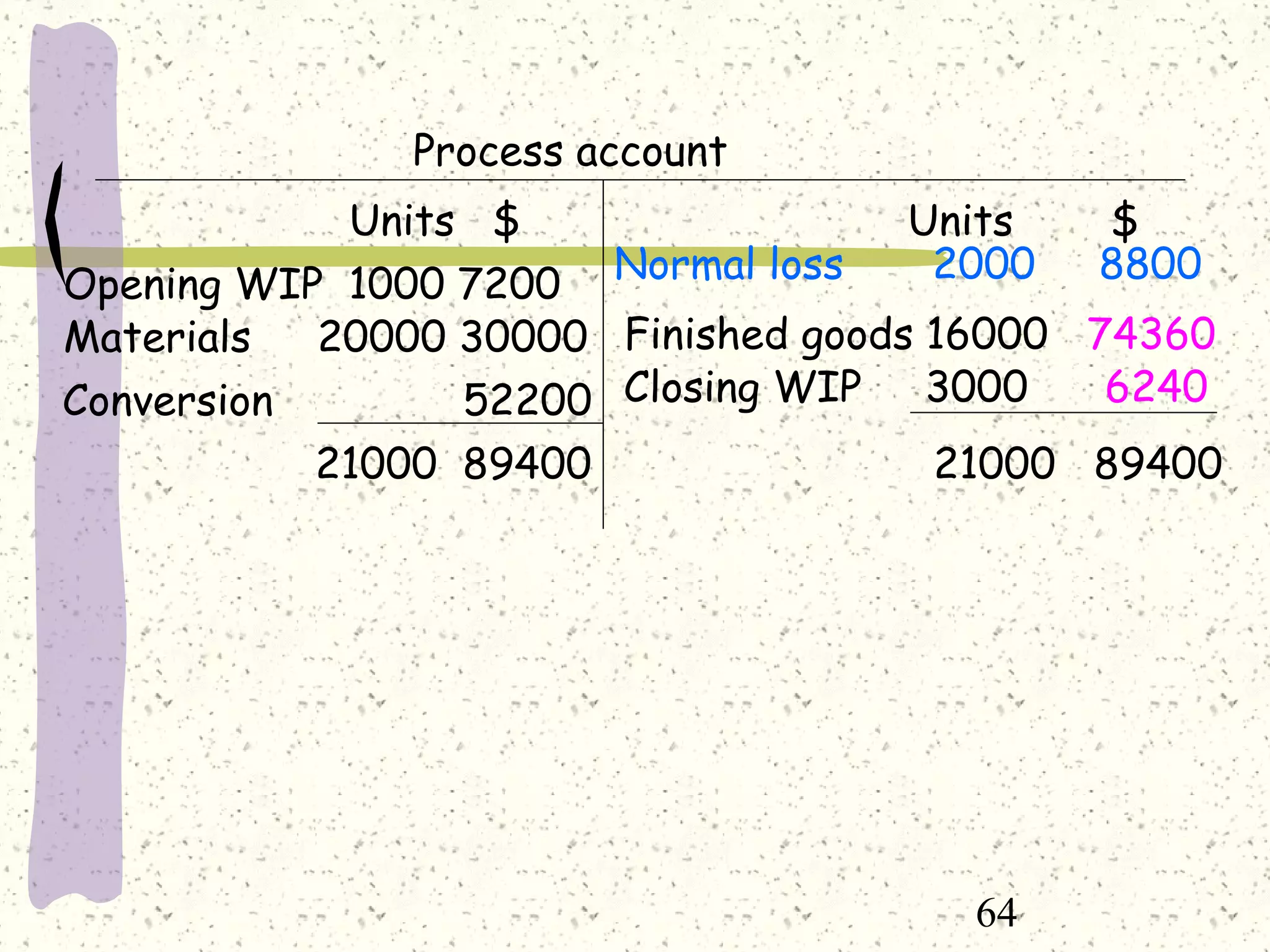

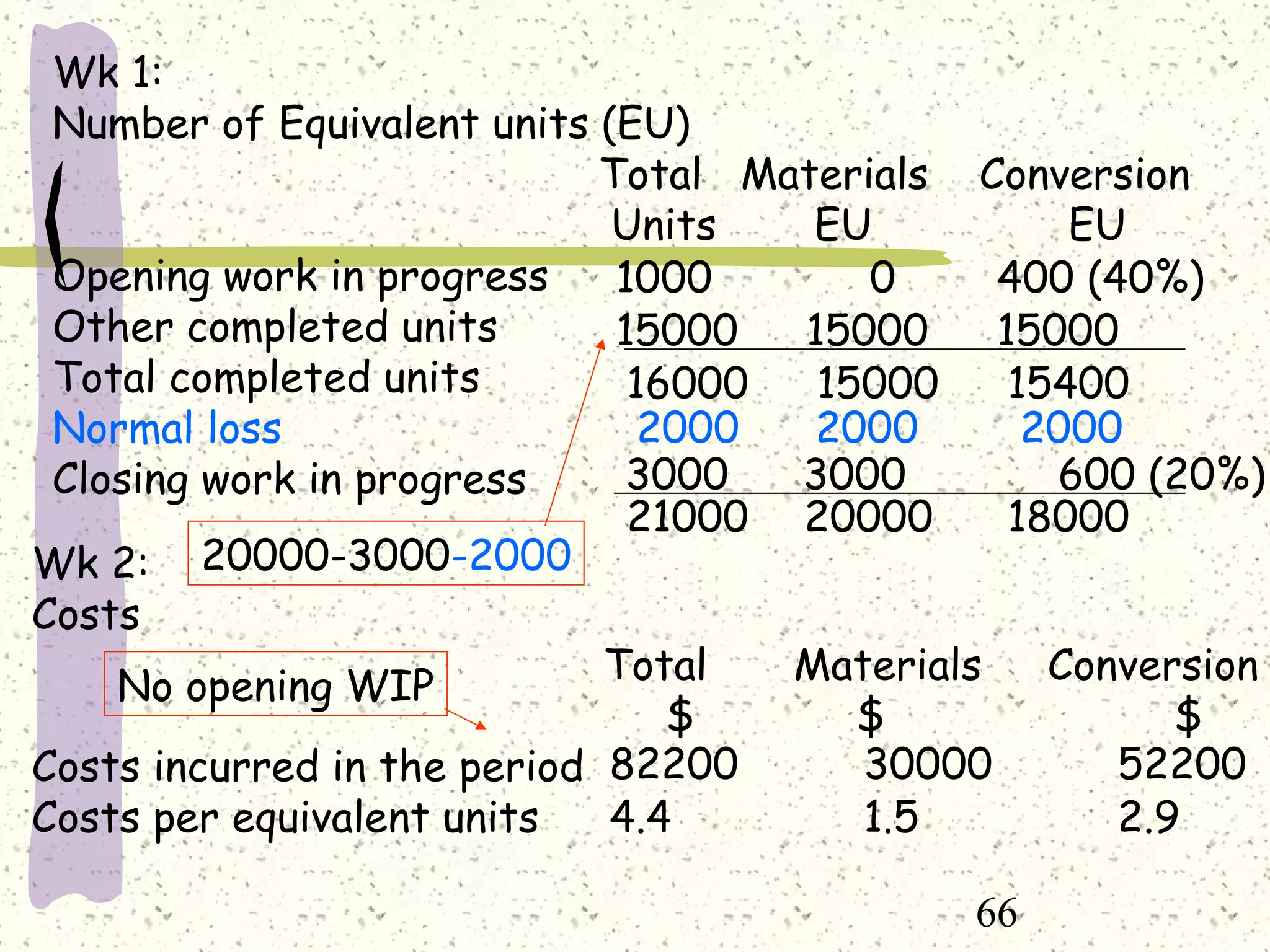

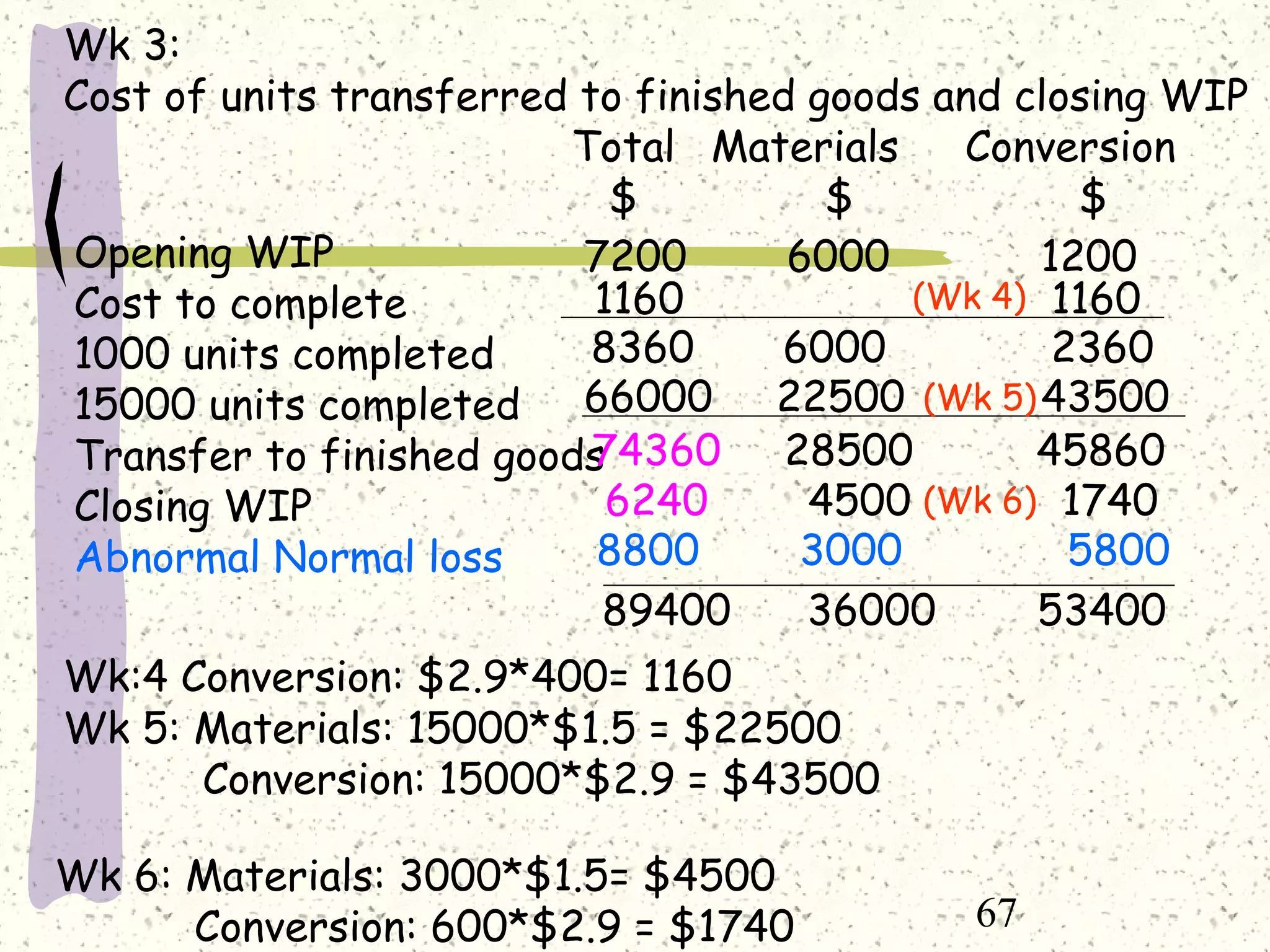

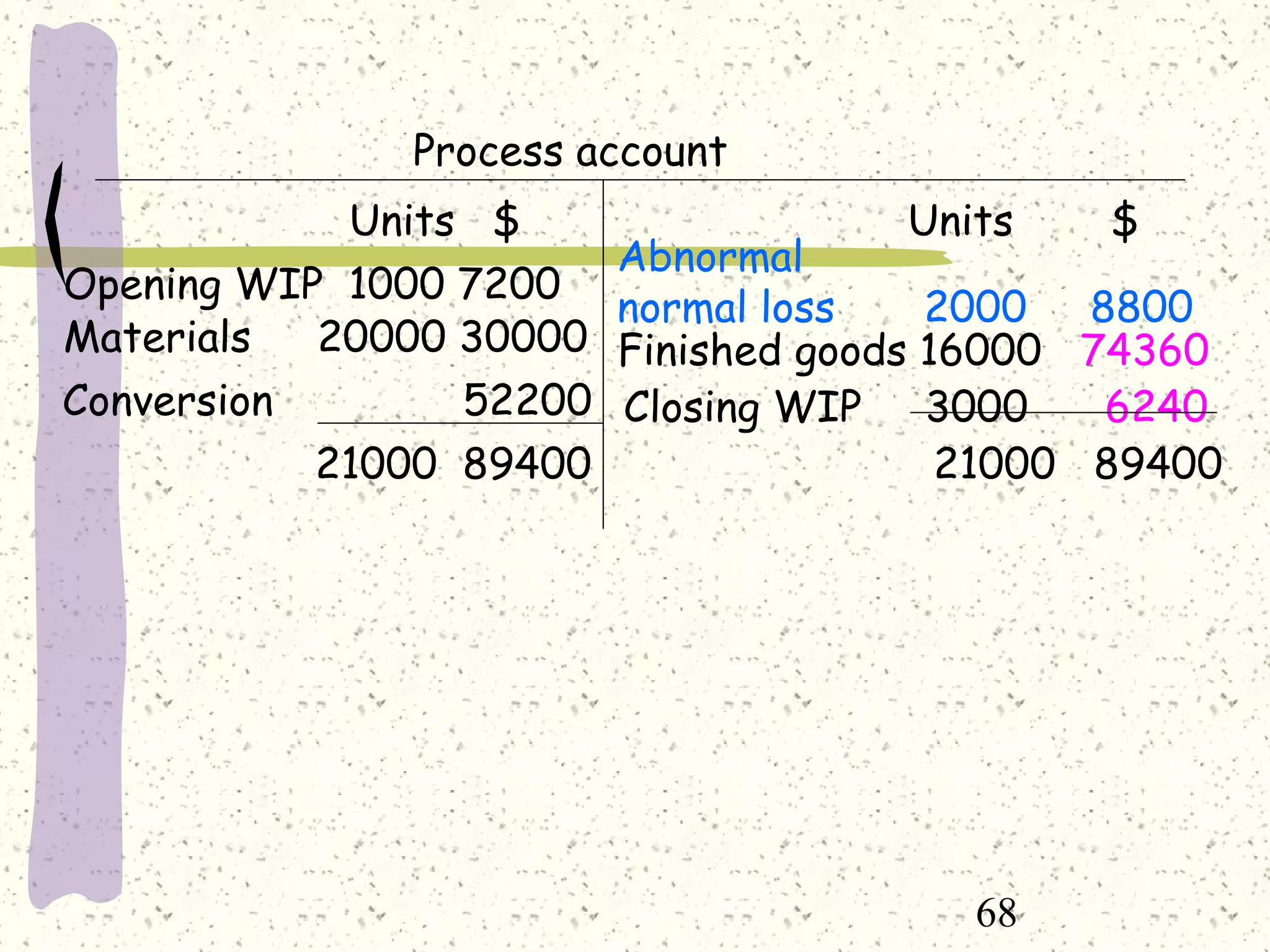

Here are the steps to prepare the Process 1 account using FIFO method considering the losses: 1. Calculate equivalent units (EUP) - Opening WIP: 1000 units (60% complete) = 600 EUP - Production: 20000 units - Closing WIP: 3000 units (20% complete) = 600 EUP - Total EUP = 21000 units 2. Calculate costs: - Opening WIP costs: Materials $6000, Conversion $1200 = $7200 - Current period costs: Materials $30000, Conversion $52200 = $82200 - Total costs = $82200 + $7200 = $89400 3. Calculate cost per EUP: